磁気の世界市場:市場シェア分析、産業動向・統計、成長予測(2024~2029年)

Magnetics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)- 発行日

- ページ情報

- 英文 152 Pages

- 納期

- 2~3営業日

- 商品コード

- 1521635

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

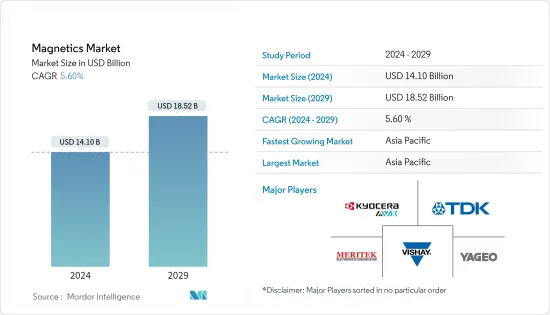

世界の磁気の市場規模は、2024年に141億米ドルに達し、2024~2029年にかけてCAGR 5.60%で成長し、2029年には185億2,000万米ドルに達すると予測されています。

磁気部品は、冷蔵庫やテレビから通信機器に至るまで、高度な産業機器と一般家庭用電化製品の両方で広く採用されています。磁気部品は自動車で重要な役割を果たしており、ダッシュボードディスプレイ、室内外照明、空調制御、その他のシステム用電源の電圧を監視しています。これらの部品は、携帯電話、コンピュータ、通信システム、その他の電子製品に使用されています。

主なハイライト

- HPCとAIの需要は世界的に爆発的に伸びています。同様に、スマートフォン、PC、インフラの需要も安定しています。スマートフォンの販売台数は2024年に大幅に回復し、これらの磁性部品の需要を牽引すると予想されます。高周波インダクタは携帯電話に使用され、高速で安定したネットサーフィンに役立っています。さらに、モバイル通信ネットワークの進歩に伴い、スマートフォンに搭載されるインダクタの数は大幅に増加しています。インダクタは、カラー液晶やバッテリー寿命の向上など、スマートフォンのさまざまな機能を強化します。

- スマートフォンのOEMは2024年に人工知能対応スマートフォンを強化し、生成AI機能と追加ストレージ容量を搭載することで、より優れたバッテリー寿命の需要を生み出しています。さらに、技術の進歩に伴い、消費者は古いデバイスよりも先進技術の製品を好むようになり、これがスマートフォンの売上を押し上げています。

- 燃料電池、風力発電、太陽光発電など、国間の電力網接続(スーパーグリッド)や直流に基づく再生可能エネルギー源のニーズは世界的に拡大しており、磁性部品の需要も拡大しています。

- 従来、変圧器は鉄製であったが、素材の発達に伴い、シリコン鋼、アモルファス鋼、フェライト・セラミックスなどが、その高い貫通性から変圧器のコア素材として使用されるようになった。同様に、インダクタやEMIフィルタにも鉄やフェライトなどの磁性素材がコア材として使用され、コイルには銅が使用されるのが一般的です。

- 現在、自律走行技術やADASの急速な進化に伴い、自動車にはレーダー、カメラ、LiDARなど数多くのセンサーが搭載されており、その結果、磁性部品は飛躍的に成長しています。自動車分野の進歩が続いているため、主なベンダーは消費者の需要に応えるため、製品開発と進歩に継続的に投資しています。

- 例えば、TDK Corporationは2024年1月、車載オーディオバス(A2B)用途向けに高耐久性、広動作範囲、高インダクタンス公差を実現した新インダクタKLZ2012-Aシリーズを発売しました。2024年1月より量産を開始します。A2B技術は、多種多様な通信バスのケーブルハーネスを軽量化するために開発されたもので、自動車の燃費向上を最終目標としています。

磁気市場の動向

産業用(モーター/UPS)が成長を牽引

- 産業用モーターは、電気エネルギーを機械エネルギーに変換する電気機器です。一般的に、発電機や送電網のような交流(AC)電源から電力を供給されます。産業用モーターは、さまざまな産業で利用されるさまざまな機器や機械に電力と動きを供給するために特別に設計されています。高負荷に耐え、厳しい環境でも機能することが要求されるため、これらのモーターは通常、住宅や商業環境で使用されるものよりも耐久性が高く、強力です。産業用モーター・用途における磁気インダクタンスへのニーズの高まりが市場を牽引します。

- Industrial Energy Acceleratorのレポートによると、企業が消費する世界の電気エネルギーの大部分は、稼働中の数百万台の電気モーターに起因しています。これらのモーターは、換気、圧縮空気の生成、水の汲み上げなど、さまざまな分野で不可欠な産業プロセスや補助システムに電力を供給する上で極めて重要です。さらに、産業用モーター市場では最近、AC電源とDC電源の両方で動作するように設計されたユニバーサルモーターが導入されています。これらのモーターに対する需要の増加と、様々なベンダーによる開発の増加は、磁気コンポーネント用途を増加させると思われます。

- 産業用モーターの設計と機能は、トルクを発生させる主要な方法として機能する磁気誘導に大きく依存しています。エンジニアは、磁気誘導の原理を十分に理解し、さまざまな設計要素を最適化することで、さまざまな用途に適した効率的で高性能なモーターを開発することができます。

- データセンターの無停電電源装置(UPS)システムに対する需要は、データセンターへの投資の増加により大きな伸びを示しています。様々な産業がデジタル業務やサービスを拡大するにつれて、データの保存、処理、管理に対する需要が急増しています。その結果、これらの要件を満たすためにデータセンターインフラに多額の投資が行われています。Cloudsceneによると、2023年9月現在、中国には448のデータセンターがあり、アジア太平洋のどの国・地域よりも多く、市場機会を大きく見出すことができます。

急成長を遂げる中国

- 中国における家電、自動車、医療機器の生産増加により、受動電子機器の需要は予測期間中も堅調に推移すると予想されます。

- Rayming PCB and Assemblyによると、中国はここ数年エレクトロニクス製造産業を支配し続けています。この国は、米国との最近の貿易にもかかわらず、エレクトロニクスの不可欠な製造場所です。大規模な製造企業として、中国はノートパソコンと携帯電話の約50%を世界に輸出しています。

- 世界のエレクトロニクス市場は、2022年の3兆5,549億4,000万米ドルから2023年には3兆7,393億7,000万米ドルに成長しました。世界のエレクトロニクス分野では、中国が収益の大きな割合を占めています。同国は電子機器生産国の上位にランクされています。コンシューマーエレクトロニクスから工業用部品まで、さまざまなエレクトロニクス製品を生産しています。南部のDongguan、Shenzhenといった都市には工場があります。また、上海や青クラウドにも工場があります。

- 中国はノートパソコンメーカーの世界の生産シェアが突出しています。中国が輸入半導体に依存しているにもかかわらず、この国は多くの世界トップクラスのノートパソコンブランドにとって良い選択肢であり続けています。KunshanとChongqingはラップトップ製造の2大クラスターであり、Dongguan、Shenzhenのような他の人気のある電子生産拠点もあります。これらのハブはノートパソコン、部品、アクセサリーの生産で知られています。

- 100万人以上の人口を抱える都市が米国には9つしかないのに比べ、中国には約160の都市があります。このため、電子機器の製造と消費の拡大により、あらゆる家電や家庭用電子機器の電気流量管理に対応するさまざまな受動部品のニーズが高まると予想されます。

- 過去15年間にわたるEV産業をターゲットとした中国の取り組みは、同国の最近の歴史における産業政策の最も成功した事例のひとつです。補助金を含む政府の大規模な介入が、国内産業と市場の同時成長を可能にしました。政策が実施されたタイミングは極めて重要で、バッテリー技術の進歩やEVの消費者受容の拡大と同時期に実施されたからです。重要なのは、既存の自動車会社の多くが最近までEV技術を否定していたことです。

- 一方、中国の競合他社は、内燃機関技術で数十年にわたって蓄積された知的財産を持つ多国籍企業を技術的に飛躍させるチャンスを素早くつかみました。中国はまた、EVの主要部品であるリチウム電池の世界の主要生産国でもあります。国際エネルギー機関(IEA)によると、中国は電池の65%、正極の80%を生産しており、エネルギー省の推定はさらに高いです。このように、同国の自動車分野で調査された市場の成長見通しが示されています。

磁気産業の概要

磁気市場は断片化されており、製品に多額の投資を行ってきた長年の既存プレーヤーで構成されています。新規参入企業は高額の投資を必要とします。各社は強力な競争戦略によって存続しており、主なプレーヤーはTDK Corporation、Yageo Corporation、Meritek Electronics Corporation、AVX Corporation(Kyocera Group)、Vishay Intertechnoloです。

2024年1月、TDK Corporationsの子会社であるTDK Ventures Inc.は、デジタルとエネルギーの変革を目指すシンガポールのハイテク企業Silicon Boxに出資しました。シリコンボックスを通じて半導体パッケージのイノベーション市場を加速させる計画です。

2023年11月、Bournsは高い自己共振周波数、高Q、厳しいインダクタンス許容差を持つエアコイルインダクタシリーズを発表しました。モデルAC4842 RAir Coil Inductor Seriesは、RF用途設計者に幅広い高Qソリューションオプションを提供する低損失、高周波ソリューションを提供します。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業の魅力度 - ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

- 磁気デバイスカテゴリーの技術概要

- 市場のマクロ動向評価

第5章 市場力学

- 市場促進要因

- 再生可能エネルギー需要の増加

- 電気自動車と自律走行車の需要増加が磁気部品市場を牽引

- 市場の課題

- 金属価格の上昇が部品製造コストに影響

第6章 市場セグメンテーション

- タイプ別

- 巻線インダクタ

- 多層インダクタ

- 薄膜インダクタ

- フェライトコア・EMC部品

- EMIフィルタ

- RF/パワートランス

- 電流センス・その他のトランス

- エンドユーザー用途別

- 太陽光・風力

- EV/HEV用

- 産業用(モーター/UPS)

- 鉄道/輸送

- コンシューマーエレクトロニクス

- その他のエンドユーザー用途

- 地域別

- 中国

- 日本

- 米国

- 台湾

- 東南アジア

- 韓国

- 欧州

- ラテンアメリカ

- 中東・アフリカ

第7章 競合情勢

- 企業プロファイル

- TDK Corporation

- Yageo Corporation

- Meritek Electronics Corporation

- AVX Corporation(Kyocera Group)

- Vishay Intertechnology

- Panasonic Corporation

- Taiyo Yuden Co. Ltd

- Exxelia Technology

- Bourns Inc.

- Wurth Elektronik Group

- Coilcraft Inc.

第8章 市場展望

目次

The Magnetics Market size is estimated at USD 14.10 billion in 2024, and is expected to reach USD 18.52 billion by 2029, growing at a CAGR of 5.60% during the forecast period (2024-2029).

Magnetic components are widely adopted in both advanced industrial and common household appliances, ranging from refrigerators and televisions to telecommunication devices. Magnetics plays a crucial role in cars, monitoring voltage in power supplies for dashboard displays, interior and exterior lighting, climate control, and other systems. These components are used in cell phones, computers, communication systems, and other electronic products.

Key Highlights

- The global demand for HPC and AI is exploding. Similarly, the demand for smartphones, PCs, and infrastructures is stabilizing. Smartphone sales are expected to recover significantly in 2024, driving the demand for these magnetic components. High-frequency inductors are used in mobile phones, which help with fast and stable internet surfing. Furthermore, with the advancement in mobile communication networks, the number of inductors in smartphones is growing significantly. Inductors enhance various smartphones' functions, including improving color LCD and battery life.

- Smartphone OEMs are ramping up Artificial intelligence-enabled smartphones in 2024, with generative AI capabilities and an additional storage capacity, which creates demand for better battery life. Further, with the advancement in technology, consumers prefer advanced technology products compared to older devices, which drives the sales of smartphones.

- The need for inter-country power grid connections (super grid) and renewable energy sources based on direct currents, such as fuel cells, wind power, and solar power, is expanding globally, as is the demand for magnetic components.

- Traditionally, transformers were made of solid iron; however, with the development of materials, silicon steel, amorphous steel, and ferrite ceramics have been used as core materials for transformers due to their higher penetrability. Similarly, inductors and EMI filters use iron, ferrite, and other magnetic materials as core material, and coils are usually made of copper.

- With the current rapid evolution of autonomous driving technologies and ADAS, automobiles are prepared with numerous sensors such as radars, cameras, and LiDAR, resulting in dramatic growth in magnetic components. Owing to ongoing advancement in automotive sector, key vendors are continuously investing on product developments and advancement to meet consumer demand.

- For instance, in January 2024, TDK Corporation launched a new inductor KLZ2012-A series, designed for automotive audio bus (A2B) applications with high durability, a wide operation range, and greater inductance tolerance. The company announced that the mass production of these new product series started in January 2024. A2B technology was developed to decrease the weight of cable harnesses containing of a broad variety of telecommunication buses, pointing at its final goal of amplified fuel efficiency of automobiles.

Magnetics Market Trends

Industrial (Motors/UPS) to Witness the Growth

- Industrial motors are electrical devices that convert electrical energy into mechanical energy. They are commonly powered by alternating current (AC) sources like generators and power grids. Industrial motors are specifically engineered to supply power and movement to various equipment and machinery utilized in different industries. Due to their requirement to endure heavy loads and function in challenging environments, these motors are typically more durable and potent than those employed in residential or commercial settings. The growing need for magnetic inductance in industrial motor applications will drive the market.

- The Industrial Energy Accelerator reports that a significant portion of the global electrical energy consumed by companies is attributed to the millions of electrical motors in operation. These motors are crucial in powering essential industrial processes and auxiliary systems such as ventilation, compressed air generation, and water pumping across various sectors. Additionally, there has been a recent introduction of universal motors in the industrial motors market, designed to work with both AC and DC power sources. The increasing demand for these motors and growing developments by the various vendors will increase the applications of magnetic components.

- The design and functioning of industrial motors heavily rely on magnetic induction, which serves as the primary method for producing torque. Engineers can develop efficient and high-performing motors suitable for various applications by thoroughly comprehending magnetic induction principles and optimizing different design elements.

- The demand for data center uninterruptable power supply (UPS) systems is experiencing significant growth due to the increasing investments in data centers. As various industries expand their digital operations and services, there is a surge in demand for data storage, processing, and management. Consequently, substantial investments are being made in data center infrastructure to meet these requirements. According to Cloudscene, as of September 2023, there were 448 data centers in China, the most of any country or territory in the Asia-Pacific region, where market opportunities can be found significantly.

China to Witness Rapid Growth

- The demand for passive electronics is expected to remain strong in the forecast period due to increased consumer electronics, automotive, and medical equipment production in China.

- According to Rayming PCB and Assembly, China has continued dominating the electronics manufacturing industry for some years. This country is an integral manufacturing place for electronics despite its recent trade with the United States. As a large manufacturing company, China exports about 50% of laptops and cell phones globally.

- The global electronics market grew from USD 3554.94 billion in 2022 to USD 3739.37 billion in 2023. In the global electronics sector, China contributes a large percentage of revenue. This country is ranked among the top producers of electronic devices. It produces various electronics products, ranging from consumer electronics to industrial components. Cities such as Dongguan and Shenzhen in the South have factories. In addition, Shanghai and Choingun are home to factories.

- China produces a prominent share of laptop manufacturers globally. Despite China's dependence on imported semiconductors, this country remains a good option for many world-class laptop brands. Kunshan and Chongqing are the two biggest clusters for laptop manufacturing and other popular electronic production hubs, like Dongguan and Shenzhen. These hubs are known for producing laptops, components, and accessories.

- The country also holds a significant consumer market considering the country's large population, with about 160 Chinese cities having a population crossing one million people, compared to the US, having only nine cities that incorporate more than one million people. Thus, the growing electronics manufacturing and consumption are expected to drive the need for various passive components to address electric flow management in all consumer and household electronics.

- China's initiatives targeting the EV industry over the past 15 years are one of the most successful cases of industrial policy in the country's recent history. Extensive government interventions, including subsidies, enabled the domestic industry and the market to grow simultaneously. The timing of the policies was crucial because they coincided with and magnified technological advancements in battery technology and greater consumer acceptance of EVs. Importantly, many existing automotive companies dismissed EV technology until recently.

- Meanwhile, their Chinese competitors quickly grasped the opportunity to technologically leapfrog multinational corporations with decades of IP accumulated in internal combustion engine technology. China is also by far the main producer of lithium batteries globally, which are the main component in EVs. According to the International Energy Agency (IEA), the country accounts for 65% of battery and 80% of cathode production, and the Department of Energy's estimate is even higher. Thus, the growing prospect of the market studied in the country's automotive sector is shown.

Magnetics Industry Overview

The magnetics market is fragmented, comprising long-standing established players who have made significant investments in the product. The new players entering the market require high investments. The companies can sustain themselves through powerful competitive strategies, and key players are TDK Corporation, Yageo Corporation, Meritek Electronics Corporation, AVX Corporation (Kyocera Group), and Vishay Intertechnolo.

* In January 2024, TDK Corporations subsidiary TDK Ventures Inc. invested in Singaporean tech company Silicon Box for digital and energy transformation. It plans to accelerate the market for semiconductor packaging innovations through Silicon Box.

* In November 2023, The Bourns introduced an air coil inductor series with high self-resonant frequency, high Q, and tight inductance tolerance. The Model AC4842R Air Coil Inductor Series offers a low-loss, high-frequency solution that gives RF application designers a wider range of high-Q solution options.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Degree of Competition

- 4.3 Technological overview of Magnetic Device Categories

- 4.4 Assessment of Macro trends in the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Demand For Renewable Energy

- 5.1.2 Rising Demand For Electric and Autonomous Vehicles Drives Magnetic Components Market

- 5.2 Market Challenges

- 5.2.1 Rising Metal Prices Impacting Component Production Costs

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Wire Wound Inductor

- 6.1.2 Multi-layer Inductor

- 6.1.3 Thin Film Inductor

- 6.1.4 Ferrite Cores and EMC Components

- 6.1.5 EMI Filters

- 6.1.6 RF/Power Transformers

- 6.1.7 Current Sense and Other Transformers

- 6.2 By End-user Application

- 6.2.1 Photovoltaics and wind

- 6.2.2 EV/HEV

- 6.2.3 Industrial (Motors/UPS)

- 6.2.4 Rail/Transportation

- 6.2.5 Consumer Electronics

- 6.2.6 Other End-user Applications

- 6.3 By Geography

- 6.3.1 China

- 6.3.2 Japan

- 6.3.3 United States

- 6.3.4 Taiwan

- 6.3.5 South East Asia

- 6.3.6 South Korea

- 6.3.7 Europe

- 6.3.8 Latin America

- 6.3.9 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles*

- 7.1.1 TDK Corporation

- 7.1.2 Yageo Corporation

- 7.1.3 Meritek Electronics Corporation

- 7.1.4 AVX Corporation (Kyocera Group)

- 7.1.5 Vishay Intertechnology

- 7.1.6 Panasonic Corporation

- 7.1.7 Taiyo Yuden Co. Ltd

- 7.1.8 Exxelia Technology

- 7.1.9 Bourns Inc.

- 7.1.10 Wurth Elektronik Group

- 7.1.11 Coilcraft Inc.

8 MARKET OUTLOOK

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 152 Pages

- 納期

- 2~3営業日