|

市場調査レポート

商品コード

1521715

低分子イノベーター受託開発・製造機関- 市場シェア分析、業界動向・統計、成長予測(2024年~2029年)Small Molecules Innovator Contract Development And Manufacturing Organization - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 低分子イノベーター受託開発・製造機関- 市場シェア分析、業界動向・統計、成長予測(2024年~2029年) |

|

出版日: 2024年07月15日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

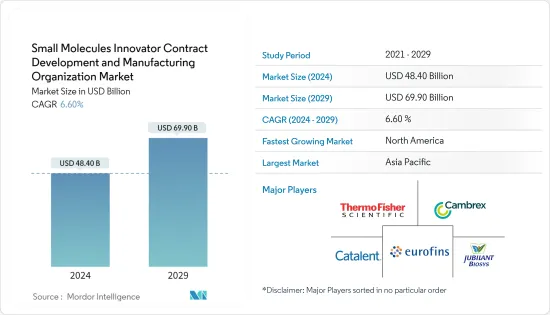

低分子イノベーター受託開発・製造機関市場規模は2024年に484億米ドルと推定・予測され、2029年には699億米ドルに達し、予測期間中(2024~2029年)のCAGRは6.60%で成長すると予測されます。

市場を牽引するのは、低分子医薬品に対する需要の増加、低分子医薬品のパイプラインの充実、慢性疾患の負担増、医薬品研究開発投資の増加です。低分子医薬品のパイプラインが充実しているということは、製薬企業やバイオテクノロジー企業がさまざまな開発段階にある化合物をより多く保有していることを意味します。そのため、製剤開発、プロセスの最適化、製造など、CDMOが提供する専門的なサービスへのニーズが高まっています。例えば、2023年2月に発表されたバイオ産業分析レポートによると、2022年時点で47の低分子新薬(NCE)が臨床パイプラインにあります。従来の全身用低分子抗生物質が97%を占め、局所用低分子が低分子パイプラインNCEsの3%を占めています。

同様に、Clinicaltrials.govによると、2024年3月現在、第Ⅱ相試験中の低分子医薬品は64品目、第Ⅲ相試験中の低分子医薬品は3品目です。従って、パイプラインの成長は様々な治療領域にまたがり、複数の病状に対応することが多いです。このような医薬品開発の多様化は、様々なセグメントに精通したCDMOへの需要を高め、市場をさらに活性化させる。

製薬企業が低分子医薬品の研究開発(R&D)に多額の投資を行っていることから、開発・製造受託機関(CDMO)が提供するサービスへの需要が高まっています。これらの組織は、新薬候補を発見段階から臨床試験まで持っていくために、専門的な専門知識とインフラを必要とします。例えば、Cambrexは2022年9月、低分子医薬品原薬(API)製造のためのノースカロライナ州ハイポイント施設への3,000万米ドルの投資の初期段階を完了しました。さらに、低分子医薬品開発のための戦略的提携は、予測期間中の市場成長を促進すると予想されます。例えば、2022年1月、SanofiとExscientiaは、実際の患者サンプルを活用したExscientiaのAI主導型プラットフォームを活用し、腫瘍学と免疫学にまたがる最大15の新規低分子化合物候補を開発する目的で、戦略的研究提携とライセンス契約を締結しました。

したがって、低分子医薬品の強力なパイプライン、低分子開発への投資の増加、市場参入企業による主要戦略の採用が、同セグメントの成長を促進すると予想されます。しかし、厳しい政府規制やアウトソーシングに伴うコンプライアンスの問題が、予測期間中の市場成長を抑制すると予想されます。

低分子イノベーター受託開発・製造機関の市場動向

神経セグメントは2024~2029年にかけて大きなシェアを占める見込み

低分子イノベーター開発・製造受託機関(CDMO)市場における神経セグメントは、神経疾患に対する認識と理解の高まりにより、アルツハイマー病、パーキンソン病、てんかん、その他さまざまな神経変性疾患などの疾患を対象とした医薬品の開発に重点が置かれるようになり、顕著な成長を遂げています。

例えば、Biogenは2023年7月、低分子のパイプライン医薬品であるズラノロン(GABAA PAM)-大うつ病性障害(MDD)の第III相臨床試験、BIIB131(プラスミノーゲン活性化因子)-急性虚血性脳卒中の第II相臨床試験を発表しました。同様に、UCB SA社も、神経疾患に対する4つの革新的な低分子医薬品のパイプラインを有していると報告しています。その中には、フェンフルラミン(5-HTアゴニスト)、ドキセシチンとドキシリブチミン(MT1621、ヌクレオシド療法)、ミンザソルミン(a-synミスフォールディング阻害剤)、STACCATOアルプラゾラム(ベンゾジアゼピン)が含まれ、様々な開発段階にあります。このような低分子新薬の膨大なパイプラインは、プロセス開発、分析試験、製造のためのCDMOに大きな需要を生み出すと予想され、2024~2029年の間にセグメントの成長に寄与すると期待されています。

パーキンソン病、筋萎縮性側索硬化症(ALS)、ハンチントン舞踏病、アルツハイマー病などの中枢神経系疾患の増加は、これらの疾患の医薬品開発には様々な臨床試験支援や規制当局の勧告などが必要となるため、CROサービスの需要を促進しています。例えば、Alzheimer's Disease Facts and Figures Annual Report 2023が発表したデータによると、600万人以上のアメリカ人がアルツハイマー病を患っており、この数字は30年以内にほぼ1,300万人に増加すると予測されています。

さらに、上記の供給源によれば、2023年、米国はアルツハイマー病やその他の認知症の治療と管理に3,450億米ドルを費やしました。2050年までには、これらの費用は1兆米ドル近くに増加する可能性があります。このように、アルツハイマー病の高い負担は、革新的で効果的な治療法に対する需要を生み出し、研究市場の成長を牽引しています。

さらに、世界保健機関(WHO)が2023年3月に更新したデータによると、世界全体で約5,500万人が認知症を患っており、毎年1,000万人近くが新たに認知症を発症しています。さらに、2023年9月に更新されたAtlas of Multiple Sclerosisのデータによると、2023年には世界で290万人が多発性硬化症に罹患しており、Parkinson's Foundationが発表したデータによると、1,000万人がパーキンソン病に罹患しています。こうした中枢神経系疾患の負担増は、2024~2029年にかけて中枢神経系治療の需要と重要な研究活動を促進すると予想されます。

製薬企業やバイオテクノロジー企業は、サービス拡大に注力する姿勢を強めています。例えば、2023年9月、Cellectriconは、神経精神医療、てんかん、神経変性などの治療領域における創薬を加速するための新しいNeuroplasticity Servicesモジュールを立ち上げ、神経科学受託研究ポートフォリオを拡大しました。

したがって、研究開発活動の増加、強力なパイプラインの存在、市場参入企業による戦略的活動が、2024~2029年にかけての市場成長に寄与すると予想されます。

北米が2024~2029年にかけて大きな市場シェアを占める展望

北米、特に米国は、確立された強固な製薬産業の本拠地です。この地域には、創薬や医薬品開発に積極的に取り組む革新的な製薬企業やバイオテクノロジー企業が集中しています。研究開発への投資額の高さ、主要市場参入企業の強固な足場、米国国立衛生研究所(National Institute of Health)による新規治療開発のための助成金の増加も、同国の市場成長に寄与しています。

製薬・バイオテクノロジー業界による低分子医薬品の開発への投資が増加していることも、市場成長に寄与すると予想されます。例えば、2023年5月、PharmEnableは、臨床ニーズの高い疾患領域に対する次世代の低分子医薬品を開発するため、750万米ドルのプレシリーズA投資ラウンドを終了したと発表しました。さらに、市場参入企業はサービスの拡大に取り組んでおり、コラボレーションが市場の成長を促進する可能性が高いです。例えば、CDMOのPhlowは2023年4月、シリーズB増資により3,600万米ドルを調達したと発表しました。Phlowは、この資金を「cdmoX」と呼ばれるCDMOプログラムの拡大を含む商業的提供の拡大に充てると述べています。さらに、2022年7月には、製薬・バイオ医薬品業界で低分子・高分子バイオ分析サービスを提供する Alliance Pharmaが、LGCからDrug Development Solutions(DDS)の買収を完了しました。Ampersand Capital PartnersとKKR &Co.Ltd.からの買収を完了しました。

したがって、市場参入企業による投資と戦略的活動の増加は、2024~2029年の間にこの地域の市場を押し上げると予想されます。

低分子イノベーター受託開発・製造機関産業概要

低分子医薬品の開発・製造受託市場は細分化されています。同市場における地位を強化するため、各社は業界のプレゼンスを拡大する注目すべき戦略や施策を実施しています。主要市場参入企業としては、Eurofins Scientific、Cambrex Corporation、Catalent、Thermo Fisher Scientific、Jubilant Pharmova Limitedなどが挙げられます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブ概要

第4章 市場力学

- 市場概要

- 市場促進要因

- 低分子医薬品の需要増加とパイプラインの成長

- 慢性疾患の負担増

- 医薬品研究開発投資の増加

- 市場抑制要因

- 厳しい政府規制

- アウトソーシングにおけるコンプライアンスの問題

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手・消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション(市場規模-米ドル)

- 製品別

- 低分子原薬

- 低分子医薬品

- 経口固形製剤

- 半固形製剤

- 液剤

- その他

- ステージ別

- 前臨床

- 臨床試験

- 第I相

- フェーズII

- 第III相

- フェーズIV

- 商業

- エンドユーザー別

- 製薬・バイオテクノロジー

- 受託研究機関

- 治療領域別

- 心血管疾患

- 腫瘍

- 呼吸器疾患

- 神経学

- 代謝疾患

- 感染症

- その他

- 地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- 英国

- ドイツ

- フランス

- スペイン

- イタリア

- その他の欧州

- アジア太平洋

- インド

- 日本

- 中国

- オーストラリア

- 韓国

- その他のアジア太平洋

- 中東・アフリカ

- GCC諸国

- 南アフリカ

- その他の中東・アフリカ

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 北米

第6章 競合情勢

- 企業プロファイル

- Eurofins Scientific

- Cambrex Corporation

- Catalent

- Thermo Fisher Scientific Inc.

- Jubilant Pharmova Limited

- Lonza Group Ltd

- Wuxi AppTec

- Syngene International Limited

- Almac Group

- Piramal Pharma Solutions

- Recipharm AB

- Labcorp Drug Development

第7章 市場機会と今後の動向

The Small Molecules Innovator Contract Development And Manufacturing Organization Market size is estimated at USD 48.40 billion in 2024, and is expected to reach USD 69.90 billion by 2029, growing at a CAGR of 6.60% during the forecast period (2024-2029).

The market is driven by increasing demand for small molecule drugs, the growing pipeline of small molecule drugs, the increasing burden of chronic diseases, and rising pharmaceutical R&D investments. A robust pipeline of small molecule drugs means that pharmaceutical and biotech companies have more compounds in various stages of development. This creates a greater need for specialized services CDMOs provide, including formulation development, process optimization, and manufacturing. For instance, according to the Bio Industry Analysis Report published in February 2023, 47 small molecule new chemical entities (NCEs) were in the clinical pipeline as of 2022. Traditional systemic small-molecule antibiotics account for 97%, and topical small molecules account for 3% of the small-molecule pipeline NCEs.

Similarly, according to Clinicaltrials.gov, as of March 2024, there were 64 small molecules of drugs in phase II trials and 3 in the phase III trials. Hence, the growing pipeline often spans various therapeutic areas, addressing multiple medical conditions. This diversification in drug development increases the demand for CDMOs with expertise in different fields, further stimulating the market.

The substantial investment by pharmaceutical companies in research and development (R&D) of small molecule drugs has led to an increased demand for the services provided by contract development and manufacturing organizations (CDMOs). These organizations require specialized expertise and infrastructure to bring their drug candidates from the discovery phase through clinical trials. For instance, in September 2022, Cambrex completed the initial stage of its USD 30 million investment in its High Point, North Carolina facility for manufacturing small molecule active pharmaceutical ingredients (APIs). Furthermore, strategic collaboration for small molecule drug development is expected to drive market growth over the projected period. For instance, in January 2022, Sanofi and Exscientia entered a strategic research alliance and licensing pact for the purpose of developing up to 15 novel small molecule candidates across oncology and immunology, leveraging Exscientia's AI-driven platform utilizing actual patient samples.

Hence, the strong pipeline for small molecule drugs, increasing investment in developing small molecules, and key adoption of key strategies by market participants are expected to drive segment growth. However, stringent government regulations and compliance issues with outsourcing are anticipated to restrain the market growth over the projected period.

Small Molecules Innovator Contract Development And Manufacturing Organization Market Trends

The Neurology Segment is Expected to Hold Significant Share Between 2024 and 2029

The neurology segment in the small molecule innovators contract development and manufacturing organization (CDMO) market has been experiencing notable growth owing to growing awareness and understanding of neurological disorders, leading to an increased emphasis on the development of drugs targeting conditions like Alzheimer's, Parkinson's, epilepsy, and various other neurodegenerative diseases.

For instance, in July 2023, Biogen announced its small molecules pipeline drug Zuranolone (GABAA PAM) - Major depressive disorder (MDD) in phase III trials and BIIB131 (plasminogen activator) - Acute ischemic stroke in Phase II Trials. Similarly, UCB SA also reported that it has 4 small molecules of innovative drugs in the pipeline for neurology diseases, which include fenfluramine (5-HT agonist), doxecitine and doxribtimine (MT1621, nucleoside therapy), minzasolmin (a-syn-misfolding inhibitor), and STACCATO alprazolam (benzodiazepine) in various phase of development. Such a huge pipeline for small molecule innovator drugs is expected to create a huge demand for CDMO for process development, analytical testing, and manufacturing, which is expected to contribute to segment growth between 2024 and 2029.

An increase in CNS diseases, like Parkinson's disease, amyotrophic lateral sclerosis (ALS), Huntington chorea, and Alzheimer's disease, facilitates the demand for CRO services since the drug development of these diseases requires various clinical trial support, regulatory recommendations, etc. For instance, according to data published by Alzheimer's Disease Facts and Figures Annual Report 2023, over 6 million Americans suffered from Alzheimer's disease, a figure predicted to climb to almost 13 million within three decades.

Additionally, as per the above source, in 2023, the United States spent USD 345 billion in treating and managing Alzheimer's and other dementias. By 2050, these costs could rise to nearly USD 1 trillion. Thus, the high burden of the disease is creating demand for innovative and effective therapies, driving the growth of the studied market.

Furthermore, the data updated by the World Health Organization in March 2023 showed that globally, about 55 million people suffer from dementia; every year, there are nearly 10 million new cases of dementia filed. Additionally, Atlas of Multiple Sclerosis data updated in September 2023 showed that 2.9 million people live with multiple sclerosis in 2023 worldwide and 10 million with Parkinson's disease, as per the data published by the Parkinson's Foundation. These increasing burdens of CNS disorders are anticipated to drive the demand for central nervous system therapeutics and significant research activities between 2024 and 2029.

Pharmaceutical and biotechnology corporations are augmenting their focus on service expansion. For instance, in September 2023, Cellectricon expanded its neuroscience contract research portfolio with a new Neuroplasticity Services launched module set to accelerate drug discovery in therapeutic areas such as neuropsychiatry, epilepsy, and neurodegeneration.

Hence, increasing research and development activities, the presence of a strong pipeline, and strategic activities by the market players are expected to contribute to market growth between 2024 and 2029.

North America is Expected to Hold a Significant Market Share Between 2024 and 2029

North America, particularly the United States, is home to a well-established and robust pharmaceutical industry. This region has a high concentration of innovative pharmaceutical and biotech companies that are actively engaged in drug discovery and development. The high investment in R&D, the strong foothold of key market players, and rising grants from the National Institute of Health for developing novel therapeutics in the country also contribute to market growth.

The increasing investment by the pharmaceutical and biotechnology industry in the development of small-molecule drugs is expected to contribute to market growth. For instance, in May 2023, PharmEnable announced it had closed a Pre-Series A investment round of USD 7.5 million to develop the next generation of small molecule drugs against disease areas of high clinical need. Further, market players are engaging in service expansion, and collaboration is likely to propel the growth of the market. For instance, in April 2023, Phlow, a CDMO, announced that it had sealed USD 36 million through a Series B capital raise. Phlow stated that it would use the capital to expand its commercial offerings, which includes growing its CDMO program, called 'cdmoX. Additionally, in July 2022, Alliance Pharma, a company providing small and large-molecule bioanalytical services in the pharmaceutical and biopharmaceutical industry, closed the purchase of Drug Development Solutions (DDS) from LGC. Ampersand Capital Partners and KKR & Co. Inc.

Hence, increasing investment and strategic activities by the market players are expected to boost the market in the region between 2024 and 2029.

Small Molecules Innovator Contract Development And Manufacturing Organization Industry Overview

The small molecules innovator contract development and manufacturing organization market is fragmented in nature. In order to strengthen their position in the market, companies are implementing noteworthy strategies and measures to expand their industry presence. Some of the key market players are Eurofins Scientific, Cambrex Corporation, Catalent, Thermo Fisher Scientific Inc., and Jubilant Pharmova Limited.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definitions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Demand for Small Molecule Drugs and Growing Pipeline of Small Molecule Drugs

- 4.2.2 Growing Burden of Chronic Diseases

- 4.2.3 Increasing Pharmaceutical R&D Investments

- 4.3 Market Restraints

- 4.3.1 Stringent Government Regulations

- 4.3.2 Compliance Issues with Outsourcing

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD)

- 5.1 By Product

- 5.1.1 Small Molecule API

- 5.1.2 Small Molecule Drug Product

- 5.1.2.1 Oral solid dose

- 5.1.2.2 Semi-Solid Dose

- 5.1.2.3 Liquid Dose

- 5.1.2.4 Others

- 5.2 By Stage

- 5.2.1 Preclinical

- 5.2.2 Clinical

- 5.2.2.1 Phase I

- 5.2.2.2 Phase II

- 5.2.2.3 Phase III

- 5.2.2.4 Phase IV

- 5.2.3 Commercial

- 5.3 By End User

- 5.3.1 Pharmaceutical and Biotechnology

- 5.3.2 Contract Research Organization

- 5.4 By Therapeutic Area

- 5.4.1 Cardiovascular disease

- 5.4.2 Oncology

- 5.4.3 Respiratory disorders

- 5.4.4 Neurology

- 5.4.5 Metabolic disorders

- 5.4.6 Infectious disease

- 5.4.7 Others

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Spain

- 5.5.2.5 Italy

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 India

- 5.5.3.2 Japan

- 5.5.3.3 China

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of the Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Eurofins Scientific

- 6.1.2 Cambrex Corporation

- 6.1.3 Catalent

- 6.1.4 Thermo Fisher Scientific Inc.

- 6.1.5 Jubilant Pharmova Limited

- 6.1.6 Lonza Group Ltd

- 6.1.7 Wuxi AppTec

- 6.1.8 Syngene International Limited

- 6.1.9 Almac Group

- 6.1.10 Piramal Pharma Solutions

- 6.1.11 Recipharm AB

- 6.1.12 Labcorp Drug Development