|

市場調査レポート

商品コード

1694047

米国の周波数制御とタイミング装置:市場シェア分析、産業動向、成長予測(2025~2030年)United States Frequency Control And Timing Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 米国の周波数制御とタイミング装置:市場シェア分析、産業動向、成長予測(2025~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 171 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

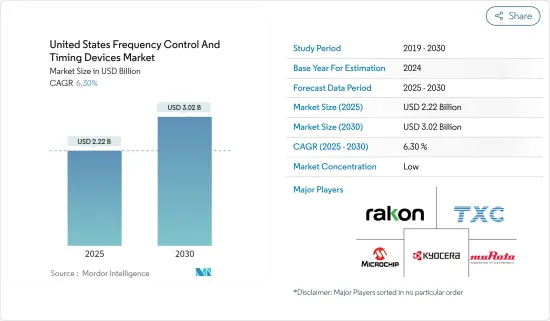

米国の周波数制御とタイミング装置市場規模は、2025年に22億2,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは6.3%で、2030年には30億2,000万米ドルに達すると予測されます。

周波数制御装置は、情報の正確な伝送に必要な信号とタイミング制御を提供し、電子システムにおいて極めて重要な役割を果たしています。水晶振動子、MEMS、セラミック共振器に応用されている原理を活用することで、これらの装置は安定した発振を発生させ、デジタルシステムのクロッキングとタイミングの安定性を確保することができます。

主要ハイライト

- 同市場は、5Gスマートフォンの普及と世界の5Gネットワークの拡大によって牽引されています。CTAの報告によると、米国の消費者向けハイテク小売売上高は2.8%増加し、2024年には5,120億米ドルに達すると予測されています。

- さらに、人工知能機能の統合により、今年はPCやスマートフォンなど様々な装置のアップグレードが進むと予想されています。今後、チップメーカーは、販売を強化し、アップグレードを促進するために、より多くのAI機能を装置に組み込むことに注力しています。

- さらに、産業のリーダーたちは、拡張現実と仮想現実ヘッドセットが今後数年間の主要促進要因になると強調しています。CES 2024では、Meta Platforms(META)のVRヘッドセットからXrealのスマートグラスまで、多様な拡張現実装置が期待できます。

- 周波数制御とタイミング装置市場は、エレクトロニクス産業の中でも重要なセグメントであり、さまざまな用途に不可欠な部品を提供しています。しかし、これらの装置の開発・製造コストが高いことが、市場成長の課題となっています。

- ロシア・ウクライナ戦争や米国・中国の緊張など、流行後の地政学的緊張が市場成長に影を落としています。特に、ロシア・ウクライナ紛争に対応する主要ベンダーは、欧州や米国の厳しい政府規制により、同地域での販売を停止しました。

- 例えば、Texas Instrumentsは2022年2月からロシア、イラン、ベラルーシへの販売を停止しました。ロシア・ウクライナ紛争は、エレクトロニクス産業に大きな影響を与えようとしています。ロシア・ウクライナ紛争は、既存の半導体サプライチェーンの課題と持続的なチップ不足をさらに悪化させています。この混乱は、ニッケル、パラジウム、銅、チタン、アルミニウムといった主要原料の価格変動や潜在的な不足につながり、製品生産に直接影響を及ぼす可能性があります。

米国の周波数制御とタイミング装置市場動向

MEMS発振器が大きく成長

- 微小電気機械システム(MEMS)発振器は正確なタイミング装置として機能し、さまざまな用途に不可欠な安定した基準周波数を生成します。これらの周波数は、電子システムのシーケンス、データ転送管理、無線周波数の定義、時間測定において極めて重要です。MEMS発振器はコンパクトな設計で、衝撃や振動に強く、正確な計時を実現します。その耐久性により、産業、商業、民生セグメントにわたる幅広い用途に適しています。

- 最近のポータブルエレクトロニクスやウェアラブルエレクトロニクスの急増は、発振器に代表される電子部品のエネルギー使用量とサイズを最小限に抑えようとする動きを浮き彫りにしています。クロック回路では、正確な周波数生成とエネルギー効率という2つの利点から、MEMSベースの発振器がますます好まれています。

- 米国ではスマートフォンやモバイル装置の普及が進んでおり、MEMS発振器市場は今後数年で大きく成長する展望です。信頼性、低消費電力、高性能で知られるMEMS発振器は、スマートフォンに自然に適合します。標準的な半導体技術との互換性により、製造と統合プロセスがさらに合理化されます。その結果、スマートフォンの利用が急増し続けるにつれて、MEMS発振器の需要は拡大する傾向にあります。

- 米国では、IoT導入の急増がMEMS発振器の需要を牽引しています。コンパクトな設計、エネルギー効率、精度で知られるMEMS発振器は、IoT用途に最適です。MEMS発振器は、正確なタイミングと同期を保証し、データの精度を高め、IoT装置のサイズと消費電力の制約に適合します。そのため、メーカーや開発者にとって好ましい選択肢となっています。MEMS発振器はIoT装置の信頼性と性能を高め、スマートホーム、産業オートメーション、医療でのシームレスな運用を可能にします。厳しいタイミング要件を満たすMEMS発振器の能力は、米国のIoT状況の拡大を反映し、MEMS発振器の需要を促進しています。

エンドユーザーとして急成長する自動車産業

- 発振器は、現代の自動車において極めて重要な役割を担っています。今日の自動車は、基本的に車輪の上の高速ネットワークであり、タイミングチップがなければ停止してしまいます。インターネット自体も、この重要な部品にかかっています。自動車セクタにおける半導体の将来の軌道は、電動化と自律走行という2つの支配的な力によって形作られています。

- 電動化は、主にハイブリッド車と電気自動車(EV)の普及が原動力となっており、今後10年間で大きく躍進する展望です。IEAによると、米国の電気自動車新規登録台数は2023年に140万台に達し、2022年比で40%の大幅増となります。2023年の成長率は前年よりやや鈍化したもの、電気自動車の需要全体は底堅さを維持しています。

- この勢いは、産業がバッテリーコストの削減、充電インフラの強化、EVの走行距離の延長に注力していることが背景にあります。同時に、自動車はセンサやインテリジェントシステムを満載した「スマート」なものになりつつあります。これが、第2の大きな動向である自律走行の舞台となります。衝突回避システムから自動駐車、車線変更センサに至るまで、かつては「贅沢品」であったこれらの機能は当たり前のものとなり、ADAS(先進運転支援システム)、自律走行、先進的テレマティクスの基礎を築いています。

- メディアの報道によると、米高速道路交通安全局(NHTSA)は2029年から、すべての新車に自動緊急ブレーキ(AEB)の搭載を義務付けた。この新規制により、米国で販売される重量1万ポンド(約4500kg)以下の新型乗用車はすべて、この安全技術を搭載しなければならなくなります。米国政府は、この措置によって年間400人の命を救い、数,000人の負傷を防ぐことができると推定しています。自動車メーカーは2029年9月1日までにこの規制に適合する必要があるが、少量生産メーカーには猶予期間が設けられています。これらの規制は、周波数制御とタイミング装置市場を著しく強化しています。

米国の周波数制御とタイミング装置産業概要

米国の周波数制御とタイミング装置市場は細分化されており、イノベーションによる持続的競争優位性は相当なものです。エンドユーザー産業の新規顧客からの需要急増が予想されることから、競争は激化する一方であり、Murata Manufacturing、京セラ、Rakon Limited、Microchip Technology Inc.、TXC Corporationなどがその一例です。

- 2024年4月-先端電子部品メーカーである京セラエイベックスは、「京セラエイベックスコンポーネンツ株式会社(Erie)」の名称で、高品質・低ノイズの水晶振動子周波数制御製品の製造・設計センターを新設することを発表しました。新設された製造施設では、特許を取得した比類のない低消費電力のOCXO(オーブン制御水晶発振器)、各種TCXO(温度演算水晶発振器)、VCXO(電圧演算水晶発振器)を120万個以上製造する予定。

- 2024年2月-ラコンはMWCバルセロナ2024で、最新の無線ネットワークとIT・通信データセンター向けの初期拡大ホールドオーバーソリューションを展示。Error Exchange OCXO(MercuryXE2)は、ラコンが最近発売した小型IC-OCXO Mercuryのバージョンです。周波数エラー交換処理とエージング補償を組み込むことで、ネットワークシンクロナイザ評価ボード上のシステムの電流同期能力を向上させ、ホールドオーバー性能を高めます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業バリューチェーン分析

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- COVID-19の影響とマクロ経済動向の産業への影響

第5章 市場力学

- 市場の促進要因

- 周波数制御とタイミング装置の需要を増大させる5Gの採用拡大

- 先進自動車用途の需要増加

- 市場課題

- 開発コストの高さ

第6章 市場セグメンテーション

- タイプ別

- 水晶振動子

- 発振器

- 温度補償型水晶発振器(TCXO)

- 電圧制御水晶発振器(VCXO)

- オーブン制御水晶発振器(OCXO)

- MEMS発振器

- その他の発振器

- 共振器

- ソー・フィルター

- リアルタイムクロック

- エンドユーザー産業別

- 自動車

- コンピュータと周辺装置

- 通信/サーバー/データストレージ

- コンシューマーエレクトロニクス

- 産業

- 防衛・航空宇宙

- IoT(ウェアラブル、フィットネストラッカー、スマートホーム装置、スマートシティ、スマート照明システム、その他)

- その他のエンドユーザー産業(医療、石油・ガス、農業、小売、検査・計測、その他)

第7章 競合情勢

- 企業プロファイル

- Murata Manufacturing Co. Ltd

- Kyocera Corporation

- Rakon Limited

- Microchip Technology Inc.

- TXC Corporation

- Seiko Epson Corporation

- Daishinku Corporation

- Hosonic Technology(Group)Co. Ltd

- Nihon Dempa Kogyo Co. Ltd

- SiTime Corporation

- SIWARD Crystal Technology Co. Ltd

- Texas Instruments Inc.

- NXP Semiconductors

- Abracon LLC

- CTS Corporation

第8章 投資分析

第9章 市場機会と今後の動向

The United States Frequency Control And Timing Devices Market size is estimated at USD 2.22 billion in 2025, and is expected to reach USD 3.02 billion by 2030, at a CAGR of 6.3% during the forecast period (2025-2030).

Frequency control devices play a pivotal role in electronic systems, providing the necessary signals and timing controls for the precise transmission of information. By leveraging principles applied to quartz crystals, MEMS, and ceramic resonators, these devices can generate stable oscillations, ensuring clocking and timing stability in digital systems.

Key Highlights

- The market is being propelled by the rising adoption of 5G smartphones and the expanding 5G network coverage globally. In the United States, consumer tech retail sales are projected to climb by 2.8% to reach a substantial USD 512 billion in 2024, as reported by CTA.

- Furthermore, the integration of artificial intelligence features is expected to drive upgrades across various devices, including PCs and smartphones, this year. Looking ahead, chip manufacturers are homing in on infusing more AI capabilities into devices to bolster sales and encourage upgrades.

- Additionally, industry leaders highlight that augmented reality and virtual reality headsets will be key growth drivers in the coming years. At CES 2024, one can expect diverse extended reality devices, ranging from VR headsets by Meta Platforms (META) to smart glasses by Xreal.

- The frequency control and timing devices market is a critical segment within the electronics industry, providing essential components for various applications. However, the high costs of developing and producing these devices challenge the market's growth.

- Post-pandemic geopolitical tensions, including the Russia-Ukraine War and US-China tensions, have cast a shadow on market growth. Notably, major vendors responding to the Russia-Ukraine conflict halted sales in the region due to stringent government restrictions from Europe and the United States.

- For example, Texas Instruments ceased sales to Russia, Iran, and Belarus starting in February 2022. The Russia-Ukraine conflict is poised to significantly impact the electronics industry. It has further exacerbated existing semiconductor supply chain challenges and the persistent chip shortage. This disruption could lead to price volatility and potential shortages in key raw materials like nickel, palladium, copper, titanium, and aluminum, directly affecting the production of products.

US Frequency Control and Timing Devices Market Trends

MEMS Oscillator to Witness Significant Growth

- Microelectromechanical system (MEMS) oscillators serve as precise timing devices, producing stable reference frequencies crucial for various applications. These frequencies are pivotal in electronic system sequencing, data transfer management, defining radio frequencies, and time measurement. MEMS oscillators offer a compact design, delivering precise timekeeping that's resilient against shocks and vibrations. Their durability makes them well-suited for a wide range of applications spanning industrial, commercial, and consumer sectors.

- The recent surge in portable and wearable electronics underscores the push to minimize energy usage and size across electronic components, notably oscillators. Clock circuits are increasingly favoring MEMS-based oscillators for their dual benefits: precise frequency generation and energy efficiency.

- The rising adoption of smartphones and mobile devices across the United States is poised to fuel substantial growth in the MEMS oscillator market in the coming years. MEMS oscillators, known for their reliability, low power consumption, and high performance, find a natural fit in smartphones. Their compatibility with standard semiconductor techniques further streamlines their manufacturing and integration processes. Consequently, as smartphone usage continues to surge, the demand for MEMS oscillators is set to escalate.

- The surge in IoT adoption is driving the demand for MEMS oscillators in the United States. Known for their compact design, energy efficiency, and precision, MEMS oscillators are ideal for IoT applications. They ensure accurate timing and synchronization, enhancing data accuracy and fitting IoT devices' size and power constraints. This makes them the preferred choice for manufacturers and developers. MEMS oscillators boost the reliability and performance of IoT devices, enabling seamless operations in smart homes, industrial automation, and healthcare. Their ability to meet stringent timing requirements is fueling the demand for MEMS oscillators, reflecting the expanding IoT landscape in the United States.

Automotive Industry to be the Fastest Growing End User

- Oscillators have ascended to a pivotal role in modern vehicles. Today's cars are essentially high-speed networks on wheels; without timing chips, they'd grind to a halt. Even the internet itself hinges on these crucial components. The future trajectory of semiconductors in the automotive sector is being shaped by two dominant forces: electrification and autonomous driving.

- Electrification, primarily driven by the rising adoption of hybrid and electric vehicles (EVs), is poised for a significant surge in the coming decade. According to the IEA, new electric car registrations in the United States hit 1.4 million in 2023, marking a robust 40% increase from 2022. While the growth rate in 2023 was slightly slower than the previous years, the overall demand for electric vehicles remained resilient.

- This momentum is fueled by the industry's focus on slashing battery costs, enhancing charging infrastructure, and extending the driving range of EVs. Concurrently, vehicles are getting 'smarter,' brimming with sensors and intelligent systems. This sets the stage for the second major trend: autonomous driving. These once ' luxury ' features are commonplace, from collision-avoidance systems to automatic parking and lane-change sensors, laying the groundwork for advanced driver-assistance systems (ADAS), autonomous driving, and sophisticated telematics.

- Media reports reveal that the National Highway Traffic Safety Administration (NHTSA) mandated Automatic Emergency Braking (AEB) on all new vehicles, effective 2029. Under this new regulation, all new passenger vehicles sold in the USA weighing under 10,000 lbs(4,500 kg) must be equipped with this safety technology. The US government estimates that this move could potentially save up to 400 lives annually and prevent thousands of injuries. Automakers are required to comply by September 1, 2029, with a grace period extending to low-volume manufacturers. These regulations are notably bolstering the frequency control and timing device market.

US Frequency Control and Timing Devices Industry Overview

The United States frequency control and timing devices market is fragmented, where the sustainable competitive advantage through innovation is considerable. The competition will only increase, considering the anticipated surge in demand from new customers from the end-user industries, and some of the players include Murata Manufacturing Co. Ltd, Kyocera Corporation, Rakon Limited, Microchip Technology Inc., TXC Corporation

- April 2024 - Kyocera Avx, a manufacturer of advanced electronic components, unveiled a new manufacturing and design center for high-quality, low-noise quartz crystal frequency control products under the name Kyocera Avx Components Corporation (Erie). The newly established production facility is expected to manufacture over 1.2 million patented and unparalleled low-power OCXO (oven-controlled crystal oscillators) and a range of TCXO (temperature-computed crystal oscillators) and VCXO (voltage-computed crystal oscillators).

- February 2024 - Rakon displays its initial extended holdover solution for modern radio networks and telecommunications data centers at MWC Barcelona 2024. The Error Exchange OCXO (MercuryXE2) is a version of Rakon's recently launched Mercury compact IC-OCXO. It improves the system's current synchronization abilities on a network synchronizer evaluation board by incorporating frequency error exchange processing and aging compensation, thereby increasing the holdover performance.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitutes

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Impact of COVID-19 Aftereffects and Macro Economic Trends on the Industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Adoption of 5G Augmenting the Demand for Frequency Control and Timing Devices

- 5.1.2 Rising Demand for Advanced Automotive Applications

- 5.2 Market Challenges

- 5.2.1 High Cost of Development

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Crystals

- 6.1.2 Oscillator

- 6.1.2.1 Temperature Compensated Crystal Oscillator (TCXO)

- 6.1.2.2 Voltage-controlled Crystal Oscillator (VCXO)

- 6.1.2.3 Oven-controlled Crystal Oscillator (OCXO)

- 6.1.2.4 MEMS Oscillator

- 6.1.2.5 Other Types of Oscillators

- 6.1.3 Resonators

- 6.1.4 Saw Filters

- 6.1.5 Real Time Clocks

- 6.2 By End-user Industry

- 6.2.1 Automotive

- 6.2.2 Computer and Peripherals

- 6.2.3 Communications/Server/Data Storage

- 6.2.4 Consumer Electronics

- 6.2.5 Industrial

- 6.2.6 Defense and Aerospace

- 6.2.7 IoT (Wearables, Fitness Tracker, Smart Home Devices, Smart Cities, Smart Lighting System, and Others)

- 6.2.8 Other End-user Industries (Healthcare, Oil and Gas, Agriculture, Retail, Test and Measurement, and Others)

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Murata Manufacturing Co. Ltd

- 7.1.2 Kyocera Corporation

- 7.1.3 Rakon Limited

- 7.1.4 Microchip Technology Inc.

- 7.1.5 TXC Corporation

- 7.1.6 Seiko Epson Corporation

- 7.1.7 Daishinku Corporation

- 7.1.8 Hosonic Technology (Group) Co. Ltd

- 7.1.9 Nihon Dempa Kogyo Co. Ltd

- 7.1.10 SiTime Corporation

- 7.1.11 SIWARD Crystal Technology Co. Ltd

- 7.1.12 Texas Instruments Inc.

- 7.1.13 NXP Semiconductors

- 7.1.14 Abracon LLC

- 7.1.15 CTS Corporation