|

市場調査レポート

商品コード

1521699

抗体受託開発・製造機関:市場シェア分析、業界動向・統計、成長動向予測(2024年~2029年)Antibody Contract Development And Manufacturing Organization - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 抗体受託開発・製造機関:市場シェア分析、業界動向・統計、成長動向予測(2024年~2029年) |

|

出版日: 2024年07月15日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

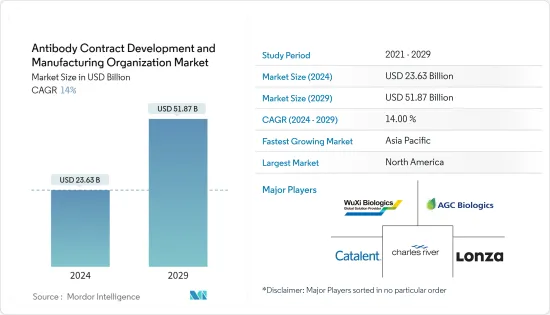

抗体受託開発・製造機関の市場規模は、2024年に236億3,000万米ドルと推定され、2029年には518億7,000万米ドルに達すると予測され、予測期間中(2024~2029年)のCAGRは14%で成長する見込みです。

この市場を牽引しているのは、臨床研究の割合の増加や抗体治療の開発資金の増加、がんの罹患率の上昇、抗体の製造コストの高さ、抗体の製造に伴う課題などです。

例えば、2022年10月、米国保健社会福祉省(HHS)内の機関であるBARDAは、特にHHS戦略的準備・対応局(ASPR)内の機関であるBARDAは、COVID-19におけるmAbの適用範囲を広げるために、新規モノクローナル抗体(mAb)候補と送達ソリューションの開発を進めるために、Virに約5,000万米ドルの新規資金を授与しました。同様に、2023年3月、Antiverse Ltdは300万米ドルの資金を調達し、自社での抗体開発を可能にしました。このように、抗体医薬品の開発・研究への投資が多いことから、予測期間中にCDMOサービスの需要が高まると予想されます。

さらに、抗体はがんの潜在的な治療オプションであり、がんの負担増は薬剤開発と製造活動を増加させると予想され、予測期間中にCDMOサービスの需要を促進すると考えられます。例えば、Canadian Cancer Statistics 2023報告書によると、カナダでは2022年の23万3,900件に対し、2023年には約23万9,200件の新たながん症例が報告されました。このように、がんの負担増は医薬品研究・製造サービスに対する需要を生み出し、同セグメントの成長に寄与すると期待されています。国立がん研究センターが2022年に更新したデータによると、2022年に日本で新たに診断されるがん患者数は、前立腺がんが9万6,400人、肝臓がんが4万400人、悪性リンパ腫が3万7,100人と推定されています。したがって、市場拡大は予測されるがん有病率の上昇によって推進されると予想されます。

共同研究、提携、M&Aなど、市場参入企業による戦略的活動は、予測期間中の市場成長を促進すると予想されます。例えば、2022年4月、旭化成メディカルは、生物製剤CDMOサービスプロバイダーであるBionova Scientific LLCを買収し、抗体CDMOセグメントに事業の領域を拡大しました。さらに2023年9月には、韓国のCDMOであるSamsung Biologicsが、世界のバイオファーマであるBristol Myers Squibbと抗体抗がん剤の大規模製造に関する契約を締結したと発表しました。

抗体開発のための資金調達の拡大、がん負担の増加、市場参入企業による戦略的活動など、上記の要因はすべて、予測期間中の市場の成長を後押しすると予想されます。しかし、アウトソーシング時の品質に関する懸念や、大手バイオ医薬品企業における最低限のアウトソーシング慣行が、予測期間中の市場拡大を妨げる可能性があります。

抗体受託開発・製造機関の市場動向

モノクローナル抗体セグメントは予測期間中に大きな市場シェアを占める展望

- いくつかの重要な要因により、モノクローナル抗体セグメントは抗体CDMO市場で最も急成長しているセグメントです。モノクローナル抗体(mAbs)は、がん、自己免疫疾患、感染症など、さまざまな疾患において大きな治療効果が期待されています。

- さらに、いくつかのモノクローナル抗体療法は臨床試験で顕著な成功を収め、様々な適応症で薬事承認を受けています。それゆえ、バイオ製薬会社はモノクローナル抗体の開発に投資しており、抗体CDMO市場の成長を後押しすると予想されています。例えば、2023年1月、英国政府はリバプールに英国第2の投資ゾーンを立ち上げ、米国の製薬メーカーTriRxはモノクローナル抗体の製造能力を強化するため、当初1,000万英ポンド(12.22米ドル)の投資を行った。

- 同様に、2023年9月、AborerIS Pharmaは、関節リウマチなどの自己免疫疾患の治療用モノクローナル抗体の開発を目的とした2,730万ユーロ(2,883万米ドル)のシリーズA資金調達を発表しました。従って、モノクローナル抗体への高い投資がCDMOサービスの需要を促進し、同セグメントの成長を後押しすると予想されます。

- バイオ製薬企業は、成長と収益性に計り知れない可能性があることから、mAbの開発と製造に高い関心を寄せています。例えば、2022年10月、CDMOのFujifilm Diosynth BiotechnologiesはArgenxと提携し、efgartigimodと呼ばれるモノクローナル抗体(mAb)フラグメントを製造しました。このmAbは重度の自己免疫疾患に苦しむ患者の治療に使用されます。モノクローナル抗体は、疾患の原因となる分子や細胞を特異的に標的とすることにより、慢性疾患の治療において顕著な成功を収めており、患者の予後改善につながります。同様に、2023年6月、CDMOのChime Biologicsは、LBL-007 mAbの開発と製造を加速し、迅速な臨床進出を図るため、Leads BiolabsとBeiGeneと三者戦略的提携を結んだと発表しました。

- したがって、モノクローナル抗体への投資の増加とCDMOのバイオ製薬企業との戦略的提携は、予測期間中の同セグメントの成長を後押しすると予想されます。

北米が予測期間中に大きな市場シェアを占める見込み

- 北米は、確立されたバイオ製薬企業が複数存在すること、抗体治療の研究開発活動が活発化していること、慢性疾患の有病率が上昇していること、抗体治療への投資が多いこと、市場参入企業による戦略的活動が活発であることなどから、世界の抗体CDMO市場で大きなシェアを占めると予想されます。

- 製薬会社は、特に生物製剤の研究開発に多額の投資を行っています。このような研究開発活動の活発化により、特に抗体開発に特化したCDMOサービスのニーズが高まっています。例えば、2023年9月、Star Therapeuticsは、ポートフォリオ企業と抗体療法の計画を強化するため、シリーズC資金調達ラウンドで9,000万米ドルを調達しました。シリーズCの資金調達は、現在第I相試験(NCT05776069)中のVGA039の臨床開発を支援します。このように、高額な投資のため、バイオテクノロジー企業は、専門知識を活用し、コストを削減し、スケジュールを早めるために、開発・製造活動を専門のCDMOに委託することが増えています。

- さらに、がんや関節リウマチのような自己免疫疾患の負担の増加は、研究開発活動を増加させ、CDMOサービスの需要を促進し、市場の成長を後押しすると予想されます。例えば、米国がん協会(ACS)が2024年1月に発表したデータによると、がん罹患率は2022年の193万件から2024年には200万件に増加し、2年間で6万件以上増加します。米国疾病予防管理センターが2023年6月に発表した統計によると、2040年までに米国の18歳以上の成人の25.9%、7,840万人が医師から関節炎と診断されると推定されています。この傾向はモノクローナル抗体セグメントの成長を後押ししており、CDMOはこうした特殊な治療法のカスタマイズや製造において重要な役割を果たしています。

- 複数の企業が買収や提携を通じて抗体開発製造受託機関セグメントに参入しています。例えば、2023年10月、Eurofins CDMO Alphora Inc.は、北米の受託開発・製造業界における多様化と成長を目指すビジョンの一環として、mAbsと治療用タンパク質に焦点を当てたバイオロジクス・イニシアチブを立ち上げました。

- 従って、モノクローナル抗体への投資の増加、慢性疾患の負担増、市場参入企業の戦略的活動が、予測期間中の北米市場を押し上げると予想されます。

抗体受託開発・製造機関業界概要

抗体受託開発・製造機関市場は、世界的・地域的に事業を展開する複数の企業が存在し、競争は中程度です。市場全体で事業を展開する主要企業は、合併、提携、買収などの組織内戦略的イニシアチブの採用に注力しています。世界の抗体医薬品開発・製造受託市場の主要企業は、Lonza、Catalent Inc.、Samsung Biologics、WuXi Biologics、AGC Biologics、Charles River Laboratoriesなどです。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブ概要

第4章 市場力学

- 市場概要

- 市場促進要因

- 臨床研究の増加と抗体研究への高額投資

- がん患者の増加

- 抗体製造コストの高騰と製造に伴う課題

- 市場抑制要因

- 外注時の品質問題

- 大手バイオファーマ企業によるアウトソーシングの制限

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手・消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション(市場規模-米ドル)

- 製品別

- モノクローナル抗体

- ポリクローナル抗体

- その他

- 供給源別

- 哺乳類

- 微生物

- 治療領域別

- 腫瘍学

- 神経学

- 循環器

- 感染症

- 免疫疾患

- その他

- エンドユーザー別

- バイオ製薬会社

- 研究機関

- その他

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- 英国

- ドイツ

- フランス

- スペイン

- イタリア

- その他の欧州

- アジア太平洋

- インド

- 日本

- 中国

- オーストラリア

- 韓国

- その他のアジア太平洋

- 中東・アフリカ

- GCC諸国

- 南アフリカ

- その他の中東・アフリカ

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 北米

第6章 競合情勢

- 企業プロファイル

- Lonza

- Catalent Inc.

- Samsung Biologics

- WuXi Biologics

- AGC Biologics

- AbbVie Inc.

- Boehringer Ingelheim International GmbH

- Charles River Laboratories

- FUJIFILM Holdings Corporation

- mAbxience

第7章 市場機会と今後の動向

The Antibody Contract Development And Manufacturing Organization Market size is estimated at USD 23.63 billion in 2024, and is expected to reach USD 51.87 billion by 2029, growing at a CAGR of 14% during the forecast period (2024-2029).

The market is driven by the increasing rate of clinical research and increasing funding for the development of antibody therapeutics, the rising incidence of cancer, the high cost of manufacturing antibodies, and challenges associated with the manufacturing of antibodies.

For instance, in October 2022, BARDA, an agency within the US Health and Human Services (HHS), specifically within the HHS Administration for Strategic Preparedness and Response (ASPR), awarded Vir approximately USD 50 million in new funding to advance the development of novel monoclonal antibody (mAb) candidates and delivery solutions to widen the applicability of mAbs in COVID-19. Similarly, in March 2023, Antiverse Ltd (Antiverse) raised USD 3 million in funding, enabling in-house antibody development. Thus, high investment in developing and researching antibody drugs is expected to fuel the demand for CDMO services during the forecast period.

Further, antibody is a potential treatment option for cancer, and the growing burden of cancer is expected to increase drug development and manufacturing activities, which are likely to propel demand for CDMO services during the forecast period. For instance, as per the Canadian Cancer Statistics 2023 report, about 239.2 thousand new cancer cases were reported in 2023 in Canada, compared to 233.9 thousand in 2022. Thus, the growing burden of cancer is expected to create the demand for drug research and manufacturing services, which is expected to contribute to the segment's growth. According to the data updated by the National Cancer Center of Japan in 2022, an estimated 96.4 thousand new prostate cancer cases, 40.4 thousand new liver cancer cases, and 37.1 thousand malignant lymphoma cases were diagnosed in Japan in 2022. Thus, market expansion is expected to be propelled by the projected rise in cancer prevalence.

Strategic activities by market players, such as collaborations, partnerships, and mergers and acquisitions, are expected to propel the market's growth during the forecast period. For instance, in April 2022, Asahi Kasei Medical expanded its business vertical into the antibody CDMO space by acquiring Bionova Scientific LLC, a biologics CDMO service provider. Additionally, in September 2023, Samsung Biologics, a Korean CDMO, announced an agreement for the large-scale manufacturing of an antibody cancer drug substance with global biopharma company Bristol Myers Squibb.

All these factors mentioned above, such as growing funding for antibody development, increasing cancer burden, and strategic activities by the market players, are expected to boost the market's growth during the forecast period. However, quality concerns during outsourcing and minimal outsourcing practices among large biopharma companies may hinder market expansion during the forecast period.

Antibody Contract Development And Manufacturing Organization Market Trends

Monoclonal Antibodies Segment is Expected to Hold Significant Market Share Over the Forecast Period

- Due to several critical factors, the monoclonal antibody segment is the fastest-growing segment in the antibody CDMO market. Monoclonal antibodies (mAbs) have demonstrated significant therapeutic potential across various diseases, including cancer, autoimmune disorders, and infectious diseases.

- In addition, several monoclonal antibody therapies have achieved notable success in clinical trials and have received regulatory approvals for various indications. Hence, the biopharmaceutical company is investing in developing monoclonal antibodies, which is anticipated to boost the growth of the antibody CDMO market. For instance, in January 2023, the UK government launched England's second Investment Zone in Liverpool, in which US pharmaceutical manufacturer TriRx made an initial GBP 10 million (USD 12.22) investment to enhance its capabilities to manufacture monoclonal antibodies.

- Similarly, in September 2023, AbolerIS Pharma announced a EUR 27.3 million (USD 28.83 million) Series A financing for advancing monoclonal antibodies for treating autoimmune diseases such as rheumatoid arthritis. Hence, high investment in monoclonal antibodies is expected to propel the demand for CDMO services, thereby boosting the segment's growth.

- Biopharmaceutical companies are highly interested in mAb development and manufacturing, as it offers immense potential for growth and profitability. For instance, in October 2022, Fujifilm Diosynth Biotechnologies, a CDMO, partnered with Argenx to manufacture a monoclonal antibody (mAb) fragment called efgartigimod. This mAb will be used to treat patients suffering from severe autoimmune diseases. Monoclonal antibodies have shown remarkable success in treating chronic illnesses by specifically targeting disease-causing molecules or cells, which leads to better patient outcomes. Similarly, in June 2023, Chime Biologics, a CDMO, announced that it had established three-way strategic cooperation with Leads Biolabs and BeiGene to accelerate LBL-007 mAb development and manufacturing for speedy clinical advancement.

- Hence, increasing investment in monoclonal antibodies and strategic collaboration of CDMO with biopharmaceutical companies is anticipated to boost the segment's growth during the forecast period.

North America is Expected to Hold a Significant Market Share Over the Forecast Period

- North America is expected to hold a significant share of the global antibody CDMO market owing to the presence of several established biopharmaceutical companies, increasing research and development activities for antibody therapeutics, rising prevalence of chronic diseases, high investment for antibody therapeutics, and strategic activities by the market players.

- Pharmaceutical companies are investing heavily in R&D, particularly in biologics. This heightened R&D activity increases the need for specialized CDMO services, particularly in antibody development. For instance, in September 2023, Star Therapeutics raised USD 90 million in an oversubscribed Series C financing round to bolster plans for its portfolio companies and antibody therapies. The Series C financing will support the clinical development of VGA039, which is currently in a Phase I trial (NCT05776069). Thus, due to high investment, biotech companies increasingly outsource their development and manufacturing activities to specialized CDMOs to leverage their expertise, reduce costs, and accelerate timelines.

- Moreover, the growing burden of cancer and autoimmune diseases such as rheumatoid arthritis is expected to increase R&D activities and thus propel the demand for CDMO services, likely boosting market growth. For instance, according to the data published by the American Cancer Society (ACS) in January 2024, the incidence of cancer cases will increase from 1.93 million in 2022 to 2.00 million in 2024, an increase of more than 60,000 cases in two years. As per the statistics released in June 2023 by the Centers for Disease Control and Prevention, it is estimated that 25.9% or 78.4 million adults in the United States aged 18 and above will be diagnosed with arthritis by a medical doctor by 2040. This trend is propelling the growth of the monoclonal antibody segment, as CDMOs play a crucial role in customizing and producing these specialized therapies.

- Several companies are penetrating the antibody contract development and manufacturing organization space via acquisition and partnerships. For instance, in October 2023, Eurofins CDMO Alphora Inc. launched a Biologics initiative, focusing on mAbs and therapeutic proteins as part of its vision to diversify and grow within North America's contract development and manufacturing industry.

- Hence, increasing investment in monoclonal antibodies, the growing burden of chronic diseases, and strategic activities by market players are expected to boost the market in North America during the forecast period.

Antibody Contract Development And Manufacturing Organization Industry Overview

The antibody contract development and manufacturing organization market is moderately competitive, with the presence of several companies operating globally and regionally. The major players operating across the market focus on adopting in-organic strategic initiatives such as mergers, partnerships, and acquisitions. Some key players in the global antibody contract development and manufacturing organization market are Lonza, Catalent Inc., Samsung Biologics, WuXi Biologics, AGC Biologics, and Charles River Laboratories.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definitions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Rate of Clinical Research and High Investment in Antibody Research

- 4.2.2 Rising Incidence of Cancer Cases

- 4.2.3 High Cost of Manufacturing Antibodies and Challenges Associated with Manufacturing

- 4.3 Market Restraints

- 4.3.1 Quality Issues While Outsourcing

- 4.3.2 Limited Outsourcing Opted by Big Biopharma Companies

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD)

- 5.1 By Product

- 5.1.1 Monoclonal Antibodies

- 5.1.2 Polyclonal Antibodies

- 5.1.3 Other Products

- 5.2 By Source

- 5.2.1 Mammalian

- 5.2.2 Microbial

- 5.3 By Therapeutic Area

- 5.3.1 Oncology

- 5.3.2 Neurology

- 5.3.3 Cardiology

- 5.3.4 Infectious Diseases

- 5.3.5 Immune-mediated Disorders

- 5.3.6 Other Therapeutic Areas

- 5.4 By End User

- 5.4.1 Biopharmaceutical Companies

- 5.4.2 Research Laboratories

- 5.4.3 Other End Users

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Spain

- 5.5.2.5 Italy

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 India

- 5.5.3.2 Japan

- 5.5.3.3 China

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of the Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Lonza

- 6.1.2 Catalent Inc.

- 6.1.3 Samsung Biologics

- 6.1.4 WuXi Biologics

- 6.1.5 AGC Biologics

- 6.1.6 AbbVie Inc.

- 6.1.7 Boehringer Ingelheim International GmbH

- 6.1.8 Charles River Laboratories

- 6.1.9 FUJIFILM Holdings Corporation

- 6.1.10 mAbxience