|

市場調査レポート

商品コード

1685209

タッキファイヤー市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Tackifier Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| タッキファイヤー市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年01月03日

発行: Global Market Insights Inc.

ページ情報: 英文 235 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

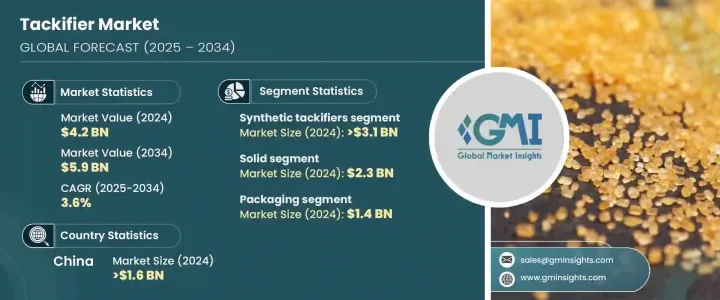

タッキファイヤーの世界市場は2024年に42億米ドルに達し、2025年から2034年にかけてCAGR 3.6%で拡大すると予測され、着実な成長が見込まれています。

タッキファイヤー(粘着付与剤)は、粘着性を高め、さまざまな産業で接着性を向上させることにより、接着剤配合において重要な役割を果たしています。特にパッケージング、自動車、建築、衛生分野での高性能接着剤の需要拡大に伴い、先進タッキファイヤーソリューションのニーズが高まっています。同市場では、特に不織布衛生用品とフレキシブル包装においてホットメルト接着剤(HMA)の需要が急増しており、業界の拡大をさらに後押ししています。

市場成長の主な促進要因としては、接着剤技術の継続的な進歩や、環境に優しいソリューションへのシフトの高まりが挙げられます。産業界がますます持続可能性を優先するようになるにつれ、バイオベースのタッキファイヤーへの移行が加速しています。再生可能な資源に由来するこれらの代替品は、揮発性有機化合物(VOC)の排出量が少なく、厳しい環境規制の遵守を目指す企業にとって好ましい選択肢となっています。さらに、eコマースの急速な拡大や、効率的な包装用接着剤へのニーズの高まりが、世界中で需要を促進しています。自動車組立や医療用途など、接着剤の性能が重要な産業では、タッキファイヤーが優れた接着能力を発揮し、現代の製造業に不可欠な役割を強化しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 42億米ドル |

| 予測金額 | 59億米ドル |

| CAGR | 3.6% |

2024年に31億米ドルと評価された合成タッキファイヤー分野が市場を独占し、予測期間のCAGRは3.5%と予測されます。脂肪族炭化水素、C9芳香族、合成ポリテルペンなどの石油ベースの原料から得られる合成タッキファイヤーは、優れた熱安定性、強力な粘着特性、さまざまなタッキファイヤーとの相溶性で広く支持されています。包装、建築、自動車などの業界では、過酷な条件下での耐久性と効率性から、これらのタッキファイヤーに大きな信頼を寄せています。高温や多様な環境条件下でも粘着力を維持できることから、長持ちする粘着ソリューションを求めるメーカーにとって最良の選択肢となっています。

固形タッキファイヤーセグメントは2024年に23億米ドルを生み出し、2034年までCAGR 3.4%で成長すると予想されています。固形タッキファイヤーは、費用対効果が高く、取り扱いが容易で、感圧接着剤やホットメルト接着剤の用途で優れた性能を発揮するため、高い人気があります。強力なポリマー適合性と熱安定性により、耐久性と柔軟性のある接着ソリューションを必要とする産業に最適です。工業包装や建築から衛生用品や自動車用途に至るまで、固形タッキファイヤーは進化するタッキファイヤー業界において基本的な要素であり続けています。

中国のタッキファイヤー市場は2024年に16億米ドルと評価され、2034年までCAGR 3.4%で拡大すると予想されています。世界の製造大国である中国は、その強力な産業基盤と様々な用途における接着剤需要の高まりにより、市場を独占しています。包装、建設、自動車産業の急成長により、タッキファイヤーのニーズが大幅に高まっています。さらに、中国のeコマースセクターの活況が高品質の包装用接着剤需要を牽引し、世界市場における中国のリーダーシップをさらに強固なものにしています。継続的な工業化とインフラ開発により、中国はタッキファイヤー業界の将来を形作る重要なプレーヤーであり続けています。

目次

第1章 調査手法と調査範囲

- 市場範囲と定義

- 基本推定と計算

- 予測計算

- データソース

- 1次データ

- 二次資料

- 有料情報源

- 公的情報源

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- 破壊

- 将来の展望

- メーカー

- 流通業者

- サプライヤーの状況

- 利益率分析

- 主要ニュースと取り組み

- 規制状況

- 影響要因

- 促進要因

- 各業界における接着剤需要の増加

- 環境に優しいタッキファイヤーの需要増加

- アジア太平洋地域の産業の成長

- 業界の潜在的リスク&課題

- 合成タッキファイヤーを制限する環境規制

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:製品タイプ別、2021年~2034年

- 主要動向

- 合成タッキファイヤー

- 天然タッキファイヤー

第6章 市場推計・予測:形態別、2021年~2034年

- 主要動向

- 固体

- 液体

- 樹脂分散体

第7章 用途別市場推計・予測:用途別、2021年~2034年

- 主要動向

- 包装

- 建築

- 不織布

- 製本

- 自動車

- その他

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第9章 企業プロファイル

- Arkema

- BASF SE

- Eastman Chemical

- Exxon Mobil

- H.B. Fuller

- Henkel AG &Co. KGaA

- Kolon Industries

- KRATON

- SI Group

- ZEON

The Global Tackifier Market reached USD 4.2 billion in 2024 and is poised for steady growth, projected to expand at a CAGR of 3.6% between 2025 and 2034. Tackifiers play a crucial role in adhesive formulations by enhancing their stickiness and improving adhesion across various industries. With the growing demand for high-performance adhesives, particularly in the packaging, automotive, construction, and hygiene sectors, the need for advanced tackifier solutions is on the rise. The market is witnessing a surge in demand for hot-melt adhesives (HMAs), particularly in nonwoven hygiene products and flexible packaging, further propelling industry expansion.

Key drivers of market growth include continuous advancements in adhesive technologies and a rising shift toward environmentally friendly solutions. As industries increasingly prioritize sustainability, the transition to bio-based tackifiers is accelerating. These alternatives, derived from renewable sources, offer lower volatile organic compound (VOC) emissions, making them a preferred choice for companies aiming to comply with stringent environmental regulations. Additionally, the rapid expansion of e-commerce and the growing need for efficient packaging adhesives are fueling demand across the globe. In industries where adhesive performance is critical, such as automotive assembly and medical applications, tackifiers provide superior bonding capabilities, reinforcing their indispensable role in modern manufacturing.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $4.2 Billion |

| Forecast Value | $5.9 Billion |

| CAGR | 3.6% |

The synthetic tackifiers segment, valued at USD 3.1 billion in 2024, dominates the market and is projected to grow at a CAGR of 3.5% over the forecast period. Derived from petroleum-based sources such as aliphatic hydrocarbons, C9 aromatics, and synthetic polyterpenes, synthetic tackifiers are widely favored for their outstanding thermal stability, strong adhesion properties, and compatibility with various adhesives. Industries such as packaging, construction, and automotive heavily rely on these tackifiers for their durability and efficiency in extreme conditions. Their ability to maintain adhesion under high temperatures and diverse environmental conditions makes them a top choice for manufacturers seeking long-lasting adhesive solutions.

The solid tackifier segment generated USD 2.3 billion in 2024 and is expected to grow at a 3.4% CAGR through 2034. Solid tackifiers are highly sought after due to their cost-effectiveness, ease of handling, and exceptional performance in pressure-sensitive and hot-melt adhesive applications. Their strong polymer compatibility and thermal stability make them ideal for industries that require durable and flexible bonding solutions. From industrial packaging and construction to hygiene products and automotive applications, solid tackifiers continue to be a fundamental component in the evolving adhesive landscape.

China tackifier market was valued at USD 1.6 billion in 2024 and is anticipated to expand at a CAGR of 3.4% through 2034. As a global manufacturing powerhouse, China dominates the market due to its strong industrial base and rising demand for adhesives across various applications. The rapid growth of the packaging, construction, and automotive industries has significantly increased the need for tackifiers. Additionally, China's booming e-commerce sector is driving demand for high-quality packaging adhesives, further solidifying the country's leadership in the global market. With continued industrialization and infrastructure development, China remains a key player in shaping the future of the tackifier industry.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Increased adhesive demand across industries

- 3.6.1.2 Rise in eco-friendly tackifier demand

- 3.6.1.3 Growth in Asia-Pacific’s industries

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 Environmental regulations limiting synthetic tackifiers

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Product Type, 2021-2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Synthetic tackifiers

- 5.3 Natural tackifiers

Chapter 6 Market Estimates & Forecast, By Form, 2021-2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Solid

- 6.3 Liquid

- 6.4 Resin dispersions

Chapter 7 Market Estimates & Forecast, By Application, 2021-2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Packaging

- 7.3 Construction

- 7.4 Non-woven

- 7.5 Bookbinding

- 7.6 Automotive

- 7.7 Others

Chapter 8 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Russia

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.6 MEA

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Arkema

- 9.2 BASF SE

- 9.3 Eastman Chemical

- 9.4 Exxon Mobil

- 9.5 H.B. Fuller

- 9.6 Henkel AG & Co. KGaA

- 9.7 Kolon Industries

- 9.8 KRATON

- 9.9 SI Group

- 9.10 ZEON