|

市場調査レポート

商品コード

1549871

アジア太平洋地域のCDMO:市場シェア分析、産業動向・統計、成長予測(2024~2029年)Asia-Pacific CDMO - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| アジア太平洋地域のCDMO:市場シェア分析、産業動向・統計、成長予測(2024~2029年) |

|

出版日: 2024年09月02日

発行: Mordor Intelligence

ページ情報: 英文 140 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

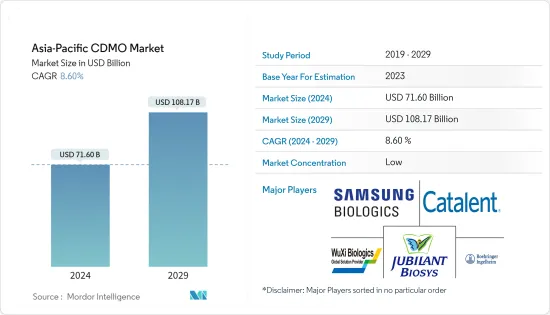

アジア太平洋地域のCDMO市場規模は2024年に716億米ドルと推計され、2029年には1,081億7,000万米ドルに達し、予測期間中(2024-2029年)のCAGRは8.60%で成長すると予測されます。

アジア太平洋地域のCDMO(医薬品開発・製造受託機関)市場は、2024年以降に大きく成長する見通しです。この成長の背景には、医薬品需要の高まり、研究開発重視の動き、医薬品開発・製造のアウトソーシング傾向の高まりがあります。

主なハイライト

- 製薬企業が医薬品開発・製造をアウトソーシングする傾向が強まっており、市場は大幅な成長を遂げます。これは、政府の強力なバックアップと、外国からの投資を誘致する魅力的なインセンティブによるところが大きいです。

- 中国、インド、韓国を含む新興国市場は、同市場における優位性を維持する構えです。これらの国々では慢性疾患の罹患率が上昇し、人口動態が高齢化しているため、医薬品に対するニーズが高まり、CDMOサービスの需要が高まることが予想されます。

- 国家衛生委員会(NHC)によると、中国には慢性疾患を患う高齢者が1億8,000万人以上おり、そのうち75%が複数の慢性疾患を抱えています。2030年までに、心血管疾患は中国政府に1兆440億米ドルの損失をもたらすと予想されています。糖尿病有病率の高さについては、中国、韓国、オーストラリアを含むアジア太平洋地域でも同様の傾向が見られます。

- 米国は依然として医薬品開発アウトソーシングの中心的な拠点であるが、APAC地域はCDMOの成長市場として注目されています。この選好は、北米や欧州に比べてコスト効率の高い製造が可能であることが主な理由です。多額の資金が割り当てられ、大学周辺に製薬研究センターが集積していることも、この動向に寄与しています。

- しかし、アジア太平洋地域のCDMO市場は深刻な労働力不足に悩まされており、人件費の大幅な高騰につながっています。この動向は、多くの欧米CDMOに米国や欧州への事業移転を促しています。さらに、国の政策、ブレグジットや米国と中国の対立のような貿易力学、パンデミックの影響は、多くの国々でサプライチェーンの再調達を促す態勢を整えています。

アジア太平洋地域のCDMO市場の動向

注射剤製剤の需要が高まる

- CDMO市場は、特にがん研究における注射薬の需要増に牽引され、成長を遂げようとしています。腫瘍学やその他の強力な薬剤(抗体結合体、ステロイド、速効性輸液など)に重点が置かれていることから、細胞毒性薬が注射剤製剤セグメントの成長の先陣を切ると予想されます。

- 注射剤は他の製剤を凌駕し、優れたリターンを提供します。これは主に、ROIの高さ、治療効果の向上、作用発現の早さに起因します。糖尿病治療薬に対する需要の急増は、これらの薬剤に依存している多くの患者の不足につながっています。この地域における注射糖尿病治療薬の需要増は、このセグメントの成長を大きく後押ししました。

- Sina Medによると、中国のヒトインスリン市場規模は2018年の27億5,000万米ドルから2030年には約46億3,000万米ドルに増加する見込みです。糖尿病の有病率の増加は、今後数年間における注射用抗糖尿病薬市場の成長を促進すると予想される主な要因です。

- さらに、細胞・遺伝子治療に対する需要の高まりが、無菌注射剤受託製造分野の成長を後押ししています。遺伝性疾患や慢性疾患向けに調整されたこれらの治療は、個別化された、しばしば治癒可能な治療を提供します。その性質上、これらの治療用の無菌注射剤の製造には、厳しい規制基準を満たすための特殊なプロセスが必要となります。

- 2023年9月、インドを拠点とするStrides社は、スペシャリティファーマCDMOの別支社を設立しました。新たに設立された同社は、生物学的製剤から複雑な注射剤、経口ソフトゼラチンカプセルまで、幅広い製品を製造しています。このような定数は、予測期間中、同地域のセグメント成長を強化すると予想されます。

インドは今後数年間で力強い成長が見込まれる

- インドの医薬品セクターは、主に製剤の基礎原料である原薬の生産に注力しています。医薬品原薬は同部門の生産高の約20%を占めるが、製剤は残りの80%を占める。インドの実力は医薬品原薬(API)にも及んでおり、500を超えるAPIを製造し、60の治療カテゴリーにまたがる60,000のジェネリックブランドの原産地となっています。

- 世界のCDMO市場は、新興市場に見られる費用対効果の高いリソースに後押しされて拡大しています。インドはCDMOの最有力候補であり、米国FDAの認可を受けた製造施設は100を超え、その数はさらに増加しています。インドの製薬セクターにおける生物製剤CDMO市場は、Zydus CadilaやLUPINのような主要プレイヤーの強固な存在感により、地歩を固めつつあります。

- インドの製薬セクターは外国投資家にとって最重要ターゲットとなっており、外資が投資する産業としては国内トップ10に入っています。インド政府は、この分野への投資をさらに強化するため、投資家に優しい外国直接投資(FDI)政策を実施しています。インド産業・国内貿易振興省によると、ヘルスケアセクター全体で、医薬品への投資額は2020年4月から2023年3月までの間に214億6,000万米ドルと最も多いです。医薬品部門へのこのような一貫した投資は、予測期間中の医薬品受託製造市場を促進する可能性があります。

- インドの医薬品セクターは、COVID-19パンデミックによって急成長を遂げました。パンデミック後、インドでは抗ウイルス薬や抗菌薬の需要と生産が顕著に増加しました。その結果、この分野の企業収益は増加しました。米国と中国の貿易摩擦の激化は、世界な医薬品サプライチェーンにおける地域多様化の必要性を浮き彫りにしました。中国のコスト構造は変化し、より高価なアウトソーシング拠点となる一方、インドの魅力は高まっています。

アジア太平洋地域のCDMO産業の概要

アジア太平洋地域のCDMO市場は、Catalent Inc.、Jubilant Biosys Ltd.、Samsung Biologics、Boehringer Ingelheim Group、WuXi Biologicsなどの大手企業が存在するため断片化されています。他のプレーヤーは、市場に参入し、提供製品を拡大するために買収やパートナーシップ戦略を採用しています。

- 2023年2月キャタレント社は、シンガポールのクリニカル・サプライに220万米ドル相当の施設拡張を完了したことを発表しました。この拡張により、敷地面積は31,000平方フィートに拡大し、新たに35台のULフリーザーの設置が可能となった。また、ULT製品の二次包装能力を追加し、mRNAベースのワクチンや細胞・遺伝子治療などのバイオ医薬品や先進モダリティの処理能力を向上させることで、より大規模なパッケージングキャンペーンに対応できるようになりました。

- 2023年6月富士フイルムジオシンスバイオテクノロジーズは、特にアジアに拠点を置く製薬会社やバイオテクノロジー企業をターゲットに、生物製剤や先端治療薬に対応する受託開発・製造サービスの営業サポートと顧客サービスを強化するため、東京の営業所を強化する意向を発表しました。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ファイブフォース分析分析

- CMOのポーター5フォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- CROのポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- CMOのポーター5フォース分析

- 産業政策

- バリューチェーン分析

- 市場力学

- 市場促進要因

- 大手製薬企業によるアウトソーシング量の増加

- 研究開発投資の増加

- 市場抑制要因

- 地域におけるサプライチェーン関連の制約によるリードタイムの増加

- 地域全体での熟練労働者の不足

- 市場促進要因

- OSDセグメントにおける3Dプリンティングの発展に関する定性的考察

- 製造プロセスにおける3Dプリンティングの進化と従来プロセスに対する主な利点

- 3Dプリンティングベースのプロセスで製造される主な医薬品の分析

- 導入された主な技術(SLSとFDM)の分析と相対的な優位性

- 利害関係者に関する主な発展

- 技術スナップショット

- 製剤化技術

- 投与経路別の剤形

- 医薬品研究開発のアウトソーシングに関する主な検討事項

- CROの主要セグメントバイオ分析試験、セントラルラボラトリー試験、cGMP試験

第5章 市場セグメンテーション

- サービスタイプ別CMOセグメント

- 医薬品原薬(API)製造

- 低分子

- 高分子

- 高力価(HPAPI)

- 最終製剤(FDF)開発・製造

- 固形製剤

- 錠剤

- その他

- 液体製剤

- 注射剤製剤

- 二次包装

- 医薬品原薬(API)製造

- 研究フェーズCROセグメント別

- 前臨床

- フェーズI

- フェーズII

- フェーズ III

- フェーズ IV

- 国別

- 中国

- 日本

- インド

- オーストラリア・ニュージーランド

第6章 競合情勢

- 企業プロファイル

- Catalent Inc.

- Jubilant Biosys Ltd

- Thermo Fisher Scientific Inc.

- Samsung Biologics

- Syngene International Limited

- Lonza Group

- WuXi Biologics

- Boehringer Ingelheim Group

- FUJIFILM Diosynth Biotechnologies

- Pfizer CentreOne

- Recipharm AB

- Stella Lifecare

第7章 投資分析

第8章 市場機会と今後の動向

The Asia-Pacific CDMO Market size is estimated at USD 71.60 billion in 2024, and is expected to reach USD 108.17 billion by 2029, growing at a CAGR of 8.60% during the forecast period (2024-2029).

The Asia-Pacific CDMO (contract development and manufacturing organization) market is poised for substantial growth in 2024 and beyond. This growth can be attributed to escalating pharmaceutical demands, increasing emphasis on R&D, and the growing trend of outsourcing drug development and manufacturing.

Key Highlights

- The market is set for substantial growth, driven by the escalating trend of pharmaceutical companies outsourcing drug development and manufacturing. This is largely due to robust government backing and enticing incentives that lure foreign investments.

- Emerging markets, including China, India, and South Korea, are poised to maintain their dominance in the market. The rising incidence of chronic diseases and aging demographics in these nations are expected to drive up the need for pharmaceuticals, subsequently boosting the demand for CDMO services.

- China has over 180 million elderly citizens suffering from chronic diseases; of that, 75% has more than one, according to the National Health Commission (NHC). By 2030, cardiovascular diseases are expected to cost the Chinese government USD 1,044 billion. Similar trends for the high prevalence of diabetes are present in Asia-Pacific, including China, South Korea, and Australia.

- While the United States remains the central hub for pharmaceutical development outsourcing, the APAC region stands out as the favored CDMO growth market. This preference is largely attributed to the region's cost-effective manufacturing compared to North America and Europe. Significant funding allocations and the clustering of pharmaceutical research centers around universities contribute to this trend.

- However, the Asia-Pacific CDMO market is grappling with a severe labor shortage, leading to a significant surge in labor costs. This trend has prompted numerous Western CDMOs to relocate their operations back to the United States and Europe. Moreover, national policies, trade dynamics like Brexit and the US-China conflict, and the repercussions of the pandemic are poised to prompt the reshoring of supply chains in numerous nations.

Asia-Pacific CDMO Market Trends

The Demand For Injectable Dose Formulation is Rising in the Market

- The CDMO market is poised for growth, driven by increasing demand for injectable drugs, notably in cancer research. With a strong emphasis on oncology and other potent medications (including antibody conjugates, steroids, and fast-acting IV fluids), cytotoxics are anticipated to spearhead the growth in the injectable dose formulation segment.

- Injectable drugs are poised to outperform other drug formulations, offering superior returns. This is primarily attributed to their higher ROI, enhanced therapeutic efficacy, and quicker onset of action. The surge in demand for diabetes drugs has led to shortages for many patients reliant on these medications. The increased demand for injectable diabetes drugs in the region significantly boosted the segment's growth.

- According to Sina Med, the value of the human insulin market in China is expected to increase from USD 2.75 billion in 2018 to around USD 4.63 billion in 2030. The increasing prevalence of diabetes is a key driver expected to propel the growth of the injectable antidiabetic drugs market in the coming years.

- Further, the rising demand for cell and gene therapies is propelling the growth of the sterile injectable contract manufacturing sector. These therapies, tailored for genetic and chronic diseases, offer personalized and often curative treatments. Given their nature, manufacturing sterile injectables for these therapies necessitates specialized processes to meet stringent regulatory standards.

- In September 2023, India-based Strides introduced a separate branch of specialty pharma CDMO. The newly established company manufactures a wide array of products, spanning from biologicals to intricate injectables and oral soft-gelatin capsules. Such constants are expected to bolster the segmental growth in the region during the forecast period.

India is Expected to Witness Robust Growth in the Upcoming Years

- The Indian pharmaceutical sector predominantly focuses on producing bulk pharmaceuticals, the foundational ingredients for formulations. While bulk pharmaceuticals constitute roughly 20% of the sector's output, formulations make up the remaining 80%. India's prowess extends to active pharmaceutical ingredients (APIs), with the country manufacturing over 500 APIs and serving as the origin for 60,000 generic brands spanning 60 therapeutic categories.

- The global CDMO market is expanding, propelled by the cost-effective resources found in emerging markets. India is the top choice for CDMOs, boasting over 100 manufacturing facilities approved by the US FDA, with this number rising. The biologics CDMO market in India's pharmaceutical sector is gaining ground, bolstered by the robust presence of key players like Zydus Cadila and LUPIN.

- The pharmaceutical sector in India has become a prime target for foreign investors, ranking among the nation's top ten industries for foreign investment. The Indian government has implemented an investor-friendly Foreign Direct Investment (FDI) policy to further bolster investments in this sector. According to the Department for Promotion of Industry and Internal Trade (India), across the entire healthcare sector, the amount invested in drugs and pharmaceuticals witnessed the highest foreign investment of USD 21.46 billion between April 2020 and March 2023. Such consistent investment in the pharmaceutical sector may propel the market for pharmaceutical contract manufacturing during the forecast period.

- The Indian pharmaceutical sector experienced a surge in growth, propelled by the COVID-19 pandemic. Post-pandemic, there was a notable uptick in demand and production for anti-viral and anti-bacterial drugs within India. Consequently, companies in this sector notched up rising revenues. The increased trade tensions between the US and China underscored the global pharmaceutical supply chain's need for geo-diversification. China's cost structure shifted, making it a pricier outsourcing hub, while India's appeal grew.

Asia-Pacific CDMO Industry Overview

The Asia-Pacific CDMO Market is fragmented because of the presence of major players like Catalent Inc., Jubilant Biosys Ltd, Samsung Biologics, Boehringer Ingelheim Group, and WuXi Biologics. The other players are adopting acquisition and partnership strategies to enter the market and expand their offerings.

- February 2023: Catalent unveiled the completion of the expansion of a facility worth USD 2.2 million to its Clinical Supply in Singapore. The expansion increased the site footprint to 31,000 sq. ft, allowing the installation of 35 new UL freezers. The investment also enabled the facility to support bigger packaging campaigns with additional secondary packaging capacities for ULT products and increased capacity to process biopharmaceutical products and advanced modalities such as mRNA-based vaccines and cell and gene therapies.

- June 2023: FUJIFILM Diosynth Biotechnologies announced its intentions to enhance the commercial office in Tokyo to enhance sales support and customer service for contract development and manufacturing services catering to Biologics and Advanced Therapies, specifically targeting pharmaceutical and biotechnology firms based in Asia.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Porter's Five Forces Analysis for CMO

- 4.2.1.1 Bargaining Power of Suppliers

- 4.2.1.2 Bargaining Power of Buyers

- 4.2.1.3 Threat of New Entrants

- 4.2.1.4 Threat of Substitute Products

- 4.2.1.5 Intensity of Competitive Rivalry

- 4.2.2 Porter's Five Forces Analysis for CRO

- 4.2.2.1 Bargaining Power of Suppliers

- 4.2.2.2 Bargaining Power of Buyers

- 4.2.2.3 Threat of New Entrants

- 4.2.2.4 Threat of Substitute Products

- 4.2.2.5 Intensity of Competitive Rivalry

- 4.2.1 Porter's Five Forces Analysis for CMO

- 4.3 Industry Policies

- 4.4 Industry Value Chain Analysis

- 4.5 Market Dynamics

- 4.5.1 Market Drivers

- 4.5.1.1 Increasing Outsourcing Volume by Big Pharmaceutical Companies

- 4.5.1.2 Increasing Investment in Research and Development

- 4.5.2 Market Restraints

- 4.5.2.1 Increasing Lead Time Owing to Supply Chain Related Constraints in the Region

- 4.5.2.2 Skilled Labour Shortages Across the Region

- 4.5.1 Market Drivers

- 4.6 Qualitative Coverage on the 3D Printing Developments in the OSD Segment

- 4.6.1 Evolution of 3D Printing in Fabrication Processes and the Key Advantages Over Conventional Processes

- 4.6.2 Analysis of Major Drugs Manufactured Using 3D Printing-based Process

- 4.6.3 Analysis of Key Techniques Deployed (SLS & FDM), Along with their Relative Advantages

- 4.6.4 Key Developments on Stakeholders

- 4.7 Technology Snapshot

- 4.7.1 Dosage Formulation Technologies

- 4.7.2 Dosage Forms by Route of Administration

- 4.7.3 Key Considerations for Outsourcing of Pharmaceutical R&D

- 4.7.4 Major Segments in CRO Bio Analytical Testing, Central Laboratory Testing, and cGMP Testing

5 MARKET SEGMENTATION

- 5.1 By Service Type CMO Segment

- 5.1.1 Active Pharmaceutical Ingredient (API) Manufacturing

- 5.1.1.1 Small Molecule

- 5.1.1.2 Large Molecule

- 5.1.1.3 High Potency (HPAPI)

- 5.1.2 Finished Dosage Formulation (FDF) Development and Manufacturing

- 5.1.2.1 Solid Dose Formulation

- 5.1.2.1.1 Tablets

- 5.1.2.1.2 Others

- 5.1.2.2 Liquid Dose Formulation

- 5.1.2.3 Injectable Dose Formulation

- 5.1.3 Secondary Packaging

- 5.1.1 Active Pharmaceutical Ingredient (API) Manufacturing

- 5.2 By Research Phase CRO Segment

- 5.2.1 Pre-clinical

- 5.2.2 Phase I

- 5.2.3 Phase II

- 5.2.4 Phase III

- 5.2.5 Phase IV

- 5.3 By Country

- 5.3.1 China

- 5.3.2 Japan

- 5.3.3 India

- 5.3.4 Australia and New Zealand

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Catalent Inc.

- 6.1.2 Jubilant Biosys Ltd

- 6.1.3 Thermo Fisher Scientific Inc.

- 6.1.4 Samsung Biologics

- 6.1.5 Syngene International Limited

- 6.1.6 Lonza Group

- 6.1.7 WuXi Biologics

- 6.1.8 Boehringer Ingelheim Group

- 6.1.9 FUJIFILM Diosynth Biotechnologies

- 6.1.10 Pfizer CentreOne

- 6.1.11 Recipharm AB

- 6.1.12 Stella Lifecare