マネージドデータセンターサービス:市場シェア分析、産業動向、成長予測(2025~2030年)

Managed Data Center Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1626887

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

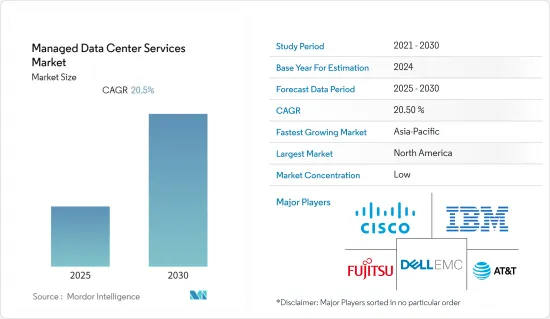

マネージドデータセンターサービス市場は予測期間中にCAGR 20.5%を記録する見込み

主なハイライト

- マネージドデータセンターサービスにより、企業は物理的インフラから脱却でき、間接コストの削減が可能になります。データセンターを所有するコストは相当なものであり、市場にはリンクされたデバイスが数多く出回っています。また、メタバースコンセプトは業界拡大を促進する主要な要素として普及し始めたばかりです。また、データセンターサービスは、企業がハードウェアを増設することなく、安価にIT業務を拡張できることから、今後さらに普及が進むと予想されます。

- サイバー脅威の高まりとデータ漏洩の可能性により、市場は拡大しています。データ保護のためのマネージドサービスで最も人気のあるもの1つがレプリケーションです。データ保護のためのマネージドサービスで最も人気のあるもの1つがレプリケーションです。サイバーハードニングは攻撃面を減らし、マルウェアが一様に拡散するのを防ぎます。データセンターのセキュリティチームは、ソフトウェアバイナリをハードニングすることで、あらゆる種類の脅威を排除します。

- 事業継続性と可用性は、データセンターサービスの2大課題です。データセンターで使用されるアプリケーションは、プロバイダーやWANが停止するとアクセスできなくなる可能性があります。予期せぬダウンタイムは、たとえサービスレベル契約がデータセンターサービスの可用性をカバーしていたとしても、重大な結果をもたらすことが予想されます。さらに、データセンターサービスはクラウドコンピューティングの一部であるため、オンライン上のさまざまな危険の影響を受けやすいです。データの安全性と可用性が業界の拡大を妨げることが予想されます。

- COVID-19の発生は、多くの産業における多くの業務の停止と、複数のデータセンターの建設を引き起こしました。社会通念上、社会的距離や企業の在宅勤務文化が好まれるため、DCaaS業界への影響はほとんどなかった。データ量の増加により、パンデミックの流行により多くの企業がITインフラ全体をクラウドに移行せざるを得なくなった。多くの企業がサービスとしてのデータセンターを選択するのは、オンプレミスのデータセンターよりもはるかに大容量でデータ処理能力が高いからと思われます。

- ラックスペース・テクノロジーとグーグル・クラウドが前年、1,400人以上のIT幹部を対象に行った世論調査によると、51%が現在インフラをクラウド化しており、49%がオンプレミスのインフラからクラウドにワークロードを移行する計画があると回答しています。さらに、流行がソーシャルメディアやその他のデジタルツールの利用を促し、世界のデータ量を増加させました。サービスとしてのデータセンターの人気は、クラウドコンピューティングへのシフトの高まりによってさらに加速すると予測されています。COVID-19の流行は市場にとって好都合だったわけです。パンデミックの間、市場は成長し、これは予測期間の残りの期間も続くと予想されます。

マネージドデータセンターサービス市場の動向

小売業界が市場を独占

- 現代社会では、データセンターはデジタルサービスやオンライン顧客体験を提供するため、小売業にとって不可欠な要素となっています。オンラインであれ実店舗であれ、消費者がブランドと接する際には、高度にカスタマイズされた適切な体験が求められるようになっています。特定の顧客のニーズに合わせてキャンペーンや体験をカスタマイズするには、多くのデータや情報が必要となります。

- eコマースやオンライン小売は、基本的に従来の実店舗での買い物の延長線上にあります。eBayとアマゾンを筆頭に、数多くの企業がオンラインとデジタルのみで事業を展開しています。消費者が店頭での比較ショッピングにスマートフォンを頻繁に利用するようになった今、実店舗を持つ大手小売企業はオンライン体験を重視し、モバイル・ショッピング・アプリをさらに展開しています。

- ショッピング体験のパーソナライズとは、顧客の取引履歴を記録し、小売業者が推奨商品を提供できるようにすることです。買い物客の増加により、堅牢なデータセンターが必須となっています。

- 新しいテクノロジーを導入するための主要な集中分野は、小売業に出現しました。アマゾン・ゴーは、レジなしで商品を受け取り、店外に出ることができるコンセプト・ストアであり、アマゾンはオンライン小売業者から実店舗へと移行しました。商品のセンサーと買い物客のモバイルアプリが取引の追跡に使われています。より現代的で最先端のソリューションは、小売業における通常のデータセンター利用に加え、多くの企業が実験を始めたばかりです。マジックミラーAR技術に基づくような革新的なデジタルサイネージは、その代表例です。

アジア太平洋地域が最も高い成長を遂げる

- 莫大なデータ量を処理するためのデータセンターの拡大がその要因と考えられます。さらに、この地域ではデジタルサービスの利用が拡大しており、幅広い通信網が市場の拡大を支えていると予想されます。さらに、新興企業や中小企業の人口が拡大していることから、データセンターサービスの利用が加速すると予想されます。アジア太平洋地域では、デジタル製品やサービスによるデータ量が増加しています。これは、同地域の人口が増加し、eコマースが増加しているためです。

- アジア太平洋地域には2つの重要なデータセンターマーケットプレースがあります。香港やシンガポールのように現地の需要に応えるものと、東京、上海、オーストラリアのように国内の需要に応えるものです。インドネシアとインドは人口が急速に増加しており、より多くのデータセンタースペースを必要としているため、興味深いティア2市場です。

- シドニーのデータセンター市場もまだ拡大しています。オーストラリアは遠隔地であるにもかかわらず、高度にデジタル化された国民性から強い需要があります。世界で最もクラウドを利用しているのはオーストラリアです。オーストラリアには数多くの国際企業が進出しています。

- インドは世界で2番目に人口が多く、最も若い人口の1つです。彼らは膨大なデータの急増に対処しなければならないです。多くの人が複数の携帯電話を所有しています。インドには252MWのデータセンターしかありませんが、この数は劇的に増加するでしょう。インド、特にムンバイには大規模データセンター用のビルがたくさんあります。

- クラウド技術はアジア太平洋で徐々に勢いを増しています。そのため、スピードと敏捷性により、マネージドサービスの需要が高まっています。クラウドベースの展開に弾みがつくと思われます。

- 規制当局は、マネージドデータセンターサービスの成長を可能にする、あるいは阻害する上で重要な役割を果たしています。アジア太平洋地域の規制当局の中には、企業がコンプライアンスを達成できるようにアウトソーシングのルールやガイドラインを明確化しているところもあるが、規制上の制限やクラウド導入の阻害要因は依然として存在しています。

マネージドデータセンターサービス業界の概要

マネージドデータセンターサービスの市場は細分化されており、大手企業の大半がデータセンター管理や企業ネットワーク・サービスなどのサービスを提供し、事業継続を実現しています。同市場の大手企業には、富士通、シスコシステムズ、Dell EMC、IBM Corporationなどがあります。参入障壁がかなり低いため、新規参入企業も増えています。

2022年11月、富士通株式会社は、コネクテッドネスと予測不可能性が高まる中、テルアビブに研究開発センターを新設する計画を発表し、データとセキュリティのイノベーションを推進するための優秀な人材の採用を急ぐ。

2022年10月、米国を拠点とするテクノロジーサービスと電気通信機器の世界的プロバイダーであるシスコは、遠隔会議、ファイル共有、コールセンター業務のためのサービス群であるWebExの専用データセンターをインドに投資すると発表しました。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 市場の定義と範囲

- 調査の前提

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の利害関係者分析

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場力学

- 市場促進要因

- サイバー攻撃とデータ漏洩リスクの増加が市場拡大の要因

- 大量データ管理の必要性が市場を拡大

- 小売業界におけるデータセンターサービスの利用増加が市場を押し上げる

- 市場抑制要因

- 熟練した専任人材の不足が市場成長の妨げに

- COVID-19がデータセンターサービス市場に与える影響

第6章 主要技術投資

- クラウド技術

- 人工知能

- サイバーセキュリティ

- デジタルサービス

第7章 市場セグメンテーション

- タイプ別

- マネージド・ストレージ

- マネージド・ホスティング

- マネージド・コロケーション

- 展開タイプ別

- クラウド

- オンプレミス

- エンドユーザー業界別

- BFSI

- エネルギー

- 小売

- ヘルスケア

- 製造業

- その他エンドユーザー産業

- 地域別

- 北米

- 米国

- カナダ

- その他北米

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- アルゼンチン

- その他ラテンアメリカ

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- 南アフリカ

- その他中東とアフリカ

- 北米

第8章 競合情勢

- 企業プロファイル

- Fujitsu Ltd

- Cisco Systems Inc.

- Dell EMC

- IBM Corporation

- AT&T Inc.

- HP Development Company LP

- Microsoft Corporation

- Verizon Communications Inc.

- Dell Inc.

- Rackspace Inc.

- TCS Limited

- Deutsche Telekom AG

第9章 投資分析

第10章 市場機会と今後の動向

目次

The Managed Data Center Services Market is expected to register a CAGR of 20.5% during the forecast period.

Key Highlights

- Enterprises could move away from physical infrastructure owing to managed data center services, enabling overhead cost savings. The cost of owning a data center is considerable, there are many linked devices on the market, and the metaverse concept is just starting to take off as a major element driving industry expansion. It is also expected that data center services will become more popular because they offer businesses a cheap way to expand their IT operations without having to invest in more hardware.

- The market is expanding due to rising cyber threats and the possibility of data leakage. One of the most popular managed services for data protection is replication. One of the most popular managed services for data protection is replication. Cyber hardening reduces attack surfaces and prevents malware from spreading uniformly. Data center security teams eliminate a whole class of threats by hardening software binaries.

- Business continuity and availability are two of the main data center services issues. Applications used by data centers may become inaccessible if there is a provider or WAN outage. Unexpected downtimes are anticipated to have significant consequences, even though a service-level agreement covers the availability of data center services. Additionally, as data center services are a part of cloud computing, they are susceptible to various online dangers. It is expected that data security and availability would hinder industry expansion.

- The COVID-19 outbreak caused the halting of numerous operations in numerous industries and the construction of multiple data centers. Due to social conventions favoring social distance and corporate work-from-home cultures, this had little to no effect on the DCaaS industry. Due to increasing data volumes, numerous businesses were forced to move their entire IT infrastructure to the cloud due to the pandemic outbreak. Many businesses are likely to choose data centers as a service because they have far greater volume and data handling capacity than on-premises data centers.

- A poll of more than 1,400 IT executives in the previous year by Rackspace Technology and Google Cloud found that 51% of them said their infrastructure is currently in the cloud, and 49% said they have plans to move workloads from on-premises infrastructure to the cloud. Additionally, the epidemic raised worldwide data volumes by encouraging more people to use social media and other digital tools. The popularity of data centers as a service is projected to be fueled by the growing shift toward cloud computing. So, the COVID-19 outbreak was good for the market. During the pandemic, the market grew, and this is expected to continue for the rest of the forecasted period.

Managed Data Center Services Market Trends

Retail Industry to Dominate the Market

- In the modern world, data centers are essential elements of retail operations since they provide digital services and online customer experiences. When interacting with brands, whether online or in a physical store, consumers now demand a highly tailored and pertinent experience. A lot of data and information are needed to customize a campaign or experience to meet the needs of specific customers.

- E-commerce and online retail are essentially an extension of traditional and physical shopping. Numerous businesses only operate online and digitally, with eBay and Amazon being the two most prominent players. Now that consumers are utilizing smartphones more frequently for in-store comparison shopping, large brick-and-mortar retailers are placing a lot of emphasis on their online experiences and rolling out more mobile shopping apps.

- Personalizing the shopping experience means customers' transaction history is recorded so that the retailer can provide recommendations. Due to the increasing number of shoppers, robust data centers have become mandatory.

- A major area of concentration for implementing new technologies has emerged in retail. With its Amazon Go concept store, which lets customers take items and walk out without a cashier, Amazon has transitioned from an online retailer to a physical store. Sensors on the merchandise and the shopper's mobile app are used to track transactions. The more contemporary or cutting-edge solutions are in addition to some of the usual data center uses in retail that many companies are just beginning to experiment with. Innovative digital signage, like that based on Magic Mirror AR technology, is a prime example.

Asia-Pacific to Witness the Highest Growth

- The expansion of data centers to handle enormous data volumes can be attributed to it. Additionally, the region's growing use of digital services and wide telecom network are anticipated to support market expansion. In addition, the region's expanding startup and SME population is expected to accelerate the use of data center services. Asia-Pacific is seeing a rise in the amount of data made by digital products and services. This is because the region's population is growing and e-commerce is on the rise.

- There are two significant data center marketplaces in the Asia Pacific region: those that cater to local demand, like those in Hong Kong and Singapore, and those that cater to domestic demand, like those in Tokyo, Shanghai, and Australia. Indonesia and India are interesting Tier II markets because their populations are growing quickly and they need more data center space.

- The market for data centers in Sydney is also still expanding. Despite its remote location, Australia has a strong demand due to its highly digitalized populace. The world's highest cloud use is found in Australia. In Australia, there are numerous international corporations.

- India is home to the second-largest and one of the youngest populations in the world. They must deal with a massive data surge. Many people own multiple cell phones. India only has 252 MW of data center power, but this number will rise dramatically. In India, particularly in Mumbai, there are a lot of buildings for large data centers.

- Cloud technology is slowly gaining momentum in Asia-Pacific. Thus, the demand for managed services is increasing due to speed and agility. It will give a boost to cloud-based deployments.

- Regulators play a crucial role in enabling-or impeding-the growth of managed data center services. While some APAC regulators are clarifying outsourcing rules and guidelines to help firms achieve compliance, regulatory restrictions and cloud adoption blockers still exist.

Managed Data Center Services Industry Overview

The market for managed data center services is fragmented, with the majority of the giants providing services like data center management and enterprise network services, resulting in business continuity. Some major players in the market are Fujitsu Ltd., Cisco Systems Inc., Dell EMC, and IBM Corporation. New companies are also entering the market as the entry barrier is quite low.

In November 2022, in an era of growing connectedness and unpredictability, Fujitsu Limited announced plans to establish a new center for research and development in Tel Aviv, expediting the hiring of top personnel to drive innovation in data and security.

In October 2022, Cisco, a US-based global provider of technology services and telecom equipment, said it would invest in a dedicated data center in India for WebEx, its suite of services for remote conferencing, file sharing, and call center operations.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Market Definition and Scope

- 1.2 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Stakeholder Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Cyber Attacks and Risk of Data Leaks is Causing the Market to Grow

- 5.1.2 Need for Management of Large Volume of Data Generated is Expanding the Market

- 5.1.3 Rising use of Data center service in Retail Industry to boost the market.

- 5.2 Market Restraints

- 5.2.1 Lack of Skilled and Dedicated Personnel is Hindering the Market Growth

- 5.3 Impact of Covid-19 on Data Center Services Market

6 KEY TECHNOLOGY INVESTMENTS

- 6.1 Cloud Technology

- 6.2 Artificial Intelligence

- 6.3 Cyber Security

- 6.4 Digital Services

7 MARKET SEGMENTATION

- 7.1 By Type

- 7.1.1 Managed Storage

- 7.1.2 Managed Hosting

- 7.1.3 Managed Collocation

- 7.2 By Deployment Type

- 7.2.1 Cloud

- 7.2.2 On-premise

- 7.3 By End-user Industry

- 7.3.1 BFSI

- 7.3.2 Energy

- 7.3.3 Retail

- 7.3.4 Healthcare

- 7.3.5 Manufacturing

- 7.3.6 Other End-user Industries

- 7.4 Geography

- 7.4.1 North America

- 7.4.1.1 United States

- 7.4.1.2 Canada

- 7.4.1.3 Rest of North America

- 7.4.2 Europe

- 7.4.2.1 Germany

- 7.4.2.2 United Kingdom

- 7.4.2.3 France

- 7.4.2.4 Spain

- 7.4.2.5 Rest of Europe

- 7.4.3 Asia-Pacific

- 7.4.3.1 China

- 7.4.3.2 Japan

- 7.4.3.3 India

- 7.4.3.4 Rest of Asia-Pacific

- 7.4.4 Latin America

- 7.4.4.1 Brazil

- 7.4.4.2 Argentina

- 7.4.4.3 Rest of Latin America

- 7.4.5 Middle East and Africa

- 7.4.5.1 UAE

- 7.4.5.2 Saudi Arabia

- 7.4.5.3 South Africa

- 7.4.5.4 Rest of Middle East and Africa

- 7.4.1 North America

8 COMPETITIVE LANDSCAPE

- 8.1 Company Profiles

- 8.1.1 Fujitsu Ltd

- 8.1.2 Cisco Systems Inc.

- 8.1.3 Dell EMC

- 8.1.4 IBM Corporation

- 8.1.5 AT&T Inc.

- 8.1.6 HP Development Company LP

- 8.1.7 Microsoft Corporation

- 8.1.8 Verizon Communications Inc.

- 8.1.9 Dell Inc.

- 8.1.10 Rackspace Inc.

- 8.1.11 TCS Limited

- 8.1.12 Deutsche Telekom AG

9 INVESTMENT ANALYSIS

10 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日