|

市場調査レポート

商品コード

1687097

油田サービス(OFS)-市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Oilfield Services (OFS) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 油田サービス(OFS)-市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 250 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

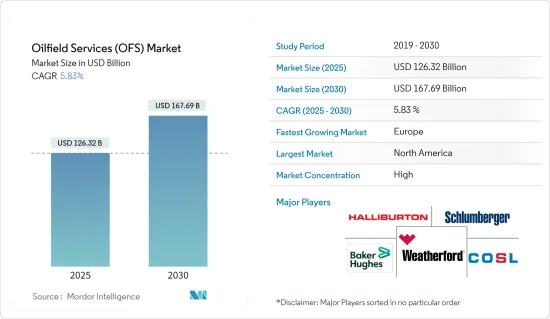

油田サービス(OFS)市場規模は2025年に1,263億2,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは5.83%で、2030年には1,676億9,000万米ドルに達すると予測されます。

主要ハイライト

- 中期的には、ガス埋蔵量の開発増加や先端技術、ツール、設備などの要因が、予測期間中の油田サービス市場を牽引すると予想されます。

- 一方、需給ギャップ、地政学、その他いくつかの要因に起因する、最近の期間における不安定な原油価格が、油田サービス市場の需要拡大を抑制しています。

- しかし、炭化水素の生産コストを最適化するための新技術や手法への注目は、予測期間中に油田サービス市場にいくつかの機会を生み出すと予想されます。

- 北米は、シェール油田での掘削・生産活動が活発であることから、予測期間中最大の市場になると予想されます。

油田サービス市場の動向

掘削サービスが市場を独占する見込み

- 世界経済は石油需要の大幅な増加を下支えすると予想されます。好調な経済はより多くの石油を消費すると予想され、その需要は長年にわたって大きく伸びると予想されます。インドと中国は、2024年までに世界の石油需要の約50%を占めるようになると考えられます。

- 石油輸出国機構(OPEC)の統計によると、2023年の世界の原油需要は日量約1億221万バレルで、2022年の9,957万バレルから増加しました。原油需要の増加は、世界中で掘削サービスの需要を増加させています。

- 2023年4月、海洋掘削会社のSeadrill LimitedがAquadrill LLCの買収に成功したと発表しました。9億5,800万米ドル相当の全株式取得により、12基のフローター、3基の過酷環境リグ、4基の良性ジャッキアップ、3基の入札支援リグから成るハイスペックフリートが誕生しました。

- 2024年2月、中東最大の国営掘削会社であるADNOC Drillingは、オマーンでのリグ供給の入札資格を取得し、サウジアラビアとクウェートでの入札参加の承認を求めています。2024年末までに、同社はアラブ首長国連邦以外に配備できるだけのリグを保有することになります。

- そのため、石油・ガス大手事業会社は、増産とエネルギー需要の増加に対応する必要に迫られています。その結果、在来型油田が成熟の兆しを見せ始めたため、いくつかの事業会社は非在来型埋蔵量の開発に重点を移しています。

- 2023年10月、Transoceanは陸上掘削リグ3基の新たな延長契約を獲得したと発表しました。これらのリグのうち1基は、Reliance Industriesとの契約により、日当33万米ドルでインドに配備されています。契約は2025年10月まで更新され、日当は34万8,000米ドルに増額されました。2023年12月の現行契約終了後、リグは45日間の準備期間を経て新たな契約を開始します。

- したがって、上記の点から、予測期間中は掘削サービスが油田サービス市場を独占すると予想されます。

北米が市場を独占する展望

- 北米は、世界的に最も発達したオフショア石油・ガス産業の1つであり、主要重点地域はメキシコ湾とアラスカ沖地域の膨大な埋蔵量です。掘削深度が年々深まるにつれて、技術的に回収可能な埋蔵量は大幅に増加し、この地域のオフショア石油・ガス部門への投資を誘致しました。上記の要因により、この地域は油田サービス市場の世界のホットスポットでもあり、そのシェアの大半は米国が占めています。

- 米国が石油・ガス生産能力の拡大に多額の投資を行ったため、メキシコ湾は海洋掘削リグサービスの重要なホットスポットとなりました。メキシコ湾は、石油・ガスを含むこの地域の豊富な天然資源を担っています。

- 米国は、主にシェール層やタイトな埋蔵量で掘削・水圧破砕される坑井の数が増加していることから、油田サービスの最大市場のひとつになると予想されます。同盆地の損益分岐価格の低さがこれを支えています。最近のシェールプレイ、水平掘削、フラッキングの開発により、この地域の油田サービス需要は大幅に増加しています。

- 米国は常に最先端を走っており、予測期間中も北米の石油・ガス市場を独占し続けると予想されます。米国は世界的に主要な石油・天然ガス生産国であり、今後数年間は世界の石油需要の約60%をカバーすると予想されています。しかし、ロシア・ウクライナ戦争の悪影響により、米国はロシアからの石油・石油精製品・天然ガス・石炭の輸入制限を課しました。この結果、米国全域でガス価格が上昇し、インフレ圧力が高まったため、2022年には資本予算と支出が減少し、生産が抑制され、事業会社による掘削リグ数が減少しました。

- しかし、このシナリオは2023年には回復しました。例えば、Baker Hughesのリグカウントによると、2024年2月、米国の稼働中のロータリーリグは626基で、うち20基がオフショアリグ、606基がオンショアリグでした。2022年末の稼働リグ数が15基であったのに比べ、オフショアリグ数は増加を記録しました。こうした動向は、同国の掘削サービスの成長を支え、油田サービス市場の成長をさらに促進すると考えられます。

- 同様に、カナダはベネズエラ、サウジアラビアに次いで世界第3位の原油埋蔵量を誇り、そのうち96%はオイルサンド埋蔵量です。同国で採掘可能な原油は密度が高く、砂粒子の含有量も多いです。このため、油井の底穴から地表まで石油を輸送するには、高い圧力と坑井への介入が必要となり、同国における油田サービスの需要が高まっている

- したがって、上記の点から、予測期間中、北米が油田サービス市場を独占すると予想されます。

油田サービス産業概要

油田サービス市場はセグメント化されています。同市場の主要企業(順不同)には、Schlumberger Limited、Baker Hughes Company、Halliburton Company、Weatherford International PLC、China Oilfield Services Limitedなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 エグゼクティブサマリー

第3章 調査手法

第4章 市場概要

- イントロダクション

- 2029年までの市場規模と需要予測(単位:10億米ドル)

- 2029年までの石油・天然ガス生産量と予測

- 2023年までの陸上と海上リグ稼動数

- 最近の動向と開発

- 政府の規制と施策

- 市場力学

- 促進要因

- ガス埋蔵量の開発と先端技術、ツール、設備の増加

- 世界の油田サービス投資の増加

- 抑制要因

- 需給ギャップに起因する、最近の期間における原油価格の変動

- 促進要因

- サプライチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場セグメンテーション

- サービスタイプ

- 掘削サービス

- 完成サービス

- 生産・介入サービス

- その他

- 配備場所

- オンショア

- オフショア

- 市場分析:地域別、2028年までの市場規模と需要予測(地域別)

- 北米

- 米国

- カナダ

- その他の北米

- 欧州

- ドイツ

- フランス

- 英国

- イタリア

- ロシア

- スペイン

- ノルディック

- トルコ

- その他の欧州

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- マレーシア

- タイ

- ベトナム

- その他のアジア太平洋

- 南米

- ブラジル

- アルゼンチン

- コロンビア

- その他の南米

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

- ナイジェリア

- カタール

- エジプト

- その他の中東・アフリカ

- 北米

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- Schlumberger Limited

- Weatherford International PLC

- Baker Hughes Company

- Halliburton Company

- Transocean Ltd

- Valaris PLC

- China Oilfield Services Limited

- Nabors Industries Inc.

- Basic Energy Services Inc.

- OiLSERV

- Expro Group

- 市場ランキング/シェア(%)分析

第7章 市場機会と今後の動向

- 炭化水素の生産コストを最適化する新技術・新方法への注目の高まり

目次

Product Code: 55022

The Oilfield Services Market size is estimated at USD 126.32 billion in 2025, and is expected to reach USD 167.69 billion by 2030, at a CAGR of 5.83% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, factors such as the increasing development of gas reserves and advanced technology, tools, and equipment are expected to drive the oilfield services market during the forecast period.

- On the other hand, the volatile oil prices over the recent period, owing to the supply-demand gap, geopolitics, and several other factors, have been restraining the growth in the demand for the oilfield services market.

- However, the focus on new technologies and methods to optimize the production cost of hydrocarbons is expected to create several opportunities for the oilfield services (OFS) market during the forecast period.

- North America is expected to be the largest market during the forecast period, owing to high drilling and production activity in shale fields.

Oilfield Services (OFS) Market Trends

Drilling Services Are Expected to Dominate the Market

- The global economy is expected to underpin a substantial increase in oil demand. Strong economies are anticipated to consume more oil, and the demand is expected to grow significantly over the years. India and China will contribute around 50% of the global oil demand by 2024.

- According to the Organization of the Petroleum Exporting Countries (OPEC) statistics, the worldwide crude oil demand was around 102.21 million barrels per day in 2023, up from 99.57 million barrels in 2022. The rising demand for crude oil increases the demand for drilling services worldwide.

- In April 2023, Seadrill Limited, an offshore drilling company, announced acquiring Aquadrill LLC successfully. The all-stock acquisition, valued at USD 958 million, creates a high-spec fleet comprised of 12 floaters, three harsh environment rigs, four benign jack-ups, and three tender-assisted rigs.

- In February 2024, ADNOC Drilling, the largest national drilling company in the Middle East, was qualified to bid to supply rigs in Oman and is seeking approvals to participate in tenders in Saudi Arabia and Kuwait. By the end of 2024, the company will have enough rigs to deploy outside the United Arab Emirates.

- Hence, the top oil and gas operating companies are under increasing pressure to increase production and meet the increasing energy demand. As a result, several operating companies have shifted their focus toward exploiting unconventional reserves, as the conventional fields have started showing signs of maturity.

- In October 2023, Transocean announced that it secured a new extension contract for three of its onshore drilling rigs. One of those rigs is deployed in India under contract with Reliance Industries Limited at a day rate of USD 330,000. The agreement was renewed until October 2025 with an increased day rate of USD 348,000. Following completion of the current contract in December 2023, the rig will undergo a 45-day preparation period before commencing the new contract.

- Therefore, owing to the above points, drilling services are expected to dominate the oilfield services (OFS) market during the forecast period.

North America is Expected to Dominate the Market

- North America has one of the most well-developed offshore oil and gas industries globally, with the primary areas of focus being the vast reserves in the Gulf of Mexico and offshore Alaska region. As drilling depths increased over the years, the volume of technically recoverable reserves increased significantly, attracting investments in the region's offshore oil & gas sector. Due to the factors mentioned above, the region is also a global hotspot for the oilfield services market, with most of the share from the United States.

- As the United States invested heavily in expanding its oil & gas production capacity, the Gulf of Mexico has become a key hotspot for offshore drilling rig services. The Gulf of Mexico is responsible for the region's rich natural resources, including oil and gas.

- The United States is expected to be one of the largest markets for oilfield services, mainly due to the increasing number of wells being drilled and fracked in shale and tight reserves. The basins' low breakeven price supports this. The recent development of shale plays, horizontal drilling, and fracking has resulted in a massive increase in demand for oilfield services in the region.

- The United States has always been at the forefront and is expected to continue dominating North America's oil and gas market during the forecast period. The United States is a major crude oil and natural gas producer globally, and it is expected to cover around 60% of the world's oil demand in the coming years. However, owing to the negative impact of the Russia-Ukraine War, the United States imposed restrictions on importing oil, refined petroleum products, natural gas, and coal from Russia. This led to higher gas prices and increased inflation pressure across the United States, leading to a decline in the capital budget and expenditure, curtailed production, and reduced drilling rig count by the operating companies in 2022.

- However, this scenario recovered in 2023. For instance, according to the Baker Hughes Rig Count, in February 2024, the United States had 626 active rotary rigs, of which 20 were offshore rigs and 606 onshore rigs. This recorded a rise in the offshore rig counts compared to the 15 active rigs at the end of 2022. These trends will likely support the growth of the country's drilling services and further promote the growth of the oilfield services market.

- Similarly, Canada has the world's third-largest crude oil reserves, after Venezuela and Saudi Arabia, of which 96% are oil sand reserves. The oil available in the country is high-density and has a high sand particle content. Due to this, oil transport from the bottom hole of the oil well to the surface requires high pressure and wellbore intervention, thus increasing the demand for oilfield services in the country.

- Therefore, owing to the above points, North America is expected to dominate the oilfield services (OFS) market during the forecast period.

Oilfield Services (OFS) Industry Overview

The oilfield services market is fragmented. Some of the major players in the market (in no particular order) include Schlumberger Limited, Baker Hughes Company, Halliburton Company, Weatherford International PLC, and China Oilfield Services Limited.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD billion, till 2029

- 4.3 Crude Oil and Natural Gas Production and Forecast, till 2029

- 4.4 Onshore and Offshore Active Rig Count, till 2023

- 4.5 Recent Trends and Developments

- 4.6 Government Policies and Regulations

- 4.7 Market Dynamics

- 4.7.1 Drivers

- 4.7.1.1 Increasing Development of Gas Reserves and Advanced Technology, Tools, and Equipment

- 4.7.1.2 Increasing Investment in the Oilfield Services across World

- 4.7.2 Restraints

- 4.7.2.1 The Volatile Oil Prices Over the Recent Period, Owing to the Supply-Demand Gap

- 4.7.1 Drivers

- 4.8 Supply Chain Analysis

- 4.9 Porter's Five Forces Analysis

- 4.9.1 Bargaining Power of Suppliers

- 4.9.2 Bargaining Power of Consumers

- 4.9.3 Threat of New Entrants

- 4.9.4 Threat of Substitutes Products and Services

- 4.9.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Service Type

- 5.1.1 Drilling Services

- 5.1.2 Completion Services

- 5.1.3 Production and Intervention Services

- 5.1.4 Other Services

- 5.2 Location of Deployment

- 5.2.1 Onshore

- 5.2.2 Offshore

- 5.3 Geography (Regional Market Analysis {Market Size and Demand Forecast till 2028 (for regions only)})

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 France

- 5.3.2.3 United Kingdom

- 5.3.2.4 Italy

- 5.3.2.5 Russia

- 5.3.2.6 Spain

- 5.3.2.7 NORDIC

- 5.3.2.8 Turkey

- 5.3.2.9 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 Malaysia

- 5.3.3.6 Thailand

- 5.3.3.7 Vietnam

- 5.3.3.8 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 South Africa

- 5.3.5.4 Nigeria

- 5.3.5.5 Qatar

- 5.3.5.6 Egypt

- 5.3.5.7 Rest of the Middle East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Schlumberger Limited

- 6.3.2 Weatherford International PLC

- 6.3.3 Baker Hughes Company

- 6.3.4 Halliburton Company

- 6.3.5 Transocean Ltd

- 6.3.6 Valaris PLC

- 6.3.7 China Oilfield Services Limited

- 6.3.8 Nabors Industries Inc.

- 6.3.9 Basic Energy Services Inc.

- 6.3.10 OiLSERV

- 6.3.11 Expro Group

- 6.4 Market Ranking/Share (%) Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Focus on New Technologies and Methods to Optimize its Production Cost of Hydrocarbons