クラウドID・アクセス管理ソフトウェア:市場シェア分析、業界動向、成長予測(2025~2030年)

Cloud Identity and Access Management Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1627127

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

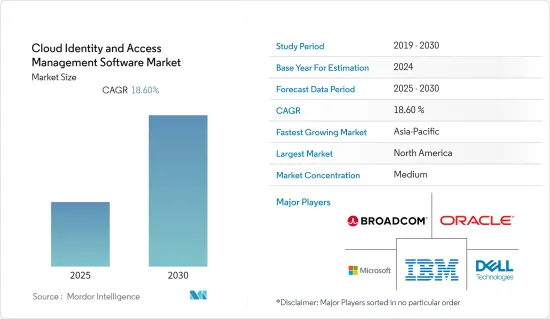

クラウドID・アクセス管理ソフトウェア市場は予測期間中にCAGR 18.6%を記録する見込み

主要ハイライト

- コスト削減と規模の経済性により、クラウド技術はビジネスの運営方法に革命をもたらしています。しかし、適切なセキュリティ対策の欠如は、クラウドコンピューティングのメリットを損なう可能性があります。このため、ID関連の犯罪に対するセキュリティを含むセキュリティソリューションの根本的な必要性が叫ばれ、クラウドID・アクセス管理市場の原動力となっています。

- パブリッククラウドは、市場で最も普及しているクラウド展開のタイプです。これは、さまざまな産業で利用が拡大しているためです。しかし、ハイブリッドクラウドの導入は、中小企業での採用が拡大しているため、予測期間中に最も高いCAGRで推移すると予想されます。

- 携帯電話やタブレットが普及するにつれ、従業員は自分の携帯電話やノートパソコンをビジネスネットワークに接続できるようになりました。古いオフィスのデスクトップを使用する代わりに、従業員は企業で自分のデバイスを使用することを好み、これがクラウドIDとアクセス管理ソフトウェアの必要性を高め、したがって市場の研究を促進します。

COVID-19の影響期間中、クラウドID・アクセス管理(IAM)ソフトウェアは市場にプラスの影響を与え、予測期間中の成長に大きく貢献すると予想されました。IAMベンダーは企業を支援するために名乗りを上げました。例えば、IBMはパンデミックの際に、IBM Security MAss360 with WatsonやIBM Cloud Identityなどの重要な技術を新規顧客向けに90日間無償で提供すると発表しました。

クラウドID・アクセス管理ソフトウェア市場動向

シングルサインオン(SSO)と統合プロビジョニングが最も高い成長を遂げる見込み

- シングルサインオン(SSO)は、IDアクセス管理における最新のイノベーションです。このソリューションはコンパクトで柔軟性が高いため、IT企業から製造業まで幅広いエンドユーザーを魅了しています。

- フェデレーテッド・プロビジョニングの場合、このソリューションは、フェデレーテッド・アイデンティとプロビジョニングと呼ばれる2つの別々のシステムをミックスしたものです。フェデレーテッド IDとは、異なる施策・ドメインがID管理の責任を共有することを可能にする標準を指します。一方、プロビジョニングは、ユーザーまたはシステムのアクセス権限を管理するために必要なライフサイクル内のすべてのステップの自動化です。

- クラウドのアプリケーションやデータを活用しながら、ユーザーアカウントを社内で管理できることは、連携プロビジョニングソリューションが提供する大きな利点であり、市場におけるこれらのソリューションの大きな成長を後押ししています。

- さらに、ソーシャル・エンジニアリング攻撃やID盗難の増加が、特に北米と欧州の先進諸国において、シングルサインオンと統合プロビジョニングの両方の成長を促進しています。

- Identity Theft Resource Centerは、米国では2022年に1,802回データが盗まれたとみています。同じ年に、データ漏洩、データ流出、データ暴露などのデータ侵入も4億2,200万人以上に影響を与えました。これらは3つの異なる事象であるにもかかわらず、いずれも同様の特徴を有しています。これら3つの事例はすべて、無許可の脅威者が機密データにアクセスした結果です。

北米が最大の市場シェアを占める

- 世界のクラウド先進企業の大半は北米地域の企業であり、クラウドをソリューション展開の最も好ましい形態とする新興企業の数も多いです。

- クラウドベースのソフトウェアサービスが最も多く採用されていることに加え、ITUの報告によると、北米地域はサイバーセキュリティに非常に積極的で、力を入れています。

- さらに、CAPEXの削減やアップデートの迅速な展開といったメリットも、北米地域でクラウドベースのID管理ソリューションが採用されている主要理由の1つです。

- 同地域におけるクラウドベースのIAMの主要採用はBFSIセクターに見られ、今後も増加する可能性があります。米国消費者センチネルネットワークが報告したように、クレジットカード詐欺や侵害がID窃盗の総数の大きな割合を占めているからです。

- 同地域はサイバー攻撃の影響を強く受けており、サイバーセキュリティのインシデントが世界で最も多い地域のひとつです。そのため、この地域も対策を実施し、サイバーセキュリティ、技術、その導入に関して最も進んだ地域のひとつとなっています。したがって、サイバーセキュリティに対するニーズの高まりも、同地域のクラウドID・アクセス管理ソフトウェア市場の原動力となると考えられます。

クラウドID・アクセス管理ソフトウェア産業概要

クラウドID・アクセス管理市場には、複数の世界企業や地域企業が参入しており、市場競争は緩やかです。しかし、市場はさまざまな小規模参入企業の統合へと移行しつつあります。いくつかの市場競争参入企業は、イノベーションを通じて市場におけるサステイナブル競争優位性を獲得しています。同市場の主要企業には、IBM Corporation、Microsoft Corporation、Oracle Corporationなどがあります。

CloudIBNは、2022年12月にID・アクセス管理サービスの採用を発表しました。このIAMソリューション・スイートの支援により、企業は組織全体のユーザーアクセス制御を効果的に管理し、データを安全に保つことができます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- セキュリティ侵害件数と関連コストの増加

- 企業におけるBYOD利用動向の増加

- 市場抑制要因

- クラウドベースのアプリケーションのサイバーリスクに対する脆弱性

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 技術スナップショット

- COVID-19の市場への影響評価

第5章 市場セグメンテーション

- 組織規模別

- 中小企業

- 大規模組織

- ソリューションタイプ別

- 監査、コンプライアンス、ガバナンス

- シングルサインオン(SSO)と統合プロビジョニング

- 特権アクセス管理

- ディレクトリサービス

- その他

- 導入タイプ別

- パブリック

- プライベート

- ハイブリッド

- 産業別

- IT・通信

- BFSI

- 医療

- エンターテイメント・メディア

- 小売

- 教育

- その他産業別

- 地域別

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

第6章 競合情勢

- 企業プロファイル

- Cyberark Software Ltd.

- Broadcom Inc.(CA Technologies)

- IBM Corporation

- Microsoft Corporation

- Oracle Corporation

- Okta Inc.

- Centrify Corporation

- Sailpoint Technologies Holdings Inc.

- Auth0 Inc.

- Dell Technologies Inc.

第7章 投資分析

第8章 市場機会と今後の動向

目次

The Cloud Identity and Access Management Software Market is expected to register a CAGR of 18.6% during the forecast period.

Key Highlights

- Due to cost savings and economies of scale, cloud technology is revolutionizing how businesses operate. However, the lack of proper security measures can undermine the benefits of cloud computing. This calls for a fundamental need for security solutions, including security for identity-related crimes, and hence drives the market for cloud identity and access management.

- The public cloud is the most popular type of cloud deployment on the market. This is because it is being used more and more in many different industries. However, hybrid cloud deployment is expected to register the highest CAGR over the forecast period because of growing adoption among small and medium-sized enterprises.

- As mobile phones and tablets become more popular, employees can connect their phones and laptops to the business network. Instead of using their old office desktops, employees like to use their own devices in enterprises, which increases the need for cloud identity and access management software and hence drives the market studied.

During the COVID-19 impact period, cloud identity and access management (IAM) software was expected to have a positive impact on the market and contribute significantly to its growth over the forecast period. IAM vendors came forward to assist the enterprises. For instance, during the pandemic, IBM announced that it would make critical technologies such as IBM Security MAss360 with Watson and IBM Cloud Identity available at no charge for new clients for 90 days.

Cloud Identity and Access Management Software Market Trends

Single Sign-on (SSO) and Federated Provisioning is Expected to Witness the Highest Growth

- Single sign-on (SSO) is the most recent innovation in identity access management. The compact and highly flexible nature of this solution is attracting a wide range of end-users, ranging from IT companies to the manufacturing sector.

- In the case of federated provisioning, the solution is a mix of two separate systems called federated identity and provisioning. Federated identity refers to the standards that allow different policy domains to share identity management responsibilities. Provisioning, on the other hand, is the automation of all the steps in the lifecycle that are needed to manage user or system access entitlements.

- The capability of retaining in-house control of user accounts while leveraging cloud applications and data is the significant advantage that federated provisioning solutions offer and is driving the immense growth of these solutions in the market.

- Furthermore, the increasing number of social engineering attacks and identity thefts is driving the growth of both single sign-on and federated provisioning, especially in the developed countries of North America and Europe.

- The Identity Theft Resource Center thinks that in the United States in 2022, there were 1802 times when data was stolen. In the same year, data intrusions such as data breaches, data leaks, and data exposure also had an impact on over 422 million people. Even though these are three distinct events, they all share a similar trait. All three instances result in an unauthorized threat actor accessing the sensitive data.

North America Occupies the Largest Market Share

- Most of the cloud-advanced organizations in the world are from the North American region, along with a high number of startups whose most preferred mode of solution deployment is in the cloud.

- Along with the highest adoption of cloud-based software services, it is also reported by the ITU that the North American region is very proactive and committed to cybersecurity.

- Moreover, benefits like reduced CAPEX and faster rollouts of updates are some of the major reasons for the adoption of cloud-based identity management solutions in the North American region.

- Major adoption of cloud-based IAM in the region is seen in the BFSI sector, and it may continue to rise, as credit card frauds and breaches accounted for a major share of the total number of identity thefts, as reported by the US consumer sentinel network.

- The region is highly affected by cyberattacks and has one of the highest cybersecurity incidents in the world. Therefore, the region has also implemented its countermeasures and has become one of the most advanced regions with respect to cybersecurity, technology, and its adoption. Therefore, rising cybersecurity needs will also drive the cloud identity and access management software market in the region.

Cloud Identity and Access Management Software Industry Overview

The cloud identity and access management market comprises several global and regional players and is a moderately contested market space. However, the market is shifting toward the consolidation of various smaller players. Several market players are gaining a sustainable competitive advantage in the market through innovations. Some of the major players in the market are IBM Corporation, Microsoft Corporation, and Oracle Corporation, among others.

CloudIBN announced the introduction of Identity and Access Management services in December 2022. With the help of this IAM solution suite, businesses can effectively manage user access control across their whole organization and keep their data safe.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Number of Security Breaches and Related Costs

- 4.2.2 Increasing Trend of Using BYODs in Enterprises

- 4.3 Market Restraints

- 4.3.1 Vulnerability of Cloud-based Applications to Cyber Risks

- 4.4 Industry Attractiveness - Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

- 4.5 Technology Snapshot

- 4.6 Assessment of Impact of COVID-19 on the Market

5 MARKET SEGMENTATION

- 5.1 By Size of Organization

- 5.1.1 SMEs

- 5.1.2 Large Organization

- 5.2 By Type of Solution

- 5.2.1 Audit, Compliance, and Governance

- 5.2.2 Single Sign-on (SSO) and Federated Provisioning

- 5.2.3 Privileged Access Management

- 5.2.4 Directory Service

- 5.2.5 Other Types of Solutions

- 5.3 By Deployment Type

- 5.3.1 Public

- 5.3.2 Private

- 5.3.3 Hybrid

- 5.4 By End-User Vertical

- 5.4.1 IT and Telecommunication

- 5.4.2 BFSI

- 5.4.3 Healthcare

- 5.4.4 Entertainment and Media

- 5.4.5 Retail

- 5.4.6 Education

- 5.4.7 Other End-User Verticals

- 5.5 Geography

- 5.5.1 North America

- 5.5.2 Europe

- 5.5.3 Asia-Pacific

- 5.5.4 Latin America

- 5.5.5 Middle East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Cyberark Software Ltd.

- 6.1.2 Broadcom Inc. (CA Technologies)

- 6.1.3 IBM Corporation

- 6.1.4 Microsoft Corporation

- 6.1.5 Oracle Corporation

- 6.1.6 Okta Inc.

- 6.1.7 Centrify Corporation

- 6.1.8 Sailpoint Technologies Holdings Inc.

- 6.1.9 Auth0 Inc.

- 6.1.10 Dell Technologies Inc.

7 INVESTMENT ANALYSIS

8 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日