アウトソーシングサービス-市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

Outsourcing Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 198 Pages

- 納期

- 2~3営業日

- 商品コード

- 1694041

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

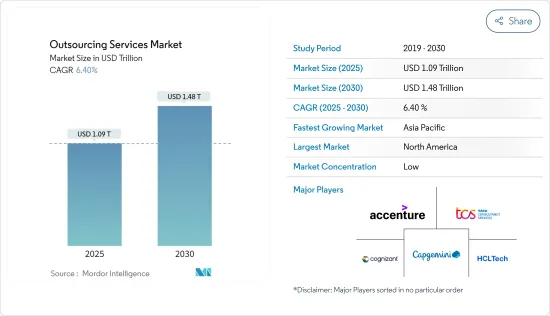

アウトソーシングサービス市場規模は2025年に1兆900億米ドルと推定され、予測期間(2025~2030年)のCAGRは6.4%で、2030年には1兆4,800億米ドルに達すると予測されます。

運用コストの最小化重視の高まり、熟練労働力の不足、アウトソーシングサービスへの先端技術の導入といった要因が、市場シェアを獲得するために各社が新たなサービスを開発することを後押ししています。同市場は予測期間中に大幅な成長が見込まれます。

主要ハイライト

- さまざまな要因から、アウトソーシングサービスを利用する企業が増えています。主要因の1つは、人件費の安い国にアウトソーシングすることでコスト削減が見込めることで、給与、福利厚生、間接費に関連する経費を大幅に削減できます。さらに、企業は資源と経営努力を中核となる事業活動に集中させることで、競合を高め、成長を促進しています。

- 市場参入企業は顧客基盤を拡大するため、欧州でさまざまなアウトソーシング企業を買収しています。例えば、カスタマーエクスペリエンスサービスの世界の参入企業であるKonectaは、2024年2月、英国を拠点とするビジネスプロセスアウトソーシング企業Bespokeを買収し、英語圏市場でのプレゼンスを強化しました。ビスポークの主要生産施設は南アフリカのダーバンにあります。

- さらに、Konectaはテキサス州サンアントニオ(米国)にオペレーションセンターを開設し、英語サービスを拡大しました。これらの戦略的動きは、Konectaの広範な地理的拡大戦略に沿ったものであり、特にオフショアリングサービスにおいて、英語圏の顧客へのサービスを充実させるものです。これらの拡大により、Konectaは産業における重要な参入企業としての地位を固めつつあります。

- さらに、ビジネスプロセスアウトソーシングにおけるクラウドコンピューティングの人気の高まりは、BPOサービスの採用に大きな影響を与えています。クラウドコンピューティングは、BPO事業者が市場投入までの時間を短縮し、コストを削減し、品質管理プロセスを強化するのに役立っています。

- さらに、市場におけるクラウドコンピューティングは、瞬時のコンピューティングサポートとシステムキー、ユニバーサル・アクセス、必要なビジネス目的に応じていつでも調整可能なプロビジョニングを保証します。これらの利点は、予測期間中、ビジネスプロセスアウトソーシングセグメントにおけるクラウドコンピューティングの全体的な導入にプラスの影響を与えると予想されます。

- しかし、データセキュリティ、カスタマイズ、データ移行に関する懸念、IT構造のダイナミックなニーズ、エンドユーザーのカスタマイズコストへの影響などが、予測期間中の市場成長の妨げになると見られています。

アウトソーシングサービス市場の動向

情報技術アウトソーシングセグメントが著しい成長を遂げる

- 同市場では、非中核業務のアウトソーシングによってコアコンピタンスを活用することに重点が置かれるようになり、アウトソーシングベンダーに依存することで差別化を図り、クラウドサービスへの移行を継続し、仮想化インフラを採用することで、ITに対する組織の関心が高まっています。さらに、デジタルトランスフォーメーションが重視されるようになったため、組織はITサービスが提供できる創造的なアプリケーションや拡大機能のパフォーマンスに依存しています。

- そのため、企業や組織の間では、自社の中核となる強みや重要な機能を優先する一方で、重要でないIT業務は外部のサービスプロバイダにアウトソーシングするという戦略的転換が進んでいます。この動向は、企業の競争優位性とビジネス全体の成長に直接貢献する活動に、社内のリソースと専門知識を集中させることの重要性を認識しています。

- このシフトの背景にある主要因の1つは、コアコンピテンシーに集中することの重要性を認識していることです。企業は、自社のリソースや専門知識への投資をますます具体化し、競争優位に直接貢献する活動に配分するようになっています。非中核的なIT業務をアウトソーシングすることで、企業はイノベーション、製品開発、顧客中心の取り組みに関心とリソースを振り向けることができ、市場でのポジショニングと俊敏性が高まっている

- さらに、中小企業が先端技術を導入するための投資が増加していることから、中小企業セクタの市場拡大が見られます。これらの要因により、ITアウトソーシング・ベンダーは今後数年間で大きな成長機会を得ることができると予想されます。

- 例えば、2023年5月、英国の3大学がHNCDI(Hartree National Centre for Digital Innovation)プログラムの下、中小企業(SME)エンゲージメントハブ設立のため、総額450万英ポンドを受け取りました。ニューカッスル大学、アルスター大学、カーディフ大学は、スーパーコンピューティング、データ分析、ビジュアルコンピューティング、人工知能(AI)などの先進的デジタル技術を導入することで、中小企業の競合と成長を高めるために、的を絞った利用しやすい支援を提供することが期待されています。

- さらに、クラウド導入の増加は、スケーラブルでコスト効率に優れ、柔軟なソリューションを提供することで、ITアウトソーシング市場の成長を大きく後押ししています。フレクセラソフトウェアによると、2024年時点で、調査対象となった企業の73%がハイブリッドクラウドを導入しています。企業はインフラコストを削減し、俊敏性を向上させるためにクラウドサービスを活用するようになっています。このシフトにより、ITアウトソーシングプロバイダは、クラウド管理、統合、セキュリティに特化したサービスを提供できるようになりました。

- その結果、企業は複雑なIT業務をアウトソーシングしながら、中核業務に集中することができます。クラウドの専門知識に対する需要がITアウトソーシングの成長を後押ししています。これは、企業が社内の大規模なリソースを必要とせずにクラウド技術の利点を活用しようとするためです。この動向は、産業全体のイノベーションと業務効率を加速させています。

北米が大きな市場シェアを占める

- 米国は北米アウトソーシングサービス市場で重要な地位を占めています。同地域のハイテク大手によるビジネスプロセスアウトソーシングサービスの需要が高まっていることから、同地域の優位性は今後も維持される展望です。また、クラウドコンピューティングの需要が急増していることや、個々のニーズに対応したサービスの個別化が進んでいることも、同地域の拡大を後押しするとみられます。

- カナダの多くの会社は、パブリッククラウドサービスだけに依存することから移行しつつあります。その代わりに、パブリック、プライベート、従来のインフラを融合させたハイブリッドITのアプローチを採用しています。このシフトは、ハイブリッドクラウド戦略を通じて業務と顧客サービスを強化することにメリットを見出す企業によって推進されています。カナダ政府は「クラウドファースト」のアプローチに基づき、IT投資、技術、プロジェクトにおいてクラウドサービスを優先しています。民間企業のイノベーションを活用することで、政府はITインフラの俊敏性を高めることを目指しています。このような政府のIT開発への取り組みは、市場の成長を促進すると期待されています。

- さらに、北米で事業を展開する企業は、アウトソーシングプロセスにAI(人工知能)や自動化技術を組み込む傾向を強めています。この動向は、効率を高め、手作業の介入を最小限に抑えることを目的としています。アウトソーシングにおけるAIと自動化の採用は着実に増加しています。企業はAI、RPA(ロボティックプロセスオートメーション)、機械学習を活用し、業務の合理化、効率化、経費削減に取り組んでいます。これを受けて、アウトソーシングサービスプロバイダはAIを中心としたソリューションに軸足を移し、よりスマートなデータ主導洞察力でサービスを充実させています。

- この地域では、さまざまな企業がBPOサービスにAIを活用しています。例えば、Expiviaは、技術とAIを優先することで、BPOサービスの展望を再構築しました。従来のベンチマークだけに頼るのではなく、同社は技術主導の戦略を優先し、顧客が戦略的価値を得られるようにしています。

- また、大企業は、より良いバックエンドITサポートとITインフラ更新のためにITアウトソーシング戦略を採用する傾向が強まっており、これが米国での市場成長を促進すると考えられます。例えば、タタコンサルタンシー・サービシズ(TCS)は2023年7月、米国を拠点とする医療技術企業GE Healthcare技術社との関係を拡大し、同社のアプリケーション管理とイノベーション推進のためのITオペレーティングモデルの変革を支援しました。今回の提携により、TCSはGE HealthcareのITアプリケーション開拓、保守、合理化、標準化などのアウトソーシングサービスを提供し、同国の大企業向け市場の成長をサポートすることになります。

アウトソーシングサービス産業概要

アウトソーシングサービス市場は、さまざまなベンダーのサービスによって半固定化されています。主要ベンダーは、Accenture、TATA Consultancy Services Limited、キャップジェミニ、コグニザント、HCL Technologies Limitedなどです。市場参入企業は、戦略的パートナーシップや革新的な製品の提供を通じて、ポートフォリオを強化し、長期的な競争優位性を追求しています。

2024年3月、セレジェンス・ホールディングス・エルエルシーは、医薬品の安全性とメディカル・アフェアーズ領域におけるアウトソーシングサービス、コラボレーション技術、データ資産の主要企業であるソテリウス社に戦略的投資を行りました。今回の投資は、ソテリウス社のシリーズA資金調達の一環であり、セレジェンス社とソテリウス社双方の強みを生かしたパートナーシップを築きました。両社のチームの専門知識を活用することで、この提携は両社のリーチを広げ、相互の成長を促進することを目的としています。

2024年1月、デジタル技術企業のVaranium Cloud Limitedは、マハラシュトラ州サワントワディに2つ目のオフィスとビジネスプロセスアウトソーシング(BPO)センターを設立します。このBPOセンターは、データ会計、身元確認、債権回収などのサービスに特化します。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- アウトソーシングサービス市場の規制状況

第5章 市場力学

- 市場の促進要因

- クラウドへの移行の進行と仮想化インフラの採用

- 効率性と拡大性に対する需要の高まり

- モノのインターネットによるBPOサービスの効率化

- 市場抑制要因

- データセキュリティ、カスタマイズ、データ移行

- IT構造のダイナミックなニーズがエンドユーザーのカスタマイズコストに影響

- アウトソーシングサービス市場の主要技術動向

第6章 市場セグメンテーション

- サービスタイプ別

- ビジネスプロセスアウトソーシング

- 情報技術アウトソーシング

- 人的資源アウトソーシング

- ナレッジプロセスアウトソーシング

- その他

- 地域別

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- アイルランド

- スウェーデン

- アジア

- 中国

- インド

- 日本

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- 南アフリカ

- 北米

第7章 競合情勢

- 企業プロファイル

- Accenture PLC

- Tata Consultancy Services Limited

- Capgemini SE

- Cognizant Technology Solutions Corporation

- HCL Technologies Ltd

- Teleperformance SE

- Evelyn Partners Group Limited

- Thomson Reuters Corporation

- TTEC Holdings Inc.

- Trinitar Solutions LLP

- Amdocs Limited

- Infosys Bpm(Infosys Limited)

- Automatic Data Processing Inc.

- General Outsourcing Public Company Limited

- Concentrix Corporation

第8章 投資分析

第9章 市場機会と将来展望

目次

The Outsourcing Services Market size is estimated at USD 1.09 trillion in 2025, and is expected to reach USD 1.48 trillion by 2030, at a CAGR of 6.4% during the forecast period (2025-2030).

Factors such as the rising emphasis on minimizing operational expenses, the unavailability of a skilled workforce, and the incorporation of advanced technology in outsourcing services are propelling players to develop new services to capture market share. The market is expected to witness significant growth during the forecast period.

Key Highlights

- Organizations are increasingly turning to outsourcing services, driven by various factors. One major factor is the cost-saving potential when outsourcing to countries with lower labor costs, which can lead to substantial reductions in expenses related to salaries, benefits, and overheads. Additionally, companies are focusing their resources and management efforts on core business activities, enhancing their competitive edge and fostering growth.

- The market players are acquiring various outsourcing firms in the European region to expand their customer base. For instance, in February 2024, Konecta, a global player in Customer Experience services, bolstered its presence in English-speaking markets by acquiring Bespoke, a United Kingdom-based business process outsourcing firm. Bespoke's primary production facilities are in Durban, South Africa.

- Additionally, Konecta expanded its English services by launching its inaugural operations center in San Antonio, Texas (USA). These strategic moves align with Konecta's broader geographic expansion strategy, enriching its offerings for English-speaking clients, notably in offshoring services. With these expansions, Konecta is solidifying its standing as a critical player in the industry.

- Moreover, the growing popularity of cloud computing in business process outsourcing is a significant factor affecting the adoption of BPO services. Cloud computing aids BPO operators in improving the time to market, reducing costs, and enhancing the quality control process.

- Furthermore, cloud computing in the market ensures instant computing support and system keys, universal access, and adjustable provisioning whenever needed for required business purposes. These advantages are expected to positively impact the overall adoption of cloud computing in the business process outsourcing sector during the forecast period.

- However, concerns related to data security, customization, and data migration, coupled with the dynamic needs of the IT structure, impacting the cost of customization for end users, are poised to hamper market growth during the forecast period.

Outsourcing Services Market Trends

The Information Technology Outsourcing Segment to Witness Significant Growth

- The market is witnessing a rising emphasis on leveraging the core competencies by outsourcing non-core operations, increasing organizations' focus on IT to gain differentiation by relying on outsourced vendors, continuing the shift to cloud services, and embracing virtualized infrastructure. Moreover, due to the growing emphasis on digital transformation, organizations depend on the performance of creative applications and extensions that IT services can provide.

- Hence, there is a strategic shift among businesses and organizations to prioritize their core strengths and critical functions while outsourcing non-essential IT operations to external service providers. This trend recognizes the importance of focusing internal resources and expertise on activities directly contributing to a company's competitive advantage and overall business growth.

- One of the primary drivers behind this shift is recognizing the critical importance of focusing on core competencies. Businesses are increasingly specific about investments in their resources and expertise, allocating them to activities directly contributing to their competitive advantage. Outsourcing non-core IT operations allows organizations to divert their attention and resources toward innovation, product development, and customer-centric efforts, enhancing their market positioning and agility.

- Further, the market is witnessing an expansion in the SME sector due to the rising investments in SMEs to adopt advanced technologies. These factors are further expected to create substantial growth opportunities for IT outsourcing vendors in the coming years.

- For instance, in May 2023, three UK universities collectively received GBP 4.5 million to establish small and medium-sized enterprise (SME) engagement hubs under the HNCDI (Hartree National Centre for Digital Innovation) program. Newcastle University, Ulster University, and Cardiff University are expected to provide targeted and accessible help for SMEs to boost their competitiveness and growth by adopting advanced digital technologies such as supercomputing, data analytics, visual computing, and artificial intelligence (AI).

- Furthermore, rising cloud deployment is significantly augmenting the growth of the IT outsourcing market by offering scalable, cost-effective, and flexible solutions. According to Flexera Software, as of 2024, 73% of enterprises surveyed implement a hybrid cloud in their organizations. Businesses increasingly leverage cloud services to reduce infrastructure costs and improve agility. This shift enables IT outsourcing providers to offer specialized cloud management, integration, and security services.

- Consequently, organizations can focus on core activities while outsourcing complex IT tasks. The demand for cloud expertise drives IT outsourcing growth as companies seek to harness cloud technology's benefits without the need for extensive in-house resources. This trend accelerates innovation and operational efficiency across industries.

North America to Hold a Significant Market Share

- The United States holds a significant position in the North American outsourcing services market. Due to the growing demand for business process outsourcing services from the region's tech giants, the region is expected to maintain its dominance. The surge in the overall demand for cloud computing and the personalization of service offerings to better meet individual needs are also expected to drive regional expansion.

- Many Canadian companies are transitioning from solely relying on public cloud services. Instead, they are embracing a hybrid IT approach, blending public, private, and traditional infrastructure. This shift is driven by the benefits these organizations see in enhancing their operations and customer service through a hybrid cloud strategy. In line with its "cloud-first" approach, the Canadian government prioritizes cloud services for IT investments, techniques, and projects. By leveraging private-sector innovations, the government aims to enhance the agility of its IT infrastructure. Such government initiatives toward IT development are expected to drive market growth.

- Moreover, businesses operating within North America are increasingly integrating AI (artificial intelligence) and automation technologies into their outsourcing processes. This trend aims to boost efficiency and minimize manual intervention. The adoption of AI and automation in outsourcing is on a steady rise. Companies are turning to AI, RPA (Robotic Process Automation), and machine learning to streamline operations, enhance efficiency, and reduce expenses. In response, outsourcing service providers are pivoting toward AI-centric solutions, enriching their services with smarter, data-driven insights for clients.

- Various players in the region are using AI in BPO services. For instance, Expiviahas reshaped the landscape of BPO services by prioritizing technology and AI. Rather than relying solely on conventional benchmarks, the company prioritizes technology-driven strategies, ensuring its clients derive strategic value.

- Also, large enterprises are increasingly adopting IT outsourcing strategies for better backend IT support and IT infrastructure updates, which would drive market growth in the United States. For instance, in July 2023, Tata Consultancy Services (TCS) expanded its relationship with GE HealthCare Technologies Inc., a medical technology company based in the United States, to help transform its IT operating model for managing its applications and driving innovation. After this collaboration, TCS would provide outsourcing services for IT application development, maintenance, rationalization, and standardization of GE Healthcare, supporting the growth of the market in the country's large enterprise sector.

Outsourcing Services Industry Overview

The outsourcing services market is semi-consolidated with an array of services from various vendors. Major vendors include Accenture, TATA Consultancy Services Limited, Capgemini, Cognizant, and HCL Technologies Limited. Market players are enhancing their portfolios and seeking long-term competitive advantages through strategic partnerships and innovative product offerings.

In March 2024, Celegence Holdings LLC strategically invested in Soterius Inc., a key player in outsourced services, collaboration technologies, and data assets within the drug safety and medical affairs domain. This investment, a part of Soterius' Series A financing, has forged a partnership that capitalizes on the strengths of both Celegence and Soterius. By leveraging the expertise of their teams, this collaboration aims to broaden their reach and fuel mutual growth.

In January 2024, Varanium Cloud Limited, a digital technology company, is establishing its second office and business process outsourcing (BPO) center in Sawantwadi, Maharashtra. The BPO center would specialize in services such as data accounting, background verification, and debt recovery.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Regulatory Landscape of Outsourcing Services Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Ongoing Migration Toward the Cloud and Adoption of Virtualized Infrastructure

- 5.1.2 Growing Demand for Efficiency and Scalable IT Infrastructure

- 5.1.3 Internet of Things for Efficient Delivery of BPO Services

- 5.2 Market Restraints

- 5.2.1 Data Security, Customization, and Data Migration

- 5.2.2 Dynamic Needs of IT Structure Impacts the Cost of Customization for End Users

- 5.3 Key Technological Trends in Outsourcing Services Market

6 MARKET SEGMENTATION

- 6.1 By Service Type

- 6.1.1 Business Process Outsourcing

- 6.1.2 Information Technology Outsourcing

- 6.1.3 Human Resource Outsourcing

- 6.1.4 Knowledge Process Outsourcing

- 6.1.5 Other Service Types

- 6.2 By Geography

- 6.2.1 North America

- 6.2.1.1 United States

- 6.2.1.2 Canada

- 6.2.2 Europe

- 6.2.2.1 United Kingdom

- 6.2.2.2 Germany

- 6.2.2.3 France

- 6.2.2.4 Ireland

- 6.2.2.5 Sweden

- 6.2.3 Asia

- 6.2.3.1 China

- 6.2.3.2 India

- 6.2.3.3 Japan

- 6.2.4 Latin America

- 6.2.4.1 Brazil

- 6.2.4.2 Mexico

- 6.2.5 Middle East and Africa

- 6.2.5.1 United Arab Emirates

- 6.2.5.2 Saudi Arabia

- 6.2.5.3 South Africa

- 6.2.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Accenture PLC

- 7.1.2 Tata Consultancy Services Limited

- 7.1.3 Capgemini SE

- 7.1.4 Cognizant Technology Solutions Corporation

- 7.1.5 HCL Technologies Ltd

- 7.1.6 Teleperformance SE

- 7.1.7 Evelyn Partners Group Limited

- 7.1.8 Thomson Reuters Corporation

- 7.1.9 TTEC Holdings Inc.

- 7.1.10 Trinitar Solutions LLP

- 7.1.11 Amdocs Limited

- 7.1.12 Infosys Bpm (Infosys Limited)

- 7.1.13 Automatic Data Processing Inc.

- 7.1.14 General Outsourcing Public Company Limited

- 7.1.15 Concentrix Corporation

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 198 Pages

- 納期

- 2~3営業日