|

市場調査レポート

商品コード

1549803

GCC諸国の段ボール箱パッケージ:市場シェア分析、産業動向・統計、成長予測(2024~2029年)GCC Corrugated Box Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| GCC諸国の段ボール箱パッケージ:市場シェア分析、産業動向・統計、成長予測(2024~2029年) |

|

出版日: 2024年09月02日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

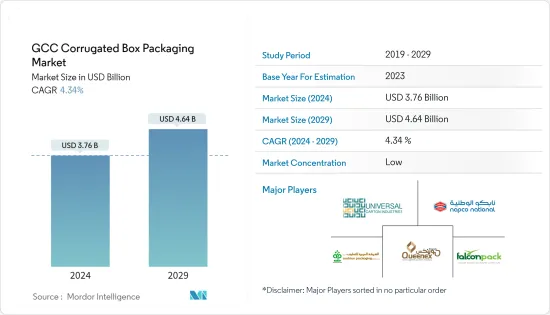

GCC諸国の段ボール箱パッケージ市場規模は2024年に37億6,000万米ドルと推定され、2029年には46億4,000万米ドルに達すると予測され、予測期間(2024-2029年)のCAGRは4.34%で成長する見込みです。

主なハイライト

- 多忙なライフスタイルの増加により、コンビニエンス・フードへの需要が高まっており、段ボール箱パッケージへの依存度が高まっています。製品を湿気から守り、長期間の出荷に耐えるその優れた能力は、顧客満足度の向上を目指す企業にとって理想的な選択肢となっています。その結果、段ボール箱は様々な業界で二次包装、三次包装の好ましい選択肢として広く採用されています。

- 段ボール箱は、電気製品、食品、パーソナルケア、化粧品など、さまざまなエンドユーザー産業向けの二次または三次梱包ソリューションとして適しています。段ボール箱は一般的に、野菜やその他の食品を小売店に出荷する際に使用されます。これは、型抜きされた内部に商品を収納する配送に適したフォーマットを持つ段ボール業者にとって、新たなチャンスです。ガラスや金属に比べ、最終製品の総重量を減らすことができます。

- eコマースの普及は小売市場を変えました。消費者行動と小売ビジネスモデルの力学を変えたこのメガ動向は、GCC諸国で成長を示しており、業界プレーヤーに大きな可能性を提供しています。GCC諸国のeコマース成長の主な原動力は、高い一人当たり所得支出の可能性、発達した輸送・物流ネットワーク、インターネット普及率の向上、そして技術です。段ボール箱パッケージ業界の主な製品動向と技術革新は、本質的な重量の少ない軽量段ボールであり、これにより運賃が大幅に削減されました。また、効果的な容積利用によって優れた印刷とコスト削減を実現する革新的なデザインも、調査対象市場の成長を後押ししています。

- 紅海危機はコンテナーボードの出荷を縮小し、地元の道路輸送の利用可能性とコスト、紅海沿岸のサウジアラビアのジッダ港の利用に影響を与えました。このため、GCC諸国地域の段ボール箱パッケージの原材料コストが上昇し、原材料の入手性が課題となることで、予測期間中の市場の成長に影響を与える可能性があります。

- COVID-19が大流行する中、GCC諸国地域ではオンライン注文が大幅に急増し、エンドユーザーの幅広い業種に対応しています。特に、段ボール箱パッケージは食品包装分野で極めて重要なプレーヤーとして台頭し、パンデミック後の市場の成長を後押ししました。

GCC諸国の段ボール箱パッケージ市場の動向

加工食品セグメントが成長を大きく支える

- 段ボール箱は包装内のスペースを最小限に抑えるように設計できるため、輸送中の製品の移動や損傷のリスクを軽減できます。これにより賞味期限が延び、食品廃棄を抑制する上で極めて重要な役割を果たします。さらに、段ボールが直接触れても食品に安全である場合、追加的な内部包装の必要性が減少し、市場の成長を支えます。

- GCC諸国の段ボール箱パッケージ市場は、食品産業における強力な用途が特徴です。消費者は、費用対効果が高く、持続可能で、軽量で、再利用可能で、リサイクル可能で、便利な製品を求める傾向があり、食品における段ボール箱パッケージの需要を牽引しています。食品を携帯可能で便利な形態で包装する需要の高まりが、様々な産業で包装製品の使用を後押ししています。リサイクル性と分解性により、段ボール箱パッケージは他の素材よりも持続可能性が高く、将来的にその採用を後押しすると予想されます。

- さらに、アラブ首長国連邦の食品産業は、主にドバイ、アブダビ、シャルジャといった主要都市部での小売・加工食品に対する食欲の高まりに後押しされ、著しい上昇を経験しています。こうした需要の急増は、ライフスタイルの変化と健康志向の高まりによるものです。アラブ首長国連邦は農業生産に制約があるため、輸入に大きく依存しており、必要な食糧の80%以上を海外から調達しています。

- しかし2024年1月、GCC諸国では国産コンテナーボードの価格が上昇しました。中東製紙会社(MEPCO)は2024年1月にトン当たり70米ドルの値上げを発表し、この地域の加工食品分野における段ボール箱パッケージの成長に影響を与えると予想されます。

- GCC諸国地域では食品の小売販売が大幅に増加しており、今後数年間は加工食品の包装に使用される段ボール箱の需要を生み出し、市場の成長を支えることが予想されます。これは廃棄物削減の取り組みをさらに強化し、食品包装における市場の成長を支えています。

大きな市場シェアを占めるサウジアラビア

- サウジアラビアはGCC諸国地域の包装業界における主要市場のひとつです。同国は注目すべき消費者基盤を持ち、国のビジョン2030の目標に沿った幅広い産業活動(石油・ガス部門を除く)を行っているため、紙・板紙パッケージングに対する急速な需要が高まっています。顧客に優しいパッケージと製品保護の強化に対する需要の高まりは、サウジアラビアにおける実行可能で費用対効果の高いソリューションとしての段ボール箱パッケージを後押しすると予想されます。

- 同国は段ボール箱パッケージソリューションの製造を支援しており、これは将来の需要を示しています。例えば、2024年3月には、段ボールパレットを生産するサウジアラビアのメガ工場の建設が最終段階に入った。この工場により、サウジアラビアのパレット生産能力は年間1,000万枚に達する見込みです。

- このメガ工場は、GCC諸国地域における革新的で持続可能なパレット・ソリューションに対する高い需要を満たすことを目的としています。8万6,000平方メートルに及ぶこの施設は、先進技術によってパレット業界を変革し、世界の物流コストと二酸化炭素排出量を大幅に削減するもので、環境の持続可能性における段ボール箱パッケージソリューションの優位性を示しています。

- さらに2024年1月には、サウジアラビアの政府系ファンドであるPIF(Public Investment Fund)が、中東製紙会社(MEPCO)への投資を発表しました。MEPCOは中東のメーカーで、紙ベースの製品とリサイクルに注力しています。PIFの支援は、MEPCOの生産拡大に弾みをつけ、経営効率を高め、環境持続可能性への取り組みを強化します。これは、サウジアラビアとPIF双方の持続可能性の目的に合致するものであり、将来的には調査対象市場の成長を支えるものと期待されます。

- サウジアラビアの非石油ベースの経済発展に伴い、同国の若年失業率は低下しており、予測期間中、同国における包装商品の需要を促進し、段ボール箱パッケージソリューションの成長機会を生み出すと予想されます。

GCC諸国段ボール箱パッケージ業界の概要

市場は、Arabian Packaging LLC、Queenex Corrugated Carton Factory、Universal Carton Industries Group、Napco National、Falcon Packなどの様々な国内企業によって断片化されています。市場のプレーヤーは、製品提供を強化し、持続可能な競争優位性を獲得するために、提携、合併、技術革新、投資、企業拡大、買収などの戦略を採用しています。

- 2023年12月Ras Al Khaimah Economic Zone(RAKEZ)に位置する主要段ボール箱製造企業の1つであるUniversal Carton Industries Groupは、アラブ首長国連邦および海外における持続可能なパッケージングソリューションの需要拡大に対応するため、約1,497万米ドルを投資して生産量を拡大しました。この拡張により、ユニバーサル・カートン・インダストリーズ・グループの生産能力は3倍の年間10万トンとなり、GCC諸国地域における段ボール箱パッケージの今後の市場成長の可能性を示すことになります。

- 2023年8月サプライチェーンソフトウェアのプロバイダーであるEPG(Erhardt Partner Group)は、ドバイを拠点とする市場ベンダーであるFalcon Packと提携し、Falcon Packの産業セットアップにEPGの輸送管理システム(TMS)を統合しました。これにより、ドバイで急速に拡大するFalcon Packのパッケージング活動のスピード、正確性、全体的な効率を高め、市場におけるFlacon Packの存在感をサポートすることを目的としています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業バリューチェーン分析

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 供給企業の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- COVID-19の業界への影響評価

- 輸出入分析

第5章 市場分析

- 市場促進要因

- eコマース分野からの需要増加

- 軽量素材への需要の高まりとエンドユーザー部門の成長余地

- 市場抑制要因

- 段ボール製品の材料入手性と耐久性に関する懸念

第6章 市場セグメンテーション

- タイプ別

- 無地

- 印刷

- 印刷タイプ別

- リトラミネート

- その他

- エンドユーザー別

- 加工食品

- 生鮮食品

- 飲料

- パーソナルケア

- その他のエンドユーザー

- 国別

- サウジアラビア

- アラブ首長国連邦

- カタール

- その他のGCC諸国

第7章 競合情勢

- 企業プロファイル

- Arabian Packaging Co. LLC

- Queenex Corrugated Carton Factory

- United Carton Industries Company(UCIC)

- Napco National

- Cepack Group

- Falcon Pack

- World Pack Industries LLC

- Universal Carton Industries Group

- Stora Enso Oyj

- Express Pack Print

- Green Packaging Boxes Ind LLC

- Tarboosh Packaging Co. LLC

- Unipack Containers & Carton Products LLC

- Al Rumanah Packaging

- NBM Pack

第8章 投資分析

第9章 市場の将来

The GCC Corrugated Box Packaging Market size is estimated at USD 3.76 billion in 2024, and is expected to reach USD 4.64 billion by 2029, growing at a CAGR of 4.34% during the forecast period (2024-2029).

Key Highlights

- The escalating demand for convenience foods, driven by increasingly hectic lifestyles, has increased the reliance on corrugated box packaging. Its exceptional ability to safeguard products from moisture and endure extended shipping periods makes it an ideal choice for companies seeking to enhance customer satisfaction. As a result, corrugated boxes are being widely adopted as a preferred option for secondary and tertiary packaging across various industries.

- A corrugated box is a suitable secondary or tertiary packaging solution for various end-user industries, including electrical goods, food, personal care, cosmetics, etc. Corrugated boxes are commonly used to ship vegetables or other foodstuffs to retailers. This is a new opportunity for corrugated board suppliers with delivery-friendly formats containing goods within a die-cut interior. It helps reduce the overall weight of the final product compared to glass or metal.

- The widespread adoption of e-commerce has changed the retail market. This megatrend, which has changed the dynamics of consumer behavior and retail business models, is witnessing growth in the GCC and offers significant potential for industry players. The GCC's main drivers of e-commerce growth are high per capita income spending potential, well-developed transportation and logistics networks, increased internet penetration, and technology. The corrugated packaging industry's primary product trends and innovations are lightweight containerboards with less essential weight, which have significantly reduced freight costs. Innovative designs, which provide superior printing and cost savings through effective volume utilization, have also been driving the growth of the market studied.

- The Red Sea crisis downsized the containerboard shipments and impacted the availability and cost of local road transport and the usage of the Saudi Arabian port in Jeddah on the Red Sea coast. This has increased the raw material cost of corrugated box packaging in the GCC region, which may impact the market's growth during the forecast period by challenging the material availability.

- Amidst the COVID-19 pandemic, online orders saw a significant surge in the GCC region, catering to a wide array of end-user verticals. Notably, corrugated packaging emerged as a pivotal player in the food packaging sector, bolstering the market's growth in the post-pandemic period.

GCC Corrugated Box Packaging Market Trends

Processed Food Segment to Significantly Support Growth

- Corrugated boxes can be designed to minimize space in packaging, reducing the risk of product movement and damage during transit. This extends shelf life and plays a pivotal role in curbing food waste. Additionally, when the corrugated board is food-safe for direct contact, it diminishes the necessity for additional inner packaging, supporting the market's growth.

- The corrugated box packaging market in GCC is characterized by strong applications in the food industry. Consumers tend to look for cost-effective, sustainable, lightweight, reusable, recyclable, and convenient products, driving the demand for corrugated packaging in food products. The rising demand for packaging foods in portable and convenient formats has helped drive the use of packaging products across various industries. Recyclability and decomposability make corrugated packaging more sustainable than other materials, which is expected to support its adoption in the future.

- Furthermore, the food industry in the United Arab Emirates has experienced a significant upswing, primarily propelled by a rising appetite for retail and processed foods in key urban centers such as Dubai, Abu Dhabi, and Sharjah. This demand surge is due to lifestyle changes and a growing emphasis on health. Given its constrained agricultural production, the United Arab Emirates leans heavily on imports, sourcing over 80% of its food requirements internationally.

- However, in January 2024, prices for locally produced container boards rose in the GCC countries. The Middle East Paper Company (MEPCO) announced a price hike of USD 70 per ton in January 2024, which is expected to impact the growth of corrugated packaging in the processed food segments in the region.

- The retail sales of food items have been increasing significantly in the GCC region, which is expected to support the growth of the market by creating a demand for corrugated boxes used for the packaging of processed foods in the coming years. It further enhances waste reduction efforts and supports the market's growth in food packaging.

Saudi Arabia to Occupy Significant Market Share

- Saudi Arabia is one of the GCC region's leading markets in the packaging industry. The country has a notable consumer base and a wide range of industrial activities (apart from the oil and gas sector) that are in line with the country's Vision 2030 objective, adding to the rapid demand for paper and paperboard packaging. The growing demand for customer-friendly packages and heightened product protection is expected to boost corrugated packaging as a viable and cost-effective solution in Saudi Arabia.

- The country has been supporting the manufacturing of corrugated packaging solutions, which indicates the demand for them in the future. For instance, in March 2024, the construction of Saudi Arabia's mega factory to produce corrugated pallets entered its final stages. The factory is expected to increase the country's capacity to produce up to 10 million pallets annually.

- The mega factory aims to meet the high demand for innovative and sustainable pallet solutions in the GCC region. Spanning 86,000 square meters, this facility would transform the pallet industry with advanced technology and significantly reduce global logistics costs and carbon emissions, which shows the advantage of corrugated packaging solutions in environmental sustainability.

- Furthermore, in January 2024, the Public Investment Fund (PIF), Saudi Arabia's sovereign wealth fund, announced its investment in the Middle East Paper Company (MEPCO). MEPCO is a Middle Eastern manufacturer that focuses on paper-based products and recycling. PIF's backing would fuel MEPCO's production expansion, enhance operational efficiency, and bolster its commitment to environmental sustainability. This would align with the sustainability objectives of both Saudi Arabia and PIF, which is expected to support the growth of the market studied in the future.

- The youth unemployment rate in the country has been decreasing in line with non-oil-based economic development in Saudi Arabia, which is anticipated to fuel the demand for packaged goods in the country and create growth opportunities for corrugated box packaging solutions during the forecast period.

GCC Corrugated Box Packaging Industry Overview

The market is fragmented with various domestic companies, such as Arabian Packaging LLC, Queenex Corrugated Carton Factory, Universal Carton Industries Group, Napco National, Falcon Pack, etc. Players in the market are adopting strategies such as partnerships, mergers, innovations, investments, company expansion, and acquisitions to enhance their product offerings and gain sustainable competitive advantage.

- December 2023: Universal Carton Industries Group, one of the leading corrugated cardboard box manufacturing companies located in Ras Al Khaimah Economic Zone (RAKEZ), invested approximately USD 14.97 million to expand its production volume to meet the growing demand for sustainable packaging solutions in the United Arab Emirates and overseas. This expansion will increase Universal Carton Industries Group's production capacity by threefold to 100,000 tons annually, which shows the future market growth potential of corrugated box packaging in the GCC region.

- August 2023: EPG (Ehrhardt Partner Group), a supply chain software provider, partnered with Falcon Pack, a market vendor based in Dubai, to integrate EPG's Transportation Management System (TMS) in Falcon Pack's industrial set-up. This aims to enhance the speed, accuracy, and overall efficiency of Falcon Pack's rapidly expanding packaging activities in Dubai, supporting the Flacon Pack's presence in the market studied.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of New Entrants

- 4.3.5 Threat of Substitutes

- 4.3.6 Intensity of Competitive Rivalry

- 4.4 Assessment of COVID-19 Impact on the Industry

- 4.5 Import and Export Analysis

5 MARKET DYANMICS

- 5.1 Market Drivers

- 5.1.1 Increased Demand from the E-commerce Sector

- 5.1.2 Growing Demand for Lightweight Materials and Scope for Growth in End-user Sectors

- 5.2 Market Restraints

- 5.2.1 Concerns About Material Availability and Durability of Corrugated-based Products

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Plain

- 6.1.2 Printed

- 6.2 By Printed

- 6.2.1 Litho-Laminate

- 6.2.2 Others

- 6.3 By End User

- 6.3.1 Processed Food

- 6.3.2 Fresh Food

- 6.3.3 Beverages

- 6.3.4 Personal Care

- 6.3.5 Other End Users

- 6.4 By Country

- 6.4.1 Saudi Arabia

- 6.4.2 United Arab Emirates

- 6.4.3 Qatar

- 6.4.4 Rest of GCC

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Arabian Packaging Co. LLC

- 7.1.2 Queenex Corrugated Carton Factory

- 7.1.3 United Carton Industries Company (UCIC)

- 7.1.4 Napco National

- 7.1.5 Cepack Group

- 7.1.6 Falcon Pack

- 7.1.7 World Pack Industries LLC

- 7.1.8 Universal Carton Industries Group

- 7.1.9 Stora Enso Oyj

- 7.1.10 Express Pack Print

- 7.1.11 Green Packaging Boxes Ind LLC

- 7.1.12 Tarboosh Packaging Co. LLC

- 7.1.13 Unipack Containers & Carton Products LLC

- 7.1.14 Al Rumanah Packaging

- 7.1.15 NBM Pack