|

市場調査レポート

商品コード

1549943

欧州のマネージドSD-WANサービス:市場シェア分析、産業動向・統計、成長予測(2024年~2029年)Europe Managed SD-WAN Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 欧州のマネージドSD-WANサービス:市場シェア分析、産業動向・統計、成長予測(2024年~2029年) |

|

出版日: 2024年09月02日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

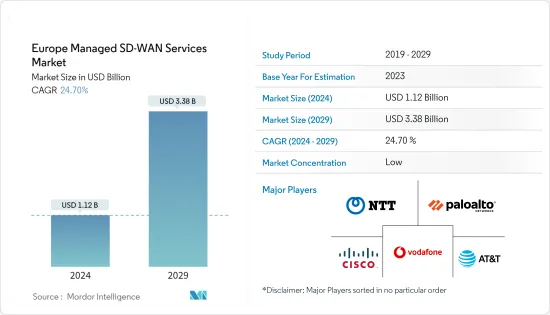

欧州のマネージドSD-WANサービス市場規模は2024年に11億2,000万米ドルと推定され、2029年には33億8,000万米ドルに達すると予測され、予測期間中(2024-2029年)のCAGRは24.70%で成長する見込みです。

欧州のマネージドSD-WANサービス市場は、現在力強い成長を遂げています。SD-WANは通信会社に、単に接続性を提供することから技術にフォーカスしたサービスプロバイダーへとシフトするチャンスを与えます。SD-WANプラットフォーム分野で重要な役割を確保することで、プロバイダはアンダーレイ、セキュリティ、LAN、UCaaS、音声サービスのリーダーとして位置づけられ、通信費管理へのスムーズな移行が可能になります。

主なハイライト

- ビジネスアプリケーションのクラウドへの大幅な移行に伴い、企業は支店のトラフィックを従来のデータセンター経由をバイパスして直接クラウドに誘導する柔軟なソリューションを求めるようになっています。AWSやMicrosoft Azureのようなクラウドプラットフォーム上で高度なSD-WANをホスティングすることで、ユーザーからクラウドサービスへのトラフィックの直接トンネルが形成され、これが容易になります。これにより、アプリケーションのパフォーマンスが向上するだけでなく、信頼性とセキュリティも強化されます。

- 高度なSD-WANソリューションにはWAN最適化機能が組み込まれています。これらの機能は、圧縮アルゴリズムと高速化されたTCPプロトコルによって、しばしば長距離によって引き起こされる遅延に対処します。さらに、これらのソリューションはSaaSアプリケーションのトラフィックを最適化します。これは、パケットロス、ジッター、遅延などのネットワーク条件を考慮して、最も効率的なルートを動的に選択することで実現します。さらに、最も近いPOP(Point of Presence)への最短パスを優先します。

- 高度なSD-WANソリューションは、BGPやOSPFなどのWAN最適化やルーティング機能以上のものを提供します。また、次世代ファイアウォール機能も組み込まれています。このような機能の統合により、企業は支店ネットワークのインフラを合理化することができます。個別のルーター、ファイアウォール、WAN最適化デバイスを単一のSD-WANデバイスに置き換えることで、企業は消費電力を節約し、管理を簡素化できます。さらに、SD-WANソリューションは仮想アプライアンスとして導入できるため、機器の設置面積とエネルギー消費量を削減できます。この統一されたアプローチはコストを削減し、異なるコンポーネントを手動で設定することで発生する可能性のあるエラーを最小限に抑えます。

- リモートワーカーは、クラウドアプリケーション、仮想デスクトップアプリ、オンプレミスソフトウェア、VoIP、SaaS(Software as a Service)など、さまざまなツールを利用しています。しかし、セキュリティの確保とネットワーク・パフォーマンスの維持は、こうしたリモート・ワーカーにとって大きな課題となります。従来のネットワークセットアップでは、リモートワークの多様な需要に対応するのに苦労することがよくありますが、SD-WANは、パブリッククラウドからでもプライベートクラウドからでも、またインターネット接続さえあれば事実上どこからでも、セキュアな接続を提供することで際立っています。その結果、リモートワークを採用する企業にとって、適切に管理されたSD-WANネットワークは重要な資産として浮上します。

- SD-WANには固有のセキュリティ機能がないため、セキュリティ管理は各プロバイダに任されています。特に、ベンダーによっては強固なセキュリティ対策を提供できない場合があります。SD-WANの重要なハードルは、セキュリティ機能を正確にカスタマイズして実装し、各ビジネスの固有の要求に合わせる必要性にあります。その結果、ITチームはサービスのデプロイメントを正確なビジネス要件に整合させることが困難になります。

欧州のマネージドSD-WANサービス市場動向

クラウドサービスの採用が市場を牽引

- 既存のクラウド利用の最適化(コスト削減)とより多くのワークロードのクラウドへの移行は、回答者の71%が強調しているように、2024年における欧州の組織にとってのクラウドへの取り組みのトップです。米国のソフトウェア会社Flexera Softwareの調査によると、回答者の61%がワークロードの自動移行を今年の重要な焦点として挙げています。

- 組織は急速にSD-WANを導入してネットワークを刷新し、支店と本社間の接続を強化しています。この急増の主な要因は、デジタルトランスフォーメーションの急速なペースとアプリケーションのクラウドプラットフォームへの移行です。堅牢で近代化されたネットワークは、マルチクラウドのフレームワークを支え、セキュリティを強化し、俊敏性を高める上で極めて重要です。逆に、不十分なネットワーク・インフラは、デジタル化のイニシアチブを妨げ、IT部門が戦略的目標と整合する妨げとなります。

- 欧州の企業は、従来のITインフラよりもクラウド・コンピューティング・サービスを選ぶ傾向が強まっています。欧州連合(EU)の統計局であるユーロスタットが2023年に報告したところによると、EU企業の45.2%がクラウドサービスを利用しています。これらのサービスは主に、電子メールシステムのホスティング、電子ファイルの保存、オフィス・ソフトウェアの実行に利用されています。特筆すべきは、これらの企業の75.3%がさらに一歩進んで、高度なクラウド・ソリューションに投資していることです。これらの高度なサービスには、セキュリティ・ソフトウェア・アプリケーション、データベース・ホスティング、アプリケーション開発・テスト・配備のためのコンピューティング・プラットフォームなどが含まれます。

- 2024年6月、ハイアール・欧州は、データ中心の企業になるために、ダイナミックなSD-WANを構築するためにOrange Businessを選択しました。Orange BusinessのEvolution Platformは、クラウド、コネクティビティ、サイバーセキュリティという3つの主要要素の調整に重点を置く。ハイアールの最初のロールアウトでは、アンダーレイとオーバーレイのオプションをハイアールのニーズに合わせて調整するために、Orange Businessのコンサルタントの指導を受けながら、汎用性の高いソフトウェア定義ワイドエリアネットワーク(SD-WAN)を特徴としています。

- クラウドサービスや分散型ネットワークへの依存度が高まる中、データのセキュリティ、機密性、完全性、コンプライアンスを確保することは極めて重要です。マネージドサービスとしてSD-WANを導入することは、ネットワークセキュリティを強化するだけでなく、このクラウド中心の状況において企業が法的義務を果たすのにも役立ちます。SD-WANをネットワークのエッジに配置することで、企業は潜在的な脅威に対するセキュリティ態勢を強化し、全体的なセキュリティ態勢をさらに強化することができます。

ドイツが大きなシェアを占める

- クラウドコンピューティングは、ドイツの企業における最新のITインフラストラクチャの要となっています。ソフトウェア、ストレージ、コンピューティング・パワーなどのITリソースをインターネット経由で提供するこの技術により、企業は業務を効率化できます。ミュンヘンを拠点とする有名な経済調査機関IFO Instituteの2023年7月時点のデータによると、ドイツ企業の46.5%がクラウド・コンピューティングを業務に組み込んでおり、さらに11.1%が計画段階にあることが明らかになった。さらに、調査対象企業の18.2%がこの技術の採用を検討しています。クラウドが様々なサイト間のセキュアで信頼性の高いスケーラブルな接続を促進することでWANパフォーマンスを向上させることを考えると、ドイツにおけるクラウドの迅速な導入は、ドイツのSD-WAN市場にとって良い兆しです。

- ドイツではクラウド技術への投資が急増しています。注目すべき動きとして、AWSは2025年末までにブランデンブルクに「ソブリンクラウド」地域を立ち上げる計画を発表しました。78億ユーロ(~97億米ドル)を超える投資に裏打ちされたこの構想は、欧州におけるデータレジデンシーを強化することを目的としています。

- COVID-19の大流行後、ドイツ企業ではリモートワークが定着しました。現在、情報部門に属する企業の80%が、少なくとも週に1回はリモートワークを行っています。ドイツのマンハイムにあるZEW-ライプニッツ欧州経済研究センターが報告しているように、伝統的にオフィス中心の製造業でさえ、この数字は45%に達しています。SD-WANは、特にクラウドベースの通信システムを活用する企業にとって、拡張性とともに堅牢なネットワークセキュリティを提供する、実行可能なソリューションとして浮上しています。

- 過去5年間、ドイツではIoTの導入が着実に増加しており、この技術が現代のビジネスシーンで極めて重要な役割を果たしていることが明らかになっています。特に、ドイツの著名なIoT接続プロバイダーであるCaburn Telecomは、リモート/スマートサービスおよびメンテナンス技術が同国で50%の採用率を誇り、世界平均の28%を上回っていると報告しています。一方、SD-WANテクノロジーは、企業がデバイスとネットワークをプログラムで管理できるようにし、以前は手作業だったオペレーションを合理化します。支店のリモートユーザーをセキュアにつなぐという役割にとどまらず、SD-WANの意義は世界ネットワーク全体のIoTデバイスを効率的に監督することにも及んでいます。この相乗効果により、SD-WANはドイツで急成長するIoTエコシステムにとって重要なイネーブラーとして位置づけられ、IoTデバイスから増大するデータ量に対応できる堅牢で安全なネットワークインフラを提供します。

- 2024年2月現在、ドイツはコロケーション・データセンター市場で欧州をリードしており、欧州大陸で最も多い522のデータセンターを誇っています。クラウド導入の急増は、AIとIoTの統合と相まって、ドイツのエスカレートするデータニーズに対応するため、ハイパースケールデータセンターの建設を検討する企業を後押ししています。SD-WANを活用することで、企業はWANをさまざまなデータセンター、支店、公開会社に容易に拡張し、手作業による介入の必要性を減らすことができます。さらに、SD-WANはパフォーマンスを向上させるだけでなく、クラウドベースやSaaSアプリケーションを利用する企業のオペレーションを合理化し、これらのプラットフォームへの直接接続を提供します。その結果、この動向はこの地域におけるSD-WANソリューションの需要を促進しています。

欧州のマネージドSD-WANサービス産業の概要

欧州のマネージドSD-WANサービス市場は本質的に断片化されています。調査対象となった市場の主なプレイヤーには、Cisco Systems Inc.、Vodafone Group PLC、NTT Limited、Palo Alto Networksがいます。同市場のプレーヤーは、サービス提供を強化し、持続可能な競争優位性を獲得するために、提携、契約、イノベーション、買収などの戦略を採用しています。

- 2024年5月:Hughes社はNetskope社と提携し、顧客にSASEソリューションを提供。このソリューションはHughesのマネージドSD-WANサービスとNetskopeの有名なセキュアサービスエッジ(SSE)ソリューションを統合したものです。SASEは革新的なネットワークアーキテクチャで、SD-WANとSSEを単一のクラウドサービスに統合します。この統合は、効率性とセキュリティの両方を強化しながら、WANデプロイメントを合理化することを目的としています。

- 2024年2月VMwareは、VeloCloud SD-WANとSymantec SSEを統合した統合SASEソリューションであるVMware VeloCloud SASEを発表しました。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- COVID-19からの回復の評価とマクロ経済動向の影響

第5章 市場力学

- 市場促進要因

- 社内ノウハウの不足が、マネージドネットワークサービスを選択する原動力に

- コアオペレーションとコスト効率に集中するメリット

- さまざまな業界におけるデジタルトランスフォーメーションとネットワークトラフィックの急増

- 市場の課題

- 主要業務のアウトソーシングに消極的な企業

- テクノロジー情勢

- ケーススタディ分析

第6章 市場セグメンテーション

- 組織規模別

- 中小企業

- 大企業

- エンドユーザー別

- BFSI

- IT・通信

- ヘルスケア

- 小売・eコマース

- 製造業

- その他エンドユーザー

- 国別

- 英国

- ドイツ

- フランス

- イタリア

- ベネルクス連合

- その他欧州

第7章 競合情勢

- 企業プロファイル

- Cisco Systems Inc.

- Vodafone Group PLC

- NTT Limited

- Palo Alto Networks

- AT&T

- Verizon Communications Inc.

- BT Group PLC

- Nokia Corporation

- Telstra

- Deutsche Telekom AG

- Fortinet Inc.

第8章 市場機会と今後の動向

The Europe Managed SD-WAN Services Market size is estimated at USD 1.12 billion in 2024, and is expected to reach USD 3.38 billion by 2029, growing at a CAGR of 24.70% during the forecast period (2024-2029).

The European managed SD-WAN services market is currently experiencing robust growth. SD-WAN presents telecommunication firms with a chance to shift from merely offering connectivity to becoming technology-focused service providers. Securing a prominent role in the SD-WAN platform arena positions providers as leaders in underlay, security, LAN, UCaaS, and voice services and facilitates a smooth transition into telecom expense management.

Key Highlights

- With the significant migration of business applications to the cloud, organizations are increasingly seeking flexible solutions to direct branch office traffic to the cloud directly, bypassing the traditional route through the data center. Hosting an advanced SD-WAN on cloud platforms such as AWS or Microsoft Azure facilitates this, creating a direct tunnel for traffic from users to cloud services. This not only enhances application performance but also bolsters reliability and security.

- Advanced SD-WAN solutions incorporate WAN optimization features. These features combat latency, often caused by long distances, through compression algorithms and accelerated TCP protocols. Additionally, these solutions optimize SaaS application traffic. They achieve this by dynamically choosing the most efficient route, factoring in network conditions like packet loss, jitter, and latency. Furthermore, they prioritize the shortest path to the nearest point of presence (POP).

- Advanced SD-WAN solutions offer more than WAN optimization and routing features, such as BGP and OSPF. They also incorporate next-generation firewall capabilities. This consolidation of features allows organizations to streamline their branch network infrastructure. By replacing separate routers, firewalls, and WAN optimization devices with a single SD-WAN device, organizations save on power consumption and benefit from simplified management. Additionally, SD-WAN solutions can be deployed as virtual appliances, reducing equipment footprint and energy consumption. This unified approach cuts costs and minimizes errors that can arise from manually configuring disparate components.

- Remote workers utilize a range of tools, including cloud applications, virtual desktop apps, on-premises software, VoIP, and Software as a Service (SaaS). However, ensuring security and maintaining network performance pose significant challenges for these remote employees. While traditional network setups often struggle to keep pace with the diverse demands of remote work, SD-WAN stands out by providing secure connectivity, whether from public or private clouds and that too, from virtually anywhere with just an internet connection. Consequently, for companies embracing remote workforces, a well-managed SD-WAN network emerges as a critical asset.

- SD-WAN lacks inherent security features, leaving security management to individual providers. Notably, some vendors may fall short of providing robust security measures. A key hurdle with SD-WAN lies in the necessity to tailor and implement security features accurately, aligning them with each business's unique demands. Consequently, IT teams encounter difficulties in aligning service deployments with precise business requisites.

Europe Managed SD-WAN Services Market Trends

Increased Adoption of Cloud Services to Drive the Market

- Optimizing the existing use of clouds (cost savings) and migrating more workloads to the cloud are the top cloud initiatives for European organizations in 2024, as highlighted by 71% of respondents. Following closely, 61% of respondents have highlighted automated workload migration as a significant focus for the year, according to a survey by Flexera Software, a US-based Software company.

- Organizations are rapidly embracing SD-WAN to revamp their networks, enhancing connectivity between branch offices and headquarters. This surge is primarily fueled by the rapid pace of digital transformation and the migration of applications to cloud platforms. A robust, modernized network is pivotal in underpinning multi-cloud frameworks, bolstering security, and enhancing agility. Conversely, an inadequate network infrastructure hampers digitization initiatives and hinders IT departments from aligning with strategic objectives.

- European enterprises are increasingly opting for cloud computing services over traditional IT infrastructure. In 2023, as reported by Eurostat, the statistical office of the European Union, 45.2% of EU enterprises utilized cloud services. These services were primarily used for hosting e-mail systems, storing electronic files, and running office software. Notably, 75.3% of these enterprises went a step further, investing in advanced cloud solutions. These sophisticated services encompassed security software applications, database hosting, and computing platforms tailored for application development, testing, and deployment.

- In June 2024, Haier Europe, in its push to become a data-centric enterprise, selected Orange Business to construct a dynamic SD-WAN. Orange Business's Evolution Platform will focus on coordinating three key elements: cloud, connectivity, and cybersecurity. Haier's initial rollout features a versatile software-defined wide area network (SD-WAN), with guidance from Orange Business consultants to tailor underlay and overlay options to Haier's needs.

- With businesses relying more on cloud services and distributed networks, ensuring data security, confidentiality, integrity, and compliance is crucial. Deploying SD-WAN as a managed service not only enhances network security but also helps companies meet their legal obligations in this Cloud-centric landscape. By positioning SD-WAN at the network's edge, organizations can bolster their security posture against potential threats, further fortifying their overall security stance.

Germany to Hold to a Major Share

- Cloud computing has become a cornerstone of modern IT infrastructure in German enterprises. This technology, which provides IT resources like software, storage, and computing power over the Internet, enables companies to streamline their operations. Data from the Munich-based IFO Institute, a renowned economic research entity, as of July 2023, revealed that 46.5% of German companies integrated cloud computing into their operations, with an additional 11.1% in the planning stages. Moreover, 18.2% of surveyed companies are deliberating the adoption of this technology. Given that the cloud enhances WAN performance by facilitating secure, reliable, and scalable connections across various sites, its swift uptake in Germany bodes well for the country's SD-WAN market.

- Germany is experiencing a surge in cloud technology investments. In a notable move, AWS announced its plans for a 'sovereign cloud' region in Brandenburg, set to launch by the close of 2025. This initiative, backed by an investment exceeding EUR 7.8 billion (~USD 9.70 billion), aims to bolster data residency in Europe.

- After the COVID-19 pandemic, remote work entrenched itself as a permanent feature in German firms. Presently, 80% of companies in the information sector have their staff working remotely at least once a week. Even in the traditionally office-centric manufacturing sector, this figure is at 45%, as reported by The ZEW - Leibniz Centre for European Economic Research in Mannheim, Germany. SD-WAN emerges as a viable solution, especially for firms leveraging cloud-based communication systems, offering robust network security alongside scalability.

- Over the past five years, Germany has witnessed a steady rise in IoT adoption, underscoring the technology's pivotal role in contemporary business landscapes. Notably, Caburn Telecom, a prominent IoT connectivity provider in Germany, reports that remote/smart service and maintenance technologies boast a 50% adoption rate in the country, surpassing the global average of 28%. Meanwhile, SD-WAN technology empowers businesses to programmatically manage their devices and networks, streamlining operations that were previously manual. Beyond its role in securely linking remote users at branch offices, SD-WAN's significance extends to efficiently overseeing IoT devices across global networks. This synergy positions SD-WAN as a crucial enabler for the burgeoning IoT ecosystem in Germany, offering a robust and secure network infrastructure capable of handling the escalating data deluge from IoT devices.

- As of February 2024, Germany led Europe in colocation data center markets, boasting 522 data centers, the highest count in the continent. The surge in cloud adoption, coupled with the integration of AI and IoT, is propelling businesses to consider constructing hyperscale data centers to cater to Germany's escalating data needs. Leveraging SD-WAN, companies effortlessly extend their WANs to various data centers, branches, and public clouds, reducing the need for manual interventions. Furthermore, SD-WAN not only enhances performance but also streamlines operations for businesses utilizing cloud-based and SaaS applications, offering them direct connectivity to these platforms. Consequently, this trend is fueling the demand for SD-WAN solutions in the region.

Europe Managed SD-WAN Services Industry Overview

The European managed SD-WAN services market is fragmented in nature. Some major players in the market studied are Cisco Systems Inc., Vodafone Group PLC, NTT Limited, and Palo Alto Networks. Players in the market are adopting strategies such as partnerships, agreements, innovations, and acquisitions to enhance their service offerings and gain sustainable competitive advantage.

- May 2024: Hughes collaborated with Netskope to offer customers a SASE solution. This solution merges Hughes' managed SD-WAN services with Netskope's renowned secure service edge (SSE) solutions. SASE, an innovative network architecture, unifies SD-WAN and SSE into a single cloud service. This integration aims to streamline WAN deployments while enhancing both efficiency and security.

- February 2024: VMware introduced the VMware VeloCloud SASE, a unified SASE solution that merges VeloCloud SD-WAN with Symantec SSE.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definitions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 An Assessment of the Recovery From COVID-19 and the Impact of Macroeconomic Trends

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Lack of In-house Expertise Driving Organizations to Opt for Managed Network Services

- 5.1.2 Benefit of Extensive Focus on Core Operations and Cost-efficiency

- 5.1.3 Rapidly Growing Digital Transformation and Network Traffic in Various Industries

- 5.2 Market Challenges

- 5.2.1 Organizations Remain Reluctant to Outsource Key Operations

- 5.3 Technology Landscape

- 5.4 Case Study Analysis

6 MARKET SEGMENTATION

- 6.1 By Organization Size

- 6.1.1 Small and Medium Enterprises

- 6.1.2 Large Enterprises

- 6.2 By End User

- 6.2.1 BFSI

- 6.2.2 IT and Telecom

- 6.2.3 Healthcare

- 6.2.4 Retail and E-commerce

- 6.2.5 Manufacturing

- 6.2.6 Other End Users

- 6.3 By Country

- 6.3.1 United Kingdom

- 6.3.2 Germany

- 6.3.3 France

- 6.3.4 Italy

- 6.3.5 Benelux Union

- 6.3.6 Rest of Europe

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Cisco Systems Inc.

- 7.1.2 Vodafone Group PLC

- 7.1.3 NTT Limited

- 7.1.4 Palo Alto Networks

- 7.1.5 AT&T

- 7.1.6 Verizon Communications Inc.

- 7.1.7 BT Group PLC

- 7.1.8 Nokia Corporation

- 7.1.9 Telstra

- 7.1.10 Deutsche Telekom AG

- 7.1.11 Fortinet Inc.