|

市場調査レポート

商品コード

1521908

食品用ポストコンシューマーリサイクル(PCR)包装:市場シェア分析、産業動向、成長予測(2024~2029年)Food-grade Post-Consumer Recycled (PCR) Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 食品用ポストコンシューマーリサイクル(PCR)包装:市場シェア分析、産業動向、成長予測(2024~2029年) |

|

出版日: 2024年07月15日

発行: Mordor Intelligence

ページ情報: 英文 103 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

食品用ポストコンシューマーリサイクル(PCR)包装市場規模は、出荷量ベースで2024年の586万トンから2029年には837万トンに、予測期間(2024~2029年)のCAGRは7.38%で成長すると予測されます。

主要ハイライト

- エネルギー使用量の削減、排出量の削減、循環型経済の推進、持続可能性目標の達成、包装廃棄物の削減、接触に敏感な用途に関するFDAやその他の規制、規制圧力などのニーズの高まりが、食品用消費者リサイクル後の包装ソリューションの需要を促進している主要要因です。

- リサイクルインフラの整備、先進的なリサイクルプロセス、効果的な処理技術、政府の積極的な対応により、包装のリサイクル率は世界的に上昇しています。その結果、消費者使用後のリサイクル材料の利用可能性が高まっています。環境庁によると、英国の包装リサイクル目標は、2023年の77%に対し、2024年末には80%に達すると予想されています。リサイクル率の増加は、食品用ポストコンシューマーリサイクル包装ソリューションの成長を助けると予想されます。

- エンドユーザーであるブランドは、競争に勝ち残り、消費者の消費後リサイクル(PCR)包装に対する意識の高まりに対応するため、規制措置を遵守しようとしています。例えば、アメリカの飲料会社であるKeurig Dr Pepperは、2025年までに同社の製品包装・ポートフォリオ全体でバージンプラスチックの使用量を20%削減し、プラスチック包装のリサイクル含有量を増やすことを約束しています。

- 包装メーカーは、先進技術を駆使して、革新的な接触感応型ポストコンシューマーリサイクル包装ソリューションを開発しています。さらに、原料メーカー、供給業者、コンバーターは最新のリサイクル技術を採用し、食品用PCR材料を提供しています。

- 2024年、Borealis AGは、食品用包装に使用される消費者使用後再生プラスチック(PCR)「Borcycle M」について、米国食品医薬品局(FDA)から異議なし(LNO)の通知を受け取った。この材料は、化粧品、パーソナルケア、食品接触などの包装用途に敏感です。同社は、革新的なメカニカルリサイクル技術を用いてBorcycle M消費者再生プラスチック(PCR)を開発しました。この技術は、エネルギー効率の高い方法で、消費者使用後のプラスチック廃棄物に新たな命を与えます。

- これに加えて、プラスチック材料の不適切なリサイクルによる、より多くの材料利用可能性の必要性が、供給問題を生み出しています。不適切に廃棄された包装材は、リサイクル時に汚染問題を引き起こし、市場の成長を妨げる可能性があります。リサイクル業者による継続的な努力とEPRによる投資の増加は、リサイクル回収とインフラを改善すると予測されます。これにより、材料入手の懸念を克服できると期待されます。

食品用ポストコンシューマーリサイクル(PCR)包装市場の動向

飲食品業界におけるリサイクル(PCR)包装ソリューションの採用増加

- 飲食品は、その品質を維持し、包装溶液との接触による化学反応を避けるため、ほとんどが食品用包装で梱包されます。これらのソリューションには、プラスチック、ガラス、金属、紙で作られたボトル、缶、パウチ、液体カートンなどが含まれます。

- サステイナブル包装ソリューションへの注目が高まる中、規制や消費者の意識が高まるにつれ、ブランドオーナーは消費者使用後のリサイクル包装ソリューションを求めるようになっています。例えば、2023年10月、Coca-Cola Indiaは250mLと750mLのrPETボトル入りのコカ・コーラを発売しました。さらに2024年4月、Coca-Colaは香港でrPET製の500mlボトルを発売しました。同社は2030年までに、包装ライン全体で50%の再生材料を使用することを目指しています。これは、循環型経済と持続可能で環境に優しい未来に向けた同社の歩みを示しています。

- 包装メーカー各社も、拡大するビジネス機会を生かすため、食品接触包装向けに革新的なポストコンシューマーリサイクル包装ソリューションを提供しようとしています。各社は、食品接触包装や接触に敏感な用途の規制要件に対応するため、先進的なリサイクルプロセスの採用に注力しています。

- 2024年3月、Amcor Group GmbHは、INEOS Olefins &Polymers EuropeとPepsiCoと共同で、PepsiCoのスナックブランド「Sunbites Crisps」の新しいスナック包装を発売しました。この新しい包装には、再生プラスチックが50%使用されています。プラスチックエナジーの技術により、消費者から排出されるプラスチック包装廃材が変換されます。従来の化石原料の代替として熱分解油を使用し、再生材料を製造し、食品接触性能要件を満たすようにコンパイルします。

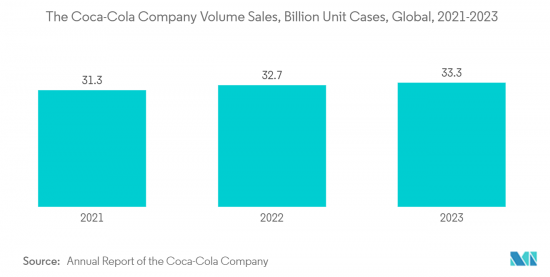

- 飲食品の消費量の増加と、サステイナブル包装へのブランドの注目が、食品用消費者使用後のリサイクル(PCR)包装ソリューションの成長を後押ししています。飲料・食品ブランドの販売数量の急増が市場の成長を助けています。主要なノンアルコール飲料ブランドであるCoca-Colaは、2022年に327億ユニットケースを販売したのに対し、2023年には333億ユニットケース(1ユニットケースは完成飲料192米国液量オンスに相当)を販売しました。

包装製品にリサイクル率を含めるよう求める各地域での規制圧力の高まり

- 様々な環境問題につながる包装廃棄物の増加により、リサイクル可能、消費者使用後の再生材料、生分解性などのサステイナブル包装ソリューションの必要性が生じています。持続可能性への懸念を克服するため、欧州、カナダ、米国など様々な地域の政府やその他の規制機関は、包装ソリューションに消費者再利用後の材料を使用するよう圧力をかけています。これは温室効果ガス排出量とエネルギー消費量の削減につながり、循環型経済に貢献します。

- 例えば、2024年4月、欧州議会は、循環型経済への移行に貢献する包装包装廃棄物規則(PPWR)を採択しました。PPWRには、市場に出回るプラスチック包装材にリサイクル率を最低限含ませるなど、包装ソリューションに関するさまざまな規定が盛り込まれています。

- 例えば、使い捨ての飲料用ペットボトルは30%PCR、接触に敏感なPET包装は30%PCR、接触に敏感なその他のプラスチック包装は10%PCRです。これらの最低割合は2040年以降増加します。この地域におけるこのような規定は、食品用消費者使用後のリサイクル(PCR)包装ソリューションの需要を促進すると予想されます。

- 同様に、カナダ環境大臣評議会によるプラスチック廃棄物ゼロに関する行動計画では、2030年までにプラスチック包装製品に50%のリサイクル率を要求することを明記した規定が承認されました。その範囲には、飲料包装容器、非飲食品ボトル、その他の硬質容器やトレイが含まれます。

- 2023年初めには、カリフォルニア州、ワシントン州、ニュージャージー州、メイン州が、プラスチック包装材に消費者使用後の再生材含有量を義務付ける法律を可決しました。カリフォルニア州の法律では、2025年までにガラスとプラスチックの飲料ボトルに25%、2050年までに50%のPCRを義務付けており、ワシントン州の法律では、2026年までにプラスチックの飲料ボトルに25%、2025年までにプラスチックのワインと乳製品の容器に15%のPCRを義務付けています。

- 食品に接触する製品には、損傷を避けるために食品用包装が義務付けられています。飲食品へのポストコンシューマーリサイクル材料の使用に関する規定と規制の増加は、食品用ポストコンシューマーリサイクル(PCR)包装の成長を助けると予想されます。

食品用ポストコンシューマーリサイクル(PCR)包装業界概要

食品用ポストコンシューマーリサイクル(PCR)包装市場はセグメント化されており、様々な世界企業やローカル企業が存在します。同市場の包装業者は、規制圧力の高まりに対応し、持続可能性目標を達成し、包装タイプに対する最小PCR含有量の需要に応えるため、食品用ポストコンシューマーリサイクル(PCR)包装ソリューションを提供しようとしています。市場の主要参入企業は、市場シェアを強化し、競合他社よりも優位に立つために新しいソリューションを開発しています。

- 2024年4月、Amcor Group GmbHは、炭酸清涼飲料(CSD)用の100%消費者再利用(PCR)コンテンツを使用した1リットルのポリエチレンテレフタレート(PET)ボトルの発売を発表しました。同社は、再生材を使用した責任ある包装の製品ポートフォリオを拡大し、顧客が持続可能性に関するコミットメントや要件を満たせるよう支援することに注力しています。

- 2024年4月、Klockner Pentaplastは100%再生PET(rPET)を使用した食品包装用トレイの発売を発表しました。100%再生PET食品トレイの発売により、同社は品質や安全性を損なうことなく、よりサステイナブル包装業界の実現に注力しています。

- 2023年12月、Novolex Holdings LLCは、消費者再生利用(PCR)原料を10%以上使用した食品用包装容器を発表しました。これらの容器はリサイクル可能です。新製品の発売により、同社は環境への影響を低減し、循環型経済を支援します。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブ概要

第4章 市場洞察

- 市場概要

- 産業バリューチェーン分析

- 業界の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 地政学的シナリオが業界に与える影響の評価

第5章 市場力学

- 市場促進要因

- 持続可能性への懸念を克服するための消費者意識の高まりと温室効果ガス排出量削減の必要性

- 包装製品にリサイクル率を最低限含めるよう求める規制圧力の高まり

- 市場抑制要因

- 不十分なリサイクル・インフラは不適切な材料供給と高価格につながる

第6章 市場セグメンテーション

- 材料別

- プラスチック

- ポリエチレンテレフタレート(PET)

- ポリエチレン(PE)

- ポリプロピレン(PP)

- その他のプラスチック

- ガラス

- 金属

- 紙・板紙

- プラスチック

- 製品タイプ別

- ボトル・容器

- 缶

- パウチ・袋

- トレイとクラムシェル

- その他

- エンドユーザー産業別

- 食品

- 飲料

- パーソナルケアと化粧品

- 医療と医薬品

- その他

- 地域

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- アジア

- 中国

- 日本

- インド

- オーストラリア・ニュージーランド

- ラテンアメリカ

- ブラジル

- アルゼンチン

- メキシコ

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- エジプト

- 北米

第7章 競合情勢

- 企業プロファイル

- Berry Global Group Inc.

- Amcor Group GmbH

- Novolex Holdings LLC

- Tekni-Plex Inc.

- Klockner Pentaplast

- Coveris Management GmbH

- Hoffmann Neopac AG

- Silgan Dispensing Systems(Silgan Holdings Inc.)

- Greiner Packaging International GmbH

- Avery Dennison Corporation

- Nussbaum Matzingen AG

- Gallo Glass Company

- Great Little Box Company Ltd

第8章 投資分析

第9章 市場の将来

The Food-grade Post-Consumer Recycled Packaging Market size in terms of shipment volume is expected to grow from 5.86 Million tonnes in 2024 to 8.37 Million tonnes by 2029, at a CAGR of 7.38% during the forecast period (2024-2029).

Key Highlights

- The increasing need for reducing energy use, lowering emissions, promoting a circular economy, achieving sustainability targets, reducing packaging waste, FDA and other regulations for contact-sensitive applications, and regulatory pressure are the major factors propelling the demand for food-grade post-consumer recycling packaging solutions.

- Packaging recycling rates worldwide are increasing due to the development of recycling infrastructure, advanced recycling processes, effective processing techniques, and positive government response. This will result in increased availability of post-consumer recycled material. According to the Environment Agency, the packaging recycling target in the United Kingdom is expected to reach 80% by the end of 2024, compared to 77% in 2023. The increasing recycling rate is expected to aid the growth of food-grade post-consumer recycling packaging solutions.

- End-user brands are trying to adhere to regulatory measures to stay ahead of the competition and address the growing consumer awareness for post-consumer recycled packaging. For instance, Keurig Dr Pepper, an American beverage company, committed to reducing virgin plastic use by 20% across the company's product packaging portfolio by 2025 and increasing recycled content in plastic packaging.

- Packaging manufacturers are developing innovative, contact-sensitive, post-consumer recycled packaging solutions using advanced technologies. Furthermore, raw material manufacturers, providers, and converters are adopting the latest recycling technology to offer food-grade PCR material.

- In 2024, Borealis AG received letters of no objection (LNOs) from the US Food & Drug Administration (FDA) for its Borcycle M post-consumer recycled plastics (PCR) used for food-grade packaging. This material is sensitive to packaging applications, including cosmetics, personal care, and food contact. The company developed Borcycle M post-consumer recycled plastics (PCR) using transformational mechanical recycling technology. This technology offers post-consumer plastic waste another life in an energy-efficient way.

- Besides this, the need for more material availability due to the improper recycling of plastic material creates supply issues. The improperly discarded packaging material creates contamination problems during recycling, which may hamper the market's growth. The continuous effort by the recyclers and increasing investments driven by EPR are projected to improve recycling collection and infrastructure. This is expected to overcome the concern of material availability.

Food-grade Post-Consumer Recycled (PCR) Packaging Market Trends

Rising Adoption of Recycled Packaging Solutions in the Food and Beverage Industry

- Food and beverage products are mostly packed in food-grade packaging to maintain their quality and avoid any chemical reaction when in contact with the packaging solution. These solutions include bottles, cans, pouches, and liquid cartons made from plastic, glass, metal, or paper.

- Considering the increasing focus on sustainable packaging solutions, along with propelling regulation and consumer awareness, brand owners are looking for post-consumer recycled packaging solutions. For instance, in October 2023, Coca-Cola India launched Coca-Cola in 250-mL and 750-mL rPET bottles. Furthermore, in April 2024, Coca-Cola rolled out 500-ml bottles made from rPET in Hong Kong. The company aims to implement 50% recycled material across its packaging lines by 2030. This showcases the company's journey toward a circular economy and a sustainable and greener future.

- Packaging manufacturers are also trying to offer innovative post-consumer recycled packaging solutions for food contact packaging to take advantage of growing opportunities. The companies are focusing on adopting an advanced recycling process to cater to the regulatory requirements for food contact packaging and contact-sensitive applications.

- In March 2024, Amcor Group GmbH collaborated with INEOS Olefins & Polymers Europe and PepsiCo to launch a new snack packaging for PepsiCo's snack brand, Sunbites Crisps. The new packaging contains 50% recycled plastic. Post-consumer plastic packaging waste is converted using Plastic Energy's technology. Pyrolysis oil is used as an alternative to traditional fossil feedstock to produce recycled material and compile it to meet food contact performance requirements.

- The increasing consumption of food and beverage products and the brand's focus on sustainable packaging fuel the growth of food-grade post-consumer recycled packaging solutions. The surge in the unit volume sales of the beverage and food brands aids the market's growth. The major non-alcoholic beverage brand, the Coca-Cola Company, sold 33.3 billion unit cases (one unit case equal to 192 US fluid ounces of finished beverage) in 2023 compared to 32.7 billion unit cases in 2022.

Increasing Regulatory Pressure in Various Regions to Include a Minimum Percentage of Recycled Content for Packaging Products

- Increasing packaging waste, which leads to various environmental problems, has created the need for sustainable packaging solutions such as recyclable, post-consumer recycled material, biodegradable, and others. To overcome the sustainability concern, governments and other regulatory agencies in various regions, such as Europe, Canada, the United States, and others, are putting pressure on using post-consumer recycled material for packaging solutions. This would result in lower greenhouse gas emissions and lower energy consumption and contribute to a circular economy.

- For instance, in April 2024, the European Parliament adopted the Packaging and Packaging Waste Regulation (PPWR), which would contribute to the transition to a circular economy. It includes various provisions for packaging solutions, such as the requirement that any plastic packaging placed on the market contain a minimum percentage of recycled content.

- The minimum percentage of recycled content will depend upon the packaging type, such as 30% PCR for single-use plastic beverage bottles, 30% PCR for contact-sensitive PET packaging, and 10% PCR for contact-sensitive other plastic packaging. These minimum percentages would increase from 2040. Such provision in the region is expected to drive the demand for food-grade post-consumer recycled packaging solutions.

- Similarly, the Action Plan on Zero Plastic Waste by the Canadian Council of Ministers of the Environment endorsed a provision stating a 50% recycled content requirement in plastic packaging products by 2030. The scope includes beverage packaging containers, non-food bottles, and other rigid containers and trays.

- In early 2023, California, Washington, New Jersey, and Maine passed laws requiring post-consumer recycled content in plastic packaging. California's law requires 25% PCR for glass and plastic beverage bottles by 2025 and 50% by 2050, while Washington's law requires 25% PCR for plastic beverage bottles by 2026 and 15% PCR for plastic wine and dairy containers by 2025.

- Food-grade packaging is required for products that come in contact with it to avoid damage. The increasing provision and regulation over the use of post-consumer recycled material for beverage products is expected to aid the growth of food-grade post-consumer recycled packaging.

Food-grade Post-Consumer Recycled (PCR) Packaging Industry Overview

The food-grade post-consumer recycled (PCR) packaging market is fragmented, with various global and local players. The packaging players in the market are trying to offer food-grade post-consumer recycled packaging solutions to adhere to the growing regulatory pressure, attain sustainability targets, and cater to the demand for minimum PCR content for packaging type. The key players in the market are developing new solutions to strengthen the market share and stay ahead of the competitors.

- In April 2024, Amcor Group GmbH announced the launch of a one-liter polyethylene terephthalate (PET) bottle made from 100% post-consumer recycled (PCR) content for carbonated soft drinks (CSD). The company focuses on expanding the product portfolio for responsible packaging made from recycled content and helping customers meet sustainability commitments and requirements.

- In April 2024, Klockner Pentaplast announced the launch of food packaging trays made with 100% recycled PET (rPET). With the launch of 100% recycled PET food trays, the company is focusing on creating a more sustainable packaging industry without compromising quality or safety.

- In December 2023, Novolex Holdings LLC introduced packaging containers for food made with a minimum of 10% post-consumer recycled (PCR) content. These containers are recyclable. The launch of new products will help the company reduce the environmental impact and support the circular economy.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Assessment of the Geopolitical Scenario Impact on the Industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rising Consumer Awareness and Need for Lowering Greenhouse Gas Emissions to Overcome the Sustainability Concerns

- 5.1.2 Increasing Regulatory Pressure to Include a Minimum Percentage of Recycled Content for Packaging Products

- 5.2 Market Restraint

- 5.2.1 Inadequate Recycling Infrastructure Leads to Improper Supply of Materials and Results in High Prices

6 MARKET SEGMENTATION

- 6.1 By Material

- 6.1.1 Plastic

- 6.1.1.1 Polyethylene Terephthalate (PET)

- 6.1.1.2 Polyethylene (PE)

- 6.1.1.3 Polypropylene (PP)

- 6.1.1.4 Other Plastics

- 6.1.2 Glass

- 6.1.3 Metal

- 6.1.4 Paper & Paperboard

- 6.1.1 Plastic

- 6.2 By Product Type

- 6.2.1 Bottles and Containers

- 6.2.2 Cans

- 6.2.3 Pouches and Bags

- 6.2.4 Trays and Clamshells

- 6.2.5 Other Product Types

- 6.3 By End-user Industry

- 6.3.1 Food

- 6.3.2 Beverage

- 6.3.3 Personal Care and Cosmetics

- 6.3.4 Healthcare and Pharmaceuticals

- 6.3.5 Other End User Industry

- 6.4 Geography***

- 6.4.1 North America

- 6.4.1.1 United States

- 6.4.1.2 Canada

- 6.4.2 Europe

- 6.4.2.1 United Kingdom

- 6.4.2.2 Germany

- 6.4.2.3 France

- 6.4.2.4 Italy

- 6.4.2.5 Spain

- 6.4.3 Asia

- 6.4.3.1 China

- 6.4.3.2 Japan

- 6.4.3.3 India

- 6.4.3.4 Australia and New Zealand

- 6.4.4 Latin America

- 6.4.4.1 Brazil

- 6.4.4.2 Argentina

- 6.4.4.3 Mexico

- 6.4.5 Middle East and Africa

- 6.4.5.1 Saudi Arabia

- 6.4.5.2 South Africa

- 6.4.5.3 Egypt

- 6.4.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles*

- 7.1.1 Berry Global Group Inc.

- 7.1.2 Amcor Group GmbH

- 7.1.3 Novolex Holdings LLC

- 7.1.4 Tekni-Plex Inc.

- 7.1.5 Klockner Pentaplast

- 7.1.6 Coveris Management GmbH

- 7.1.7 Hoffmann Neopac AG

- 7.1.8 Silgan Dispensing Systems (Silgan Holdings Inc.)

- 7.1.9 Greiner Packaging International GmbH

- 7.1.10 Avery Dennison Corporation

- 7.1.11 Nussbaum Matzingen AG

- 7.1.12 Gallo Glass Company

- 7.1.13 Great Little Box Company Ltd