|

市場調査レポート

商品コード

1876795

コネクテッドトラック市場の機会、成長要因、業界動向分析、および2025年から2034年までの予測Connected Trucks Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| コネクテッドトラック市場の機会、成長要因、業界動向分析、および2025年から2034年までの予測 |

|

出版日: 2025年11月04日

発行: Global Market Insights Inc.

ページ情報: 英文 280 Pages

納期: 2~3営業日

|

概要

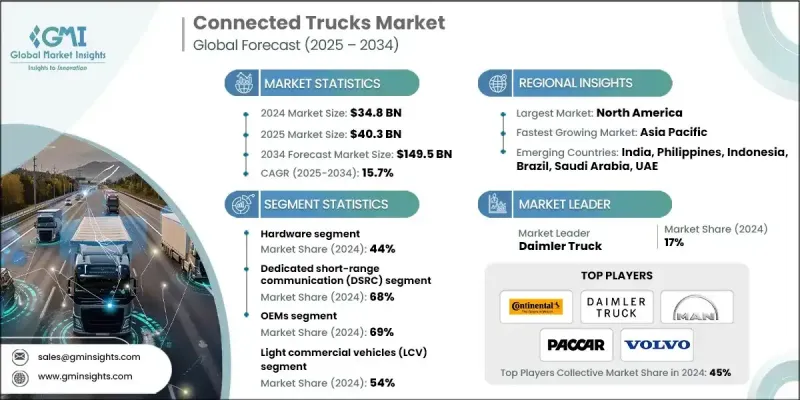

世界のコネクテッドトラック市場は、2024年に348億米ドルと評価され、2034年までにCAGR15.7%で成長し、1,495億米ドルに達すると予測されています。

コネクテッドトラック技術への需要の高まりは、世界中の物流および長距離輸送ネットワークの在り方を変革しております。高度なテレマティクス、予測型フリート分析、車内接続性により、オペレーターがルートを監視し、配送時間を予測し、積載を最適化し、アイドリングや空荷走行を最小化する手法が変革されております。デジタルツインシミュレーションの活用により、フリート管理者やOEMメーカーは運用モデルを仮想的にテストでき、コスト削減、安全性向上、配送信頼性の改善につながります。業界が電気自動車や低排出ガス車両への移行を進める中、コネクテッドトラックプラットフォームはエネルギー配分の管理、充電スケジュールの調整、航続距離効率の最適化に活用されています。スマート充電システムとV2G(車両から電力網への通信)システムの統合により、エネルギー使用の均衡化と電力網への負荷軽減が実現されます。さらに、混合フリート運用においては、接続システムにより動的な負荷分散とルート最適化が可能となり、バッテリー寿命の維持に貢献します。自動ブレーキ、車線維持、トラック・プラトーニングなどのADASの急速な統合は、信頼性の高い低遅延接続の重要性をさらに強調しています。OEMおよびフリート運営者は、センサーフュージョンとクラウド分析への投資を拡大し、リアルタイムデータを実用的な安全性とコンプライアンスの知見へと転換しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年度 | 2025-2034 |

| 開始時価値 | 348億米ドル |

| 予測金額 | 1,495億米ドル |

| CAGR | 15.7% |

ハードウェアセグメントは2024年に44%のシェアを占め、2034年までCAGR 13.9%で成長すると予測されています。ハードウェアは、接続性、通信、テレマティクス統合を可能にする不可欠な基盤を形成するため、引き続き市場をリードしています。テレマティクス制御ユニット(TCU)、GPS/GNSSデバイス、センサー、無線通信モジュールなどの主要コンポーネントは、リアルタイムの運用データを収集・伝送する基盤として機能します。これらのシステムは、車両、クラウドプラットフォーム、フリート管理ネットワーク間のシームレスな相互運用を支え、デジタル輸送エコシステムを駆動する物理層を形成しています。

専用近距離通信(DSRC)セグメントは2024年に68%のシェアを占め、2025年から2034年にかけてCAGR15.1%で成長すると予測されています。DSRC技術は、堅牢な性能と低遅延性を備えていることから、接続型トラック向けの優先通信方式として位置づけられています。これらの特性は、リアルタイムの車両間通信(V2V)および車両とインフラ間通信(V2I)において極めて重要です。これにより、衝突検知、車線変更警報、緊急対応システムなど、安全性を高めるアプリケーションにおける瞬時のデータ交換が可能となります。その実証済みの信頼性と規制適合性は、現代のトラック輸送業務における採用をさらに強化し続けています。

米国接続型トラック市場は85%のシェアを占め、2024年には123億米ドルの規模に達しました。米国市場は、先進的接続システムの早期導入、広範なテレマティクスインフラ、グローバルトラックメーカーの積極的な参画により恩恵を受けています。OEMメーカーは、リアルタイム監視、遠隔診断、性能最適化をサポートする工場出荷時搭載のデジタル接続プラットフォームを統合しており、これが市場の急速な浸透を促進しています。さらに、フリート効率化への需要の高まり、厳格な安全規制、主要テレマティクスプロバイダーの存在が、地域フリート全体での技術導入を加速させています。

グローバルコネクテッドトラック市場で事業を展開する主要企業には、Trimble、Continental、Daimler Truck、BYD Company、Tata Motors、PACCAR、MAN Truck &Bus、Scania、Geotab、Volvoなどが挙げられます。コネクテッドトラック市場の主要プレイヤーは、市場での存在感を強化するため、複数の戦略を実施しています。多くの企業が、ハードウェア、ソフトウェア、テレマティクスを統合した先進的なコネクティビティ・エコシステムの開発に注力し、統合的なフリートインテリジェンスの提供を目指しています。製品ポートフォリオの拡大と大規模導入の実現に向け、物流事業者やOEMメーカーとの戦略的提携も推進されています。また、予測保全、ドライバーの安全性、エネルギー最適化の向上を図るため、AIおよびデータ駆動型分析技術への多額の投資も行われています。

よくあるご質問

目次

第1章 調査手法

- 市場範囲と定義

- 調査設計

- 調査アプローチ

- データ収集方法

- データマイニングの情報源

- グローバル

- 地域別/国別

- 基本推定値と計算

- 基準年計算

- 市場推定における主要な動向

- 1次調査および検証

- 一次情報

- 予測モデル

- 調査の前提条件と制限事項

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率分析

- コスト構造

- 各段階における付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- フリート管理効率化への需要の高まり

- 5GおよびIoT技術の統合

- 安全性と排出ガスに関する政府規制

- クラウドベースのテレマティクスプラットフォームの導入拡大

- 予知保全への需要の高まり

- 業界の潜在的リスク&課題

- 初期導入および保守コストの高さ

- データセキュリティとプライバシーに関する懸念

- 市場機会

- 自律走行および準自律走行トラックの拡大

- リアルタイム分析のためのエッジコンピューティングの台頭

- 商用車の電動化拡大

- 新興市場における普及の拡大

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- 技術とイノベーションの動向

- 現在の技術動向

- 新興技術

- 特許分析

- 価格動向

- 地域別

- 製品別

- 生産統計

- 生産拠点

- 消費拠点

- 輸出と輸入

- コスト内訳分析

- 持続可能性と環境影響分析

- ライフサイクルアセスメントおよび環境モデリング

- 持続可能な設計と最適化

- 環境コンプライアンスと報告

- グリーンテクノロジーとイノベーション

- ビジネスケース及び投資利益率(ROI)分析

- 総所有コスト(TCO)フレームワーク

- ROI算出調査手法

- 導入スケジュールと主要マイルストーン

- リスク評価と軽減戦略

- パフォーマンスベンチマーキングと主要業績評価指標(KPI)

- 業務効率化指標

- 安全性とコンプライアンス指標

- 財務実績のベンチマーク

- ドライバーパフォーマンス評価システム

- 業界標準とプロトコル

- SAE J1939通信規格

- TMC推奨プラクティス

- 相互運用性及びデータ交換プロトコル

- サイバーセキュリティ及び機能安全基準

- 導入におけるベストプラクティス

- 導入戦略と調査手法

- 変更管理およびドライバー研修

- データ統合と分析環境の構築

- 保守・サポートの最適化

- ベンダー選定・評価フレームワーク

- 技術評価基準

- 統合能力評価

- 拡張性と将来性への配慮

- サポート及びサービスレベル要件

- 将来展望と技術ロードマップ

- 技術進化のタイムライン

- 自律走行トラックの統合

- 電気トラックの接続性

- データ収益化戦略

- 規制の進化による影響

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ地域

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

- 主な発展

- 合併・買収

- 提携・協業

- 新製品の発売

- 事業拡大計画と資金調達

第5章 市場推計・予測:コンポーネント別、2021-2034

- 主要動向

- ハードウェア

- テレマティクス制御ユニット(TCU)

- 車載診断装置(OBD)

- 通信モジュール(セルラー、Wi-Fi、Bluetooth)

- センサー及びデータ収集装置

- GPS/GNSS測位システム

- その他

- ソフトウェア

- フリート管理ソフトウェアプラットフォーム

- モバイルアプリケーション及びドライバーインターフェース

- アナリティクスおよびビジネスインテリジェンスツール

- 統合およびAPI管理ソフトウェア

- サイバーセキュリティおよびデータ保護ソフトウェア

- その他

- サービス

- 設置・統合サービス

- データ分析およびコンサルティングサービス

- 保守・技術サポート

- 研修および変更管理サービス

- マネージドサービスおよびアウトソーシング

- その他

第6章 市場推計・予測:接続方式別、2021-2034

- 主要動向

- 車両とインフラ間の通信(V2I)

- 信号機統合

- スマートハイウェイシステム

- 料金徴収・支払いシステム

- 計量ステーション通信

- 駐車・荷役区域管理

- 車両ークラウド間通信(V2C)

- フリート管理プラットフォーム

- 遠隔診断・監視

- 無線による更新および設定

- データ分析とビジネスインテリジェンス

- 規制コンプライアンス報告

- 車両間通信(V2V)

- プラトーニングおよびコンボイ運転

- 衝突回避システム

- 交通流の最適化

- 緊急車両通信

- 協調型アダプティブ・クルーズ・コントロール

- その他

第7章 市場推計・予測:範囲別、2021-2034

- 主要動向

- 専用短距離通信(DSRC)

- 長期

第8章 市場推計・予測:車両別、2021-2034

- 主要動向

- 小型商用車(LCV)

- クラス1-2車両

- ピックアップトラック及び貨物バン

- 小型配送車両

- サービス・ユーティリティ車両

- 都市部におけるラストマイル配送ソリューション

- 中型商用車(MCV)

- クラス3~5車両

- ボックス型トラック及びステップバン

- フードサービス・飲料トラック

- ユーティリティ車両および自治体車両

- 地域別分布アプリケーション

- 冷蔵輸送ユニット(リーファーユニット)

- 大型商用車(HCV)

- クラス6-8車両

- 長距離用トラクター及びセミトレーラー

- 大型トラック及びトレーラー

- 建設車両および特殊用途車両

- 特殊重機

第9章 市場推計・予測:用途別、2021-2034

- 主要動向

- フリート管理

- 安全性とコンプライアンス

- 遠隔診断・保守

- インフォテインメントおよびコネクティビティ

- その他

第10章 市場推計・予測:販売チャネル別、2021-2034

- 主要動向

- OEM

- アフターマーケット

第11章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- ロシア

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- フィリピン

- インドネシア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ地域

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第12章 企業プロファイル

- グローバル企業

- BYD Company

- Daimler Truck

- Iveco

- MAN Truck &Bus

- Navistar International

- PACCAR

- Scania

- Tata Motors

- Tesla

- Volvo

- Telematics Providers

- Fleet Complete

- Geotab

- MiX Telematics

- Omnitracs

- Platform Science

- Samsara Networks

- Teletrac Navman

- Trimble

- Verizon Connect

- Zonar Systems

- ADAS &Component Suppliers

- Aptiv

- Autoliv

- Continental

- DENSO

- Knorr-Bremse

- Magna International

- Mobileye

- Robert Bosch

- Valeo

- ZF Friedrichshafen

- Connectivity &Hardware

- HARMAN International

- Murata Manufacturing

- NXP Semiconductors

- Qualcomm Technologies

- Sierra Wireless

- TE Connectivity