|

市場調査レポート

商品コード

1521651

貨物輸送:市場シェア分析、産業動向と統計、成長予測(2024年~2029年)Cargo Shipping - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 貨物輸送:市場シェア分析、産業動向と統計、成長予測(2024年~2029年) |

|

出版日: 2024年07月15日

発行: Mordor Intelligence

ページ情報: 英文 70 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

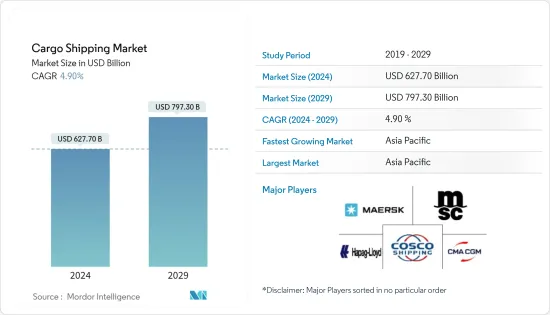

貨物輸送の市場規模は2024年に6,277億米ドルと推定・予測され、2029年には7,973億米ドルに達し、予測期間中(2024-2029年)のCAGRは4.90%で成長すると予測されます。

海上貨物活動の増加によるコンテナ船、ばら積み貨物輸送、その他の貨物輸送に対する需要の高まりが、貨物輸送市場を牽引しています。

船舶による貨物輸送需要の増加や貿易関連協定の急増などの要因が貨物輸送市場の成長を補完しています。輸送コストと在庫コストの変動は貨物輸送市場の成長を妨げます。しかし、海上輸送の自動化が予想され、海上安全基準が高まるなどの要因が、予測期間中の貨物輸送市場の成長に機会を提供すると予想されます。

主なハイライト

- 2022年の日本の沿岸船舶による国内輸送貨物量は、2021年の3億2,466万トンに対し、3億2,093万トンとなった。

- インド港湾海運水路省によると、2022年度のインド全土の海港における貨物取扱量は13億2,300万トンに達し、2021年度比で前年比6.0%増加しました。

貨物輸送市場の動向

市場拡大を支えるクロスボーダー取引の増加

海上を介したクロスボーダー取引の増加、eコマース産業の成長による海上貨物量の増加、各国間の様々な自由貿易協定の実施が海上貿易活動の拡大に寄与しており、これが貨物輸送市場の成長にプラスに寄与しています。

- 2022年現在、世界の商船隊の一般貨物輸送の数は17,784隻、ばら積み貨物輸送の数は12,941隻に達しています。

世界の商船隊の船腹容量はここ数十年で着実に増加しているが、これは海上貿易の需要増に起因しており、1回の航海でより多くの量を輸送するために、より大型の船舶が必要とされています。

- 2022年には、コンテナ船の容量は2億9,300万重量トンに達し、2018年から2022年にかけて3.1%のCAGRを記録しました。

海上貿易活動の増加に伴い、これらの船舶が様々な商品を輸送するため、これらの貨物輸送に対するより大きな需要が存在し、それによって市場の急成長にプラスの影響を与えています。

世界中の主要な海上貨物輸送業者は、国境を越えたeコマース活動の成長により、近年輸送貨物量の急増を目の当たりにしています。海上輸送は依然として長距離輸送の主流であるため、貨物輸送業者の需要は大幅に増加しています。

- 2022年には、オンラインショッピングを利用するインドの消費者の間では米国が越境EC市場全体の21%を占め、次いでオーストラリアが続いた。

このように、eコマースの急速な進展は、海上輸送活動の活発化と相まって、今後数年間の貨物輸送市場の急成長に寄与する可能性があります。

欧州が市場で大きなシェアを占める

海上貿易の増加と経済成長に伴い、貨物輸送の需要は欧州市場で顕著な成長が見込まれます。

海運部門はドイツ経済の最も重要な部門のひとつです。年間売上高は500億ユーロ(532億2,000万米ドル)に上り、海運業に直接または間接的に依存する雇用者数は2022年には40万人に達します。

ドイツでは、360以上の海運会社が約2,700隻の船舶を運航しています。船主の国籍別に見ると、ドイツはギリシャ、日本、中国(第4位)に次いで商船隊を有する最大の海運国です。

- ドイツは、世界のコンテナ輸送能力の約29%をコンテナ船で占めており、船主の国籍別では依然として国際的なリーダーです。

約9つの造船所がドイツ海軍造船産業を支えており、約2,800社が造船および海洋産業で活躍しています。これらの企業は、ドイツの造船所からの納品で約85%の国内付加価値を生み出しています。

同様に、英国の輸出入のほぼ95%は、400以上の英国の港を経由して海上で行われています。

- 2022年、スペインは米国、中国、日本に次ぐ世界第4位の魚介類輸入国となった。

- 2022年、スペインの全産地からの水産物輸入額は96億米ドルで、2021年から7.6%増加しました。2022年のスペインの輸出総額は前年比3.4%増の59億米ドルに達しました。

スペインは欧州の海運と物流にとって不可欠です。スペインの海運業界は、あらゆる部門(道路、鉄道、航空)にまたがる整備されたインフラ・ネットワークに支えられており、欧州内外の効率的で有能な供給ルートを誇っています。スペインには100社以上の海運会社があり、巨大な船隊を形成しています。スペインは三方を海に囲まれているため、港やその他の海運ハブを設置するのに理想的な国です。接続の良い施設は、この地域のいくつかの国際空港とつながっています。

上記の要因から、市場の欧州セグメントは予測期間中に成長すると予想されます。

貨物輸送業界の概要

貨物輸送市場は細分化されており、多くの国際企業が参入しています。このセグメントの主要企業は、マースク、MSC、CMA、COSCO、Hapag Lloydなどです。参入障壁の高さは、車両コストの高騰やスケールメリットの増大により市場を抑制しており、これが業界の競合に影響を与えています。しかし、主要企業は、今後数年間の市場シェアを獲得するために、戦略的パートナーシップや買収に関与しています。

- 2023年1月、A.P. Moller-Maersk(マースク)はデンマークのプロジェクト・ロジスティクスのエキスパートであり、コンテナ輸送以外のプロジェクト・ロジスティクスと世界・オペレーションに優れた能力を持つMartin Bencher Groupの買収完了を発表しました。マーティン・ベンチャーの加入により、両社は世界中の顧客にプロジェクト・ロジスティクス・サービスを提供する能力を強化するとともに、幅広い業界により包括的なサービスを提供することになります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の成果

- 調査の前提

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 国家間の貿易協定の増加

- 国際貿易量の増加

- 市場抑制要因

- 燃料費の高騰が市場に影響

- バリューチェーン/サプライチェーン分析

- 業界の規制と政策

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 船種

- バルクキャリア

- 一般貨物輸送

- コンテナ船

- タンカー

- リーファー船

- 業種

- 飲食品

- 製造業

- 石油・ガス

- 製薬

- 電気・電子

- その他

- 貨物タイプ

- リキッドカーゴ

- ドライカーゴ

- 一般カーゴ

- 地域

- 北米

- 米国

- カナダ

- その他北米地域

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州

- アジア太平洋

- インド

- 中国

- 日本

- 韓国

- その他アジア太平洋地域

- 世界のその他の地域

- 南米

- 中東・アフリカ

- 北米

第6章 競合情勢

- ベンダー市場シェア

- 企業プロファイル

- A. P. Moller-Maersk AS

- MSC Mediterranean Shipping Company SA

- CMA CGM

- China COSCO Holdings Company Limited

- Hapag-Lloyd

- ONE(Ocean Network Express)

- Evergreen Line

- Wan Hai Lines

- Zim

- SITC

- Zhonggu Logistics Corp.

- Antong Holdings(QASC)

第7章 市場機会と今後の動向

- ロジスティクス分野における技術開発

The Cargo Shipping Market size is estimated at USD 627.70 billion in 2024, and is expected to reach USD 797.30 billion by 2029, growing at a CAGR of 4.90% during the forecast period (2024-2029).

The rising demand for cargo vessels such as container ships, bulk carriers, and others due to the growth in sea freight activity is driving the cargo shipping market.

Factors such as the increasing demand for cargo transportation through ships and the surge in trade-related agreements supplement the growth of the cargo shipping market. Fluctuations in transportation and inventory costs hamper the growth of the cargo shipping market. However, factors such as the anticipated trend of automation in marine transportation and an increase in marine safety norms are expected to provide opportunities for the growth of the cargo shipping market during the forecast period.

Key Highlights

- In 2022, the freight volume transported domestically via coastwise vessels in Japan stood at 320.93 million metric ton, compared to 324.66 million metric ton in 2021.

- According to the Indian Ministry of Ports, Shipping, and Waterways, the total volume of cargo handled at seaports across India touched 1,323 million metric ton in FY 2022, witnessing a Y-o-Y increase of 6.0% compared to FY 2021.

Cargo Shipping Market Trends

Increasing Cross-border Trading to Support Market Expansion

The increasing cross-border trading activity via sea, rising sea freight volumes due to the growth of the e-commerce industry, and the implementation of various free-trade agreements across nations are contributing to expanding sea trade activity, which, in turn, is positively contributing to the growth of the cargo shipping market.

- The number of general cargo ships in the global merchant fleet stood at 17,784 units as of 2022, while the number of bulk cargo carriers reached 12,941 units.

The capacity of the global merchant fleet has increased steadily in recent decades, attributed to the rising demand for more seaborne trade, which calls for larger vessels to transport more volume in one trip.

- In 2022, the capacity of container ships touched 293 million dwt, registering a CAGR of 3.1% between 2018 and 2022.

With the rising seaborne trade activity, there exists a greater demand for these cargo carriers as these ships transport various goods, thereby positively impacting the surging growth of the market.

Leading ocean freight forwarders across the world are witnessing a rapid surge in the volume of freight they are transporting in recent years, owing to the growth in cross-border e-commerce activity. Since sea freight remains the dominant transportation medium to ship goods across long distances, the demand for cargo carriers shoots up extensively.

- In 2022, the United States was the leading market among Indian consumers who shop online, capturing 21% of the cross-border e-commerce market out of the overall cross-border e-commerce share, followed by Australia.

Thus, the rapid advancement in e-commerce, coupled with rising sea freight activity, may contribute to the surging growth of the cargo shipping market in the coming years.

Europe Holds a Significant Share in the Market

With the increasing seaborne trade and economic growth, the demand for cargo shipping is anticipated to witness evident growth in the European market.

The marine sector is one of the most important sectors of the German economy. The annual turnover is up to EUR 50 billion (USD 53.22 billion), and the number of jobs directly or indirectly dependent on the maritime industry was up to 400,000 in 2022.

In Germany, more than 360 shipping companies operate around 2,700 seagoing vessels. According to owner nationality, Germany is the largest shipping nation after Greece, Japan, and China (ranked 4th) with its merchant fleet.

- Germany holds around 29% of all container-carrying capacities worldwide in container shipping and is still positioned as an international leader according to owner nationality.

About nine shipyards support the German naval shipbuilding industry, and about 2,800 companies are active in the shipbuilding and ocean industries. The companies generate a domestic value added of approximately 85% on deliveries from German shipyards.

Likewise, almost 95% of all UK imports and exports move by sea through over 400 British ports.

- In 2022, Spain was the world's fourth largest importer of fish and seafood after the United States, China, and Japan.

- In 2022, Spain's seafood imports from all origins were USD 9.6 billion, up 7.6% from 2021. Total Spanish exports in 2022 reached USD 5.9 billion, up 3.4% compared to the previous year.

Spain is vital to the shipping and logistics in Europe. Spain's shipping industry is supported by its network of maintained infrastructure across all sectors (road, rail, and air), allowing it to boast efficient and capable supply routes through Europe and beyond. Over a hundred different shipping companies in Spain make up its massive fleet. Spain is covered by water on three sides, making it ideal for establishing ports and other shipping hubs. Well-connected facilities are linked to several international airports in the region.

Owing to the abovementioned factors, the European segment of the market is expected to grow during the forecast period.

Cargo Shipping Industry Overview

The cargo shipping market is fragmented in nature, with the presence of many international companies in the market. The top players in the segment include Maersk, MSC, CMA, COSCO, and Hapag Lloyd. High barriers to entry restrain the market due to the high cost of vehicles and increasing economies of scale, which affect competition in the industry. However, key players are involved in strategic partnerships and acquisitions to capture market share in the coming years.

- In January 2023, A.P. Moller-Maersk (Maersk) announced the completion of its acquisition of Martin Bencher Group, a Danish project logistics expert with premium capabilities within non-containerized project logistics and global operations. With the addition of Martin Bencher, these companies are strengthening their ability to offer project logistics services to their global clients while providing a more comprehensive offering to a wide array of industries.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 The Rise of Trade Agreements Between Nations

- 4.2.2 Increasing Volume of International Trade

- 4.3 Market Restraints

- 4.3.1 Surge in Fuel Costs Affecting the Market

- 4.4 Value Chain/Supply Chain Analysis

- 4.5 Industry Policies and Regulations

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Ship Type

- 5.1.1 Bulk Carriers

- 5.1.2 General Cargo Ships

- 5.1.3 Container Ships

- 5.1.4 Tankers

- 5.1.5 Reefer Ships

- 5.2 Industry Type

- 5.2.1 Food and Beverages

- 5.2.2 Manufacturing

- 5.2.3 Oil and Gas

- 5.2.4 Pharmaceutical

- 5.2.5 Electrical and Electronics

- 5.2.6 Others

- 5.3 Cargo Type

- 5.3.1 Liquid Cargo

- 5.3.2 Dry Cargo

- 5.3.3 General Cargo

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Rest of North America

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 India

- 5.4.3.2 China

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 Rest of Asia-Pacific

- 5.4.4 Rest of the World

- 5.4.4.1 South Ameria

- 5.4.4.2 Middle East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 A. P. Moller-Maersk AS

- 6.2.2 MSC Mediterranean Shipping Company SA

- 6.2.3 CMA CGM

- 6.2.4 China COSCO Holdings Company Limited

- 6.2.5 Hapag-Lloyd

- 6.2.6 ONE (Ocean Network Express)

- 6.2.7 Evergreen Line

- 6.2.8 Wan Hai Lines

- 6.2.9 Zim

- 6.2.10 SITC

- 6.2.11 Zhonggu Logistics Corp.

- 6.2.12 Antong Holdings (QASC)

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Technological Developments in the Logistics Sector