|

市場調査レポート

商品コード

1536797

自動車用アンチロックブレーキシステムと電子制御スタビリティコントロール:市場シェア分析、産業動向、成長予測(2024~2029年)Automotive Anti Lock Braking System And Electronic Stability Control - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 自動車用アンチロックブレーキシステムと電子制御スタビリティコントロール:市場シェア分析、産業動向、成長予測(2024~2029年) |

|

出版日: 2024年08月14日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

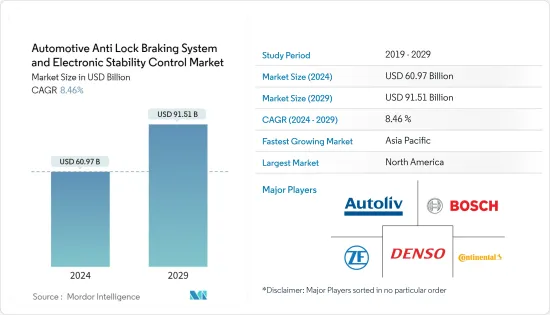

自動車用アンチロックブレーキシステムと電子制御スタビリティコントロール市場規模は、2024年に609億7,000万米ドルと推定・予測され、2029年には915億1,000万米ドルに達し、予測期間(2024-2029年)のCAGRは8.46%で成長すると予測されます。

2022年には、世界中で約8,500万台の自動車が生産されました。2022年、中国は乗用車生産の世界的リーダーとして頭角を現し、約2,384万台の自動車を319万台の商用車とともに生産し、世界の乗用車生産の第一人者としての地位を固めました。

長期的に見れば、ABSシステムが受け入れられつつあるのは、安全への関心が高まり、交通事故死が減少する可能性があるからです。交通事故が原因で毎日3,300人近くが死亡しており、死傷者の約10分の9は世界の自動車保有台数の半分に満たない中低所得国で発生しています。

自動車用アンチロックブレーキシステム市場は、これらのシステムがエントリーレベルの二輪車に広く使われ始めていることから、高い成長率を示すと予想されます。新興国市場の二輪車のほとんどは、標準的な安全機能を備えた高級車です。しかし、新興市場では、二輪車は最も安価なエントリーレベルの自動車です。このような安全システムの乗用車への採用が増加することで、予測期間中に市場が活性化すると予想されます。

しかし、アジア太平洋地域は自動車用アンチロックブレーキシステムの主要市場になると予測されています。予測期間中、日本、インド、中国が自動車製造の主要拠点となっています。

自動車用アンチロックブレーキシステム市場の動向

政府規制が乗用車へのABS採用を促進する見込み

世界の自動車台数の増加により、世界的に交通事故が大幅に増加しています。例えば

- 2023年7月、KostromaにあるItelma LLCの施設で乗用車用アンチロックブレーキシステム(ABS)と電子安定制御システム(ESP)の生産が開始され、ロシア初のこうした施設となった。同地方行政のプレスサービスがInterfaxに伝えました。

このプロジェクトを促進するために、完全自動化された生産ラインを備えた新しい作業場が建設されました。イテルマLLCは、ABSとESPシステムの現地製造ライセンスも取得しています。特筆すべきは、このプロジェクト全体が商業的に推進されており、補助金や政府資金に依存していないことです。生産能力は、国産ABSおよびESPシステムの年間生産台数85万台を目指しており、120万台まで拡張できる可能性があります。

自動車用アンチロックブレーキシステム市場は、アンチロックブレーキ(ABS)など、自動車の安全性と制御システムに対する需要の高まりが主な要因となっています。また、安全基準を定めた厳しい規制や、自動車の安全性の重要性を強調するさまざまなプログラムの開始も、市場の拡大を後押ししています。

欧州では2004年以降、すべての新型乗用車にABSの装着が義務付けられています。米国では、すべての新型乗用車にABSを義務付けるまでに10年近くかかった。米国運輸省道路交通安全局(NHTSA)は、2007年3月の連邦自動車安全基準(FMVSS)No.126の規定に基づいて、ESC(エレクトロニックスタビリティコントロール)とともにABSを義務付けた。

世界の自動車産業における安全基準の高まりは、発展途上国を先進国に追随させる原動力となっており、新車の乗用車にはABSが標準装備されて販売されています。インドの道路交通高速道路省(MoRTH)は、すべての新車乗用車と二輪車にABSを義務付けることを通達しました。2022年には、日本やブラジルなどでABSが義務化されたため、販売される乗用車の92%近くにABSが装着されています。

ほぼすべての国の政府によって実施されている厳しい規則や規制を考慮すると、将来的に市場が活性化すると思われます。

世界各国の政府規制がABS市場を牽引している

事故率の増加と死傷者数を減らすための世界各国政府の継続的な努力は、アンチロックブレーキシステム市場の重要な促進要因です。

アジア太平洋は、世界的に最も急成長している市場のひとつです。同地域のアンチロックブレーキシステム(ABS)需要の増加は、すべての新車にABSを装備させるという交通安全規則の強化によって支えられています。たとえば、

- インド政府は、すべての自動車とミニバスにアンチロックブレーキシステム(ABS)の装着を義務付けています。道路交通省によると、2018年4月以降、すべての新車はこの基準に適合しなければならないです。同様に、既存モデルの新車にもABSの装着が義務付けられます。さらに、125cc以上の二輪車にもABSの装着が義務付けられます。

- 規則(EU)第168/2013号に基づき、L3e-A1サブカテゴリーの二輪車には、メーカーの判断により、アンチロックブレーキシステム(ABS)または複合ブレーキシステム(CBS)のいずれか、あるいは両方からなる先進ブレーキシステムを装着しなければならないです。

米国運輸安全委員会(NTSB)は、米国における二輪車の製造工程でアンチロックブレーキの装着を推進しています。NTSBには法律を制定する権利はないため、交通安全規則の導入と施行を担当する組織であるNHTSAを説得することを目的としています。米国道路安全保険協会によると、アンチロックブレーキを装備しているオートバイは、装備していないオートバイに比べて事故率が31%低いです。

欧州連合議会は、2016年に製造されるオートバイにアンチロックブレーキシステムを標準装備することを義務付けた。米国道路安全保険協会の報告によると、2017年には登録二輪車の8.9%にアンチロックブレーキシステムの装着が義務付けられていました。この数字は、アンチロック・ブレーキ技術がオートバイの0.2%にしか標準装備されていなかった2002年以降、着実に増加しています。

アンチロックブレーキシステム(ABS)市場は予測期間中に成長すると予想されます。先進国および新興諸国は、死傷者数を減らすために、四輪車および二輪車にアンチロックブレーキシステム(ABS)を義務化しています。

自動車用アンチロックブレーキシステム業界の概要

Robert Bosch GmbH、Autoliv Inc.、Continental Reifen Deutschland GmbH、株式会社デンソー、ZF Friedrichshafen AGなどの大手企業が、自動車用アンチロックブレーキシステム市場を独占しています。

各社は、主要技術への戦略的投資、買収、提携を進めています。また、ほぼすべての乗用車がアンチロックブレーキシステムを搭載しており、市場成長を牽引しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場促進要因

- 自動車の安全性に関する厳しい規制

- 市場抑制要因

- 統合の複雑さ

- 業界の魅力- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 自動車タイプ

- 二輪車

- 乗用車

- 商用車

- 地域

- 北米

- 米国

- カナダ

- メキシコ

- その他北米地域

- 欧州

- ドイツ

- 英国

- フランス

- ロシア

- スペイン

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- 韓国

- その他アジア太平洋地域

- 世界のその他の地域

- ブラジル

- アルゼンチン

- アラブ首長国連邦

- 南アフリカ

- その他南米

- 北米

第6章 競合情勢

- ベンダー市場シェア

- 企業プロファイル

- Continental Reifen Deutschland GmbH

- Delphi Technologies PLC

- DENSO Corporation

- Autoliv Inc.

- ZF Friedrichshafen AG

- Robert Bosch GmbH

- Haldex AB

- WABCO Holdings Inc.

- Hyundai Mobis Co. Ltd

第7章 市場機会と今後の動向

- センサーとAIの統合

The Automotive Anti Lock Braking System And Electronic Stability Control Market size is estimated at USD 60.97 billion in 2024, and is expected to reach USD 91.51 billion by 2029, growing at a CAGR of 8.46% during the forecast period (2024-2029).

In 2022, some 85 million motor vehicles were produced worldwide. In 2022, China emerged as the global leader in passenger car production, manufacturing approximately 23.84 million vehicles alongside 3.19 million commercial vehicles, solidifying its position as the foremost producer of passenger cars worldwide.

Over the long term, the increasing acceptance of ABS systems is the growing focus on safety and the potential reduction in road-accident-related deaths. Nearly 3,300 people die every day due to road crashes, and about 9/10th of the casualties occur in middle and low-income countries that have less than half of the world's total vehicles.

The automotive anti-lock brake system market is expected to show a high growth rate as these systems are starting to be used extensively in entry-level two-wheelers. Most two-wheelers in the developed markets are high-end vehicles with safety features similar to the standard. However, in emerging markets, two-wheelers are the cheapest and entry-level vehicles. Increased adoption of such safety systems in passenger vehicles is expected to boost the market during the forecast period.

However, Asia-Pacific is projected to become the key automotive anti-lock braking system market. During the forecast period, Japan, India, and China are the major automotive manufacturing hubs.

Automotive Anti-lock Braking System Market Trends

Government Regulations Likely to Drive Adoption of ABS in Passenger Cars

Due to the rising number of motor vehicles worldwide, there has been a significant increase in road accidents globally. For instance,

- In July 2023, the production of anti-lock braking systems (ABS) and electronic stability control systems (ESP) for passenger cars commenced at the Itelma LLC facility in Kostroma, making it the first such facility in Russia. The regional administration's press service informed Interfax about this development.

A new workshop equipped with a fully automated production line has been constructed to facilitate this project. Itelma LLC is also licensed to manufacture ABS and ESP systems locally. Notably, the entire project is commercially driven, with no reliance on subsidies or government funds. The production capacity aims to achieve an annual output of 850,000 units of domestic ABS and ESP systems, with the potential for expansion to 1.2 million units.

The automotive anti-lock braking system market is primarily driven by the growing demand for vehicle safety and control systems in automobiles, such as anti-lock brakes (ABS). Also, strict regulations dictating safety standards and the launch of various programs highlighting the importance of vehicle safety have fuelled market expansion.

All new passenger cars must be equipped with ABS since 2004 in Europe. The United States took nearly a decade to mandate ABS in all new passenger cars. The National Highway Traffic Safety Administration (NHTSA) mandated ABS in conjunction with Electronic Stability Control (ESC) under the provisions of the March 2007 Federal Motor Vehicle Safety Standard (FMVSS) No. 126.

The increasing safety standards in the global automotive industry are driving developing countries to follow their developed counterparts, where new passenger cars are sold with ABS as a standard feature. The Ministry of Road Transport and Highways (MoRTH) in India notified that ABS is mandatory for all new passenger cars and two-wheelers. In 2022, nearly 92% of the passenger cars sold had been equipped with ABS, owing to the compulsory ABS rule in countries like Japan and Brazil.

Considering the strict rules and regulations implemented by the governments of almost all the countries will drive the market in the future.

Government Regulations Across the World are Driving the ABS Market

The increasing rate of accidents and the continuous efforts of governments worldwide to reduce the number of casualties is a significant driver for the anti-lock braking systems market.

Asia-Pacific is one of the fastest-growing markets globally. The increasing demand for the region's anti-lock braking system (ABS) is supported by increased road safety rules, ensuring all new vehicles are equipped with ABS. For instance,

- The Indian government has mandated that all cars and mini-buses install an anti-lock braking system (ABS). According to the Road Transport Ministry, all new vehicles must comply with the norms from April 2018 onward. Similarly, all new cars of the existing models will have to install the ABS. Moreover, ABS will be mandatory for two-wheelers with more than a 125cc engine.

- Under Regulation (EU) No. 168/2013, motorcycles in the L3e-A1 subcategory must be fitted with an advanced braking system consisting of either an anti-lock braking system (ABS) or a combined braking system (CBS) or both at the discretion of the manufacturer.

The National Transportation Safety Board (NTSB) promotes anti-lock brakes in the manufacturing process of motorcycles in the United States. The NTSB does not have the right to create laws, so it aims to persuade the NHTSA, an organization responsible for introducing and enforcing road safety rules. The Insurance Institute for Highway Safety found that motorcycles with anti-lock brakes have a 31% lower crash rate than bikes without the feature.

The European Union parliament mandated that anti-lock braking systems be the standard equipment for motorcycles built in 2016. The Insurance Institute of Highway Safety reported that 8.9% of registered motorcycles were required to have anti-lock brake systems in 2017. This number has increased steadily since 2002, when anti-lock brake technology was considered standard equipment on only 0.2% of motorcycles.

The anti-lock brake system (ABS) market is anticipated to grow during the forecast period. Developed and developing countries are making the anti-lock braking system (ABS) mandatory for four-wheelers and two-wheelers to reduce the number of casualties.

Automotive Anti-lock Braking System Industry Overview

Major players, such as Robert Bosch GmbH, Autoliv Inc., Continental Reifen Deutschland GmbH, DENSO Corporation, and ZF Friedrichshafen AG, dominate the automotive anti-lock braking system market.

The companies are strategically investing, making acquisitions, and entering into partnerships in key technologies. Also, almost all passenger vehicles have an anti-lock braking system, driving market growth.

- In March 2022, ZF announced that its new Commercial Vehicle Solutions division would introduce its entire product and technology portfolio for heavy-duty trucking applications at TMC 2022 in Orlando. ZF's show floor exhibit includes a virtual tour of the company's entire commercial vehicle product line, including chassis technology: air management; suspension solutions; air disc brakes, brake actuators, and vacuum pumps; vehicle dynamics: ADAS, anti-lock braking systems (pneumatic and hydraulic), and steering solutions.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.1.1 Strict Rules and Regulations in Vehicle Safety

- 4.2 Market Restraints

- 4.2.1 Integration Complexity

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Vehicle Type

- 5.1.1 Motorcycles

- 5.1.2 Passenger Cars

- 5.1.3 Commercial Vehicles

- 5.2 Geography

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.1.3 Mexico

- 5.2.1.4 Rest of North America

- 5.2.2 Europe

- 5.2.2.1 Germany

- 5.2.2.2 United Kingdom

- 5.2.2.3 France

- 5.2.2.4 Russia

- 5.2.2.5 Spain

- 5.2.2.6 Rest of Europe

- 5.2.3 Asia-Pacific

- 5.2.3.1 China

- 5.2.3.2 Japan

- 5.2.3.3 India

- 5.2.3.4 South Korea

- 5.2.3.5 Rest of Asia-Pacific

- 5.2.4 Rest of the World

- 5.2.4.1 Brazil

- 5.2.4.2 Argentina

- 5.2.4.3 United Arab Emirates

- 5.2.4.4 South Africa

- 5.2.4.5 Rest of South America

- 5.2.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share**

- 6.2 Company Profiles*

- 6.2.1 Continental Reifen Deutschland GmbH

- 6.2.2 Delphi Technologies PLC

- 6.2.3 DENSO Corporation

- 6.2.4 Autoliv Inc.

- 6.2.5 ZF Friedrichshafen AG

- 6.2.6 Robert Bosch GmbH

- 6.2.7 Haldex AB

- 6.2.8 WABCO Holdings Inc.

- 6.2.9 Hyundai Mobis Co. Ltd

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Integration of Sensors and AI