タイのパッケージング:市場シェア分析、産業動向、成長予測(2025~2030年)

Thailand Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 95 Pages

- 納期

- 2~3営業日

- 商品コード

- 1644890

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

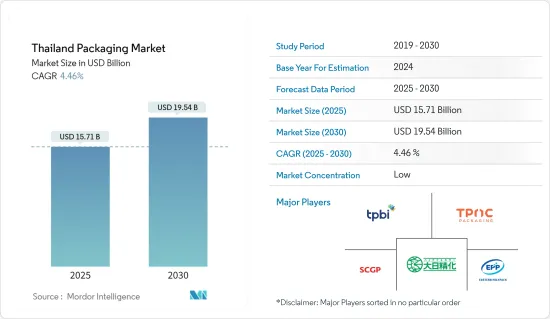

タイのパッケージング市場規模は2025年に157億1,000万米ドルと推計され、予測期間(2025-2030年)のCAGRは4.46%で、2030年には195億4,000万米ドルに達すると予測されます。

タイの経済拡大により、パッケージング用品の生産と消費の両方が着実に増加しています。タイのパッケージング産業は拡大し、大きな経済貢献をしています。これは、何にでも適しており、何にでも梱包できるパッケージング用品へのニーズが高まっている結果です。

主なハイライト

- タイのパッケージング業界は、基材の嗜好の変化、新市場の開拓、所有者の原動力の変化により、過去10年間一貫して成長してきました。特に先進国では、持続可能性と環境への懸念が依然として強調されており、業界では紙とプラスチックパッケージングに対応する様々な技術が見られます。

- さらに、リサイクル不可能なプラスチックパッケージングの消費は増加傾向にあります。その結果、二次パッケージングの必要性が減り、紙や板紙、回収PET(rPET)、バイオプラスチックなど、環境にやさしいパッケージング材料への需要が高まる可能性があります。

- フレキシブルパッケージングは最終的には従来のパッケージングに取って代わるかもしれないです。様々な食品では、ハイバリアフィルムやスタンドアップレトルトパウチが、金属缶やガラス瓶のような硬いパッケージング形態と競合する可能性があります。電子レンジで調理可能な調理済み食品、より持ち運びしやすいパッケージング、外出先で消費するためのパッケージング、イージーオープンやリシール部品のような便利な機能によって、食品における消費者の利便性へのニーズが満たされるかもしれないです。

- さらに、小売業界における競争の複雑さとレベルも、市場に影響を与える重要な側面です。スーパーマーケットやコンビニエンスストアのような近代的な小売店では、冷凍食品の品揃えが豊富で、より広く利用されています。シュリンクフィルム、フレキシブルバッグ、リディングフィルム、ハイバリア熱成形フィルム、スキンフィルムなどの冷凍食品用フレキシブルパッケージングは、多くの成長国で以前には考えられなかった速度で採用されています。

- プラスチックの使用に関する規制が台頭しているため、タイではフレキシブルパッケージングの成長が抑制される可能性があるが、例えば2023年1月、タイ工業標準院(TISI)は食品用プラスチック袋に関する省令案(TIS 1027-25xx(20xx))を発表しました。これは、材料に含まれる物質の安全要件、マーキング、ラベリング、試験基準の仕様を概説しています。特に、食品パッケージング用の単層プラスチックフィルムとしてバージン樹脂から作られたプラスチック袋に適用されます。この規格は、インクでカスタム印刷されたプラスチック袋には適用されないことに注意することが重要です。

タイのパッケージング市場の動向

プラスチックが市場で大きなシェアを占める見込み

- タイのパッケージング市場は、特にオン・ザ・ゴー・パック、サステイナブル・パック、カスタマイズ・パックなどを通じて商品の有用性を向上させるパッケージングによって区別されます。この地域のポリエチレン(PE)市場は、こうした傾向の結果として拡大しています。ポリ袋、プラスチックフィルム、ジオメンブレンなどは、一般的にポリエチレンでパッケージングされています。この熱可塑性樹脂は薄く、やや結晶性があり、耐薬品性が強く、吸湿性が少なく、遮音性があります。

- 予測期間中、パッケージング用PE樹脂のニーズは急増すると予想されるが、その主な理由はバリューチェーンのインテリジェント化です。工業生産はインダストリー4.0とモノのインターネット(IoT)の結果として変化しており、これがPEバリューチェーンに新たな展望を開いています。インダストリー4.0によって提供されるトレーサビリティの向上は、パッケージの作成から最終製品が小売店の店頭に並ぶまで、パッケージの構成、特にリサイクル素材が含まれる場合などを確実に監視できるようにする上で、重要な役割を果たすと期待されています。

- ホットミールでのプラスチックの使用には、材料の長期間の使用がもたらす健康障害のリスクが含まれます。TSH、HCY、A1Cはすべて、ホットミールでのプラスチックの毎日の使用と良い相関があるが、ビタミンE、亜鉛、セレン濃度は悪い相関があります。ホットミールでのプラスチックの使用による特定の成分の放出に関連した複雑なホルモンおよび代謝異常は、この技術に関する今後の研究の主な焦点です。

- 直鎖状低密度ポリエチレン(LLDPE)袋は、適度な透明度を特徴とし、食品袋、新聞袋、買い物袋、ゴミ袋の製造に使用されています。中密度ポリエチレン(MDPE)は、ゴミ袋の製造や、トイレットペーパーやペーパータオルのような紙製品の消費者向けパッケージングに一般的に使用されています。

食品産業が市場の成長を牽引すると予想される

- 世界銀行の発表によると、タイのGDPの1/4は飲食品セクターによって生み出されており、タイに多大な経済的貢献をしています。米、ツナ缶、砂糖、豚肉、キャッサバ製品、パイナップル缶詰などが主な食品輸出品目です。タイ工業連盟(FTI)、タイ商工会議所(TCC)、国立食品研究所(NFI)によると、食品輸出は2023年に1兆5,500億バーツ、2024年には1兆6,500億バーツに達すると予想されています。

- タイプラスチック工業協会の報告によると、タイではプラスチックパッケージングの市場が拡大しています。医薬品、家庭用品、飲食品、柔軟性のあるプラスチックベースのプロジェクトは、需要が予測される品目と産業のひとつです。プラスチックは、安価で加工しやすく、成形しやすく、耐薬品性に優れ、軽量で、幅広い物理的性質を持っているため、食品パッケージングに便利でよく使われています。

- ここ数年、タイでは、ベーカリー製品やシリアルバー、短納期の調理済み食品、コーヒーやホットチョコレートのスティックやパウチ、ドライ食品(インスタントスープ、グレービーソースやソースのパック、米、フードミックス)、スナック菓子やナッツ類、スパイス食品、チョコレートやお菓子、アイスクリームのノベルティグッズ、クッキー(ビスケット)やケーキ、チップスなどのベーカリー製品への支出が大幅に増加しています。

- 市場は現在、製品の品質が顧客に評価された結果、冷凍食品パッケージングの需要が増加しています。タイでは経済の拡大とライフスタイルの進化により、冷凍食品パッケージングのニーズが拡大しており、業界は今後数年間で収益性の高い拡大が見込まれています。

- また、市場は小売業界の複雑さと競合からも大きな影響を受けています。スーパーマーケットやコンビニエンスストアなど、冷凍食品の品揃えが豊富な近代的な小売業の立地では、より頻繁に使用されています。シュリンクフィルム、フレキシブルバッグ、リディングフィルム、ハイバリア熱成形フィルム、スキンフィルムはすべて、冷凍食品パッケージングのためにいくつかの新しい国々で、以前には考えられなかったような割合で採用されています。

タイパッケージング業界の概要

タイのパッケージング市場は非常に断片化されており、いくつかの主要企業で構成されています。Dainichiseika Color &Chemicals Mfg.、Fagerdala Singapore Pte Ltd、Eastern Polypack、TPBI Public Company Limited、TPAC Packagingなど、市場で大きなシェアを持つ大手企業は、様々な技術を採用することで、外国での顧客基盤の拡大に注力しています。

- 2023年12月- 花王インダストリアル(タイランド)(花王)は、リサイクル可能なパッケージングを開発するために、SCGケミカルズ(SCGC)およびダウ・タイランド・グループ(ダウ)の2つの世界のパッケージングの専門家と提携しました。このパートナーシップの目的は、消費者により持続可能なパッケージングの選択肢を提供することであり、高品質、低カーボンフットプリント、リサイクル可能なパッケージングに焦点を当てています。本日、3社はトゥルー・デジタル・パーク・ウエストにあるダウ・タイランド本社で覚書に調印しました。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 産業バリューチェーン分析

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- COVID-19パンデミックの業界への影響評価

第5章 市場洞察

- 市場促進要因

- エンドユーザー産業からの需要増加

- 便利なパッケージングに対する需要の増加

- 市場抑制要因

- 環境とリサイクルに関する懸念

第6章 市場セグメンテーション

- パッケージング材料別

- プラスチック

- 紙・板紙

- ガラス

- 金属

- パッケージングタイプ別

- フレキシブルパッケージング

- パウチ

- 袋

- パッケージングフィルム

- その他の製品タイプ

- リジッドパッケージング

- ボトルとジャー

- 段ボール箱と折りたたみカートン

- 金属缶

- ドラム缶

- バルク容器

- フレキシブルパッケージング

- エンドユーザー別

- 食品

- 飲料

- 美容・パーソナルケア

- 工業用

- 医薬品

- その他のエンドユーザー

第7章 競合情勢

- 企業プロファイル

- TBPI Public Company Limited

- TPAC Packaging

- SCG Packaging

- Dainichiseika Color & Chemicals Mfg. Co. Ltd

- Eastern Polypack Co. Ltd

- Huhtamaki Flexible Packaging

- Fagerdala Singapore Pte Ltd

- Sealed Air Corporation

- Amcor PLC

- Toppan(Thailand)Co. Ltd

第8章 投資分析

第9章 市場の将来

目次

The Thailand Packaging Market size is estimated at USD 15.71 billion in 2025, and is expected to reach USD 19.54 billion by 2030, at a CAGR of 4.46% during the forecast period (2025-2030).

Thailand's economic expansion has led to a steady rise in both the production and consumption of packaging goods throughout time. The Thailand packaging industry is expanding and making a substantial economic contribution. This is a result of the growing need for packaging supplies that are appropriate for anything and can be used to pack anything.

Key Highlights

- The Thai packaging industry has consistently grown over the past 10 years due to changes in substrate preferences, the opening of new markets, and shifting ownership dynamics. Sustainability and environmental concerns may still be highlighted, especially in developed nations, and the industry is seeing a variety of technologies that cater to paper and plastic packaging.

- Moreover, consumption of non-recyclable plastic packaging is on the rise. As a result, there could be less need for secondary packaging and increasing demand for environmentally friendly packaging materials, including paper and board, recovered PET (rPET), and bioplastic.

- Flexible packaging may eventually supplant conventional packaging. For a variety of food goods, high-barrier films and stand-up retort pouches may compete with rigid pack forms like metal cans and glass jars. Consumers' need for convenience in food may be met via microwaveable ready meals, more portable packaging, packaging for consumption on the go, and convenience features like easy-open and reseal components.

- Furthermore, the complexity and level of competition in the retail industry are other important aspects that influence the market. Modern retail trade shops, such as supermarkets and convenience stores, which may stock a wider variety of frozen food goods, are more widely used. Flexible packaging for frozen foods, such as shrink films, flexible bags, lidding films, high barrier thermoforming films, and skin films, are being adopted at previously unheard-of rates in a number of growing countries.

- While regulations emerging on plastic usage could restrain the growth of flexible packaging in Thailand, for instance, in January 2023, the Thai Industrial Standards Institute (TISI) released the Draft Ministerial Regulation on Plastic Bags for Food (TIS 1027-25xx (20xx)). This outlines safety requirements for substances in the material, as well as specifications for marking, labeling, and testing criteria. It specifically applies to plastic bags made from virgin resin as single-layer plastic films for food packaging. It's important to note that this standard does not apply to custom-printed plastic bags with ink.

Thailand Packaging Market Trends

Plastic is Expected to Hold a Significant Share in the Market

- The Thai packaging market is distinguished by packaging that improves the usefulness of goods through, among other things, on-the-go packs, sustainable packs, or customized packs. The polyethylene (PE) market in the area is expanding as a result of this tendency. Plastic bags, plastic films, and geomembranes are commonly packaged with polyethylene. This thermoplastic resin is thin, somewhat crystalline, and has strong chemical resistance, little moisture absorption, and sound-insulating qualities.

- The country's need for PE resin for packaging is expected to soar during the forecast period, mostly because of the intelligent value chain. Industrial production is changing as a result of Industry 4.0 and the Internet of Things (IoT), and this is opening up new prospects for the PE value chain. The greater traceability provided by Industry 4.0 is expected to play a significant role in ensuring that the package composition can be monitored, particularly where recycled content is present, from the creation of the package through the end product being put on the retail shelf.

- The risk of health problems brought on by prolonged use of the materials is included in the usage of plastics with hot meals. TSH, HCY, and A1C are all favorably correlated with daily usage of plastics with hot meals, but vitamin E, zinc, and selenium concentrations are adversely correlated. The complicated hormonal and metabolic anomalies connected to the release of certain components caused by the usage of plastics with hot meals are the main focus of future studies on the technology.

- Linear low-density polyethylene (LLDPE) bags feature moderate clarity and are used to manufacture food bags, newspaper bags, shopping bags, and garbage bags. Medium-density polyethylene (MDPE) is commonly used to manufacture garbage bags and in consumer packaging for paper products, such as toilet paper or paper towels.

The Food Industry is Expected to Drive the Market's Growth

- One-fourth of Thailand's GDP is generated by the food and beverage sector, which makes a substantial economic contribution to the nation, as stated by the World Bank. Rice, canned tuna, sugar, pork, cassava products, and canned pineapple are some of the main food exports. Food exports were expected to reach THB 1.55 trillion in 2023 and THB 1.65 trillion in 2024, according to the Federation of Thai Industries (FTI), the Thai Chamber of Commerce (TCC), and the National Food Institute (NFI).

- The Thailand Plastics Industry Association reports that there is a growing market for plastic packaging in Thailand. Pharmaceuticals, home goods, food and beverage, and flexible plastic-based projects are among the items and industries that are projected to witness demand. Plastic is convenient and often used in food packaging because it is inexpensive, easily processed, formable, chemically resistant, lightweight, and has a wide range of physical qualities.

- Over the past few years, Thailand has seen a significant increase in spending on bakery goods and cereal bars, short-run ready meals and coffee or hot chocolate sticks and pouches, dry foods (instant soup, gravy and sauce packets, rice, and food mixes), snack foods and nuts, spice foods, chocolates and sweets, ice-cream novelty items, and bakery goods like cookies (biscuits), cakes, and chips.

- The market is now experiencing a rise in demand for frozen food packaging as a result of customer appreciation of the product quality. The need for frozen food packaging has expanded in Thailand due to the country's expanding economy and evolving lifestyles, and the industry is anticipated to expand profitably over the next years.

- The market is also significantly impacted by the retail industry's complexity and competitiveness. Modern retail trade locations with a wider selection of frozen food items, such as supermarkets and convenience stores, are more often used. Shrink films, flexible bags, lidding films, high barrier thermoforming films, and skin films are all being adopted at previously unheard-of rates in several new countries for frozen food packaging.

Thailand Packaging Industry Overview

The Thai packaging market is highly fragmented and consists of several major players. Major players with a prominent share in the market, including Dainichiseika Color & Chemicals Mfg. Co. Ltd, Fagerdala Singapore Pte Ltd, Eastern Polypack Co. Ltd, TPBI Public Company Limited, and TPAC Packaging, focus on expanding their customer base across foreign countries by adopting various technologies.

- December 2023 - Kao Industrial (Thailand) Co. Ltd (Kao) teamed up with two leading global packaging experts, SCG Chemicals Co. Ltd (SCGC) and Dow Thailand Group (Dow), to develop recyclable packaging. The goal of the partnership is to offer consumers more sustainable packaging choices, focusing on high-quality, lower carbon footprint, and recyclable packaging. Today, the three companies signed a Memorandum of Understanding (MoU) at Dow Thailand's headquarters in True Digital Park West.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Assessment of the Impact of the COVID-19 Pandemic on the Industry

5 MARKET INSIGHTS

- 5.1 Market Drivers

- 5.1.1 Increasing Demand from End-user Industries

- 5.1.2 Increased Demand for Convenient Packaging

- 5.2 Market Restraints

- 5.2.1 Concerns Regarding the Environment and Recycling

6 MARKET SEGMENTATION

- 6.1 By Packaging Material

- 6.1.1 Plastic

- 6.1.2 Paper and Paperboard

- 6.1.3 Glass

- 6.1.4 Metal

- 6.2 By Packaging Type

- 6.2.1 Flexible Packaging

- 6.2.1.1 Pouches

- 6.2.1.2 Bags

- 6.2.1.3 Packaging Films

- 6.2.1.4 Other Product Types

- 6.2.2 Rigid Packaging

- 6.2.2.1 Bottles and Jars

- 6.2.2.2 Corrugated Boxes and Folding Cartons

- 6.2.2.3 Metal Cans

- 6.2.2.4 Drums

- 6.2.2.5 Bulk Containers

- 6.2.1 Flexible Packaging

- 6.3 By End User

- 6.3.1 Food

- 6.3.2 Beverage

- 6.3.3 Beauty and Personal Care

- 6.3.4 Industrial

- 6.3.5 Pharmaceutical

- 6.3.6 Other End Users

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 TBPI Public Company Limited

- 7.1.2 TPAC Packaging

- 7.1.3 SCG Packaging

- 7.1.4 Dainichiseika Color & Chemicals Mfg. Co. Ltd

- 7.1.5 Eastern Polypack Co. Ltd

- 7.1.6 Huhtamaki Flexible Packaging

- 7.1.7 Fagerdala Singapore Pte Ltd

- 7.1.8 Sealed Air Corporation

- 7.1.9 Amcor PLC

- 7.1.10 Toppan (Thailand) Co. Ltd

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 95 Pages

- 納期

- 2~3営業日