|

市場調査レポート

商品コード

1536899

ネットワークオートメーション:市場シェア分析、産業動向・統計、成長予測(2024~2029年)Network Automation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ネットワークオートメーション:市場シェア分析、産業動向・統計、成長予測(2024~2029年) |

|

出版日: 2024年08月14日

発行: Mordor Intelligence

ページ情報: 英文 160 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

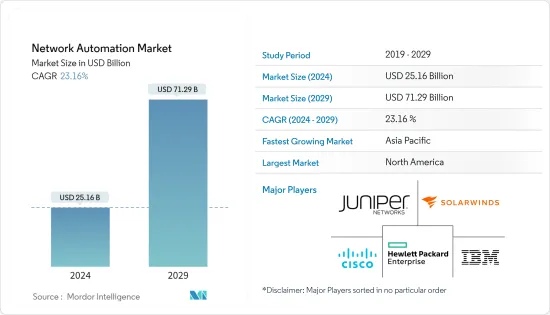

世界のネットワークオートメーションの市場規模は、2024年に251億6,000万米ドルに達し、2024~2029年の予測期間中にCAGR 23.16%で成長し、2029年には712億9,000万米ドルに達すると予測されています。

ネットワークオートメーション市場は、ネットワークの複雑化と効率的な管理ソリューションの必要性により、近年著しく成長しています。この成長の主な原動力は、クラウドコンピューティングと仮想化技術の採用が増加し、より俊敏でスケーラブルなネットワークインフラが必要になったことです。

主なハイライト

- Software-Defined Networking(SDN)はネットワーク機能仮想化(NFV)技術と統合され、仮想化によるネットワークオートメーションを利用しながら、ビジネスやサービスの目標に応じてネットワークを構成・変更します。SDNはハードウェアデバイスの動作方法を制御します。管理者は仮想マシン間で仮想ソフトウェアネットワークを作成したり、ネットワークソフトウェアで複数の物理ネットワークを管理することができます。

- ネットワーク仮想化とネットワークオートメーションは計画外の使用急増が発生する環境には特に有用です。オートメーションされたネットワークはネットワークトラフィックをネットワークの影響の少ないエリアのサーバに自動的にリダイレクトすることでこれらの急増に対応できるからです。

- IoTデバイスの急増とリアルタイムのデータ処理に対する需要により、膨大な量のネットワークトラフィックとデバイスを処理するためのオートメーションの必要性がさらに高まっています。企業は、手作業によるミスを減らし、運用効率を向上させ、迅速なサービス展開を可能にすることで、オートメーションによるコスト削減のメリットを認識しています。

- ネットワークオートメーション市場における熟練した専門家の不足は、高度なネットワーキング技術の導入を目指す産業にとって大きな抑制要因となっています。ネットワークオートメーションシステムの複雑さは大きな課題であり、プログラミング、ネットワークアーキテクチャ、サイバーセキュリティの専門知識が必要となります。

- ネットワークオートメーション市場には、いくつかのマクロ経済要因が大きく影響しています。これらには、経済成長、世界貿易力学、金利、労働市場の状況、規制シフト、技術の進歩、地政学的安定性、デジタル変革への取り組み、持続可能性への配慮などが含まれます。これらの動向は総体的にネットワークオートメーション技術の採用と進化を形成し、企業や政策立案者が十分な情報に基づいた意思決定を行うことを可能にします。

ネットワークオートメーション市場の動向

IT・通信エンドユーザー産業が大きな市場シェアを占める見込み

- スマートフォンの急速な普及とウェブ接続デバイス数の拡大により、既存の通信ネットワークが疲弊しています。その結果、ネットワーク事業者は帯域幅の不足と輻輳に悩まされ、通話の切断や不安定なネットワークパフォーマンスが発生しています。このようなときに、ネットワークオートメーションの需要が生まれます。

- IT・通信産業で調査された市場の成長は、接続されたデバイスやサービスの急増によるネットワークの複雑化によってもたらされています。5Gネットワークの展開には、スケーラブルで柔軟なソリューションが必要であり、オートメーションがそれを実現します。

- オートメーションは、迅速な脅威の検知と対応を可能にすることで、ネットワークセキュリティを向上させます。また、一貫したネットワークパフォーマンスと信頼性を確保することでサービス品質を高め、ユーザーエクスペリエンスと顧客満足度を向上させます。

- 2024年2月、Dell Technologiesは、通信サービスプロバイダー(CSP)のネットワーククラウドと運用変革の効率化を支援するソリューションスイートを発表しました。Dellは、デジタルトランスフォーメーションにおける幅広い経験と産業との強固な協力関係を活用し、CSPのリスクを軽減する通信ソリューションを構築しています。これらのソリューションは、導入の合理化、運用のオートメーション、分離されたネットワーククラウドインフラのサポートとライフサイクル管理の簡素化を目的として設計されています。

- 2024年5月、世界の通信技術分野で著名なTata Communicationsは、Tata Communications CloudLyteを発表しました。この先進的なプラットフォームは完全にオートメーションされており、エッジコンピューティングに重点を置き、データ中心化が進む環境で企業が成功を収めることを目的としています。Tata Communications CloudLyteはエッジコンピューティングの分野で際立っており、アクセス方法、クラウドプロバイダー、インフラにとらわれない汎用的なアーキテクチャを提供することで、世界中の企業にとって最適な選択肢となっています。

- GSMAは、IoT接続の総数は2021~2030年の間に倍増し、374億に達すると予測しています。拡大するIoTエコシステムがそれを後押ししています。重点地域のライセンシングセルラーIoT接続数は2021~2030年の間に倍増し、1億5600万に達します。そのため、IoTの導入は、それ自体が技術であるというよりも、センシング、オートメーション、ソフトウェア、クラウドコンピューティングに関連するさまざまな技術を統合しています。

- 企業がハイパーコネクティビティを採用し、5GやIoTなどの技術が勢いを増す中、リアルタイムのデータ処理、低遅延アプリケーション、スマートな意思決定に対する需要が最重要となり、市場の成長機会を大きく後押ししています。

北米が大きな市場シェアを占める見込み

- 北米で最も大きな市場シェアを持つ米国は、ネットワークオートメーション市場の最前線に位置しています。これは、Cisco、IBM、SolarWinds、VMWare、Extreme Networks、Juniper Networksといった主要ソリューションプロバイダーの強固なプレゼンスに支えられています。

- この地域は、5G技術の採用と導入が急速に急増する態勢にあります。Ericssonの調査によると、5Gの総契約数は2023年のわずか2億6,000万件から、2028年には推定4億2,000万件に急増すると予測されています。このように5Gの普及が進むと、高度なネットワークサービスへのニーズが高まり、ネットワークオートメーションニーズが高まることになります。

- SaaSベースアプリケーション、ネットワーク分析、DevOps、仮想化など、さまざまな先進技術の台頭が、北米のユーザーや企業にネットワークオートメーションソリューションの導入を促しています。これには、インテントベースネットワーキング、SD-WAN、各種ネットワークオートメーションツールが含まれます。

- エンドユーザー産業別では、IT・通信産業が北米ネットワークオートメーション市場で最も大きな成長を遂げようとしています。この急成長の主な要因は、効率的なネットワーク管理に対する需要の高まり、5G技術の展開、クラウドサービスの拡大です。データトラフィックと接続デバイスの増加に伴い、オートメーションソリューションは複雑なネットワーク運用を処理し、サイバーセキュリティを確保するために不可欠となっています。

ネットワークオートメーション産業の概要

ネットワークオートメーション市場は非常に細分化されており、Cisco Systems Inc., Juniper Networks Inc., IBM Corporation, Hewlett Packard Enterprise, Development LP, SolarWinds Inc.などの大手企業が参入しています。市場競争は、製品ラインナップを強化し、持続可能な競争優位性を獲得するために、提携や買収などの戦略を採用しています。

- 2024年3月:IBMは、著名なネットワークおよびITインフラオートメーション製品プロバイダーであるPliantの買収を発表。Pliantの機能は、ネットワークとITインフラのタスクをオートメーションし、これらの機能をアプリケーション層に抽象化する上で極めて重要です。これにより、アプリケーションと開発者は、簡素化されたプロビジョニングとインフラ管理をアプリケーション内で直接コントロールできるようになります。

- 2024年1月:Juniper Networksは、産業に先駆けてAIネイティブネットワーキングプラットフォームを発表しました。このプラットフォームは、AIを活用するために特別に設計されており、通信事業者とエンドユーザーに最適な体験を保証します。ジュニパーのプラットフォームは、7年間の知見とデータサイエンスから導き出されたものです。デバイス、ユーザー、アプリケーション、資産など、あらゆる接続において信頼性、測定可能性、セキュリティを実現するよう、綿密に設計されています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 産業の魅力度 - ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

- 産業バリューチェーン分析

- 技術スナップショット

- マクロ経済動向の市場への影響

第5章 市場力学

- 市場促進要因

- データセンターネットワーク需要の増加

- コネクテッドデバイスの動向の高まり

- 市場抑制要因

- 各産業における専門技術者の不足

第6章 市場セグメンテーション

- ネットワークタイプ別

- フィジカル

- バーチャル

- ハイブリッド

- コンポーネント別

- ソリューションタイプ

- ネットワークオートメーションツール

- SD-WAN・ネットワーク仮想化

- インテントベースネットワーキング

- サービスタイプ

- マネージドサービス

- プロフェッショナルサービス

- ソリューションタイプ

- 展開別

- クラウド

- オンプレミス

- ハイブリッド

- エンドユーザー産業別

- IT・通信

- 製造業

- エネルギー・公益事業

- 銀行・金融サービス

- 教育

- その他のエンドユーザー産業

- 地域別

- 北米

- 欧州

- アジア

- オーストラリア・ニュージーランド

- ラテンアメリカ

- 中東・アフリカ

第7章 競合情勢

- 企業プロファイル

- Cisco Systems Inc.

- Juniper Networks Inc.

- IBM Corporation

- Hewlett Packard Enterprise Company

- Solarwinds Corporation

- Fortra LLC

- Open Text Corporation

- NetBrain Technologies Inc.

- Arista Networks Inc.

- Extreme Networks Inc.

- BMC Software Inc.

- Fujitsu Limited

- Broadcom Inc.

- Nuage Networks(Nokia Corporation)

- Forward Networks Inc.

- AppViewX Inc.

第8章 投資分析

第9章 市場の将来

The Network Automation Market size is estimated at USD 25.16 billion in 2024, and is expected to reach USD 71.29 billion by 2029, growing at a CAGR of 23.16% during the forecast period (2024-2029).

The network automation market has significantly grown in recent years, driven by the increasing complexity of networks and the need for efficient management solutions. The key driver behind this growth is the rising adoption of cloud computing and virtualization technologies, which has necessitated more agile and scalable network infrastructures.

Key Highlights

- Software-defined networking (SDN) is integrated with network functions virtualization (NFV) technology to configure and change the network according to business or service goals while using network automation with virtualization. The SDN controls how the hardware devices operate. Administrators can create virtual software networks between virtual machines or manage multiple physical networks with networking software.

- Network virtualization and network automation are especially useful for environments that experience unplanned usage surges because the automated network can accommodate these surges by automatically redirecting network traffic to servers in less impacted areas of the network.

- The proliferation of IoT devices and the demand for real-time data processing have further fueled the need for automation to handle the sheer volume of network traffic and devices. Enterprises are recognizing the cost-saving benefits of automation by reducing manual errors, improving operational efficiency, and enabling faster service deployment.

- The shortage of skilled professionals in the network automation market presents a significant restraint for industries seeking to adopt advanced networking technologies. The complexity of network automation systems presents a significant challenge, necessitating expertise in programming, network architecture, and cybersecurity.

- Several macroeconomic factors significantly influence the network automation market. These include economic growth, global trade dynamics, interest rates, labor market conditions, regulatory shifts, technological advancements, geopolitical stability, digital transformation efforts, and sustainability considerations. These trends collectively shape the adoption and evolution of network automation technologies, enabling businesses and policymakers to make informed decisions.

Network Automation Market Trends

IT and Telecom End-user Industry is Expected to Hold Significant Market Share

- The surge in smartphone adoption and the expanding web-connected device count have strained existing telecom networks. Consequently, network operators grapple with bandwidth shortages and congestion, resulting in call drops and erratic network performance. It is when the demand for network automation comes into play.

- The growth of the market studied in the IT and telecom industry is driven by the increasing complexity of networks due to the proliferation of connected devices and services. The rollout of 5G networks demands scalable and flexible solutions, which automation provides.

- Automation improves network security by enabling rapid threat detection and response. It also enhances service quality by ensuring consistent network performance and reliability, improving user experiences and customer satisfaction.

- In February 2024, Dell Technologies unveiled a suite of solutions tailored to assist communications service providers (CSPs) in streamlining their network cloud and operational transformations. Leveraging its widespread experience in digital transformation and robust industry collaborations, Dell is crafting telecom solutions to mitigate risks for CSPs. These solutions are designed to streamline deployment, automate operations, and simplify support and lifecycle management for disaggregated network cloud infrastructures.

- In May 2024, Tata Communications, a prominent player in the global communication technology sector, introduced Tata Communications CloudLyte. This advanced platform is fully automated and focuses on edge computing, aiming to equip enterprises for success in an increasingly data-centric environment. Tata Communications CloudLyte stands out in edge computing, offering a versatile architecture that is agnostic to access methods, cloud providers, and infrastructure, making it a fitting choice for enterprises globally.

- GSMA estimates that the total number of IoT connections will double between 2021 and 2030, reaching 37.4 billion. The expanding IoT ecosystem assists it. Licensed cellular IoT connections in the focus regions will double between 2021 and 2030, reaching 156 million. Therefore, rather than being a technology by itself, IoT deployment integrates various technologies related to sensing, automation, software, and cloud computing.

- With businesses embracing hyperconnectivity and technologies such as 5G and IoT gaining momentum, the demand for real-time data processing, low-latency applications, and smart decision-making has become paramount, driving the market's growth opportunities significantly.

North America is Expected to Hold Significant Market Share

- With the most significant market share in North America, the United States is at the forefront of the network automation market. This is underpinned by the robust presence of major solution providers such as Cisco, IBM, SolarWinds, VMWare, Extreme Networks, and Juniper Networks.

- The region is poised for a swift surge in the adoption and implementation of 5G technology. As per Ericsson's study, the total number of 5G subscriptions is projected to soar to an estimated 420 million by 2028, up from a mere 260 million in 2023. This rise in the adoption of 5G is set to fuel a greater need for advanced network services, subsequently spurring the need for increased network automation.

- The rise of various advanced technologies, such as SaaS-based applications, network analytics, DevOps, and virtualization, has spurred users and businesses in North America to adopt network automation solutions. These include intent-based networking, SD-WAN, and various network automation tools.

- By end-user industry, the IT and telecom industry is poised for the most significant growth in the North American network automation market. This surge is mainly driven by the growing demand for efficient network management, the rollout of 5G technology, and the expansion of cloud services. As data traffic and connected devices multiply, automated solutions become essential for handling complex network operations and ensuring cybersecurity.

Network Automation Industry Overview

The network automation market is highly fragmented, with major players like Cisco Systems Inc., Juniper Networks Inc., IBM Corporation, Hewlett Packard Enterprise, Development LP, and SolarWinds Inc. Market players adopt strategies like partnerships and acquisitions to enhance their product offerings and gain sustainable competitive advantage.

- March 2024: IBM announced its acquisition of Pliant, a prominent network and IT infrastructure automation product provider. Pliant's capabilities are crucial for automating network and IT infrastructure tasks and abstracting these functions to the application layer. This gives applications and developers maximum control over simplified provisioning and infrastructure management directly within applications.

- January 2024: Juniper Networks unveiled the industry's pioneering AI-native networking platform. This platform is specifically engineered to harness AI, guaranteeing optimal experiences for operators and end-users. Juniper's platform is drawn from seven years of insights and data science. It is meticulously crafted to deliver reliability, measurability, and security across all connections, whether for devices, users, applications, or assets.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Threat of New Entrants

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Bargaining Power of Suppliers

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Technology Snapshot

- 4.5 Impact of Macroeconomic Trends on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Demand for Data Center Network

- 5.1.2 Rising Trend of Connected Devices

- 5.2 Market Restraints

- 5.2.1 Lack of Skilled Professional Across Industries

6 MARKET SEGMENTATION

- 6.1 By Network Type

- 6.1.1 Physical

- 6.1.2 Virtual

- 6.1.3 Hybrid

- 6.2 By Component

- 6.2.1 Solution Type

- 6.2.1.1 Network Automation Tools

- 6.2.1.2 SD-WAN and Network Virtualization

- 6.2.1.3 Intent-based Networking

- 6.2.2 Service Type

- 6.2.2.1 Managed Service

- 6.2.2.2 Professional Service

- 6.2.1 Solution Type

- 6.3 By Deployment

- 6.3.1 Cloud

- 6.3.2 On-premise

- 6.3.3 Hybrid

- 6.4 By End-user Industry

- 6.4.1 IT and Telecom

- 6.4.2 Manufacturing

- 6.4.3 Energy and Utility

- 6.4.4 Banking and Financial Services

- 6.4.5 Education

- 6.4.6 Other End-user Industries

- 6.5 By Geography***

- 6.5.1 North America

- 6.5.2 Europe

- 6.5.3 Asia

- 6.5.4 Australia and New Zealand

- 6.5.5 Latin America

- 6.5.6 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles*

- 7.1.1 Cisco Systems Inc.

- 7.1.2 Juniper Networks Inc.

- 7.1.3 IBM Corporation

- 7.1.4 Hewlett Packard Enterprise Company

- 7.1.5 Solarwinds Corporation

- 7.1.6 Fortra LLC

- 7.1.7 Open Text Corporation

- 7.1.8 NetBrain Technologies Inc.

- 7.1.9 Arista Networks Inc.

- 7.1.10 Extreme Networks Inc.

- 7.1.11 BMC Software Inc.

- 7.1.12 Fujitsu Limited

- 7.1.13 Broadcom Inc.

- 7.1.14 Nuage Networks (Nokia Corporation)

- 7.1.15 Forward Networks Inc.

- 7.1.16 AppViewX Inc.