|

市場調査レポート

商品コード

1690709

弾力性フローリング:市場シェア分析、産業動向と統計、成長予測(2025~2030年)Resilient Flooring - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 弾力性フローリング:市場シェア分析、産業動向と統計、成長予測(2025~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

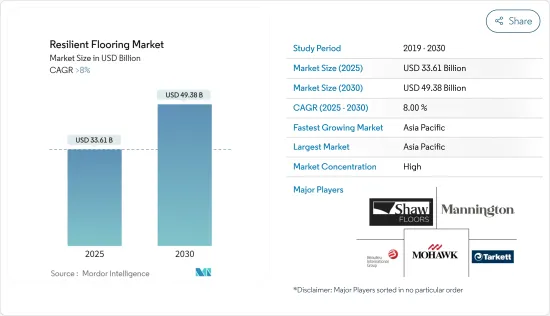

2025年の弾力性フローリング市場規模は336億1,000万米ドルと推定され、2030年には493億8,000万米ドルに達すると予測され、予測期間中(2025~2030年)のCAGRは8%を超えると予測されています。

COVID-19パンデミックは弾力性フローリング市場に悪影響を与えました。全国的なロックダウンと厳しい社会的避難措置により、世界中の住宅や商業施設の建設活動が停止し、その結果、弾力性フローリングの市場に影響を与えました。しかし、COVIDパンデミック後は、規制解除後、市場は順調に回復しました。世界中で商業と住宅建設活動が増加しているため、市場は大幅に回復しました。

商業施設における弾力性フローリングの用途の増加と高級ビニール弾力性フローリングの需要の増加が、弾力性フローリング市場を牽引すると予想されます。

フローリング製造時の環境への影響に対する懸念の高まりと他のフローリング製品の入手可能性が市場の成長を妨げると予想されます。

弾力性フローリングにおける技術革新の増加は、予測期間中に市場に機会を創出すると予想されます。

アジア太平洋は最大の市場を占めており、中国、インド、日本などの国々からの消費の増加により、予測期間中に最も急成長する市場になると予想されます。

弾力性フローリングの市場動向

住宅用途セグメントが市場を独占する

- 弾力性フローリングは高密度で非吸収性であり、表面に弾力性があるため歩行が快適です。さらに、弾力性フローリングは他のフローリングよりもメンテナンスが少なくて済みます。そのため、弾力性フローリングの需要は住宅で増加しています。

- 弾力性フローリングは、弾力性のないフローリングよりもはるかに安価であり、比較的に耐久性があるため、住宅や商業ビルにとって比較的費用対効果の高い選択肢となっています。住宅用建物のフローリングや製造プロセスにおけるカスタマイズへの注目の高まりは、住宅用建物の建設による弾力性フローリングの需要拡大に大きな影響を与えました。

- アジア太平洋と北米は、世界的に住宅建設が最も盛んな地域です。北米では、米国やカナダなどの国々で住宅建設活動が増加しており、これが弾力性フローリング市場を牽引しています。米国国勢調査局によると、米国における住宅建設の年間生産額は、2021年の8,020億米ドルに対し、2022年には9,080億米ドルとなりました。

- 同様にカナダでも、新規住宅建設プロジェクトが同国の弾力性フローリング市場を牽引すると予想されています。カナダの新設住宅着工戸数は、2023年第1四半期の4万6,851戸に対し、2023年第2四半期は6万4,042戸です。

- 同様に、欧州でも住宅建設が増加しています。ドイツは同地域最大の住宅建設市場です。同国の建設産業は成長を続けており、新築住宅建設活動の増加がその原動力となっています。例えば、Eurostatによると、建築建設収入は2022年に1,140億米ドルで登録され、2024年には1,254億米ドルに達すると予想されています。

- したがって、上記の要因から、住宅用途セグメントは予測期間中に弾力性フローリング市場を独占すると予想されます。

アジア太平洋が市場を独占する

- アジア太平洋は、予測期間中、弾力性フローリング市場を独占すると予想されます。中国、日本、インドなどの新興諸国では、住宅建設による弾力性フローリングへの需要の高まりと、商業セグメントでの用途の拡大が、この地域の弾力性フローリング需要を牽引すると予想されます。

- 中国はこの地域で最大の建設市場の一つです。中国国家統計局によると、建設生産額は2021年の29兆3,000億人民元(4兆2,000億米ドル)から2022年には31兆2,000億人民元(4兆5,000億米ドル)に増加します。中国は2030年までに建築物に13兆米ドル近くを費やすと予想されています。

- さらに、国内の可処分所得の増加が、ショッピングモール、ホテル、オフィスなどの豪華な商業地区の成長を促しています。中国は、ショッピングセンター建設における主要国のひとつです。中国には約4,000のショッピングセンターがあり、2025年までにさらに7,000がオープンすると推定されています。さらに、武漢佛山外灘中心T1のようなオフィススペースの建設が、中国での市場調査を後押しすると予想されます。建設工事は2021年第3四半期に開始され、2025年第4四半期に完了すると予測されています。

- 同様にインドでは、2023~2024年の予算により、Tier IIとTier IIIの都市に年間12億1,800万米ドルの都市インフラ開発資金が割り当てられています。これにより、質の高い都市インフラが整備されます。これはまた、住宅や商業施設の建設需要の増加につながり、弾力性フローリング市場を牽引することになります。

- 「世界建設2030」(Global Construction PerspectivesとOxford Economics発行)によると、東南アジアの建設市場は2030年までに1兆米ドルを超えると予想されており、これが住宅建設における弾力性フローリングの需要を押し上げます。

- 上記の要因から、アジア太平洋の弾力性フローリング市場は調査期間中に大きく成長すると予測されます。

弾力性フローリング産業概要

弾力性フローリング市場は、その性質上、部分的に統合されています。同市場の主要企業には、Beaulieu International Group、Mannington Mills Inc.、Mohawk Industries、Shaw Industries Group Inc.、Tarkettなどがあります(順不同)。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 商業施設における弾力性フローリングの用途拡大

- 高級ビニール弾力性フローリングの需要増加

- その他の促進要因

- 抑制要因

- フローリング製造時の環境影響に対する懸念の高まり

- その他のフローリング製品の入手可能性

- 産業バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション

- タイプ

- ビニルフローリング

- ポリ塩化ビニル(PVC)

- 充填材

- ビニールシート・フローリング

- ゴムフローリング

- リノリウム・フローリング

- その他(コルクフローリング、ビニル複合タイルなど)

- 用途

- 商業

- 住宅

- 施設

- 地域

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- マレーシア

- タイ

- インドネシア

- ベトナム

- その他のアジア太平洋

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- スペイン

- ノルディック

- トルコ

- ロシア

- その他の欧州

- 南米

- ブラジル

- アルゼンチン

- コロンビア

- その他の南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- ナイジェリア

- カタール

- エジプト

- アラブ首長国連邦

- その他の中東・アフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア(%)**/ランキング分析

- 主要企業の戦略

- 企業プロファイル

- AWI Licensing LLC

- Ardex Endura

- Beaulieu International Group

- Forbo Flooring Systems

- Gerflor.

- Interface, Inc

- Mannington Mills, Inc.

- Milliken & Company

- Mohawk Industries

- Nora

- Polyflor Ltd

- Shaw Industries Group, Inc

- Tarkett

- Unilin

第7章 市場機会と今後の動向

- 弾力性フローリングにおける技術革新の増加

- その他の機会

The Resilient Flooring Market size is estimated at USD 33.61 billion in 2025, and is expected to reach USD 49.38 billion by 2030, at a CAGR of greater than 8% during the forecast period (2025-2030).

The COVID-19 pandemic had negatively impacted the resilient flooring market. The nationwide lockdowns and strict social distancing measures had resulted in a halt in residential and commercial construction activities across the globe, thereby affecting the market for resilient flooring. However, post-COVID pandemic, the market recovered well after the restrictions were lifted. The market recovered significantly, owing to the increasing commercial and residential construction activities across the world.

The increasing application of resilient flooring at commercial places and the increasing demand for luxury vinyl resilient flooring are expected to drive the market for resilient flooring.

The increasing concern over environmental impact during the manufacturing of flooring materials and the availability of other flooring products are expected to hinder the market's growth.

The increasing innovations in resilient flooring are expected to create opportunities for the market during the forecast period.

The Asia-Pacific region represents the largest market and is also expected to be the fastest-growing market over the forecast period, owing to the increasing consumption from countries such as China, India, and Japan.

Resilient Flooring Market Trends

Residential Application Segment to Dominate the Market

- The resilient flooring system is denser and non-absorbent and ensures a pliant surface that makes walking comfortable. Additionally, resilient flooring also ensures less maintenance than other flooring. Thus, the demand for resilient flooring is increasing in residential buildings.

- Resilient flooring is a lot cheaper than non-resilient, and its comparably durable nature makes it a relatively cost-effective option for residential homes and commercial buildings. The increasing focus on customization in the flooring of residential buildings and manufacturing processes had a significant impact on the growing demand for resilient flooring from residential building construction.

- The Asia-Pacific and North America are the most significant regions for residential construction globally. In North America, residential construction activities are increasing in countries like the United States and Canada, which are driving the market for resilient flooring. According to the US Census Bureau, the annual value of residential construction output in the United States was valued at USD 908 billion in 2022, compared to USD 802 billion in 2021.

- Similarly, in Canada, new residential construction projects are expected to drive the country's market for resilient flooring. The number of new housing starts in Canada is registered at 64,042 units in Q2, 2023, compared to 46,851 units started in Q1, 2023.

- Similarly, in Europe, residential construction activities are increasing. Germany is the largest market for residential construction in the region. The country's construction industry has been growing and is driven by increasing new residential construction activities. For instance, according to Eurostat, the building construction revenue is registered at USD 114 billion in 2022 and is expected to reach USD 125.4 billion by 2024.

- Hence, owing to the factors mentioned above, the residential application segment is expected to dominate the resilient flooring market during the forecast period.

Asia-Pacific Region to Dominate the Market

- The Asia-Pacific region is expected to dominate the resilient flooring market during the forecast period. The rising demand for resilient flooring from residential building construction and growing application in the commercial sector in developing countries like China, Japan, and India is expected to drive the demand for resilient flooring in this region.

- China is one of the largest construction markets in the region. According to the National Bureau of Statistics of China, the value of construction output accounted for CNY 31.2 trillion (USD 4.5 trillion) in 2022, up from CNY 29.3 trillion (USD 4.2 trillion) in 2021. China is expected to spend nearly USD 13 trillion on buildings by 2030.

- Furthermore, the increasing disposable income in the country has triggered the growth of lavish commercial spaces like malls, hotels, offices, etc. China is one of the leading countries in the construction of shopping centers. China has almost 4,000 shopping centers, while 7,000 more are estimated to be open by 2025. Moreover, the construction of office spaces such as Wuhan Fosun Bund Center T1 in China is expected to boost the market studied. Construction work started in Q3 2021 and is forecasted to complete in Q4 2025.

- Similarly, in India, as per the Budget of 2023-2024, a dedicated amount of USD 1,218 million per annum has been allocated through urban infra-development funds for Tier II and Tier III cities. This will result in the creation of quality urban infrastructure. This will also translate to higher demand for housing and commercial construction activities, thereby driving the market for resilient flooring.

- According to Global Construction 2030 (published by Global Construction Perspectives and Oxford Economics), Southeast Asia's construction market is anticipated to exceed USD 1 trillion by 2030, which in turn boosts the demand for resilient flooring in residential building construction.

- Owing to the above-mentioned factors, the market for resilient flooring in the Asia-Pacific region is projected to grow significantly during the study period.

Resilient Flooring Industry Overview

The resilient flooring market is partially consolidated in nature. Some of the major players in the market include (not in any particular order) Beaulieu International Group, Mannington Mills Inc., Mohawk Industries, Shaw Industries Group Inc., and Tarkett.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Application of Resilient Flooring at Commercial Places

- 4.1.2 Increasing Demand for Luxury Vinyl Resilient Flooring

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Increasing Concern Over Environmental Impact During Manufacturing of Flooring Materials

- 4.2.2 The Availability of Other Flooring Products

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Type

- 5.1.1 Vinyl Flooring

- 5.1.2 Poly Vinyl Chloride (PVC)

- 5.1.3 Fillers

- 5.1.4 Vinyl Sheet Flooring

- 5.1.5 Rubber Flooring

- 5.1.6 Linoleum Flooring

- 5.1.7 Others (Cork Flooring, Vinyl Composite Tiles, etc.)

- 5.2 Application

- 5.2.1 Commercial

- 5.2.2 Residential

- 5.2.3 Institutional

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Malaysia

- 5.3.1.6 Thailand

- 5.3.1.7 Indonesia

- 5.3.1.8 Vietnam

- 5.3.1.9 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Spain

- 5.3.3.6 NORDIC

- 5.3.3.7 Turkey

- 5.3.3.8 Russia

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Nigeria

- 5.3.5.4 Qatar

- 5.3.5.5 Egypt

- 5.3.5.6 UAE

- 5.3.5.7 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 AWI Licensing LLC

- 6.4.2 Ardex Endura

- 6.4.3 Beaulieu International Group

- 6.4.4 Forbo Flooring Systems

- 6.4.5 Gerflor.

- 6.4.6 Interface, Inc

- 6.4.7 Mannington Mills, Inc.

- 6.4.8 Milliken & Company

- 6.4.9 Mohawk Industries

- 6.4.10 Nora

- 6.4.11 Polyflor Ltd

- 6.4.12 Shaw Industries Group, Inc

- 6.4.13 Tarkett

- 6.4.14 Unilin

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Innovations in Resilient Flooring

- 7.2 Other Opportunities