|

市場調査レポート

商品コード

1851504

ビール包装:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Beer Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ビール包装:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年07月13日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

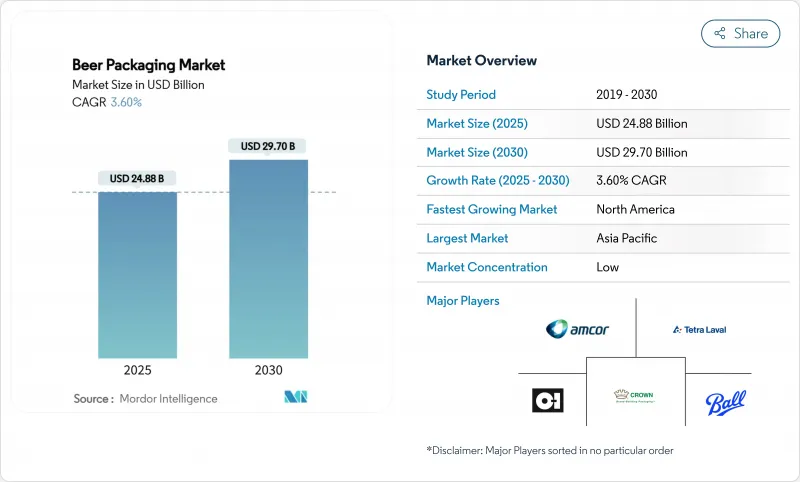

ビール包装の市場規模は2025年に248億8,000万米ドル、2030年には297億米ドルに達すると予測され、予測期間中のCAGRは3.60%で推移する見込みです。

この成長は、持続可能な素材に対する需要の高まり、プレミアムフォーマットの加速、消費チャネルの継続的なシフトを反映しています。アルミニウムのシェアは、リサイクル性とロジスティクスの効率性が大手・中小のビールメーカーを問わず惹きつけていることから拡大を続けており、PETはコールドチェーンの品質保証が改善されつつあることから支持を集めています。ガラスは数量では明らかにリードしているが、エネルギー集約的な生産とより重い貨物輸送によるコスト圧力に直面しています。地域的なビジネスチャンスは、都市化がパッケージ・ビールの売上を押し上げるアジア太平洋と、クラフトビールメーカーが小売店の棚動態にマッチした、差別化された環境に優しいフォーマットを求める北米に集中しています。大手缶メーカー、ガラスメーカー、フレキシブルパックのスペシャリストによる供給サイドの投資は、材料投入量を削減し、ブランドの俊敏性を高める、高速で廃棄物の少ないテクノロジーへの業界の軸足を示すものです。

世界のビール包装市場の動向と洞察

クラフトビール醸造所の急増が北米の短納期缶デザインを牽引

Ball社のDynamark Advanced Proのようなデジタル印刷では、1パレットに複数のグラフィックを印刷できるため、従来の最低注文数の壁がなくなり、クラフトビール醸造所の成長がパッケージングの経済性を再構築しています。フレキシブルな缶ラインは、醸造業者が過剰なガラス瓶を購入することなく、在庫を管理し、新しいSKUを試験的に製造し、季節ごとに発売するのに役立ちます。デジタル印刷のプレミアムはオフセット印刷より300%近く高いが、地域全体で9,000を超えるビール醸造所で、より迅速なセルスルー率とより強力な棚アピールがコストを相殺します。

EUのデポジット・リターン制度に支えられた軽量リターナブルガラスびんの採用増加

ドイツではデポジット制度が義務化され、返送率は98%に達し、Vetropack社のEchovai強化ボトルのようなイノベーションを促しています。フランスでは、年間6,000万本のボトルを洗浄できる集中洗浄ハブを追加し、コスト構造を一方的な廃棄から循環型資産管理へとシフトさせています。

欧州でPETを削減する使い捨てプラスチック禁止法

EUの包装・容器包装廃棄物規制は、2030年までにリサイクル率30%を強制し、2025年から対象フォーマットを段階的に廃止します。拡大生産者責任料金は、無限にリサイクル可能なアルミニウムと比較してPETのコストを引き上げ、金属や軽量リターナブルガラスへのポートフォリオのシフトを促しています。

セグメント分析

ガラスは、感覚的中立性と消費者の定着した連想により、2024年には80.98%のシェアを維持します。しかし、2030年までに100%リサイクル可能な包装を目指すという政策目標に後押しされ、アルミのリサイクル性の優位性と輸送の節約により、数量は減少します。PETはCAGR5.81%の伸びを示し、今やビールの炭酸ニーズを満たすバリアコーティングボトルに引き寄せられるが、紙は依然として二次パックに限られています。

エネルギーコストの上昇と炭素税の賦課により、アルミのトータルコストでの優位性は炉焚きガラスよりも拡大します。一方、使用済み食用油を原料とするバイオパラキシレンPETのような技術革新は、ブランドの信頼性を向上させ、ポリマーの幅広い採用を予感させる。ビールメーカーは、高級品向けのニッチなガラスSKUを維持しているが、ビール包装市場では、新しい生産能力をより軽量な基材に向ける傾向が強まっています。

2024年の世界販売量の75.32%はボトルが占める。それでも缶は、クラフトビール、コンビニエンス・ショッピング、屋外消費におけるダイナミズムがフォーマットを金属製に傾けるため、CAGR 6.75%で加速しています。樽生は、新興地域における洗浄システムの設備投資によって成長が鈍化し、パウチもわずかな伸びにとどまる。

デジタル印刷により、小規模ビールメーカーは多国籍企業のパッケージング品質と肩を並べることができ、無駄なオーバーランをすることなくSKUの回転率を上げることができます。ブラジルに見られるような地域缶ラインへの投資は、単位当たりのコストを削減し、供給力を高める経済性をさらに拡大します。ガラスメーカーは、エンボス加工やテーパー加工を施したプロファイルで対抗し、店頭での認知価値を高めています。

地域分析

2024年のシェアは38.43%でアジア太平洋がリードし、人口規模、所得の上昇、急速な都市化に支えられ、パッケージ化された業態が好まれます。ベトナムとインドネシアではコールドチェーンの拡大がPETの浸透を支え、中国では工芸品分野が2024年に331億人民元まで成長し、ブティックデザインの缶やギフト志向のガラス瓶が育っています。

2030年までのCAGRが最も速いのは北米で6.43%です。9,000を超えるクラフトビール醸造所が小ロット缶の安定した需要を生み出しているが、関税とスラブ不足がコストを押し上げています。ボールのフロリダ買収のような投資は、供給網を合理化し、持続可能な生産能力を追加し、この地域の成長エンジンとしてのアルミの役割を強化します。

欧州は依然としてプレミアムの牙城であるが、一人当たりのビール摂取量の横ばいに直面しています。EUのリサイクル義務化は、強化ガラス、リターナブルガラス、高リサイクルコンテント缶への資本シフトの引き金となります。ドイツのビール会社は、サーキュラー・エコノミーのKPIを満たしながら工業的な速度を達成するエンボスラインを導入することで、プレミアムパッケージングを披露しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- クラフトビール醸造所の急増が北米の短納期缶デザインを牽引

- EUのデポジット・リターン制度に支えられた軽量リターナブルガラスびんの採用増加

- コールドチェーンの急速な拡大がアジアのビールへのPET浸透を可能にする

- ブランド・プレミアム化がドイツのビール会社のエンボス加工特殊ボトルを後押し

- アルミ関税引き下げが南米での缶転換を誘発

- eコマース・マルチパックが英国の段ボール二次包装需要を加速する

- 市場抑制要因

- 欧州におけるPETを抑制する使い捨てプラスチック禁止法

- 米国のアルミスラブ供給の逼迫がクラフトビールメーカーの缶コストを上昇させる

- 消費者の硬質炭酸飲料へのシフトがオーストラリアのガラス販売量を減少させる

- 新興市場におけるリターナビリティを制限する樽の改修にかかる高いキャップエックス

- サプライチェーン分析

- 規制の見通し

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力/消費者

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- 包装材料別

- ガラス

- 金属

- PET

- 紙

- パッケージングタイプ別

- ボトル

- 缶

- ケグ

- ポーチ

- パックサイズ別

- 330ml未満

- 331-650 ml

- 650ml以上

- 流通チャネル別

- 直接販売

- 間接販売

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- ロシア

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア、ニュージーランド

- その他アジア太平洋地域

- 中東・アフリカ

- 中東

- アラブ首長国連邦

- サウジアラビア

- トルコ

- その他中東

- アフリカ

- 南アフリカ

- ナイジェリア

- エジプト

- その他アフリカ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Amcor Ltd.

- Ardagh Group SA

- Crown Holdings Inc.

- Ball Corporation

- Tetra Laval International SA

- O-I Glass Inc.

- Canpack Group

- Silgan Holdings Inc.

- Vidrala SA

- Allied Glass Containers Ltd.

- Plastipak Holdings Inc.

- Nampak Ltd.

- Orora Limited

- Graphic Packaging International

- Toyo Seikan Group Holdings Ltd.

- Envases Universales

- Berlin Packaging LLC

- Sidel(Sidel Group)

- Krones AG