|

市場調査レポート

商品コード

1851076

クラウド無線アクセスネットワーク:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Cloud Radio Access Network - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| クラウド無線アクセスネットワーク:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年06月19日

発行: Mordor Intelligence

ページ情報: 英文 106 Pages

納期: 2~3営業日

|

概要

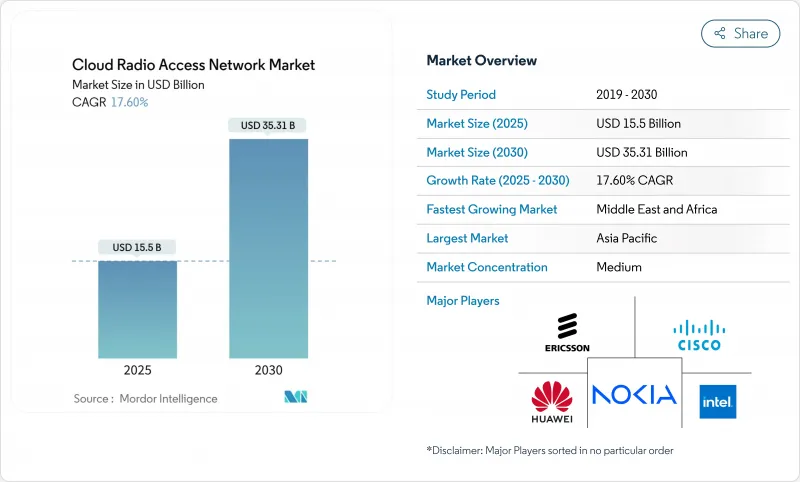

クラウド無線アクセスネットワーク市場規模は2025年に155億米ドル、2030年には353億1,000万米ドルに達すると推定・予測され、予測期間(2025-2030年)のCAGRは17.60%です。

5Gの急速な展開、ベースバンド処理の集中化の推進、ネットワーク運用コストの削減へのプレッシャーの高まりにより、需要は高止まりしています。通信事業者は、クラウドにリソースをプールすることでセルサイトのスループットと周波数利用を向上させる、密集した都市クラスターにおけるマルチレイヤーのカバレッジ戦略を策定しています。米国、日本、欧州の主要都市における商業実証は、AI支援スケジューリングがアクティブ無線全体の消費電力を削減し、ネットワークの近代化と同時に持続可能性目標をサポートできることを示しています。既存ベンダーがソフトウェア中心の参入企業からシェアを守るために競争が激化しており、無線、コンピュート、シリコンの専門知識を組み合わせて製品ロードマップを加速させる提携が相次いでいます。クラウド無線アクセスネットワーク市場は、政策的な支援策から恩恵を受けているもの、国によって大きく異なる周波数帯域の解放スケジュールやフロントホールのボトルネックに関連する逆風に直面しています。

世界のクラウド無線アクセスネットワーク市場の動向と洞察

5Gの急速な普及と高密度化がアーキテクチャの変化を促す

世界の通信事業者は、ミッドバンド5Gレイヤーをライトアップし、カバレッジギャップを埋めるためにスモールセルを追加しています。このような環境において、クラウド無線アクセスネットワーク市場は、ハードウェアを重複させることなく、何千もの無線を管理するために必要な集中型コンピュートプールを提供します。東京、ソウル、ニューヨークでの実地試験では、ベースバンドのワークロードを動的にシフトさせることで、利用率を30%向上させ、セルのピークスループットを25%向上させることができました。商用5Gスタンドアロン・コアは現在、仮想ベースバンド機能と時間的制約のあるスケジューリングを調整しており、クラウドネイティブの原則が機能リリース・サイクルをいかに短縮するかを明確に示しています。中国と米国での大規模な展開により、同じクラウドサイトで複数の無線世代をホストできることが明らかになり、周波数帯の再調達の決定が容易になり、漸進的な移行経路がサポートされるようになりました。このような利点は、特に屋内カバレッジの義務で高密度の無線グリッドが必要とされる場合、継続的な投資に拍車をかける。

CAPEXとOPEXの削減がビジネスケースを支える

仮想化ベースバンドプールの経済的な魅力は即座に発揮されます。プーリングにより、ハードウェアの重複が減り、不動産費用が削減され、アップグレードが簡素化されます。北米のベンダーのケーススタディによると、3種類のレガシーベースバンドを単一のクラウドクラスタに統合した事業者は、1年間のロールアウトでCAPEXを3分の1近く削減できたといいます。自動化ツールによって予防保守やリモート・ソフトウェア更新の規模が拡大すると、OPEXも減少します。AIスケジューラーがオフピーク時に負荷の軽い無線をディープスリープモードにすることで、ネットワークの電力効率プロファイルが改善され、エネルギー代が減少します。このような節約は、積極的な5G拡張計画を支えるものであり、特に通信事業者にとっては、配当コミットメントとサービス品質向上の必要性とのバランスを取る上で重要です。パブリック・クラウドの消費ベースの価格設定モデルが普及するにつれて、通信事業者はトラフィックのピークに合わせて支出を調整する柔軟性が増し、クラウド・アーキテクチャの魅力が高まっています。

スペクトルの希少性と規制の制限による勢いの低下

ミッドバンド周波数帯のタイムリーなクリアランスとオークションは、依然として全国的な5G構築の抑制要因となっています。米国連邦通信委員会のオークション権限が2024年に失効したことで、将来のリリースに関する不確実性が生じ、一部の通信事業者の投資サイクルが鈍化しました。また、多くの新興市場では、クラウドRANに最適化された5Gレイヤーのターンキー展開を遅らせる不透明な割り当てプロセスや政治主導の割り当てプロセスに取り組んでいます。ライセンスが整備されている場合でも、ガードバンド条件や電力レベルの上限によってネットワークレイアウトが制限されることがあり、事業者は無線計画を複雑にする断片的な保有物に頼らざるを得ないです。このような現実は、展開速度を緩やかにし、プーリングの経済性が説得力を持つようになる時点を先送りする可能性があります。

セグメント分析

ソリューションの市場セグメンテーション市場規模は、2024年には113億米ドルに達し、セグメント収益の73%に相当します。しかし、マルチベンダー環境が主流になるにつれて、サービス市場のCAGRは18.4%と急速に拡大しています。初期のグリーンフィールド導入では、主にハードウェアと仮想化ベースバンドライセンスが必要だったが、現在のブラウンフィールドでのアップグレードでは、統合、ネットワークの最適化、ライフサイクルサポートが求められています。欧州の通信事業者は、AI主導のパフォーマンス分析とDevOpsの実現をバンドルした複数年のマネージドサービス契約を締結し、社内チームが新サービスの設計を優先できるようにしています。コンサルティングチームは現在、レガシー4Gトラフィックと新たなプライベート5Gユースケースのバランスを取る既存キャリアにとって重要な役割である、周波数帯のリファーミング、機能分割の選択、移行の順序決定を指導しています。ハードウェア・プロバイダは、オープン・インターフェイスとリファレンス・オートメーション・ワークフローを組み込むことで対応し、製品とプロフェッショナル・サービスの境界線を曖昧にしています。2030年が近づくにつれ、このような組み合わせは、クラウド無線アクセスネットワーク市場の収益プールに占めるサービスの割合を高めることになります。

着実な技術革新の流れがソリューション事業の活力を維持しています。シリコンメジャーの各社は、ビームフォーミングとフォワードエラー補正のための統合アクセラレーションを導入し、ラックユニット当たりのベースバンド容量を2023年ブレードと比較して2倍以上に引き上げました。無線サプライヤーは、屋上や屋内用に調整された軽量のMassive MIMOアレイによって、これらの利点を補完しています。このような進歩は、総所有コストを削減すると同時に、対応可能な顧客ベースを拡大し、ソリューション側の収益成長を緩やかながらも一貫して支えています。その結果、ソフトウェア、シリコン、サービスがそれぞれ、一元的にオーケストレーションされた無線レイヤーへの移行を強化し、市場セグメンテーションの既存セグメントや企業セグメントでの採用を拡大するという、バランスの取れた状況になっています。

2024年には、通信事業者がミッドバンド周波数帯の活用に資本を投下するため、5G層がクラウド無線アクセスネットワーク市場全体の収益の61%を占める。通信事業者は、インダストリー4.0のワークロードに不可欠なスライシングと超低遅延パイプラインを可能にするスタンドアロン・アーキテクチャに迅速に転換しました。仮想化されたベースバンドプールは、一般的なサーバー上で非スタンドアロンの5G、LTE、NRを実行することを可能にし、キャリアは容量のアップグレードを優先して3Gを段階的に廃止することができます。4G LTEは依然として有意義なリターンを生み出しているが、データ量の多い消費者の利用が補助金付きのデバイスを使った5Gバンドルに引き寄せられるにつれて、そのシェアは年々低下しています。

オープンRANは、サプライチェーンの多様化に熱心な北米とアジアのティアオンの注目度の高いコミットメントによって後押しされ、2030年まで27%のCAGRで最も速い軌道を示しています。このモデルのオープン・インターフェースは、ベスト・オブ・ブリードの組み合わせを促進するが、統合のオーバーヘッドは依然として大きいです。とはいえ、ダラスとソウルで実稼働しているネットワークの試験結果は、統一されたクラウドプラットフォームからオーケストレーションすれば、マルチベンダーのMassive MIMOスタックがモノリシックなシステムと同等のスペクトル効率を達成できることを示しています。米国政府からの助成金プログラムなどの規制支援も、さらに勢いを増しています。これらの力を総合すると、Open RANは主要なディスラプターとして位置付けられ、サプライヤーの多様性を広げると同時に、市場全体の競争力学を激化させています。

地域分析

アジア太平洋地域は、2024年の売上シェア39%でクラウド無線アクセスネットワーク市場を独占し、CAGR 23.1%で成長をリードしています。中国、日本、韓国の積極的な5G展開は、大規模な地域データセンターにリンクされた高密度スモールセルグリッドに依存しています。深センとソウルの通信事業者は、すでに中核ビジネス街で商用オープンインターフェイスクラスターを運用しており、祭りのピーク時のビデオストリーミングのためのリアルタイム周波数プーリングを披露しています。政府は、仮想化投資に対する周波数帯料金のリベートなど、支援的な政策枠組みを提供しています。ベンダーのエコシステムはオープンテストベッドを中心に発展し、OREXイニシアチブのようなジョイントベンチャーは輸出の機会を狙い、この地域のリーダーシップを確固たるものにしています。

北米は売上高で第2位です。米国の通信事業者は、2026年までにレガシー・ハードウェアをオープン対応無線に切り替えるため、数十億米ドルの予算を計上しました。CHIPSおよび科学法に基づく連邦補助金は、AIベースのスケジューリングエンジンを強化するシリコン研究に共同出資し、国内のサプライチェーンに高い回復力を与えます。ラスベガスとシアトルでの初期導入により、GPUアクセラレーションを用いたクラウドノードが、XRゲームや産業オートメーション向けのミリ秒レベルの厳しいレイテンシ目標を達成できることが証明されます。カナダの事業者がフィンランドや韓国のベンダーと協力することで、地域のイノベーション領域が拡大し、より広いクラウド無線アクセスネットワーク市場をサポートする国境を越えた技術交流が強調されています。

欧州では、規制の強化と競合の必要性により、導入が加速しています。英国、ドイツ、スペインの通信事業者は、無線、ベースバンド、管理システム間の相互運用性を証明する公的テストラボに支えられ、最初の商用5G Open RANマクロサイトを展開しました。欧州連合(EU)は、5Gおよび6Gネットワークの研究開発に資金を提供しており、RANソフトウェアの人材確保のための産学パイプラインを強化しています。単体での5Gカバー率が遅れているにもかかわらず、既存事業者は、総所有コストの削減とサービス革新の迅速化を主な動機として、無線レイヤーのクラウド化計画を急ピッチで進めています。現在進行中のインフラ・プログラムにより、地方回廊を通るファイバー・バックボーンがアップグレードされ、歴史的なボトルネックが解消されるとともに、クラウド無線アクセスネットワークの市場展開が地域全体でさらに拡大します。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 急速な5G展開と高密度化

- 集中ベースバンドによるCAPEX-OPEXの節約

- モバイルデータの指数関数的成長

- ネットワーク仮想化とSDNの需要

- AIによるRAN最適化の採用

- エネルギー効率規制がクラウドRANを後押し

- 市場抑制要因

- 周波数帯の希少性と規制の限界

- 限られたフロントホール・ファイバーと遅延の課題

- 集中型アーキテクチャにおけるセキュリティとプライバシーのリスク

- 新興市場における不確実なROI

- バリュー/サプライチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

- 投資分析

第5章 市場規模と成長予測

- コンポーネント別

- ソリューション

- サービス

- プロフェッショナル

- マネージド

- ネットワークタイプ別

- 5G

- 4G

- LTE

- 3G(EDGE)

- 展開モデル別

- 集中型RAN(C-RAN)

- 仮想化RAN(vRAN)

- オープンRAN(O-RAN)

- ハイブリッド・クラウドRAN

- エンドユーザー別

- モバイルネットワーク事業者

- 企業

- 政府・公共安全

- ニュートラルホスト/タワーコス

- 地域別

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- その他欧州地域

- アジア太平洋地域

- 中国

- 日本

- 韓国

- インド

- その他アジア太平洋地域

- 南米

- ブラジル

- その他南米

- 中東・アフリカ

- GCC

- 南アフリカ

- トルコ

- その他中東・アフリカ地域

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Huawei Technologies Co. Ltd.

- Nokia Corporation

- Telefonaktiebolaget LM Ericsson

- Cisco Systems Inc.

- Samsung Electronics Co. Ltd.

- ZTE Corporation

- Intel Corporation

- Fujitsu Limited

- NEC Corporation

- Mavenir Systems Inc.

- Parallel Wireless Inc.

- Rakuten Symphony

- Altiostar(Rakuten)

- CommScope Holding Co. Inc.

- Casa Systems Inc.

- Airspan Networks Inc.

- Hewlett Packard Enterprise(HPE)