|

市場調査レポート

商品コード

1536833

自動車用自動緊急ブレーキシステム:市場シェア分析、産業動向・統計、成長予測(2024~2029年)Automotive Autonomous Emergency Braking System - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 自動車用自動緊急ブレーキシステム:市場シェア分析、産業動向・統計、成長予測(2024~2029年) |

|

出版日: 2024年08月14日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

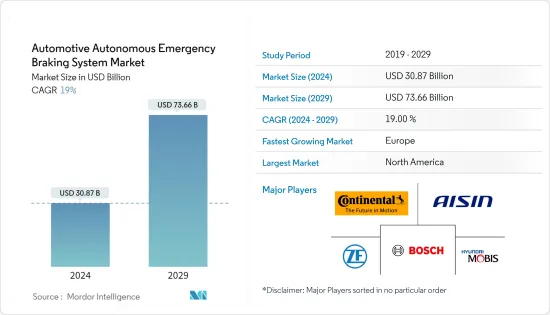

世界の自動車用自動緊急ブレーキシステムの市場規模は、2024年に308億7,000万米ドルに達し、2024~2029年の予測期間中にCAGR 19%で成長し、2029年には736億6,000万米ドルに達すると予測されます。

中期的には、消費者や当局の間で安全に対する意識が高まり、自動車用自動緊急ブレーキシステムが大きく発展し、その結果、安全性が向上し、路上での事故が減少しています。技術のさらなる進歩により、市場はさらに安全で信頼性の高いブレーキシステムを目にするようになると予想されます。

各自動車メーカーがブレーキ効率を向上させるために先進的なブレーキシステムを車両に組み込んでいることや、業界各社が幅広い製品を提供していることなどが、予測期間中の市場成長をさらに促進すると予想されます。

年間約125万人が交通事故で死亡しており、その数は発展途上国で最も多いです。世界の多くの政府は、交通事故の増加を抑制するために厳しい規制を導入し始めています。

大手OEMは、先進技術開発のための研究開発への投資を増やしています。自動車の安全性に関する懸念の高まり、先進的なブレーキシステムの採用の増加、先進的なAIを搭載したシステムの出現、政府の自動車安全基準の増加と、世界の自動車生産台数の増加が相まって、自動車用自動緊急ブレーキシステム市場は予測期間中に促進されると予想されます。

多くの相手先商標製品メーカーが、中級車や高級車の大半にAEBシステムを搭載しています。その結果、自律走行車の生産台数が増加しています。予測期間中、このような自動車の生産台数はCAGR 21%以上を記録すると予想されます。

自動車用自動緊急ブレーキシステムの市場動向

乗用車が主要市場シェアを占める

自動車における高度な安全機能に対する需要の高まりと、世界の主要地域における乗用車の販売台数の増加が、今後数年間の市場の大きな成長をもたらすとみられます。

自動緊急ブレーキは先進安全技術システムであり、 促進要因が対応できなかった場合に、事故を防ぐために車両を自律的に減速または完全に停止させる。他の先進運転支援技術と同様、自動緊急ブレーキも100%確実というわけではないです。

こうした需要の高まりに対応するため、複数の自動車メーカーがこうした技術を搭載した新型車を発売しています。Teslaはすでに全車種にAEB機能を標準装備しており、Daimler、BMW、Fordといった他の自動車メーカーも、今後発売する全車種にAEBを搭載する見通しです。Teslaの車には、完全な自律性を実現するために必要なハードウェアがすべて装備されています。例えば

*2023年11月、RenaultはフランスでDacia Duster SUVを発表しました。この新型SUVは、5つの走行モードと自動緊急ブレーキシステムを備えた4x4 Terrain Controlトランスミッションを提供します。

*2023年11月、トヨタ自動車は北米市場にミッドサイズクロスオーバーSUV「Crown Signia」を投入しました。この新型SUVは自動緊急ブレーキシステムを搭載しています。

自動緊急ブレーキシステムに対する世界中の自動車所有者の関心の高まりが、世界市場を牽引しています。この需要には、交通事故件数の増加も拍車をかけています。世界各国の政府は、交通事故を回避するため、さまざまな種類の安全機能の開発を奨励しています。

可処分所得の増加や、安全機能が満載された自動車への顧客嗜好の移行が進んでいることも、市場を牽引しています。予測期間中、乗用車セグメントが市場をリードすると予想されます。

EURO NCAPの調査によると、都市走行環境における衝突事故の75%は時速25マイル以下で発生しており、AEBによって追突事故が38%減少しています。レベル4および5の自律走行車で提供される自律走行技術は、今後数年間で世界的に大きな市場になる可能性があります。

上記のような世界の進展に伴い、乗用車の自動緊急ブレーキシステムの需要は今後数年間は高水準で推移すると思われます。

北米が市場をリードする見込み

米国では、OEMが提供するモデルラインの51%で自律ブレーキが提供されています。TeslaとVolvoは、100%の車両にAEBを標準装備しています。

米国運輸省道路交通安全局(NHTSA)は最近、乗用車と小型トラックに自動緊急ブレーキと歩行者用AEBシステムを義務付ける規制案を公告しました。

この規則案は、歩行者関連の事故や追突事故を劇的に減らすことが期待されています。NHTSAは、この規則案が最終決定されれば、少なくとも年間360人の命が救われ、少なくとも年間24,000人の負傷者が減少すると推定しています。

さらに、これらのAEBシステムは、追突事故による物的損害を大幅に減らすことにつながります。多くの事故は完全に回避できるだろうし、他の事故は被害が少なくなると思われます。

同局のその他の交通安全対策には、2023年に向けて各州に義務付けられているアセスメントを支援するための「脆弱な道路利用者の安全アセスメント」の作成が含まれます。交通弱者に関する州の安全性能とその安全性向上計画は、評価されるパラメータのひとつです。

技術の進歩に伴い、OEMはAEBの公約達成に積極的であり続けなければならず、そうでなければ安全性の進歩で他の市場プレーヤーに遅れをとり、ブランドが失墜する可能性に直面します。特に、米国政府の安全格付けにAEBが組み込まれたことで、消費者の認識が変わる可能性があります。

以上のような発展により、市場は今後高い成長を遂げると予想されます。

自動車用自動緊急ブレーキシステム産業の概要

自動車用自動緊急ブレーキシステム市場は、Robert Bosch GmbH、Continental AG、ZF Friendrichagen AG、Hyundai Mobis、Hitachi Automotive System Ltd.などの主要企業によって支配されています。主要企業は戦略的アプローチに取り組むことで、世界市場での競争力を獲得し続けています。ブレーキシステムの一貫した進歩と革新は、メーカーが競争市場で牽引力を得るのに役立っています。例えば

*2023年7月、ZF Friedrichshafen AGとVolta Trucksは、全電気式電気トラック、Volta Zeroのコンポーネントと部品の統合に関する長期契約を締結。ZFは、先進緊急ブレーキシステム「OnGuardACTIVE」、ブレーキペダルボックスを含む電子ブレーキシステム、電子安定制御システム「ESCsmart」、および電空式ハンドブレーキ「OnHand」を提供。

*2023年6月、米国高速道路運輸安全局(NHTSA)は、大型トラックおよびバスに5年以内に自動緊急ブレーキ装置(AEB)を搭載することを義務付けると発表しました。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場促進要因

- 自動車の安全機能に対する需要の高まり

- 市場抑制要因

- システムに関連する高コスト

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション(市場規模:米ドル)

- 車両タイプ別

- 乗用車

- 商用車

- 技術別

- LiDar

- レーダー

- カメラ

- 地域別

- 北米

- 米国

- カナダ

- その他の北米

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- その他の欧州

- アジア太平洋

- インド

- 中国

- 日本

- 韓国

- その他のアジア太平洋

- その他の地域

- 南米

- 中東・アフリカ

- 北米

第6章 競合情勢

- ベンダー市場シェア

- 合併と買収

- 企業プロファイル

- Robert Bosch GmbH

- WABCO Holdings Inc.

- Hyundai Mobis Co. Ltd

- Denso Corporation

- ZF Friedrichshafen AG

- Continental AG

- Autoliv Inc.

- Valeo SA

- Aisin Corporation

- Delphi Automotive PLC

第7章 市場機会と今後の動向

The Automotive Autonomous Emergency Braking System Market size is estimated at USD 30.87 billion in 2024, and is expected to reach USD 73.66 billion by 2029, growing at a CAGR of 19% during the forecast period (2024-2029).

Over the medium term, increasing awareness about safety among consumers and authorities has led to significant developments in the automotive automated emergency brake system, resulting in improved security and reduced accidents on the road. With further technological advancements, the market is expected to see even safer and more reliable brake systems.

Factors such as individual vehicle manufacturers incorporating advanced braking systems in their vehicles to improve braking efficiency and industry players offering a wide range of products are further expected to drive market growth during the forecast period.

Annually, around 1.25 million people are killed in road accidents, with the highest numbers being registered in developing countries. Many governments worldwide have started imposing stringent regulations to curb the rising number of road accidents.

Major OEMs have started increasingly investing in R&D efforts to develop advanced technologies. Increasing concerns regarding vehicle safety, the growing adoption of advanced braking systems, the emergence of advanced AI-powered systems, and an increase in government vehicle safety norms, combined with a rise in vehicle production worldwide, are expected to propel the automotive autonomous emergency braking system market during the forecast period.

Many original equipment manufacturers are equipping AEB systems in most of their medium and luxury car ranges. This is resulting in the increasing production of autonomous vehicles. During the forecast period, the production of such vehicles is expected to record a CAGR of over 21%.

Automotive Autonomous Emergency Braking System Market Trends

Passenger Cars Hold Major Market Share

The rise in demand for advanced safety features in vehicles and the increase in passenger car sales across major regions worldwide are likely to result in major growth for the market over the coming years.

Automatic emergency braking is an advanced safety technology system that autonomously slows or completely stops a vehicle in order to prevent an accident if the driver fails to respond. As with other advanced driver assistance technologies, automatic emergency braking is not 100% foolproof.

To cater to this growing demand, several automakers are launching new vehicle models with these technologies. Tesla is already offering AEB features as standard across all its cars, while other automakers like Daimler, BMW, and Ford are expected to provide AEB in all their upcoming models. Tesla's cars are equipped with all the necessary hardware to achieve full autonomy. For instance,

* In November 2023, Renault introduced the Dacia Duster SUV in France. The new SUV offers a 4x4 Terrain Control transmission with five driving modes and an automatic emergency braking system.

* In November 2023, Toyota Motor Corporation introduced the Crown Signia mid-size crossover SUV in the North American market. The new SUV is equipped with an automatic emergency braking system.

The growing interest among vehicle owners worldwide in autonomous emergency braking systems is driving the global market. This demand has also been fueled by a rising number of road accidents. Governments worldwide are encouraging the development of several kinds of safety features in order to avoid road accidents.

Rising disposable incomes and customer preferences increasingly transitioning toward cars with fully loaded safety features are driving the market. The passenger cars segment is expected to lead the market during the forecast period.

As per research by EURO NCAP, 75% of all collisions in urban driving environments occur at speeds below 25 mph, with AEB having led to a 38% reduction in rear-end crashes. Autonomous vehicle technology offered with level 4 and 5 autonomous cars may become a large market worldwide over the coming years.

In line with the abovementioned developments globally, the demand for automatic emergency braking systems in passenger cars will be high over the coming years.

North America Expected to Lead the Market

Autonomous braking is provided with 51% of the model lines offered by OEMs across the United States. Tesla and Volvo offer AEB as a standard feature in 100% of their vehicles.

The US Department of Transportation's National Highway Traffic Safety Administration (NHTSA) recently issued a notice of proposed regulations that would require automatic emergency braking and pedestrian AEB systems for passenger vehicles and light trucks.

The proposed rule is expected to dramatically reduce pedestrian-related accidents and rear-end collisions. The NHTSA estimates that this proposed rule, if finalized, would save at least 360 lives per year and reduce the number of injuries by at least 24,000 annually.

In addition, these AEB systems would lead to a significant reduction in property damage caused by rear-end collisions. Many accidents could be avoided entirely, while others would be less destructive.

The Department's other road safety actions include the preparation of the Vulnerable Road User Safety Assessment to assist states with the required assessments for 2023. The safety performance of the state in terms of vulnerable road users and its plan to improve their safety are among the parameters assessed.

In line with growing technological advancements, OEMs must remain active in achieving their AEB commitments or face the possibility of brand erosion due to falling behind other market players in safety advances. In particular, the incorporation of AEB into the US government's safety ratings may alter consumer perception.

Based on the aforementioned developments, the market is expected to witness high growth in the upcoming period.

Automotive Autonomous Emergency Braking System Industry Overview

The automotive autonomous emergency braking system market is dominated by several key players, such as Robert Bosch GmbH, Continental AG, ZF Friendrichagen AG, Hyundai Mobis, and Hitachi Automotive System Ltd. Key players continue to gain a competitive edge in the global market by engaging in strategic approaches. Consistent advancements and innovations in braking systems have assisted manufacturers in gaining traction in the competitive market. For instance,

* In July 2023, ZF Friedrichshafen AG and Volta Trucks signed a long-term agreement for the integration of components and parts in the all-electric Volta Zero electric truck. ZF provided the OnGuardACTIVE advanced emergency braking system, the electronic braking system including the brake pedal box, the ESCsmart electronic stability control, and the OnHand electro-pneumatic handbrake.

* In June 2023, the US National Highway Transportation Safety Administration (NHTSA) announced that heavy trucks and buses must include automatic emergency braking equipment (AEB) within five years.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.1.1 Rise in Demand for Safety Features in Vehicles

- 4.2 Market Restraints

- 4.2.1 High Costs Associated with the System

- 4.3 Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size in Value - USD)

- 5.1 By Vehicle Type

- 5.1.1 Passenger Cars

- 5.1.2 Commercial Vehicles

- 5.2 By Technology

- 5.2.1 LiDar

- 5.2.2 Radar

- 5.2.3 Camera

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 India

- 5.3.3.2 China

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 Rest of the World

- 5.3.4.1 South America

- 5.3.4.2 Middle East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Mergers and Acquisitions

- 6.3 Company Profiles*

- 6.3.1 Robert Bosch GmbH

- 6.3.2 WABCO Holdings Inc.

- 6.3.3 Hyundai Mobis Co. Ltd

- 6.3.4 Denso Corporation

- 6.3.5 ZF Friedrichshafen AG

- 6.3.6 Continental AG

- 6.3.7 Autoliv Inc.

- 6.3.8 Valeo SA

- 6.3.9 Aisin Corporation

- 6.3.10 Delphi Automotive PLC