|

市場調査レポート

商品コード

1550529

米国のオプトエレクトロニクス:市場シェア分析、産業動向、成長予測(2024年~2029年)United States Optoelectronics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 米国のオプトエレクトロニクス:市場シェア分析、産業動向、成長予測(2024年~2029年) |

|

出版日: 2024年09月02日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

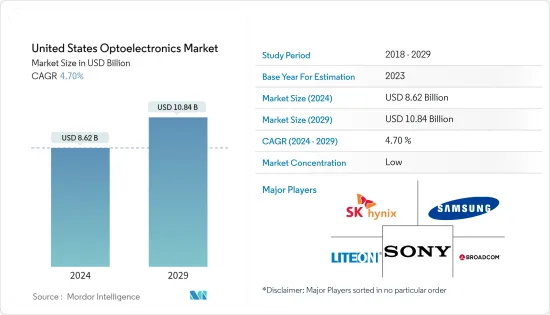

米国のオプトエレクトロニクス市場規模は2024年に86億2,000万米ドルと推定され、2029年には108億4,000万米ドルに達すると予測され、予測期間(2024-2029年)のCAGRは4.70%で成長します。

主なハイライト

- オプトエレクトロニクス(またはオプトロニクス)は、光を検出、制御、放射するデバイスやシステムの研究と応用に焦点を当てたエレクトロニクスの一分野です。この分野には、可視光、赤外線、紫外線、さらにはガンマ線やX線など、さまざまな形態の光が含まれます。オプトエレクトロニクス・デバイスは、電気信号を光信号に変換したり、逆に光信号を電気信号に変換したりする変換器として機能します。オプトエレクトロニクスは主に、光と電子材料(特に半導体)との相互作用による量子力学的効果に基づいています。

- オプトエレクトロニクスは電気的絶縁を提供し、異なる電圧で動作する2つのシステムのインターフェイスを可能にします。これは、誘導ノイズ、クロストーク、磨耗による信号劣化に起因するデータ・トランスミッションの問題を抑制するのに役立ちます。オプトエレクトロニクスは通信に高い帯域幅を提供するため、トランスミッションやデータ伝送などさまざまな用途で有利です。オプトエレクトロニクス・デバイスは消費電力が少ないため、エネルギー効率が高く、消費電力が懸念される用途に適しています。

- また、オプトエレクトロニクス・デバイスは、電子回路間を危険な電圧が通過するのを防ぐため、通信、エネルギー変換、センシングなど様々なアプリケーションの安全性を高めることができます。さらに、オプトエレクトロニクス・デバイスは物理的に距離を隔ててもデータをやり取りできるため、物理的なスペースに制約のあるアプリケーションに適しています。

- 従来の白熱光源からLEDへの移行は、米国の照明業界に革命をもたらしました。LEDはエネルギー効率が高く、長寿命で環境に優しいため、消費者にとっても企業にとっても大幅なコスト削減につながります。建築物の照明にLEDランプの使用が増加していることも、オプトエレクトロニクスに大きな可能性をもたらしています。

- 米国エネルギー省によると、米国では2020年から2035年にかけてLED照明が急激に普及すると予想されています。2025年までに、LED照明は住宅照明の73%に導入され、あらゆる分野で最も一般的な光源になるはずです。このことは、予測期間を通じて市場が成長・向上するための大規模な成長機会を生み出し、市場を大きく牽引すると思われます。

- さらに米国エネルギー省によると、予測期間中に最もLED照明が設置されるのは住宅部門であり、2025年には38億ユニット、2035年には62億1,000万ユニットを記録します。

- 心拍数モニタや血糖値センサのようなウェアラブル健康技術の人気が高まっていることが、米国の光電子センサ需要を牽引しています。これらのデバイスは、光ベースの技術を利用して様々な健康パラメータをリアルタイムでモニタします。

- しかし、製造コストや加工コストが高いこと、光電子デバイスのエネルギー損失や加熱に課題があることが、調査した市場成長の抑制要因になりそうです。

- さらに、インフレと金利の上昇は、個人消費を減少させ、半導体とエレクトロニクスの需要を妨げ、調査市場の成長鈍化につながっています。さらに、米国と中国の貿易戦争は世界の半導体サプライチェーンを混乱させました。さらに、米国による中国の半導体製造装置に対する厳格な輸出入規制のために、民生用電子機器部門の生産が危うくなっています。

米国オプトエレクトロニクス市場動向

需要を牽引すると予想されるイメージセンサセグメント

- イメージセンサーは、オプトエレクトロニクスにおいて、カメラやイメージングデバイスが光子を解釈・処理可能な電気信号に変換するための重要なコンポーネントです。最初のデジタルカメラでは、電荷結合素子(CCD)を使用して、変調のための電荷の移動を促進しました。しかし、最近のカメラでは、低消費電力、高集積、標準的なCMOS製造プロセスとの互換性から、CMOS(相補型金属酸化膜半導体)センサーが主流となっています。

- 様々な業界で高解像度の画像キャプチャデバイスの需要が急増する中、CMOS技術は高い採用率を記録しています。CMOS技術は、高品質の画像を提供しながら、より速いシャッタースピードを提供します。さらに、人工知能(AI)と機械学習の進歩により、よりスマートな画像処理アルゴリズムが可能になった。これらのアルゴリズムは画質を向上させ、顔認識、物体検出、拡張現実(AR)などの機能を可能にし、様々なイメージセンサーに新たな機会を生み出しています。

- スマートフォンや家電製品の普及は、米国のイメージセンサー市場を大きく牽引しています。スマートフォンはどこにでもあるものとなり、これらのデバイスに搭載される高画質カメラへの需要が急増しています。消費者が写真やビデオ撮影をスマートフォンに依存するようになっているため、メーカー各社は先進的なイメージセンサーを搭載したカメラシステムのアップグレードを続けています。

- さらに、ビジュアルコンテンツが極めて重要なソーシャル・メディア・プラットフォームの台頭により、カメラの性能に対する消費者の期待が高まっています。この動向により、光学ズーム、低照度性能、手ぶれ補正などの機能を備えた高解像度イメージセンサーへの投資が増加しています。

- 自動車業界がADAS(先進運転支援システム)や自律走行車にシフトしていることも、イメージセンサー市場の重要な促進要因となっています。イメージセンサーは、バックカメラ、車線逸脱警告、駐車支援システムなどのアプリケーションを通じて、自動車の安全性と機能性を高める上で重要な役割を果たしています。

- 自動車メーカーが360度の視界や歩行者検知などの機能をサポートするためにより高度なセンサー技術を取り入れるにつれて、高性能画像センサーの需要は拡大すると予想されます。完全自律走行車の開発が進めば、この動向はさらに加速し、イメージセンサー・メーカーに新たなビジネスチャンスをもたらすと思われます。

- 米国は世界最大級の自動車市場です。ゼネラル・モーターズ、フォード、クライスラーといった自動車業界の著名なリーダーの本拠地であり、北米における自動車生産は著しく成長しています。米国では自動車の利用が増加しているため、スマートパーキングの需要も伸びており、パーキング・サラウンド・ビュー用の小型カメラ・モジュールの需要が高まっています。BEAによると、2023年5月の米国自動車市場セグメントでは、ライトトラックの販売台数が107万台弱と、2023年4月の107万台強から減少し、前年同月比約23.06%増となり、引き続き最も重要なセグメントとなっています。

情報技術分野が大きな市場シェアを占める

- オプトエレクトロニクスの主な用途の一つは光ファイバー通信です。光ファイバーケーブルは、レーザーや発光ダイオード(LED)によって生成された光パルスとしてデータを伝送します。この技術は、従来の銅線ケーブルよりもはるかに高い帯域幅を可能にし、より速いインターネット速度とより大きなデータ容量を実現します。光ファイバーは、都市や国を結ぶバックボーン・ネットワークや、家庭や企業へのラスト・マイル接続に不可欠です。

- 光検出器や光増幅器などの光電子部品も通信システムには欠かせないです。光検出器は入力された光信号を電気信号に変換し、光増幅器は長距離にわたってこれらの信号の強度を高め、データの完全性の損失を最小限に抑えます。波長分割多重(WDM)のような技術は、光電子原理を利用して、複数のデータストリームを単一のファイバーで同時に送信し、ネットワークの効率を大幅に向上させます。

- さらに、コンパクトでエネルギー効率の高い光トランシーバーに対する需要は、近年増加傾向にあります。このような需要の増加は、データセンターのアグリゲーションやバックプレーン用途での光トランシーバの設置が増加していることや、高速データ伝送の必要性など、いくつかの要因に起因しています。このような動向は、市場成長に有利な機会を提供すると予想されます。

- 通信に加え、オプトエレクトロニクスは、高速データ処理やストレージシステムをサポートするデータセンタでは極めて重要です。レーザベースの相互接続と光スイッチは、サーバ内およびサーバ間のデータ転送の速度と効率を高め、全体的なパフォーマンスを向上させ、エネルギー消費を削減します。

- データ需要が増加するにつれ、光インターコネクトへの移行が一般的になり、将来の成長に対応する拡張性のあるソリューションが提供されています。Cloudsceneによると、2024年3月現在、米国には5,381のデータセンターがあると報告されており、これは世界のどの国よりも多いです。米国の堅牢なデータセンターエコシステムは、調査対象市場の成長を大きく促進する可能性が高いです。

- さらに、オプトエレクトロニクスは、モノのインターネットや5Gネットワークのような新興技術に不可欠です。IoTでは、オプトエレクトロニクスセンサやデバイスがリアルタイムのデータ収集とトランスミッションを容易にし、スマートホーム、産業システムなど多様なアプリケーションの接続性と自動化を強化します。5Gでは、オプトエレクトロニクスコンポーネントがより高い周波数とより速いデータレートを可能にし、米国で高まるモバイル接続のニーズをサポートします。

米国オプトエレクトロニクス産業概要

米国オプトエレクトロニクス市場は、パナソニック株式会社、サムスン電子、Omnivision Technologies Inc.、ソニー株式会社、Osram Licht AG、Koninklijke Philips N.V.、Vishay Intertechnology, Inc.、Texas Instruments Inc.、LITE-ON Technology Corporation、ローム(ROHM SEMICONDUCTOR)、三菱電機株式会社、Broadcom Inc.、シャープ株式会社、SK Hynix Inc.など様々な企業が存在する断片的な市場です。市場の各社は、消費者の複雑で進化する要求に応える先進的な製品を革新しています。

- 2023年11月、ソニーセミコンダクタソリューションズ株式会社(SSS)は最新のイノベーションであるIMX992短波長赤外(SWIR)イメージセンサーを発表しました。有効画素数は532万画素。同社によると、SSSの先駆的なCu-Cu接続技術により、SWIRセンサー領域で最小となるわずか3.45μmの強固なピクセルサイズを実現しました。さらに、このセンサーのピクセル構造は、光の取り込み効率を高めるために最適化されています。また、光を効率よく取り込むために画素構造を最適化。可視域から不可視域の短波長赤外域(波長:0.4~1.7μm)までの広帯域にわたり、高精細な撮像が可能となります。

- 2023年9月、テキサス・インスツルメンツ・インコーポレイテッドは、信号分離半導体の新しいオプトエミュレータ・ポートフォリオを発表しました。TI初のオプトエミュレータは、シグナルインテグリティの向上、消費電力の削減、産業用および車載用高電圧システムの寿命延長を目的として設計されています。TI初のオプトエミュレータは、業界で広く使用されているオプトカプラとのピン互換性を誇ります。この互換性により、二酸化ケイ素(SiO2)絶縁技術の明確な利点を活用しながら、現在の設計へのスムーズな移行が保証されます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業バリューチェーン分析

- 業界の魅力度ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

- COVID-19の影響とその他のマクロ経済要因が市場に与える影響

第5章 市場力学

- 市場促進要因

- スマート家電と次世代技術への需要の高まり

- 技術の産業応用の増加

- Li-Fi市場の拡大

- 市場の課題/抑制要因

- 高い製造・加工コスト

- 光電子デバイスのエネルギー損失と加熱に関する課題

第6章 市場セグメンテーション

- デバイスタイプ別

- LED

- レーザーダイオード

- イメージセンサー

- オプトカプラ

- 太陽電池

- その他

- エンドユーザー産業別

- 自動車

- 航空宇宙・防衛

- 家電

- 情報技術

- ヘルスケア

- 住宅・商業

- 産業

- その他

第7章 競合情勢

- 企業プロファイル

- SK Hynix Inc.

- Panasonic Corporation

- Samsung Electronics

- Omnivision Technologies Inc

- Sony Corporation

- Osram Licht AG

- Koninklijke Philips N.V.

- Vishay Intertechnology, Inc

- Texas Instruments Inc

- LITE-ON Technology Corporation

- Rohm Co., Ltd(ROHM SEMICONDUCTOR)

- Mitsubishi Electric Corporation

- Broadcom Inc.

- Sharp Corporation

第8章 投資分析

第9章 市場機会と今後の動向

The United States Optoelectronics Market size is estimated at USD 8.62 billion in 2024, and is expected to reach USD 10.84 billion by 2029, growing at a CAGR of 4.70% during the forecast period (2024-2029).

Key Highlights

- Optoelectronics (or optronics) is a branch of electronics that focuses on the study and application of devices and systems that detect, control, and emit light. This field encompasses a variety of light forms, including visible light, infrared, ultraviolet, and even gamma rays and X-rays. Optoelectronic devices function as transducers, converting electrical signals into optical signals and vice versa. They are primarily based on the quantum mechanical effects of light interacting with electronic materials, particularly semiconductors.

- Optoelectronics provide electrical isolation, allowing two systems that operate at different voltages to interface. This helps in limiting data transmission issues caused by induced noise, crosstalk, and signal degradation due to worn runs. Optoelectronics provide a high bandwidth for communications, which is advantageous in various applications like telecommunications and data transmission. Optoelectronic devices consume less power, making them energy-efficient and suitable for applications where power consumption is a concern.

- Optoelectronics devices also prevent dangerous voltages from passing between electronic circuits, enhancing safety in various applications in files such as communications, energy conversion, and sensing. Moreover, optoelectronic devices can be physically separated by a distance and still pass data, making them suitable for applications where physical space is a constraint.

- The transition from traditional incandescent light sources to LEDs has revolutionized the lighting industry in the United States. LEDs are more energy-efficient, longer-lasting, and environmentally friendly, leading to substantial cost savings for consumers and businesses alike. The rising growth in the use of LED lamps in buildings for lighting also provides enormous possibilities for optoelectronics.

- As per the US Department of Energy, LED lights are expected to gain popularity drastically between 2020 and 2035 in the United States. By 2025, LED lights should be installed in 73% of residential lighting and become the most common light source in all sectors. This will create massive growth opportunities for the market to grow and improve throughout the forecast period, driving the market significantly.

- Further, according to the US Department of Energy, the residential sector will see the most LED light installations in the forecasted period, recording 3,800 million units in 2025 and 6,210 million units by 2035.

- The increasing popularity of wearable health technology, like heart rate monitors and blood glucose sensors, drives the demand for optoelectronic sensors in the United States. These devices utilize light-based technologies to monitor various health parameters in real-time.

- However, high manufacturing and fabrication costs, as well as challenges with energy loss and heating of optoelectronic devices, are likely to act as restraining factors in the growth of the studied market.

- Further, the increased inflation and interest rates reduced consumer spending and hampered the demand for semiconductors and electronics, leading to slow growth in the studied market. Further, the United States and China trade war disturbed the global semiconductor supply chain. Additionally, owing to strict export and import controls on semiconductor manufacturing equipment in China by the United States, the production of the consumer electronics sector is compromised.

United States Optoelectronics Market Trends

The Image Sensors Segment Anticipated to Drive Demand

- Image sensors are a crucial component in optoelectronics that allows cameras and imaging devices to convert photons into electrical signals that can be interpreted and processed. The first digital cameras used charge-coupled devices (CCDs) to facilitate the movement of electrical charge through the device for modulation. However, modern cameras predominantly use complementary metal-oxide-semiconductor (CMOS) sensors due to their low power consumption, high integration, and compatibility with standard CMOS fabrication processes.

- With the upsurge in the demand for high-definition image-capturing devices in various industries, CMOS technology has experienced a high adoption rate. CMOS technology provides a faster shutter speed while delivering high-quality images. Moreover, advancements in artificial intelligence (AI) and machine learning have enabled smarter image-processing algorithms. These algorithms enhance image quality and enable features such as facial recognition, object detection, and augmented reality (AR), creating new opportunities for image sensors in various.

- The proliferation of smartphones and consumer electronics is a significant driver of the image sensor market in the United States. Smartphones have become ubiquitous, and the demand for high-quality cameras in these devices has surged. With consumers increasingly relying on their smartphones for photography and videography, manufacturers are continually upgrading camera systems to include advanced image sensors.

- Additionally, the rise of social media platforms, where visual content is extremely important, has heightened consumer expectations for camera performance. This trend has led to increased investment in high-resolution image sensors with features such as optical zoom, low-light performance, and image stabilization.

- The automotive industry's shift towards advanced driver-assistance systems (ADAS) and autonomous vehicles is another critical driver of the image sensor market. Image sensors play a vital role in enhancing vehicle safety and functionality through applications such as rearview cameras, lane departure warnings, and parking assistance systems.

- As automakers incorporate more sophisticated sensor technologies to support features like 360-degree visibility and pedestrian detection, the demand for high-performance image sensors is expected to grow. The ongoing development of fully autonomous vehicles will further accelerate this trend, creating new opportunities for image sensor manufacturers.

- The United States is one of the largest automotive markets in the world. Being home to prominent automotive industry leaders, such as General Motors, Ford, and Chryslers, vehicle production in North America is growing significantly. With the increasing usage of cars in the United States, the demand for smart parking is also growing, propelling the demand for compact camera modules for application in parking surround view. According to BEA, at just under 1.07 million unit sales, light trucks remained the most significant US auto market segment in May 2023, down from over 1.07 unit sales in April 2023 and increasing by approximately 23.06% year-on-year.

The Information Technology Sector to Hold a Major Market Share

- One of the primary applications of optoelectronics is in fiber-optic communication. Fiber-optic cables transmit data as light pulses generated by lasers or light-emitting diodes (LEDs). This technology allows for much higher bandwidth than traditional copper cables, enabling faster internet speeds and greater data capacity. Fiber optics are essential for backbone networks, connecting cities and countries, and for last-mile connections to homes and businesses.

- Optoelectronic components, such as photodetectors and optical amplifiers, are also vital in communications systems. Photodetectors convert incoming light signals back into electrical signals, while optical amplifiers boost the strength of these signals over long distances, ensuring minimal loss of data integrity. Technologies like wavelength-division multiplexing (WDM) utilize optoelectronic principles to send multiple data streams simultaneously over a single fiber, significantly increasing network efficiency.

- Additionally, the demand for compact and energy-efficient optical transceivers has been on the rise in recent years. This increase in demand can be attributed to several factors, including the growing installation of optical transceivers for data center aggregation and backplane applications, as well as the need for high-speed data transmission. Such trends are anticipated to offer lucrative opportunities for the growth of the market.

- In addition to communication, optoelectronics is crucial in data centers, where it supports high-speed data processing and storage systems. Laser-based interconnects and optical switches enhance the speed and efficiency of data transfer within and between servers, improving overall performance and reducing energy consumption.

- As data demands increase, the transition to optical interconnects becomes more common, offering a scalable solution for future growth. According to Cloudscene, as of March 2024, there were a reported 5,381 data centers in the United States, the most of any country worldwide. The robust data center ecosystem in the United States is likely to significantly drive the growth of the studied market.

- Moreover, optoelectronics is integral to emerging technologies like the Internet of Things and 5G networks. In IoT, optoelectronic sensors and devices facilitate real-time data collection and transmission, enhancing connectivity and automation in a diverse range of applications, like from smart homes, industrial systems, etc. For 5G, optoelectronic components enable higher frequencies and faster data rates, supporting the growing need for mobile connectivity in the United States.

United States Optoelectronics Industry Overview

The United States optoelectronics market is a fragmented market with the presence of various players like Panasonic Corporation, Samsung Electronics, Omnivision Technologies Inc., Sony Corporation, Osram Licht AG, Koninklijke Philips N.V., Vishay Intertechnology, Inc., Texas Instruments Inc., LITE-ON Technology Corporation, Rohm Co., Ltd (ROHM SEMICONDUCTOR), Mitsubishi Electric Corporation, Broadcom Inc., Sharp Corporation, SK Hynix Inc., etc. The companies in the market are innovating advanced products that cater to the complex and evolving requirements of consumers.

- In November 2023, Sony Semiconductor Solutions Corporation (SSS) unveiled its latest innovation, the IMX992 short-wavelength infrared (SWIR) image sensor. It features a 5.32 effective megapixels. As per the company, its SSS's pioneering Cu-Cu connection technology enables it to achieve a robust pixel size of just 3.45 μm, the smallest in the SWIR sensor realm. Moreover, the sensor's pixel structure has been optimized to enhance light capture efficiency. It also features an optimized pixel structure for efficiently capturing light. It enables high-definition imaging across a broad spectrum ranging from visible to invisible short-wavelength infrared regions (wavelength: 0.4 to 1.7 μm).

- In September 2023, Texas Instruments Incorporated introduced its new opto-emulator portfolio of signal isolation semiconductors. TI's first opto-emulators are engineered to enhance signal integrity, reduce power consumption, and prolong the lifespan of high-voltage systems in industrial and automotive settings. These opto-emulators, a debut from TI, boast pin-to-pin compatibility with the industry's prevalent optocouplers. This compatibility ensures a smooth transition into current designs while harnessing the distinct advantages of silicon dioxide (SiO2) isolation technology.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness Porters Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Impact of COVID-19 Aftereffects and Other Macroeconomic Factors on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Demand for Smart Consumer Electronics and Next-Generation Technologies

- 5.1.2 Increasing Industrial Applications of the Technology

- 5.1.3 Expansion of the Li-Fi Market

- 5.2 Market Challenges/restraints

- 5.2.1 High Manufacturing and Fabrication Costs

- 5.2.2 Challenges With Energy Loss and Heating of Optoelectronic Devices

6 MARKET SEGMENTATION

- 6.1 By Device Type

- 6.1.1 LED

- 6.1.2 Laser Diode

- 6.1.3 Image Sensors

- 6.1.4 Optocouplers

- 6.1.5 Photovoltaic cells

- 6.1.6 Others

- 6.2 By End-User Industry

- 6.2.1 Automotive

- 6.2.2 Aerospace & Defense

- 6.2.3 Consumer Electronics

- 6.2.4 Information Technology

- 6.2.5 Healthcare

- 6.2.6 Residential and Commercial

- 6.2.7 Industrial

- 6.2.8 Others

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 SK Hynix Inc.

- 7.1.2 Panasonic Corporation

- 7.1.3 Samsung Electronics

- 7.1.4 Omnivision Technologies Inc

- 7.1.5 Sony Corporation

- 7.1.6 Osram Licht AG

- 7.1.7 Koninklijke Philips N.V.

- 7.1.8 Vishay Intertechnology, Inc

- 7.1.9 Texas Instruments Inc

- 7.1.10 LITE-ON Technology Corporation

- 7.1.11 Rohm Co., Ltd (ROHM SEMICONDUCTOR)

- 7.1.12 Mitsubishi Electric Corporation

- 7.1.13 Broadcom Inc.

- 7.1.14 Sharp Corporation