|

市場調査レポート

商品コード

1537606

氷結防止コーティング:市場シェア分析、産業動向・統計、成長予測(2024~2029年)Anti-icing Coating - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 氷結防止コーティング:市場シェア分析、産業動向・統計、成長予測(2024~2029年) |

|

出版日: 2024年08月14日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

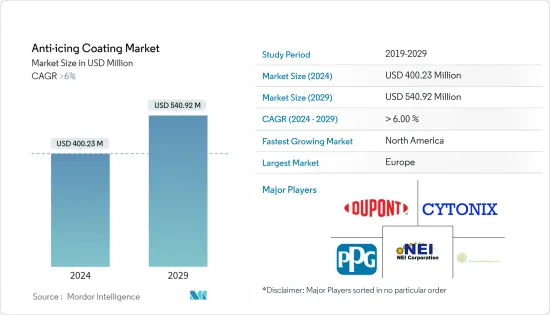

世界の氷結防止コーティングの市場規模は、2024年に4億23万米ドルに達し、2024~2029年の予測期間中にCAGR 6%以上で成長し、2029年には5億4,092万米ドルに達すると予測されています。

主なハイライト

- COVID-19パンデミックは、世界の閉鎖、厳しい社会的隔離措置、サプライチェーンの混乱により、市場に悪影響を及ぼしました。鎖国期間中に原材料価格が上昇したことも、氷結防止コーティング剤市場に悪影響を及ぼす一因となりました。

- しかし、規制解除後の市場は順調に回復しました。自動車、輸送、建設、IT・通信、再生可能エネルギー産業における氷結防止コーティング剤の消費増に牽引され、市場は大幅に回復しました。

- 自動車・航空宇宙分野からの需要の増加、寒冷地での需要の高さ、および氷結防止コーティングの優れた特性は、氷結防止コーティング市場を牽引すると予想されます。

- 費用対効果の高い代用品があることが、市場成長の妨げになると予想されます。

- 予測期間中、自己持続的な潤滑性凍結防止層の開拓が市場にチャンスをもたらすと期待されます。

- 欧州地域が市場を独占しているが、これは同地域の寒冷な気候条件下で氷結防止コーティングの用途が拡大しているためであり、これが氷結防止コーティングの需要を増大させています。

氷結防止コーティング市場動向

自動車産業と輸送産業が市場を独占

- 氷結防止コーティングは、エネルギーコストと消費量の削減、技術製品の性能向上、製品の安全性向上に貢献し、氷結防止コーティング市場を後押しします。

- 自動車・輸送産業は、寒冷な気候条件下で氷結防止コーティング剤が広く使用されていることから、支配的なセグメントとなっています。電気自動車イニシアチブのようなクリーンエネルギー閣僚会議(CEM)の下でのイニシアチブや電気自動車の人気の高まりは、近い将来、氷結防止コーティング剤の消費を促進すると思われます。

- 世界の自動車生産台数の増加が、氷結防止コーティング剤市場を牽引すると予想されます。国際自動車製造者機構(OICA)によると、世界の自動車生産台数は2021年の8,021万台に対し、2022年には8,501万台に達し、成長率は6%です。中国、米国、インドが世界で最も顕著な自動車市場です。

- 中国は、自動車とその部品の生産・輸出で世界をリードしています。中国は引き続き世界最大の自動車市場です。OICAによると、中国の自動車生産台数は2022年に合計2,702万台に達し、同時期の前年比3%増となった。

- 米国は中国に次ぐ世界第2位の自動車市場で、世界の自動車市場で大きなシェアを占めています。OICAによると、2022年の米国自動車生産台数は、2021年の生産台数915万台に対し1,006万台に達し、成長率は9%に達しました。これにより自動車産業の成長が促進され、氷結防止コーティングの市場需要が刺激されました。

- さらに最近では、航空機メーカーが受注残を埋めるために生産を加速する方法を模索しています。例えば、Boeing Commercial Outlook 2022-2041によると、新型航空機の世界総納入数は2041年までに4万1,170機になると推定されています。従って、航空機生産の増加が現在の研究市場を牽引すると予想されます。

- したがって、上記の要因から、自動車および輸送のエンドユーザー産業が氷結防止コーティング市場を牽引すると予想されます。

欧州地域が市場を独占

- 欧州地域は、氷結防止コーティング剤市場を独占すると予想されます。航空宇宙、通信、送電線、建設、オフショアプラットフォームなど、多くの産業で用途が拡大していることが、氷結防止コーティング剤の需要を促進すると予想されます。

- ドイツの自動車製造業は、欧州地域の自動車生産全体の中で有数の株主です。同国は、Volkswagen, Mercedes-Benz, Audi, BMW, Porscheなど、主要な自動車製造ブランドを擁しています。OICAによると、自動車と小型商用車の総生産台数は、2021年の330万台に対し、2022年には367万台に達し、成長率は11%です。そのため、このような自動車産業の成長も、氷結防止コーティング剤の需要を牽引しています。

- 同様にフランスでも、自動車産業は大きな成長率を記録しました。OICAによると、同国の2022年の自動車総生産台数は138万台で、前年比2%の成長を記録しました。乗用車、小型商用車、大型商用車、バス、コーチは、車両コストの上昇により、2022年の販売台数が減少しました。

- ドイツは欧州で最も建設産業が盛んな国です。同国の建設産業は、新規住宅建設活動の増加に牽引され、緩やかな成長を続けています。例えば、Eurostatによると、2022年の建築建設収入は1,140億米ドルで、2024年には1,254億米ドルに達すると予想されています。このように、建設産業の成長が現在の研究市場を牽引する可能性が高いです。

- 欧州では、航空交通量の増加に伴い、航空機の需要が増加しています。Boeing Commercial Outlook 2022-2041によると、2041年までに新型航空機の納入総数は8,550機、市場サービス額は8,500億米ドルに達すると推定され、それによって同地域の氷結防止コーティング剤需要が増加しています。

- 氷結防止コーティングは、機械的強度への着氷の影響から保護し、メンテナンスコストを削減し、円滑な運転を確保するために、風力タービンのローターブレードに広く使用されています。欧州では風力発電容量が増加しています。2022年、欧州は新たに19ギガワットの風力発電容量を設置しました。さらに欧州は、2023~2027年にかけて129GW(ギガワット)の新規風力発電所の設置を目指しています。したがって、風力エネルギー分野の成長は、同地域の氷結防止コーティング市場を牽引すると予想されます。

- したがって、このような市場動向はすべて、予測期間中に同地域の氷結防止コーティング市場の需要を促進すると予想されます。

氷結防止コーティング産業の概要

氷結防止コーティング市場は部分的に統合されています。同市場の主要企業としては、NEI Corporation、Cytonix、PPG Industries, Inc.、DuPont、NanoSonic, Inc.などが挙げられます(順不同)。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 自動車・航空宇宙分野からの需要拡大

- 寒冷地における高い需要

- 氷結防止コーティングの優れた特性

- 抑制要因

- 費用対効果の高い代替品の入手可能性

- その他の抑制要因

- 産業バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション(市場規模:金額ベース)

- 基板

- 金属

- ガラス

- セラミックス

- コンクリート

- エンドユーザー産業

- 自動車・輸送

- 建設

- 通信

- 再生可能エネルギー

- その他のエンドユーザー産業

- 地域

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他のアジア太平洋

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- その他の欧州

- その他の地域

- 南米

- 中東・アフリカ

- アジア太平洋

第6章 競合情勢

- 合併・買収、合弁事業、提携、協定

- 市場シェア(%)**/ランキング分析

- 主要企業の戦略

- 企業プロファイル

- Aerospace & Advanced Composites GmbH

- Battelle Memorial Institute

- CG2 Nanocoatings

- Cytonix

- DuPont

- Fraunhofer

- Helicity Technologies, Inc.

- HygraTek

- NanoSonic, Inc.

- NEI Corporation

- Opus Materials Technologies

- PPG Industries, Inc.

第7章 市場機会と今後の動向

- 持続可能な自己潤滑氷結防止層の開発

- その他の機会

目次

Product Code: 69435

The Anti-icing Coating Market size is estimated at USD 400.23 million in 2024, and is expected to reach USD 540.92 million by 2029, growing at a CAGR of greater than 6% during the forecast period (2024-2029).

Key Highlights

- The COVID-19 pandemic negatively impacted the market due to worldwide lockdowns, strict social distancing measures, and disruptions in supply chains, which had adverse effects on the market for anti-icing coatings. The prices of raw materials increased during the lockdown, further contributing to the negative impact on the anti-icing coatings market.

- However, the market recovered well after the restrictions were lifted. It rebounded significantly, driven by increased consumption of anti-icing coatings in the automotive, transportation, construction, telecommunication, and renewable energy industries.

- The growing demand from the automotive and aerospace sectors, high demand in cold climatic conditions, and the superior properties of anti-icing coatings are expected to drive the market for anti-icing coatings.

- The availability of cost-effective alternate substitutes for anti-icing coatings is expected to hinder market growth.

- The development of a self-sustainable lubricating anti-icing layer is expected to create opportunities for the market during the forecast period.

- The European region dominates the market, owing to the growing application of anti-icing coatings in cold climatic conditions in the region, which augments the demand for anti-icing coatings.

Anti-Icing Coating Market Trends

Automotive and Transportation Industries to Dominate The Market

- Anti-icing coatings help reduce the cost and consumption of energy, enhance the performance of technical goods, and contribute to product safety, which will provide a boost to the anti-icing coating market.

- The automotive and transportation industry stands to be the dominant segment owing to the extensive consumption of anti-icing coatings in vehicles under cold climatic conditions. The initiatives under the Clean Energy Ministerial (CEM), like the electric vehicle initiative and the growing popularity of electric vehicles, are likely to drive the consumption of anti-icing coatings in the near future.

- The increase in the global production of automotive vehicles is expected to drive the market for anti-icing coatings. According to the Organisation Internationale des Constructeurs d'Automobiles (OICA), global automotive vehicle production reached 85.01 million in 2022, compared to 80.21 million manufactured in 2021, at a growth rate of 6%. China, the United States, and India are the most prominent automotive vehicle markets globally.

- China is the world's leading producer and exporter of automobiles and their parts. China continues to be the world's largest vehicle market. According to OICA, automotive vehicle production in China reached a total of 27.02 million units in 2022, an increase of 3% over the previous year for the same period.

- The United States is the second-largest automotive market in the world after China, which occupies a significant share of the global automotive vehicles market. According to OICA, in 2022, the United States automotive vehicle production reached 10.06 million compared to 9.15 million units manufactured in 2021, at a growth rate of 9%. This enhanced the growth of the automobile industry, which has stimulated the market demand for anti-icing coatings.

- Furthermore, recently, aircraft manufacturers have been looking for ways to accelerate production to fill order backlogs. For instance, according to the Boeing Commercial Outlook 2022-2041, the total global deliveries of new airplanes are estimated to be 41,170 by 2041. Thus, the increased aircraft production is expected to drive the current studied market.

- Hence, owing to the above-mentioned factors, the automotive and transportation end-user industry is expected to drive the market for anti-icing coatings.

Europe Region to Dominate the Market

- The European region is expected to dominate the market for anti-icing coatings. The increasing application in many industries, including aerospace, telecommunications, power lines, construction, and offshore platforms, is expected to propel the demand for anti-icing coatings.

- The automobile manufacturing industry in Germany is a prominent shareholder of the overall automotive production in the European region. The country hosts major car-making brands, including Volkswagen, Mercedes-Benz, Audi, BMW, Porsche, etc. According to OICA, the total production volume of cars and light commercial vehicles reached 3.67 million units in 2022, compared to 3.30 million units manufactured in 2021, at a growth rate of 11%. Therefore, such growth in the automotive industry has also been driving the demand for anti-icing coatings.

- Similarly, in France, the automotive industry registered a significant growth rate. According to OICA, the total production of vehicles in the country amounted to 1.38 million units in 2022, registering a growth of 2% from the previous year. Passenger cars, light commercial vehicles, heavy commercial vehicles, buses, and coaches witnessed a decline in 2022 sales in the country owing to the growing cost of vehicles.

- Germany has the most significant construction industry in Europe. The country's construction industry has been growing slowly, driven by increasing new residential construction activities. For instance, according to Eurostat, the building construction revenue is registered at USD 114 billion in 2022 and is expected to reach USD 125.4 billion by 2024. Thus, growth in the construction industry is likely to drive the current studied market.

- In Europe, with the increase in air traffic, the demand for aeroplanes is increasing in the country. According to the Boeing Commercial Outlook 2022-2041, the total deliveries of new airplanes are estimated to be 8,550 units by 2041, with a market service value of USD 850 billion, thereby increasing the demand for anti-icing coatings in the region.

- Anti-icing coatings are widely used on rotor blades of wind turbines to protect against the effect of icing on mechanical strength, reduce maintenance costs, and ensure smooth operations. Europe is increasing its wind energy generation capacity. In 2022, Europe installed 19 gigawatts of new wind energy capacity. Furthermore, Europe aims to install 129 GW (gigawatts) of new wind farms over the period 2023-2027. Thus, the growth in the wind energy sector is expected to drive the anti-icing coating market in the region.

- Hence, all such market trends are expected to drive the demand for the anti-icing coating market in the region during the forecast period.

Anti-Icing Coating Industry Overview

The anti-icing coating market is partially consolidated in nature. Some of the major players in the market include (not in any particular order) NEI Corporation, Cytonix, PPG Industries, Inc., DuPont, and NanoSonic, Inc., amongst others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing demand from Automotive and Aerospace Sector

- 4.1.2 High Demand in Cold Climatic Conditions

- 4.1.3 Superior Properties of Anti-icing Coatings

- 4.2 Restraints

- 4.2.1 Availability of Cost-Effective Alternate Substitutes

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Substrate

- 5.1.1 Metal

- 5.1.2 Glass

- 5.1.3 Ceramics

- 5.1.4 Concrete

- 5.2 End User Industry

- 5.2.1 Automotive and Transportation

- 5.2.2 Construction

- 5.2.3 Telecommunication

- 5.2.4 Renewable Energy

- 5.2.5 Other End-User Industries (Marine, Industrial, etc.)

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 Rest of the World

- 5.3.4.1 South America

- 5.3.4.2 Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Aerospace & Advanced Composites GmbH

- 6.4.2 Battelle Memorial Institute

- 6.4.3 CG2 Nanocoatings

- 6.4.4 Cytonix

- 6.4.5 DuPont

- 6.4.6 Fraunhofer

- 6.4.7 Helicity Technologies, Inc.

- 6.4.8 HygraTek

- 6.4.9 NanoSonic, Inc.

- 6.4.10 NEI Corporation

- 6.4.11 Opus Materials Technologies

- 6.4.12 PPG Industries, Inc.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Development of Self Sustainable Lubricating Anti-Icing Layer

- 7.2 Other Opportunities