|

市場調査レポート

商品コード

1549858

液体用板紙の世界市場:市場シェア分析、産業動向・統計、成長予測(2024年~2029年)Liquid Paperboard - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 液体用板紙の世界市場:市場シェア分析、産業動向・統計、成長予測(2024年~2029年) |

|

出版日: 2024年09月02日

発行: Mordor Intelligence

ページ情報: 英文 140 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

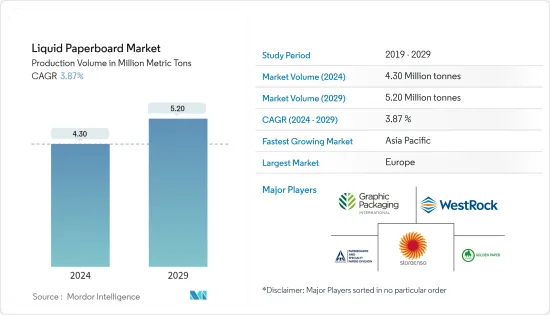

生産量ベースの世界の液体用板紙市場規模は、2024年の430万トンから2029年には520万トンに拡大し、予測期間(2024年~2029年)のCAGRは3.87%と予測されます。

主なハイライト

- 液体用板紙(LPB)は汎用性が高く持続可能な包装材料であり、主に飲食品業界で使用されています。板紙は、ポリエチレンやその他のバイオポリマーなど、様々なバリア材料でコーティングされた層で構成され、保護性を高めています。この多層構造は、堅牢な物理的保護と水分、酸素、光に対する効果的なバリアを提供し、牛乳、ジュース、スープ、ソースなどの液体製品の包装に理想的です。

- 液体用板紙は、その持続可能性とバリア性により、液体用カートンの包装に広く使用されています。メーカー各社は、ミニマリスト的でデザイン性の高いアプローチを採用し、一人分に対応する小型パックを作ることで、材料の使用量と廃棄量を削減しています。こうしたコンパクトなデザインは消費者の利便性を高め、包装に伴う二酸化炭素排出量を最小限に抑えることで環境への責任を促進します。

- バリアコーティングの技術的発展が、液体用板紙の開発・強化の主な原動力となっています。バイオベースや生分解性材料を含む革新的なコーティング技術は、環境への影響を最小限に抑えながらLPBの性能を向上させるために開発されています。これらのコーティングは、汚染や腐敗を防ぐことで包装製品の保存期間や品質を向上させるだけでなく、持続可能な包装を求める消費者や規制の高まりにも合致しています。例えば、ナノテクノロジーの進歩により、極薄でありながら非常に効果的なバリア層を作ることが可能になり、LPBに塗布することで、重量やコストを大幅に増加させることなく機能性を向上させることができるようになりました。

- しかし、液体用板紙は板紙とポリエチレンの複合材料であるため、リサイクルには課題があります。既存のリサイクル・インフラでは、これらの層を分離するのに手助けが必要な場合が多く、効率的なリサイクル・プロセスの妨げとなっています。この複雑さにより、液体用板紙を効果的に処理し、持続可能性を向上させるためのリサイクル技術やシステムの進歩が必要となっています。

液体用板紙の市場動向

飲料セグメントの需要増加が市場を押し上げる

- 飲料分野からの需要の高まりが、液体用板紙市場を大きく押し上げています。包装メーカーや消費者ブランドは、プラスチックやガラスのような他の材料と比較して、より少ない原材料を使用し、より少ない廃棄物を生成し、コスト削減を提供することができるため、ますます液体用板紙を選択しています。液体用板紙を利用することで、企業はより軽量で持続可能な包装を製造することができ、輸送コストを削減し、環境への影響を最小限に抑えることができます。この効率性は、包装の容積や重量が物流全体やカーボンフットプリントに大きな影響を与える飲料業界では特に有益です。

- プレミアム液体包装用板紙は、コスト効率に優れ、卓越した製品保護を実現し、飲料の鮮度と安全性を保証します。これらの板紙は、優れた印刷、加工、充填性能を備えており、ブランドは高品質の基準と視覚的に魅力的なデザインを維持することができます。この機能性と美観の組み合わせにより、液体用板紙は、ジュース、スープ、水、ヨーグルトなどの飲料業界の包装用途に魅力的な選択肢となっています。水分、酸素、光に対する強力なバリア機能を備えているため、これらの製品の保存期間と品質がさらに向上し、液体用板紙はメーカーに好まれる素材となっています。

- 液体用板紙の持続可能性と効率をさらに高めるため、Stora Ensoのような企業は、使用済み飲料用カートンの循環性を高めるために多額の投資を行っています。StoraEnsoは、材料効率の改善と、液体用板紙の性能を高める革新的なソリューションの開発に注力しています。このような進歩のひとつに、軽量化しながら板紙を強化する微小繊維化セルロース(MFC)の採用があります。この改良により、必要な原材料の量が減り、包装の耐久性と機能性が向上し、他のフォーマットに対する競争力が高まります。

- 乳製品、豆乳、ジュース、果実ベースのレモネード、非炭酸水などの長寿命の液体製品用の飲料用カートンは、さらに箔ラミネート加工が施されています。この薄いアルミ層は、光と酸素から飲料を保護します。アルミニウム層の厚さはわずか6.5マイクロメートルで、髪の毛の4分の1にも満たない薄さです。アルミニウムは酸素と光に対して優れたバリアーであり、これらの飲料は保存料や冷蔵なしで18ヶ月までもちます。

- 2023年のメッツァ板紙年次報告書に掲載された報告書によると、年間需要500万トンの液体包装用板紙は、5,900万トンに上るカートン板紙総需要のわずか8.5%を占めるに過ぎません。この分野は、耐久性、耐湿性、持続可能性などの特殊な特性により、液体の包装に人気があり、飲料や乳製品のような分野にとって極めて重要です。

欧州は著しい成長を遂げる見込み

- 欧州の液体用板紙市場は、主に持続可能性への関心の高まりによって、変革的な変化を経験しています。環境意識の高まりから、消費者の嗜好はますます環境に優しい包装に傾いています。この動向は、従来のプラスチック包装に代わる、より持続可能な液体用板紙の需要を大幅に押し上げています。

- また、EUの使い捨てプラスチック指令のような、使い捨てプラスチックの削減を義務付け、液体用板紙のような再生可能でリサイクル可能な材料の使用を奨励する欧州の規制によっても、このシフトは強化されています。

- さらに、eコマースの急成長も市場に影響を与えています。オンラインショッピングの増加により、環境に配慮しながら輸送中の商品を保護する、堅牢で信頼性の高い包装ソリューションのニーズが高まっています。液体用板紙は、耐久性と持続可能性の両方を提供し、この要件によく適合しています。この2つの利点により、液体用板紙は、持続可能性の目標に沿って事業を展開し、環境に配慮した包装に対する消費者の期待に応えようとする小売業者やeコマース企業にとって魅力的なものとなっています。

- 欧州の液体用板紙セクターの市場統合も注目に値します。少数の大手企業が市場を独占しているため、高いレベルでの統合が進んでいます。この統合により、研究開発への多額の投資が可能になり、技術革新と効率改善が促進されます。これらの大手メーカーは、技術の進歩を通じて液体用板紙の性能と持続可能性を高める方法を絶えず模索しています。

- デジタル印刷技術などの発展により、ブランドの差別化や消費者の関心を引く、高品質でカスタマイズ可能な包装ソリューションが可能になりました。さらに、生分解性と堆肥化可能なコーティングの進歩により、液体用板紙の持続可能性がさらに高まっています。これらの技術革新は、液体用板紙の環境フットプリントを改善し、様々な分野での用途を拡大し、市場成長をさらに促進します。

- 食糧農業機関のデータによると、ドイツの2024年の生産能力は2,453万トンです。一方、カートン板紙の生産能力は174万トンで、紙・板紙全体の生産能力の7%に過ぎません。カートン板紙には、折りたたみ牛乳パックや外食用ボックス板紙が含まれます。

液体用板紙業界の概要

液体用板紙市場は、Stora Enso, ITC, Graphic Packaging, WestRock, and Golden Paper Groupのような主要企業によって独占されています。 大手企業は戦略的な合併や買収を通じてこの統合を推進し、市場シェアを高め、持続可能な包装に対する高まる需要を満たすために世界的な展開を拡大しています。

2023年6月:Stora EnsoとTetra Pakは、ポーランドにあるStora EnsoのOstroleka段ボール工場で、消費後飲料カートンの新しいリサイクルラインを開始しました。両社によると、新たに追加された能力により、同工場は液体用板紙パッケージの欧州における主要なリサイクル拠点となる予定です。Stora Ensoによると、新ラインの処理能力は年間5万トンです。飲料カートンだけを扱い、繊維とポリマーやアルミニウムを分離します。その後、繊維はリサイクルされ、板紙製造に再利用されます。チェコのPlastigram IndustriesとTetra Pakは、繊維以外の「PolyAl」画分を新しい製品にリサイクルするソリューションを工業化しています。

2023年3月:Asia Symbol Jiangsuは、Rugao工場のカートン板紙ラインの業務改革と業務効率向上のため、ティートエブリーの製造実行システム(MES)を採用しました。最新の情報技術、デジタル化、主要ビジネスプロセスの自動化により、生産およびオペレーション管理の改善が可能になります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業バリューチェーン分析

- 業界の魅力度-ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

- 液体用板紙と液体カートンの現在の市場シナリオ

- バリア性の向上と賞味期限の延長につながる技術の進歩

- 飲料カートンパックの小型化をもたらすミニマルデザインの動向分析

- 板紙材料の輸出入に関する国際貿易政策

- 業界規制

第5章 市場力学

- 市場促進要因

- 便利で使いやすい包装形態への需要の高まり

- 持続可能で環境に優しい包装ソリューションへの注目の高まり

- 市場の課題

- 代替包装形態による市場成長の課題

第6章 市場セグメンテーション

- 材料タイプ別

- 液体包装板紙

- 食品・カップストック

- 最終用途別

- 飲料

- 食品

- 栄養補助食品

- ホームケアおよびパーソナルケア

- その他の最終用途

- 地域別

- 北米

- 欧州

- アジア

- ラテンアメリカ

- 中東・アフリカ

第7章 ベンダー市場シェア

第8章 競合情勢

- 企業プロファイル

- Stora Enso Oyj

- Graphic Packaging International

- WestRock Company

- ITC Limited

- Golden Paper Company

- Greatview Aseptic Packaging Co. Ltd

- Ningbo Sure Paper Co. Ltd

- Suneja Sons

- Billerud AB

- Asia Symbol Paper Co. Ltd

第9章 投資分析

第10章 市場の将来展望

The Liquid Paperboard Market size in terms of production volume is expected to grow from 4.30 Million metric tons in 2024 to 5.20 Million metric tons by 2029, at a CAGR of 3.87% during the forecast period (2024-2029).

Key Highlights

- Liquid paperboard (LPB) is a versatile and sustainable packaging material predominantly used in the food and beverage industry. Liquid paperboard consists of layers coated with various barrier materials, typically polyethylene or other biopolymers, to enhance its protective qualities. This multi-layered structure provides robust physical protection and effective barriers against moisture, oxygen, and light, making it ideal for packaging liquid products like milk, juices, soups, and sauces.

- Liquid paperboard is widely used in packaging for liquid cartons due to its sustainability and barrier properties. Manufacturers employ a minimalist, designable approach to create smaller packs that cater to single servings, reducing material usage and waste. These compact designs enhance convenience for consumers and promote environmental responsibility by minimizing the carbon footprint associated with packaging.

- Technological advancements in barrier coating have been a key driver in developing and enhancing liquid paperboard. Innovative coating technologies, such as those involving bio-based and biodegradable materials, are being developed to improve the performance of LPB while minimizing its environmental impact. These coatings not only enhance the shelf life and quality of the packaged products by preventing contamination and spoilage but also align with the growing consumer and regulatory push for sustainable packaging. For instance, advancements in nanotechnology have enabled the creation of ultra-thin yet highly effective barrier layers that can be applied to LPB, improving its functionality without significantly increasing its weight or cost.

- However, recycling liquid paperboard presents challenges because it is a composite material made from paperboard and polyethylene. Existing recycling infrastructure often needs help to separate these layers, hindering the recycling process efficiently. This complexity necessitates advancements in recycling technologies and systems to effectively handle liquid paperboard and improve its sustainability credentials.

Liquid Paperboard Market Trends

Rising Demand from the Beverage Segment Boosts The Market

- The rising demand from the beverage segment is significantly boosting the liquid paper board market. Packaging manufacturers and consumer brands increasingly opt for liquid paperboard because it can use fewer raw materials and create less waste, offering cost savings compared to other materials such as plastic or glass. By utilizing liquid paperboard, companies can produce lighter, more sustainable packaging that reduces transportation costs and minimizes environmental impact. This efficiency is particularly beneficial in the beverage industry, where the volume and weight of packaging can substantially influence overall logistics and carbon footprint.

- Premium liquid packaging boards are cost-effective and deliver exceptional product protection, ensuring the freshness and safety of beverages. These boards offer superior printing, converting, and filling performance, enabling brands to maintain high-quality standards and visually appealing designs. This combination of functionality and aesthetics makes liquid paperboard an attractive choice for packaging applications in the beverage industry, including juice, soups, water, and yogurt. The ability to provide a strong barrier against moisture, oxygen, and light further enhances these products' shelf life and quality, making liquid paperboard a preferred material for manufacturers.

- To further enhance the sustainability and efficiency of liquid paperboard, companies like Stora Enso are making significant investments in boosting the circularity of used beverage cartons. They are focusing on improving material efficiency and developing innovative solutions to enhance the performance of liquid paperboard. One such advancement is incorporating microfibrillated cellulose (MFC), which strengthens the paperboard while reducing its weight. This improvement decreases the amount of raw material needed and enhances the durability and functionality of the packaging, making it more competitive against other formats.

- Beverage cartons for long-life liquid products, like dairy products, soy milk, juices, fruit-based lemonades, and non-carbonated waters, additionally have a foil laminate. This thin aluminum layer protects beverages from light and oxygen. The aluminum layer is just 6.5 micrometers thick, less than a quarter of a hair. Aluminum is an excellent barrier for oxygen and light, and these drinks can last up to 18 months without preservatives or refrigeration.

- According to a report published in the annual report of the Metsa Board in 2023, a liquid packaging board with an annual demand of 5 million tons represents only 8.5% of the total carton board demand, which stands at 59 million tons. This segment is popular for packaging liquids due to specialized properties, such as durability, moisture resistance, and sustainability, making it crucial for sectors like beverages and dairy.

Europe is Set To Witness Significant Growth

- The European liquid paperboard market is experiencing a transformative shift, primarily driven by a heightened focus on sustainability. Consumer preferences increasingly lean toward eco-friendly packaging options due to growing environmental awareness. This trend significantly boosts the demand for liquid paperboard, a more sustainable alternative to traditional plastic packaging.

- The shift is also reinforced by European regulations, such as the EU's single-use plastics directive, which mandates the reduction of single-use plastics and encourages using renewable, recyclable materials like liquid paperboard.

- Additionally, the market is being influenced by the rapid growth of e-commerce. The rise in online shopping has increased the need for robust and reliable packaging solutions that protect goods during transit while being environmentally friendly. Liquid paperboard fits this requirement well, offering both durability and sustainability. This dual benefit makes liquid paperboard attractive for retailers and e-commerce companies looking to align their operations with sustainability goals and meet consumer expectations from green packaging.

- The market consolidation in the European liquid paperboard sector is also noteworthy. A few large players dominate the market, leading to high levels of consolidation. This consolidation enables significant investments in research and development, fostering innovation and efficiency improvements. These large manufacturers are continually exploring ways to enhance the performance and sustainability of liquid paperboard through technological advancements.

- Developments such as digital printing technologies allow for high-quality, customizable packaging solutions that cater to brand differentiation and consumer engagement. Additionally, biodegradable and compostable coating advancements make liquid paperboard even more sustainable. These technological innovations improve the environmental footprint of liquid paperboard and expand its applications across various sectors, further driving market growth.

- According to Food and Agriculture Organization data, Germany has a production capacity of 24.53 million tons in 2024. In contrast, the country has a production capacity of 1.74 million tons for carton boards, which is only 7% of total paper and paperboard production capacity. The carton boards include folding milk cartons and foodservice boxboards.

Liquid Paperboard Industry Overview

The market for liquid paperboard is dominated by key players such as Stora Enso, ITC, Graphic Packaging, WestRock, and Golden Paper Group. Major players are driving this consolidation through strategic mergers and acquisitions, enhancing their market share and expanding their global reach to meet the rising demand for sustainable packaging.

June 2023: Stora Enso and Tetra Pak started a new recycling line for post-consumer beverage cartons at Stora Enso's Ostroleka corrugated packaging plant in Poland. According to the companies, the newly added capacity intends to make the site one of Europe's main recycling hubs for liquid paperboard packaging. Stora Enso reported that the new line has a capacity of 50,000 tonnes a year. It handles only beverage cartons, separating the fibers from polymers and aluminum. The fibers are then recycled and reused for board production. Czech companies Plastigram Industries and Tetra Pak are industrializing a solution to recycle the non-fiber "PolyAl" fraction into new products.

March 2023: Asia Symbol Jiangsu Co. Ltd selected Tietoevry's Manufacturing Execution System (MES) to execute business transformation and increase operational efficiency in their Rugao mill's carton board line. The latest information technologies, digitalization, and automation of key business processes enable production and operations management improvements.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Current Market Scenario For Liquid Paperboard and Liquid Cartons

- 4.4.1 Technological Advancements Leading to Better Barrier Properties and Extended Shelf Life

- 4.4.2 Trend Analysis for Minimalist Designs Resulting in Smaller Beverage Carton Packs

- 4.4.3 International Trade Policies on Import and Export of Paperboard Materials

- 4.4.4 Industry Regulations

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Demand for Convenient and Easy-to-Use Packaging Formats

- 5.1.2 Growing Focus on Sustainable and Eco-Friendly Packaging Solutions

- 5.2 Market Challenge

- 5.2.1 Alternative Forms of Packaging is Challenging the Market Growth

6 MARKET SEGMENTATION

- 6.1 By Material Type

- 6.1.1 Liquid Packaging Board

- 6.1.2 Food and Cupstock

- 6.2 By End-Use Application

- 6.2.1 Beverage

- 6.2.2 Food

- 6.2.3 Nutraceuticals

- 6.2.4 Homecare and Personal Care

- 6.2.5 Other End-use Applications

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia

- 6.3.4 Latin America

- 6.3.5 Middle East and Africa

7 VENDOR MARKET SHARE

8 COMPETITIVE LANDSCAPE

- 8.1 Company Profiles

- 8.1.1 Stora Enso Oyj

- 8.1.2 Graphic Packaging International

- 8.1.3 WestRock Company

- 8.1.4 ITC Limited

- 8.1.5 Golden Paper Company

- 8.1.6 Greatview Aseptic Packaging Co. Ltd

- 8.1.7 Ningbo Sure Paper Co. Ltd

- 8.1.8 Suneja Sons

- 8.1.9 Billerud AB

- 8.1.10 Asia Symbol Paper Co. Ltd