コネクテッドトラック:市場シェア分析、産業動向と統計、成長予測(2024~2029年)

Connected Truck - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1536938

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

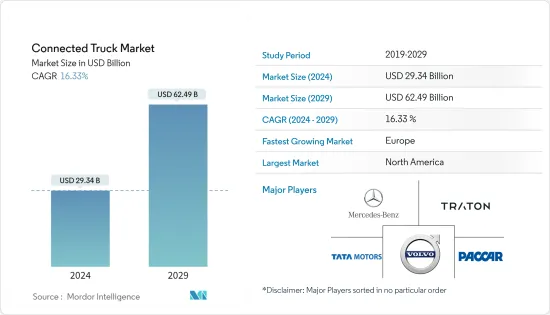

コネクテッドトラック市場規模は2024年に293億4,000万米ドルと推定され、2029年には624億9,000万米ドルに達すると予測され、予測期間中(2024-2029年)のCAGRは16.33%で成長する見込みです。

コネクテッドトラック市場は、輸送・物流分野への先端技術の急速な統合によって力強い成長を遂げています。商用車におけるテレマティクスソリューション、IoT対応コネクティビティ、データ分析アプリケーションに対する需要の急増が市場を特徴づけています。主な促進要因としては、車両管理の効率化、安全性の向上、厳しい排出ガス基準や規制基準の遵守に対するニーズが挙げられます。

eコマースの台頭と産業化の進展が、商用車のリアルタイム追跡、遠隔診断、予知保全の需要を促進しています。フリートオペレーターは、ルートを最適化し、 ドライバーの行動をモニターし、ダウンタイムを最小化し、全体的な業務効率を改善するために、コネクテッドトラックテクノロジーをますます採用するようになっています。コネクテッドトラック技術を通じて、フリートオペレーターは、燃料、メンテナンス、 ドライバーの賃金など、総所有コストの60%以上を占める要素の最適化を期待しています。今後5年以内に、世界で3,500万台以上のトラックがコネクテッドトラックになると予想されています。

さらに、北米と欧州は、確立されたインフラと規制枠組みに後押しされ、コネクテッドトラック市場を独占しています。しかし、アジア太平洋地域は、新興経済圏におけるコネクテッドソリューションの採用増加により、潜在的な市場として台頭しつつあります。市場情勢は激しい競合によって特徴付けられ、主要企業は競争優位を得るために戦略的提携、パートナーシップ、製品イノベーションに注力しています。例えば

2023年5月、ダイムラートラック、MFTBC、日野自動車、トヨタの4社は、CASE技術(コネクテッド/自律・自動運転/シェアード/電動)の開発と商用車事業の世界規模での強化により、カーボンニュートラルの達成と豊かなモビリティ社会の実現を目指して提携しました。MFTBCと日野はシナジーを創出し、日本のトラックメーカーの競争力を強化します。

有望な成長にもかかわらず、データセキュリティの懸念、相互運用性の問題、初期導入コストなどの課題が、市場拡大の潜在的な障壁となっています。しかし、現在進行中の技術的進歩や、スマート交通を推進する政府の有利な取り組みが、コネクテッドトラック市場の明るい軌道を維持すると予想されます。

コネクテッドトラック市場の動向

商用車市場におけるテレマティクス利用の増加がコネクテッドトラック市場を牽引

テレマティクスは、効率的なサプライチェーンロジスティクスと車両管理のための独自のソリューションを開発する上で重要な役割を果たしています。テレマティクスはリアルタイムの可視性とデータを提供し、手順とプロセスの最適化、製品の完全性の維持、賞味期限の最適化、サプライチェーン全体の損失と保険リスクの低減を実現します。

テレマティクスは、安全性や規制の遵守、 ドライバーのモニタリング、保険、インフラに関する重要な課題に対処するため、商業ロジスティクスやサプライチェーンにおいて重要な要素となりつつあります。

テレマティクスソリューションは、ライブ交通情報、スマートルーティングとトラッキング、事故や故障時の迅速なロードサイドアシスタンス、自動料金決済、保険テレマティクスなどの機能を統合しています。そのため、燃料コストの削減、リソースの最適化、リアルタイムの接続性など、車両の運行指標の最適化には不可欠です。

eコマース部門の成長とオンラインショッピング活動の増加も、コネクテッドトラックの需要拡大に大きく寄与しています。2022年の世界の小売eコマース売上高は6兆米ドルを超え、年間成長率は11.16%を記録しました。アジア諸国だけでも、2022年のオンライン小売総売上は1兆7,000億米ドル近くに上ります。

さらに、ほとんどのeコマース企業は自社で物流業務を行い、テレマティクス制御ユニットを組み込んだコネクテッドトラックの大規模なフリートを発注しています。テレマティクス・コントロール・ユニットを搭載したトラックは、安全性、車両性能、燃料効率、 ドライバーの行動、予知保全のためにトラックを遠隔監視することを可能にします。例えば

アマゾンは2022年10月、今後5年間で欧州全域の電気バン、トラック、低排出ガスパッケージハブに10億ユーロを投資すると発表しました。これらの車両には、テレマティクスのような次世代コネクテッドテクノロジーも搭載されます。同社は、電気バンとコネクテッドバンの保有台数を3,000台から10,000台に増やすことを目指しています。同社はまた、中距離配送用に欧州で1,500台の大型電気トラックを配備する計画です。

さらに、企業はテレマティクス技術の高度化と商用車へのテレマティクスデバイスの統合に巨額の費用を投じています。例えば

と北米ダイムラートラック社は、2022年10月に新たな提携を発表し、Lytx Inc.は北米で販売されるウェスタンスターとフレートライナーの一部モデルに工場装着される新しいテレマティクスとカメラのソリューションを発表しました。

上記のすべての要因に基づき、テレマティクスの利用拡大とeコマース企業からの大規模な車両発注が、予測期間中のコネクテッドトラック市場の成長を促進すると予想されます。

北米と欧州がコネクテッドトラック市場の成長で重要な役割を果たす

地域的には、欧州と北米がコネクテッドトラック市場の主要シェアを占めています。両地域の強固な輸送インフラは、コネクテッドテクノロジーをトラック輸送業務に統合するための強固な基盤を提供しています。さらに、よく発達した道路網と通信システムは、商用車におけるテレマティクスソリューション、リアルタイム追跡、データ駆動型分析のシームレスな実装を促進します。

さらに、北米と欧州における厳しい規制環境は、コネクテッドトラック・ソリューションの採用を推進する上で極めて重要な役割を果たしています。安全性、排出ガス、燃費基準に対応する規制は、リアルタイムのモニタリングとコンプライアンスを可能にする先進技術の必要性を高めています。例えば、北米のACF(Advanced Clean Fleets)規制は、2024年1月1日から、カリフォルニア州でドレージ活動を行うには、トラックをCARB(カリフォルニア大気資源局)オンラインシステムに登録しなければならないとしています。

業界の協力体制もまた、これらの地域の優位性に貢献している重要な要素です。主要トラックメーカー、テクノロジープロバイダー、およびフリート管理会社は戦略的パートナーシップを獲得し、コネクテッドトラック・ソリューションの開発と展開を加速させています。北米全域の主要な電気通信企業は、主要なコネクテッドトラック企業と提携し、その製品ポートフォリオを拡大しています。例えば

2022年10月、コネクテッドトラック・サービスのリーダーで北米最大の官民計量所バイパス・ネットワークを運営するDrivewyzeは、通信大手のVerizon Connectと提携し、Verizon Connect Revealの顧客にDrivewyze計量所バイパスとDrivewyze Safety+サービスへの統合アクセスを提供します。

アジア太平洋におけるコネクテッドトラックの需要は、同地域の経済が急成長し、スマート輸送ソリューションが重視されるようになったことから、今後5年間で急成長すると予想されています。中国政府は、ADAS機能や電動モビリティなど、いくつかの先進車両技術に注力しています。同国の主要自動車メーカーは、新しいレベル2およびレベル3のADAS機能を導入することで、ポートフォリオを更新しています。例えば

2022年7月、東風成龍H5は中国初の大型自律走行トラックの認可を取得しました。Chenglong H5の遠隔運転システムはChina Mobileの5Gネットワークで稼働します。

現在は北米と欧州がリードしているが、予測期間中に他の地域、特にアジア太平洋が成長ペースに追いつくと予想されます。

コネクテッドトラック産業の概要

コネクテッドトラック市場は、Daimler Truck SE、Traton SE、Tata Motors Ltd、Volvo Trucks Corporation、PACCARを含む少数の世界的企業によって統合され、主に支配されています。これらの企業は、ブランドポートフォリオを拡大し、市場での地位を固めるために、合弁事業、M&A、新製品の発売、製品開拓も行っています。

例えば、2022年10月、Aurora Innovation Inc.とRyder Technology Inc.は、現場での車両メンテナンスを試験的に行うために協力しました。ライダーは、オーロラのサウス・ダラス・キャンパスでオーロラの技術者と共に働く熟練技術者を雇用します。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場促進要因

- 商用車へのコネクテッド技術搭載を義務付ける政府規範が成長を促進

- その他の促進要因

- 市場抑制要因

- 新興国におけるITインフラ不足がコネクテッドトラック市場の成長を抑制

- サイバーセキュリティの脅威が引き続き市場の懸念材料に

- 業界の魅力- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 車両タイプ

- 小型商用車

- 大型商用車

- 通信距離

- 専用近距離通信(DSRC)

- 死角警報(BSW)

- 前方衝突警報(FCW)

- 車線逸脱警報(LDW)

- 緊急ブレーキアシスト(EBA)

- その他の通信距離

- 長距離(テレマティクス・コントロール・ユニット)

- 専用近距離通信(DSRC)

- 通信タイプ

- 車両間通信(V2V)

- 車両対クラウド(V2C)

- 車両対インフラ(V2I)

- 地域別

- 北米

- 米国

- カナダ

- その他北米

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋地域

- 世界のその他の地域

- 南米

- 中東・アフリカ

- 北米

第6章 競合情勢

- ベンダー市場シェア

- 企業プロファイル

- Robert Bosch GmbH

- Continental AG

- Denso Corporation

- Aptiv Global Operations Limited

- ZF Friedrichshafen AG

- NXP Semiconductors NV

- Magna International Inc.

- Sierra Wireless

- Mercedes-Benz Group AG

- AB Volvo

- Harman International

第7章 市場機会と今後の動向

- 自動車における5Gとクラウド基盤技術の融合が今後の動向となる

第8章 市場規模(台数ベース)と予測

第9章 コネクテッドトラック市場における技術動向とイノベーションの分析

第10章 コネクテッドトラック市場に影響を与える規制枠組みの分析

目次

The Connected Truck Market size is estimated at USD 29.34 billion in 2024, and is expected to reach USD 62.49 billion by 2029, growing at a CAGR of 16.33% during the forecast period (2024-2029).

The connected truck market is experiencing robust growth, fuelled by the rapid integration of advanced technologies into the transportation and logistics sector. A surge in demand for telematics solutions, IoT-enabled connectivity, and data analytics applications in commercial vehicles characterizes the market. Key drivers include the need for enhanced fleet management efficiency, improved safety, and compliance with stringent emissions and regulatory standards.

The rise of e-commerce and increasing industrialization are driving the demand for real-time tracking, remote diagnostics, and predictive maintenance in commercial vehicles. Fleet operators increasingly adopt connected truck technologies to optimize routes, monitor driver behavior, and minimize downtime, improving overall operational efficiency. Through connected truck technology, fleet operators anticipate optimizing factors, such as fuel, maintenance, and wages of drivers, which together contribute more than 60% of the total cost of ownership. More than 35 million trucks globally are expected to be connected within the next five years.

Furthermore, North America and Europe dominate the connected truck market, propelled by established infrastructure and regulatory frameworks. However, the Asia-Pacific region is emerging as a potential market with the increasing adoption of connected solutions in emerging economies. The market landscape is characterized by intense competition, with major players focusing on strategic collaborations, partnerships, and product innovations to gain a competitive edge. For instance,

In May 2023, Daimler Truck, MFTBC, Hino, and Toyota joined hands to achieve carbon neutrality and create a prosperous mobility society by developing CASE technologies (Connected / Autonomous & Automated / Shared / Electric) and strengthening the commercial vehicle business on a global scale. MFTBC and Hino would create synergies and enhance the competitiveness of Japanese truck manufacturers.

Despite the promising growth, challenges such as data security concerns, interoperability issues, and initial implementation costs pose potential barriers to market expansion. However, ongoing technological advancements and favorable government initiatives promoting smart transportation are expected to sustain the positive trajectory of the connected truck market.

Connected Truck Market Trends

Increasing Use of Telematics in the Commercial Vehicle Market to Drive the Connected Truck Market

Telematics plays a significant role in developing unique solutions for efficient supply chain logistics and fleet management. Telematics provides real-time visibility and data to optimize procedures and processes, maintain product integrity, optimize shelf-life, and reduce losses and insurance risks across the supply chain.

Telematics is becoming a critical component in commercial logistics and supply chains because it addresses key challenges related to safety and regulatory compliance, driver monitoring, insurance, and infrastructure.

Telematics solutions integrate capabilities like live traffic updates, smart routing and tracking, rapid roadside assistance in case of accidents or breakdowns, automatic toll transactions, and insurance telematics. Therefore, they are critical to optimizing the operational metrics of fleets, such as fuel cost reduction, resource optimization, and real-time connectivity.

The growing e-commerce sector and increased online shopping activities also significantly contribute to the growing demand for connected trucks. Retail e-commerce sales worldwide in 2022 remained over USD 6 trillion, registering an annual growth rate of 11.16%. The total online retail revenue in Asian countries alone added up to nearly USD 1.7 trillion in 2022.

Additionally, most e-commerce companies have in-house logistics operations and are ordering large fleets of connected trucks incorporating telematics control units. Trucks with telematics control units enable them to monitor trucks remotely for safety, fleet performance, fuel efficiency, the behavior of drivers, and predictive maintenance. For instance,

In October 2022, Amazon announced it would invest EUR 1 billion in electric vans, trucks, and low-emission package hubs across Europe over the next five years. These vehicles also feature next-generation connected technologies like telematics. The company aims to increase its electric and connected vans fleet from 3,000 to 10,000. The company also plans to deploy 1,500 heavy-duty electric trucks in Europe for middle-mile deliveries.

Moreover, companies are spending huge amounts on making telematics technology more advanced and integrating telematics devices in commercial vehicles. For instance,

In October 2022, Lytx Inc. and Daimler Trucks, North America, announced their new partnership wherein Lytx Inc. would launch a new telematics and camera solution factory-fitted on select Western Star and Freightliner models sold in North America.

Based on all the above factors, the growing usage of telematics and the large fleet orders from e-commerce companies are expected to drive the growth of the connected trucks market over the forecast period.

North America and Europe are Playing Key Role in the Connected Truck Market Growth

Geographically, Europe and North America hold the major shares of the connected truck market, owing to the expansion of the automotive sector in these regions. The robust transportation infrastructures in both regions provide a solid foundation for integrating connected technologies into trucking operations. Additionally, well-developed road networks and communication systems facilitate the seamless implementation of telematics solutions, real-time tracking, and data-driven analytics in commercial vehicles.

Furthermore, stringent regulatory environments in North America and Europe play a pivotal role in propelling the adoption of connected truck solutions. Regulations addressing safety, emissions, and fuel efficiency standards drive the need for advanced technologies that enable real-time monitoring and compliance. For instance, North America's Advanced Clean Fleets (ACF) regulation states that beginning January 1, 2024, trucks must be registered in the CARB (California Air Resources Board) Online System to conduct drayage activities in California.

Industry collaboration is another key factor contributing to the dominance of these regions. Major truck manufacturers, technology providers, and fleet management companies have garnered strategic partnerships, accelerating the development and deployment of connected truck solutions. Major telecom companies across North America are partnering with leading connected truck companies to expand their product portfolios. For instance,

In October 2022, Drivewyze, the leader in connected truck services and operator of the largest public-private weigh station bypass network in North America, partnered with telecom major Verizon Connect to provide Verizon Connect Reveal customers with integrated access to Drivewyze weigh station bypass and Drivewyze Safety+ services.

The demand for connected trucks in Asia-Pacific is anticipated to grow rapidly over the next five years owing to the region's burgeoning economies and increasing emphasis on smart transportation solutions. The Chinese government focuses on several advanced vehicle technologies, like ADAS features and electric mobility. Major automakers in the country are updating their portfolio by introducing the new level 2 and level 3 ADAS features. For instance,

In July 2022, the Dongfeng Chenglong H5 was licensed for its first heavy-duty autonomous truck in China. The Chenglong H5's remote driving system runs on China Mobile's 5G network.

While North America and Europe currently lead the way, other regions, particularly the Asia-Pacific, are expected to catch up with the growth pace during the forecast period.

Connected Truck Indsutry Overview

The connected truck market is consolidated and majorly dominated by a few global players, which include Daimler Truck SE, Traton SE, Tata Motors Ltd, Volvo Trucks Corporation, and PACCAR. These players also engage in joint ventures, mergers and acquisitions, new product launches, and product development to expand their brand portfolios and cement their market positions.

For instance, in October 2022, Aurora Innovation Inc. and Ryder Technology Inc. collaborated to pilot on-site fleet maintenance. Ryder would embed skilled technicians to work alongside Aurora technicians at Aurora's South Dallas campus.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.1.1 Government Norms Mandating the Integration of Connected Technologies in Commercial Vehicles are Driving the Growth

- 4.1.2 Other Drivers

- 4.2 Market Restraints

- 4.2.1 Lack of IT Enabled Infrastructure in Emerging Economies Restricts the Connected Truck Market Growth

- 4.2.2 Cyber Security Threats Remain a Concern for the Market

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD Billion)

- 5.1 Vehicle Type

- 5.1.1 Light Commercial Vehicles

- 5.1.2 Heavy Commercial Vehicles

- 5.2 Range

- 5.2.1 Dedicated Short-Range Communication (DSRC)

- 5.2.1.1 Blind Spot Warning (BSW)

- 5.2.1.2 Forward Collision Warning (FCW)

- 5.2.1.3 Lane Departure Warning (LDW)

- 5.2.1.4 Emergency Brake Assist (EBA)

- 5.2.1.5 Other Ranges

- 5.2.2 Long-range (Telematics Control Unit)

- 5.2.1 Dedicated Short-Range Communication (DSRC)

- 5.3 Communication Type

- 5.3.1 Vehicle-to-Vehicle (V2V)

- 5.3.2 Vehicle-to-Cloud (V2C)

- 5.3.3 Vehicle-to-Infrastructure (V2I)

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Rest of North America

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 Rest of Asia-Pacific

- 5.4.4 Rest of the World

- 5.4.4.1 South America

- 5.4.4.2 Middle-East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles*

- 6.2.1 Robert Bosch GmbH

- 6.2.2 Continental AG

- 6.2.3 Denso Corporation

- 6.2.4 Aptiv Global Operations Limited

- 6.2.5 ZF Friedrichshafen AG

- 6.2.6 NXP Semiconductors NV

- 6.2.7 Magna International Inc.

- 6.2.8 Sierra Wireless

- 6.2.9 Mercedes-Benz Group AG

- 6.2.10 AB Volvo

- 6.2.11 Harman International

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Integration of 5G and Cloud-based Technology in Automobiles to be a Future Trend

8 MARKET SIZE AND FORECAST IN TERMS OF VOLUME

9 ANALYSIS OF THE TECHNOLOGICAL TRENDS AND INNOVATIONS WITHIN THE CONNECTED TRUCK MARKET

10 ANALYSIS OF REGULATORY FRAMEWORKS IMPACTING THE CONNECTED TRUCK MARKET

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日