|

市場調査レポート

商品コード

1521761

セキュリティサービス:市場シェア分析、産業動向・統計、成長予測(2024年~2029年)Security Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| セキュリティサービス:市場シェア分析、産業動向・統計、成長予測(2024年~2029年) |

|

出版日: 2024年07月15日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

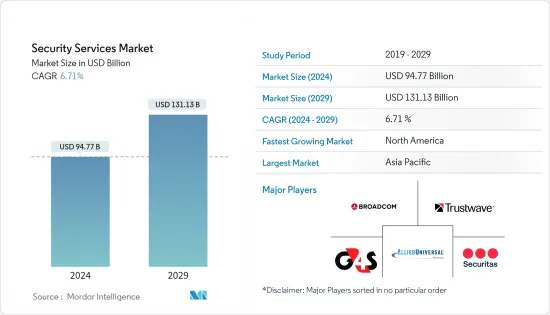

セキュリティサービスの市場規模は2024年に947億7,000万米ドルと推定され、2029年には1,311億3,000万米ドルに達すると予測され、予測期間中(2024-2029年)のCAGRは6.71%で成長すると予測されます。

主なハイライト

- 物理的領域とデジタル領域の関係はますます複雑化しており、特に新興経済諸国ではより高度なセキュリティシステムの開発が必要となっています。これらのシステムがスマートデバイスやIoTを通じてビッグデータや人工知能(AI)などのテクノロジーと統合されるにつれて、セキュリティサービスに対するニーズは急速に高まっています。バーチャルな職場環境の出現や、施設利用に対する要求の日進月歩は、新たなセキュリティサービスやソリューションにつながっています。さらに、eコマースの成長により、物流センターや同様の構造物におけるテクノロジー対応のセキュリティソリューションに対する需要がさらに高まっています。

- ますます多くの人々が都市に移り住むようになり、都市化と工業化の速度が加速しています。世界の都市人口は毎週平均150万人ずつ増加しており、この人口密度の高さは犯罪行為への懸念を高める可能性があります。セキュリティサービス市場は、技術的な監視機器の利用が増えるにつれて、大半の新興国で急拡大すると予想されます。工業化の進行と世界の工業生産の成長により、生産施設、オフィス、その他の職場環境への投資が必要となり、それぞれにセキュリティ要件が求められます。

- 世界人口の可処分所得が増加するにつれて、セキュリティサービスへの要求も高まると思われます。例えば、公共交通機関や公共物流施設などのインフラ投資では、これらの財産の保護が必要となるため、セキュリティ需要が増加します。経済成長と世界の新築投資の継続は、いずれもセキュリティサービス市場の開拓に寄与しています。例えば、2023年7月には、全国100都市に数十億米ドルを投資することで、急速に拡大するインドの都市人口に対応しようとする「スマート・シティ・ミッション」が予定されています。

- サイバー脅威の性質は常に変化しているため、セキュリティサービスも常に適応していく必要があります。新たな攻撃ベクトルが出現する中、セキュリティサービスが不十分であれば、組織はリスクにさらされ、市場開拓の妨げになりかねないです。例えば、2023年にデータ漏洩件数が最も多かったのは、ヘルスケア、金融サービス、製造業の3業界でした。

- COVID-19パンデミックは世界のセキュリティサービス市場に悪影響を及ぼしました。例えば、コンサート会場、会議、スポーツ大会などの重要な公共イベントが閉鎖されたため、セキュリティサービスの必要性が低下しました。しかし、COVID-19後は、社会の平常への復帰を促進するために、ロックダウン中の小売業やヘルスケアなどの必要不可欠な機能に対するセキュリティサービスや、接触者追跡や群衆監視などのセキュリティやテクノロジーを活用したセキュリティサービスに対する需要が増加しています。

セキュリティサービス市場の動向

クラウド展開が大きな市場シェアを占める

- クラウドで展開されるマネージド・セキュリティサービスは、適応性と拡張性に優れています。さらに、サービス・プロバイダーは、クラウド内のあらゆる問題にアクセスし、追跡し、リモートで解決することもできます。継続的な監視により、あらゆる問題を迅速かつ効果的に解決できます。機械学習(ML)、人工知能(AI)、ビッグデータ分析、脅威インテリジェンス、高度な自動化プラットフォームの導入が進んでいることも、クラウド管理型セキュリティサービスへの移行を後押ししています。市場参入企業の中には、業界の変化するニーズに対応するため、革新的かつ協調的な取り組みを通じて包括的なサービスを導入している企業もあります。

- パンデミックによるリモートワークの急速な拡大により、クラウドベースのコラボレーション・ツールやアクセス・ソリューションへの依存度が高まっています。こうした環境の安全性を保証するには、安全なアクセスや包括的な保護など、専門的なセキュリティサービスが必要です。その結果、企業はクラウドセキュリティに関連するコストと複雑さを削減するために、自動化されたセキュリティ対策と手動プロセスを組み合わせたハイブリッドアーキテクチャを選択することが増えています。

- デジタルトランスフォーメーションに取り組む企業が、オンプレミスのITインフラを近代化し、業務の一部をクラウドに移行するという、困難ではあるが必要なプロセスに着手する際、ITの意思決定者は通常、規制遵守、セキュリティ、リスク削減の課題に直面します。有能なIT人材が不足し、最新のツール、テクノロジー、プラクティスに対応できないことが、こうした企業の悩みを悪化させています。ネットワークとデータのセキュリティリスクが高まっている今、MSSPは、クラウド構成の管理、リスクの低減、法規制へのコンプライアンスの確保において、圧倒されている企業を支援することができます。

- 複雑で大規模なアーキテクチャのためにカスタム・セキュリティクラウドの展開が必要な組織や、異種システムによる特定の実装要件がある組織は、このようなサービスから大きな恩恵を受けることができます。動的なリソース割り当てに依存している組織は、通常、動的な環境を効率的に監視するために、自動化の改善を必要としています。このような複雑な自動化要件は、AT&T、Verizon、IBM、SecureWorksなどのプロバイダーが提供するサービスを通じて満たすことができます。

- 2023年10月、CyberArkは、同社のリスクベースのインテリジェントな特権コントロールに基づき、クラウドサービスや最新のインフラストラクチャへのアクセスをすべてのユーザーに対して保護するための新機能を発表しました。この新しいセキュリティ制御により、クラウド環境のあらゆるレイヤーへの安全なアクセスが可能になると同時に、開発者やその他のユーザーがクラウドサービスにアクセスする方法に混乱や変更をもたらすことはないです。

アジア太平洋地域が著しい成長を遂げる

- アジア太平洋地域ではここ数年、サイバー脅威や攻撃が増加しています。人々のインターネット利用が増加し、ビジネスのデジタル化が進み、地政学的な緊張が存在しています。こうした要因により、サイバー攻撃や侵害から身を守るための信頼性の高いサイバーセキュリティサービスの必要性が高まっています。

- MeitYが提供したデータによると、インドでは2023年に150万件以上のサイバー攻撃が報告されており、これは以前よりかなり増加しています。インドは、この年にサイバーセキュリティインシデントの件数が最も多かった5カ国のうちの1つでした。さらに、インドは現在、インターネット・ユーザー数で世界第3位にランクされています。

- ITランサムウェア攻撃、分散型サービス拒否(DDoS)攻撃、データ抜き取り、メディアにおける大規模サイバー攻撃の認知度向上など、サイバーセキュリティに対する脅威が増大しているため、この地域の組織はますますマネージド・セキュリティサービスを利用するようになっています。伝統的な業界では、デジタルトランスフォーメーションの導入とIT技術の向上が進み、インターネットセンターサービスへの需要が高まっており、市場の成長にさらに貢献しています。

- 人工知能、5G、モノのインターネット、仮想現実技術の急速な登場と、これらの技術の商業化により、データ処理と情報交換の必要性が高まっています。こうした要因により、当地域ではデータセンター建設が加速し、業界の急拡大につながる可能性があります。インドでは、組織情報のセキュリティ、機密性、可用性に対する脅威が増加傾向にあるため、顧客の全体的なセキュリティのために、ビジネスリスクアプローチに基づく情報セキュリティの標準モデルを導入、実装、運用、監視、見直し、保守、改善する必要性が強調されています。

- アジア太平洋地域では、デジタルトランスフォーメーションを最優先事項として採用する企業が増加しています。取り組みを促進するために正式な戦略を採用する企業が増えるにつれ、デジタルトランスフォーメーションに対する市場の需要は大幅に増加しています。中国、インド、日本、韓国などいくつかの国では、ヘルスケア、金融サービス、行政、製造などさまざまな分野で急速なデジタル変革が進んでいます。この変革には、クラウドコンピューティングやモノのインターネット(IoT)、デジタルプラットフォームの活用が必要であり、デジタル資産を保護するための高度なセキュリティサービスの提供が求められています。

セキュリティサービス業界の概要

セキュリティサービス市場は競争が激しいです。大小さまざまなプレーヤーが存在するため、市場は断片化されています。大手企業はいずれも大きな市場シェアを占めており、消費者基盤の拡大に注力しています。同市場の大手企業には、Broadcom、Trustwave Holdings Inc.、G4S Limited、Securitas Inc.、Allied Universal、Unity Resource Group、Constellis、DSS Securitech Pvt.Ltd.、Fortra LLCなどがあります。各社は予測期間中に競争力を獲得するため、複数のパートナーシップ、提携、買収を結び、新製品の導入に投資することで市場シェアを拡大しています。

2023年4月セキュリティと施設サービスのプロバイダーであるアライド・ユニバーサルは、アライド・ユニバーサルの子会社であるMSA Securityと提携し、Elite Tactical Security Solutionsを買収しました。エリート・タクティカルの買収により、アライド・ユニバーサルはセキュリティとエグゼクティブ保護サービス、爆発物・銃器探知犬チームの提供が可能になります。この買収の結果、アライド・ユニバーサルのソリューション・ポートフォリオは、ラスベガスにおける警備員とエグゼクティブ保護サービスの管理を担当することになります。Elite Tacticalのイヌ・サービスは、MSA Securityのプログラムに統合されます。

2023年3月-FortraのTerranova SecurityはElevate Securityと提携し、マーケットプレースに最高のセキュリティ意識と脅威監視をもたらします。この要素は、機密情報の保護、情報セキュリティの強化、サイバー攻撃やデータ侵害の人的リスクの軽減を目指す組織にとって不可欠です。フィッシング・インシデントの80%は4%のユーザーが、マルウェア・インシデントの92%は3%のユーザーが占めています。Elevate Securityは、組織の最も脆弱なユーザーをプロアクティブに識別して対応し、セキュリティインシデントを引き起こす前にユーザー・リスクを軽減するための可視性と分析機能をセキュリティチームに提供します。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- COVID-19の影響とその他のマクロ経済要因が市場に与える影響

第5章 市場力学

- 市場促進要因

- デジタル破壊とコンプライアンス要求の高まり

- マルチクラウドまたはハイブリッドクラウド戦略の採用の増加

- 各国政府のサイバーセキュリティへの注力

- 市場の課題

- セキュリティサービスに対する認識不足

- セキュリティサービスに対する組織の限られた予算制約

- 複雑性と統合の課題

第6章 市場セグメンテーション

- サービスタイプ別

- マネージド・セキュリティサービス

- プロフェッショナル・セキュリティサービス

- コンサルティング・サービス

- 脅威インテリジェンス・セキュリティサービス

- 導入形態別

- オンプレミス

- クラウド

- エンドユーザー業界別

- ITおよびインフラ

- 政府機関

- 産業

- ヘルスケア

- 運輸・物流

- 銀行

- その他エンドユーザー産業

- 地域*別

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- アジア

- インド

- 中国

- 日本

- オーストラリア・ニュージーランド

- ラテンアメリカ

- 中東・アフリカ

- 北米

第7章 競合情勢

- 企業プロファイル

- Broadcom

- Trustwave Holdings Inc

- G4S Limited

- Allied Universal

- Securitas Inc

- Unity Resource Group

- Constellis

- DSS Securitech Pvt. Ltd

- Fortra LLC

- IBM Corporation

- VS4 Security Services

- Fujitsu

- Verizon

- Wipro

第8章 投資分析

第9章 市場の将来

The Security Services Market size is estimated at USD 94.77 billion in 2024, and is expected to reach USD 131.13 billion by 2029, growing at a CAGR of 6.71% during the forecast period (2024-2029).

Key Highlights

- The relationship between the physical and digital realms is becoming increasingly complex, necessitating the development of more sophisticated security systems, particularly in more developed economies. The need for security services is rapidly growing as these systems integrate with technologies such as big data and artificial intelligence (AI) through smart devices and the IoT. The emergence of virtual working environments and the ever-evolving demands for facility utilization are leading to new security services and solutions. Additionally, the growth of e-commerce has further increased the demand for technology-enabled security solutions in distribution centers and similar structures.

- The rate of urbanization and industrialization is accelerating as more and more people relocate to cities. The world's urban population is increasing by an average of 1.5 million individuals each week, and this high population density could raise concerns about criminal activity. It is anticipated that the security services market will experience a rapid expansion in the majority of developed countries as the utilization of technological monitoring equipment increases. The ongoing industrialization and growth of global industrial production necessitates the investment of production facilities, offices, and other work environments, each with its security requirements.

- As the global population increases its disposable income, the requirement for security services is likely to grow. For instance, infrastructure investments in public transport and public logistics facilities require the protection of these properties, thus necessitating an increase in the demand for security. Economic growth and ongoing global investment in new construction are both contributing to the development of the security services market. For instance, in July 2023, the Smart Cities Mission seeks to address India's rapidly expanding urban population by investing billions in 100 cities nationwide.

- The ever-changing nature of cyber threats necessitates that security services must be constantly adapted. As new attack vectors emerge, organizations can be put at risk if security services are inadequate, thus impeding market development. For instance, in 2023, the three industries that experienced the highest number of data breaches were the healthcare, financial services, and manufacturing sectors.

- The COVID-19 pandemic had a detrimental effect on the global security services market. For instance, the closure of significant public events, such as concert venues, conferences, and sports competitions, reduced the need for security services. However, post-COVID-19, there is an increase in the demand for security services for essential functions, such as retail and healthcare during lockdown, as well as for security and technology-enabled security services, such as contact tracing and crowd surveillance, to facilitate the return of societies to normalcy.

Security Services Market Trends

Cloud Deployment to Hold Significant Market Share

- Managed security services deployed in the cloud are highly adaptable and scalable. Additionally, the service provider can access, track, and even remotely resolve any problems within the cloud. Continuous monitoring ensures the prompt and effective resolution of any issues. The rising adoption of machine learning (ML), artificial intelligence (AI), big data analytics, threat intelligence, and advanced automation platforms further supports the transition to cloud-managed security services. Several market participants are introducing comprehensive services through innovative and collaborative initiatives to meet the changing needs of the industry.

- The rapid expansion of remote work due to the pandemic has necessitated a greater reliance on cloud-based collaborative tools and access solutions. Specialized security services are necessary to guarantee the safety of these environments, including secure access and comprehensive protection. As a result, enterprises will increasingly opt for hybrid architectures that combine automated security measures with manual processes to reduce the costs and intricacies associated with cloud security.

- IT decision-makers typically face regulatory compliance, security, and risk reduction challenges as companies amid digital transformation embark on the difficult yet necessary process of modernizing their on-premise IT infrastructure and transitioning some of their operations into the cloud. The lack of qualified IT personnel and the inability to remain up-to-date with the latest tools, technologies, and practices exacerbate these corporate worries. At a time when network and data security risks are on the rise, MSSPs can assist overwhelmed enterprises in managing cloud configuration, reducing risk, and ensuring regulatory compliance.

- Organizations that require a custom security cloud deployment due to a complex or expansive architecture or have specific implementation requirements with disparate systems can benefit significantly from such services. Organizations that rely on dynamic resource allocation typically require improved automation to monitor their dynamic environments efficiently. These complex automation requirements can be met through the services provided by providers such as AT&T, Verizon, IBM, and SecureWorks.

- In October 2023, CyberArk announced new capabilities for securing access to cloud services and modern infrastructure for all users based on the company's risk-based intelligent privilege controls. The new security controls enable secure access to every layer of cloud environments while causing no disruption or change to how developers and other users access cloud services.

Asia-Pacific to Witness Significant Growth

- Cyber threats and attacks have increased in Asia-Pacific over the last few years. People increasingly use the internet, businesses are digitalizing, and geopolitical tension exists. These factors have heightened the need for reliable cybersecurity services to safeguard against cyberattacks and breaches.

- In India, according to data provided by MeitY, more than 1.5 million cyberattacks were reported in 2023, which was a considerable rise from previous years. India was one of the five countries with the highest number of cybersecurity incidents in the year. Additionally, India is currently ranked third worldwide in terms of internet user numbers.

- Organizations in the region are increasingly turning to managed security services due to the growing threats to cybersecurity, such as IT ransomware attacks, distributed denial-of-service (DDoS) attacks, data extraction, and the increased visibility of major cyberattacks in the media. Traditional industries are increasingly embracing digital transformation and improving their IT technologies, increasing the demand for Internet center services, further contributing to the market's growth.

- The rapid emergence of artificial intelligence, 5G, the Internet of Things, and virtual reality technologies, as well as the commercialization of these technologies, has increased the need for data processing and the exchange of information. These factors may lead to accelerating data center construction in the region, potentially resulting in a rapid expansion of the industry. The threats to the security, confidentiality, and availability of organization information are on the rise in India, thus emphasizing the need for a standardized model of information security based on the business risk approach to be implemented, implemented, operated, monitored, reviewed, maintained, and improved for the overall security of customers.

- Asia-Pacific has seen an increase in the adoption of digital transformation as a top priority. As more businesses adopt formal strategies to facilitate their efforts, the market demand for digital transformation has increased significantly. Several countries, such as China, India, Japan, and South Korea, are experiencing rapid digital transformation in various sectors, including healthcare, financial services, administration, and manufacturing. This transformation necessitates the utilization of cloud computing and the Internet of Things (IoT), as well as digital platforms, which requires the provision of sophisticated security services to protect digital assets.

Security Services Industry Overview

The security services market is very competitive. The market is fragmented due to the presence of various small and large players. All the major players account for a significant market share and focus on expanding the consumer base. Some of the significant players in the market are Broadcom, Trustwave Holdings Inc., G4S Limited, Securitas Inc., Allied Universal, Unity Resource Group, Constellis, DSS Securitech Pvt. Ltd, and Fortra LLC. Companies are increasing their market share by forming multiple partnerships, collaborations, and acquisitions and investing in introducing new products to earn a competitive edge during the forecast period.

April 2023: Allied Universal, a security and facility services provider, partnered with MSA Security, a subsidiary of Allied Universal, to acquire Elite Tactical Security Solutions, a strategic extension of their services to the Las Vegas area. The acquisition of Elite Tactical will enable Allied Universal to provide security and executive protection services and explosives and firearms detection canine teams. As a result of this acquisition, Allied Universal's portfolio of solutions will be responsible for managing security guard and executive protection services in Las Vegas. Elite Tactical's canine services will be integrated into MSA Security's program.

March 2023 - Fortra's Terranova Security partnered with Elevate Security to bring the best security awareness and threat monitoring to the marketplace. This factor is essential for organizations looking to protect sensitive information, enhance information security, and mitigate the human risk of cyber-attacks and data breaches. 4% of users account for 80% of all phishing incidents and 3% for 92% of all malware incidents. Elevate security proactively identifies and responds to an organization's most vulnerable users and provides security teams with visibility and analytics to mitigate user risk before enabling a security incident.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Impact of COVID-19 Aftereffects and Other Macroeconomic Factors on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rising Digital Disruption and Increased Compliance Demands

- 5.1.2 Increasing Adoption of Multi-Cloud or Hybrid Cloud Strategies

- 5.1.3 Governments Focus on CyberSecurity

- 5.2 Market Challenges

- 5.2.1 Lack of Awareness of Security Services

- 5.2.2 Limited Budget Constraints by Organizations for Security Services

- 5.2.3 Complexity and Integration Challenges

6 MARKET SEGMENTATION

- 6.1 By Service Type

- 6.1.1 Managed Security Services

- 6.1.2 Professional Security Services

- 6.1.3 Consulting Services

- 6.1.4 Threat Intelligence Security Services

- 6.2 By Mode of Deployment

- 6.2.1 On-Premise

- 6.2.2 Cloud

- 6.3 By End-user Industry

- 6.3.1 IT and Infrastructure

- 6.3.2 Government

- 6.3.3 Industrial

- 6.3.4 Healthcare

- 6.3.5 Transportation and Logistics

- 6.3.6 Banking

- 6.3.7 Other End-user Industries

- 6.4 By Geography***

- 6.4.1 North America

- 6.4.1.1 United States

- 6.4.1.2 Canada

- 6.4.2 Europe

- 6.4.2.1 Germany

- 6.4.2.2 United Kingdom

- 6.4.2.3 France

- 6.4.3 Asia

- 6.4.3.1 India

- 6.4.3.2 China

- 6.4.3.3 Japan

- 6.4.3.4 Australia and New Zealand

- 6.4.4 Latin America

- 6.4.5 Middle East and Africa

- 6.4.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles*

- 7.1.1 Broadcom

- 7.1.2 Trustwave Holdings Inc

- 7.1.3 G4S Limited

- 7.1.4 Allied Universal

- 7.1.5 Securitas Inc

- 7.1.6 Unity Resource Group

- 7.1.7 Constellis

- 7.1.8 DSS Securitech Pvt. Ltd

- 7.1.9 Fortra LLC

- 7.1.10 IBM Corporation

- 7.1.11 VS4 Security Services

- 7.1.12 Fujitsu

- 7.1.13 Verizon

- 7.1.14 Wipro