|

市場調査レポート

商品コード

1906924

パルプおよび製紙用化学品:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)Pulp And Paper Chemicals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| パルプおよび製紙用化学品:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

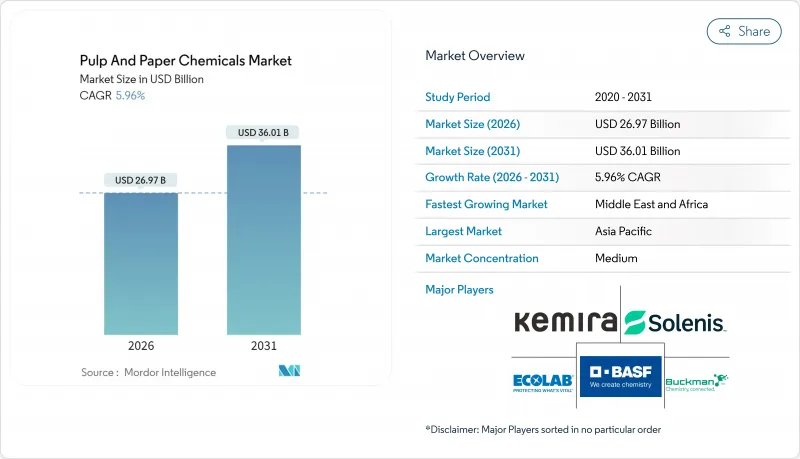

パルプおよび製紙用化学品市場は、2025年の254億5,000万米ドルから2026年には269億7,000万米ドルへ成長し、2026年から2031年にかけてCAGR5.96%で推移し、2031年までに360億1,000万米ドルに達すると予測されております。

包装用紙の需要増加、漂白・サイジング技術における急速な進歩、持続可能性への要求強化が相まって、持続的な成長の追い風と逆風が生まれています。アジア太平洋地域における生産能力の拡大、電子商取引の継続的な拡大、再生繊維への顕著な移行が、輝度向上、強度改善、淡水使用量削減を実現する特殊化学品の消費増加に寄与しています。一方で、排出規制の強化、原料価格の変動、エネルギー集約的な従来プロセスが、酵素系・バイオベース・クローズドループソリューションを中心とした技術革新をサプライヤーに迫っています。競合上の差別化は、保持性・排水性・バリア性能を最適化しつつ、製紙工場の炭素排出量・排水目標達成を支援する統合プログラムにかかっています。このため業界の既存企業は、ダウンタイムと化学薬品の過剰供給を削減する、対象を絞った買収、地域別生産拠点、デジタルサービスモデルに注力しています。

世界のパルプおよび製紙用化学品市場の動向と洞察

アジアにおける包装用紙生産能力の拡大

グリーンベイ・パッケージング社の10億米ドル規模の施設やスザノ社の16億6,000万レアル投資といった大規模資本プロジェクトは、高速機械向けに特化した保持助剤、排水化学薬品、表面サイジング剤に対する前例のない下流需要を引き起こしています。これらの巨大製紙工場は、輸送コスト増を避けるため現地調達を優先しており、サプライヤーは地域工場やサービスラボの展開を迫られています。生産能力の増加は世界の繊維需給バランスを逼迫させ、間接的に輸出志向の他地域製紙工場における添加剤消費を促進します。技術チームをエンドユーザーの操業開始スケジュールに連動させるサプライヤーは、初期段階の需要量と長期供給契約を獲得できます。最後に、地域的な過剰生産能力リスクの高まりは、コスト最適化プログラムの必要性を強め、化学薬品とリアルタイム分析を組み合わせたソリューションを提供できるベンダーを有利にします。

再生繊維原料の採用急増

循環型経済の要請とブランドオーナーの取り組みにより、特に欧州と北米において、平均再生原料含有率が上昇しています。二次繊維に含まれる汚染物質、粘着性物質、インク残渣の増加により、製紙工場では高度な浮選薬品、酵素ベースの脱墨処理、輝度と引張強度を維持する高電荷マイクロ粒子の採用が進んでいます。統合された「フルライン」化学薬品パッケージは調達を簡素化し、データ豊富なモニタリングは添加剤の過剰投与を削減します。100%再生原料を採用する段ボール原紙工場やティッシュ工場において、機会は最も急速に拡大しています。

AOXおよびCOD排出基準の厳格化

EUおよび米国の規制当局は、許容されるAOX(酸性有機性物質)およびCOD(化学的酸素要求量)の基準値を引き下げており、製紙工場は漂白工程の再設計や高資本コストを伴う三次処理設備の導入を迫られています。規模の経済性を欠く小規模工場では、コンプライアンス対応により年間運営コストが15~20%増加します。化学薬品サプライヤーは、低AOX蛍光増白剤、汚泥脱水補助剤、監査対応に有効な性能証明が可能なオンラインセンサーなどで対応しています。

セグメント分析

漂白剤はパルプ・製紙化学品市場を独占し、2025年には32.45%のシェアを占めました。このセグメントの優位性は、白度目標達成における不可欠な役割と、二酸化塩素から過酸化水素・酸素系への移行が進んでいることに起因します。この移行は、AOX規制の強化と塩素系残留物に対する消費者の監視強化によって後押しされています。供給業者は、化学的酸素要求量(COD)を低減する安定化過酸化物グレード、高効能活性化剤、分散剤への投資を進めています。

サイズ剤は絶対的な金額規模では小さいもの、2031年までCAGR6.31%で最も急速に成長するセグメントです。バイオベースおよび酵素系サイズ剤は、食品サービスや電子商取引向け包装に必要な、インク保持性、耐油性、炭素削減のバランスをコンバーターに提供します。パルプ化化学品は、統合クラフト工場に連動した安定した基盤を維持しています。一方、GCCやPCCなどの充填剤は、グラム当たりの高い不透明度を求める軽量化動向の恩恵を受けています。バインダー、特に再生ティッシュやタオルグレードに使用される湿潤強度樹脂は、衛生製品の需要が堅調に推移していることから、緩やかな伸びを示しています。

地域別分析

アジア太平洋地域は、堅調な設備投資と一人当たり包装消費量の増加に牽引され、2025年のパルプおよび製紙用化学品市場で46.85%のシェアを占めました。中国の最新五カ年計画では、コンテナボードと特殊ティッシュを戦略的セグメントと位置付け、省エネルギー型化学薬品パッケージへの補助金を促進しています。インドのティッシュブームは、ソフト強度樹脂と香料配合技術の需要を加速させています。東南アジアはサプライチェーンの多様化の恩恵を受けており、ベトナムとインドネシアはクラフトライナー工場への外国投資を誘致しています。

北米では、軽量化コンテナボードへの転換やカリフォルニア州などにおける再生繊維使用義務化の進展を背景に、安定した需要が継続しています。製紙工場では、企業のネットゼロ目標に沿うため、酸素脱リグニン化設備の改修や二酸化炭素回収パイロットプロジェクトへの投資が進められています。欧州では、グリーンディールや厳格な包装指令を背景に、バイオベースサイズ剤やPFASフリーバリアコーティングの採用が先行しています。

中東・アフリカ地域は、インフラ整備と食品・飲料包装の現地化を背景に、2031年までCAGR6.05%で拡大が見込まれます。サウジアラビアとエジプトにおける新たなティッシュ製造機の稼働が添加剤需要を牽引する一方、オマーンのソハール石油化学投資は脂肪酸誘導体の地域調達を強化します。南米ではブラジルのパルプ生産能力拡大を基盤に安定した成長が見込まれ、化学品サプライヤーは木材由来原料の確保に向け上流工程への統合を進めています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- アジアにおける包装用紙生産能力の拡大

- 再生繊維原料の採用急増

- 無水酵素漂白技術の革新

- カーボンネガティブ型バイオベースサイジング剤

- 電子商取引主導のSKU増加が特殊化学品を牽引

- 市場抑制要因

- AOXおよびCOD排出基準の厳格化

- 代替基質と比較した高いエネルギー集約度

- 塩素単体の価格変動性

- バリューチェーン分析

- ポーターのファイブフォース

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場規模と成長予測

- タイプ別

- バインダー

- 漂白剤

- 充填剤

- パルプ製造用化学品

- サイジング剤

- その他の種類

- 用途別

- 新聞用紙

- 包装用紙および工業用紙

- 印刷用紙および筆記用紙

- パルプ工場および水処理

- その他の用途

- 地域別

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- インドネシア

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- トルコ

- 南アフリカ

- エジプト

- その他の中東・アフリカ

- アジア太平洋地域

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア**/順位分析

- 企業プロファイル

- Arkema

- Ashland Inc.

- BASF

- Buckman

- Cargill Incorporated

- Celanese

- Chemours

- Clariant

- Ecolab

- ERCO Worldwide

- Georgia-Pacific

- Imerys S.A.

- Kemira

- Nouryon

- Omya International AG

- Solenis

- Solvay

- Stora Enso

- UPM

- Valmet