日本の自動車ローン:市場シェア分析、産業動向・統計、成長予測(2024年~2029年)

Japan Car Loan - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)- 発行日

- ページ情報

- 英文 145 Pages

- 納期

- 2~3営業日

- 商品コード

- 1521490

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

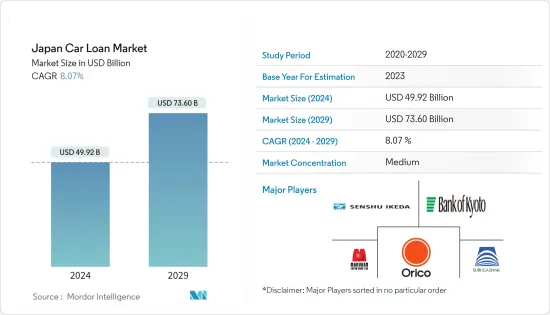

日本の自動車ローン市場規模は2024年に499億2,000万米ドルと推定され、2029年には736億米ドルに達すると予測され、予測期間中(2024-2029年)のCAGRは8.07%で成長すると予測されます。

日本の自動車ローン市場は、公正な融資慣行と消費者保護を確保するため、金融庁(FSA)による規制の対象となっています。日本の自動車ローン市場は、ドライビング・エクスペリエンスを向上させるために旧モデルから新モデルへの買い替えが進み、保有台数が増加しているため、着実な成長を遂げています。日本のマイカーローンは一般に、柔軟なローン期間が設定されており、多くの場合、12ヶ月から84ヶ月となっています。借り手は、経済状況や予算に最も適した期間を選ぶことができます。

日本のデジタル化率は今後上昇することが予想され、オフラインおよびオンライン企業が自動車ローン市場に参入することが予想されます。さらに、フィンテック・プラットフォームの台頭は、エンド・ツー・エンドのデジタル・ローン承認、処理、支払いを可能にすることで、オートローンを簡素化しています。フィンテック業界は、いくつかの方法で世界の金融情勢を根本的に変えつつあります。

自動車ローン・プロバイダーは、人工知能、ビジネス・アナリティクス、ブロックチェーン技術を活用することで、顧客に付加価値サービスを提供することに戦略的に注力しています。商品やサービスの幅を広げることで、これらの企業はサービスの質を高め、顧客満足度を高めることを目指しています。

従来の自動車ローンに加え、消費者が一定期間車両をリースできるリースオプションを提供する金融機関もあります。日本の借り手は、より良い条件を見つけたり、返済スケジュールを調整したい場合、マイカーローンを借り換える選択肢があります。日本の自動車ローン市場は顧客サービスに重点を置いており、ほとんどの金融機関はローンの申し込みから返済プロセスを通じてサポートと支援を提供しています。

日本の自動車ローン市場動向

日本の乗用車市場

乗用車は、マイカーローンの需要を同時に高める可能性が高いです。自動車を購入しようとする消費者は、購入資金の調達に自動車ローンを利用する可能性があり、自動車ローン市場の成長を促進します。金融機関は、自動車購入者の多様なニーズに応えるため、多様なローン商品を導入する可能性があります。柔軟な返済条件、競争力のある金利、特別キャンペーンなど、差別化されたローン商品が登場し、幅広い顧客を惹きつける可能性があります。自動車販売の増加は、自動車ローン市場におけるデジタル技術の採用を加速させる。金融機関はローン処理、承認、管理のためのデジタル・プラットフォームに投資し、顧客に便利で効率的なオンライン体験を提供します。金融機関は自動車ディーラーと提携し、統合された融資ソリューションを提供します。こうした提携は、自動車購入プロセスを合理化し、顧客にシームレスな体験を提供することで、自動車ローンの魅力を高める可能性があります。

日本市場における電気自動車販売の増加

電気自動車の人気の高まりは、「グリーン」または環境にやさしい自動車ローン・オプションへの需要の増加につながる可能性があります。金融機関は、電気自動車の普及を促進するために、有利な条件の専門ローン商品を導入する可能性があります。金融機関は、電気自動車購入者に特化した差別化されたローン商品を開発するかもしれないです。これらの商品には、消費者が従来の自動車よりも電気自動車を選ぶことを奨励するために、低金利、返済期間の延長、または特別なインセンティブが含まれる可能性があります。政府と金融機関が協力して、電気自動車を購入する消費者にインセンティブや補助金を提供することも考えられます。こうしたインセンティブは、金利の引き下げ、税額控除、またはよりクリーンな交通手段の採用を促進するためのその他の金融特典という形で提供される可能性があります。金融機関は電気自動車メーカーと提携し、共同融資プログラムを提供します。こうした提携は、電気自動車を購入する消費者にとって、独占的なローン取引、割引、その他の特典につながる可能性があります。

日本の自動車ローン業界の概要

日本の自動車ローン市場の競合情勢は多様であり、様々な金融機関や貸金業者が消費者に様々なローン商品を提供しています。競争力は、オンライン・ローン・プラットフォーム、テレマティクス・ベースのローン商品、エコカーに合わせたオプションなど、市場のイノベーションを推進してきました。金融機関が提供する顧客サービスとサポートの質は、競合情勢における重要な差別化要因となりうる。日本では、リース会社がリースと自動車ローンの選択肢を提供し、消費者に自動車の資金調達方法に柔軟性を与えています。以下は、同市場で事業を展開する主要企業である:スルガ銀行、オリエントコーポレーション、京都銀行、マルハンジャパン銀行、池田泉州銀行など。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学と洞察

- 市場概要

- 市場促進要因

- 自動車に対する消費者需要の増加

- 市場抑制要因

- 信用市場の状況

- 市場機会

- 革新的で柔軟なローン商品の提供

- 市場におけるテクノロジーの影響に関する洞察

- 業界の魅力- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- COVID-19の市場への影響

第5章 市場セグメンテーション

- 自動車タイプ別

- 乗用車

- 商用車

- 所有者別

- 新車

- 中古車

- 業者タイプ別

- 銀行

- NBFC(非銀行系金融会社)

- 信用組合

- その他(フィンテック企業)

- 契約期間別

- 3年未満

- 3~5年

- 5年以上

第6章 競合情勢

- 市場集中度の概要

- 企業プロファイル

- SURUGA bank Ltd.

- Orient Corporation

- Bank of Kyoto, Ltd.

- MARUHAN Japan Bank Lao Co., Ltd.

- The Senshu Ikeda Bank, Ltd.

- Toyota Financial Services Corporation

- The Kinokuni Shinkin Bank

- Sompo Japan Insurance Inc

- AK Kogyo Co., Ltd.

- The 77 bank, Ltd.*

第7章 市場動向

第8章 免責事項および出版社について

目次

The Japan Car Loan Market size is estimated at USD 49.92 billion in 2024, and is expected to reach USD 73.60 billion by 2029, growing at a CAGR of 8.07% during the forecast period (2024-2029).

The car loan market in Japan is subject to regulation by the Financial Services Agency (FSA) to ensure fair lending practices and consumer protection. Japan's car loan market is experiencing steady growth due to an increase in the number of vehicles owned as people replace older models with newer models to improve their driving experience. Car loans in Japan generally come with flexible loan terms, often ranging from 12 to 84 months. Borrowers can choose the term that best suits their financial situation and budget.

Japan's digitalization rate is expected to increase in the future, and offline and online companies are expected to enter the auto loan market. Additionally, the rise of fintech platforms is simplifying auto loans by enabling end-to-end digital loan approval, processing, and disbursements. The fintech industry is fundamentally changing the global financial landscape in several ways.

Car loan providers strategically focus on delivering value-added services to their clientele by harnessing artificial intelligence, business analytics, and blockchain technologies. Expanding their products and services range, these companies aim to elevate service quality and enhance customer satisfaction.

In addition to traditional car loans, some lenders offer leasing options, allowing consumers to lease a vehicle for a fixed period. Borrowers in Japan have the option to refinance their car loans if they find better terms or want to adjust their repayment schedules. The Japanese car loan market places a strong emphasis on customer service, with most lenders providing support and assistance throughout the loan application and repayment process.

Japan Car Loan Market Trends

Passenger Cars in Japan Market

Passenger cars are likely to be a concurrent rise in the demand for car loans. Consumers seeking to purchase vehicles may turn to car loans to finance their purchases, driving growth in the car loan market. Financial institutions may introduce diverse loan products to cater to the varying needs of car buyers. Differentiated loan offerings, such as flexible repayment terms, competitive interest rates, and special promotions, could emerge to attract a broader range of customers. The increase in car sales accelerates the adoption of digital technologies in the car loan market. Financial institutions invest in digital platforms for loan processing, approval, and management, providing customers with convenient and efficient online experiences. Financial institutions establish partnerships with car dealerships to provide integrated financing solutions. These collaborations can streamline the car-buying process and offer customers a seamless experience, potentially increasing the appeal of car loans.

Rising Sales of Electric Vehicles in Japan Market

The growing popularity of electric vehicles may lead to increased demand for "green" or environmentally friendly auto financing options. Financial institutions may introduce specialized loan products with favorable terms to incentivize the adoption of electric vehicles. Financial institutions might develop differentiated loan products specifically tailored to electric vehicle buyers. These products could include lower interest rates, extended repayment periods, or special incentives to encourage consumers to choose electric over traditional vehicles. Governments and financial institutions may collaborate to offer incentives or subsidies for customers purchasing electric vehicles. These incentives could come in the form of reduced interest rates, tax credits, or other financial perks to promote the adoption of cleaner transportation options. Financial institutions form partnerships with electric vehicle manufacturers to provide joint financing programs. These collaborations can lead to exclusive loan deals, discounts, or other benefits for consumers purchasing electric cars.

Japan Car Loan Industry Overview

The competitive landscape of the car loan market in Japan is diverse, with various financial institutions and lenders offering a range of loan products to consumers. Competitive forces have driven innovations in the market, Such as online loan platforms, telematics-based loan products, and options tailored to eco-friendly vehicles. The quality of customer service and support offered by lenders can be a significant differentiator in the competitive landscape. In Japan, Leasing companies provide leasing and car loan options, giving consumers flexibility in how they finance their vehicles. The following are the major companies operating in the market: SURUGA Bank Ltd, Orient Corporation, Bank of Kyoto, Ltd, MARUHAN Japan Bank Lao Co., Ltd, The Senshu Ikeda Bank, Ltd, etc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS AND INSIGHTS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Consumer Demand for Vehicles

- 4.3 Market Restraints

- 4.3.1 Credit Market Conditions

- 4.4 Market Opportunities

- 4.4.1 Offering innovative and flexible loan products

- 4.5 Insights on impact of technology in the Market

- 4.6 Industry Attractiveness - Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Impact of COVID-19 on the Market

5 MARKET SEGMENTATION

- 5.1 By Vehicle Type

- 5.1.1 Passenger Vehicle

- 5.1.2 Commercial Vehicle

- 5.2 By Ownership

- 5.2.1 New Vehicles

- 5.2.2 Used Vehicles

- 5.3 By Provider Type

- 5.3.1 Banks

- 5.3.2 NBFCs (Non Banking Financials Companies)

- 5.3.3 Credit Unions

- 5.3.4 Other Provider Types (Fintech Companies)

- 5.4 By Tenure

- 5.4.1 Less than Three Years

- 5.4.2 3-5 Years

- 5.4.3 More Than 5 Years

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration Overview

- 6.2 Company Profiles

- 6.2.1 SURUGA bank Ltd.

- 6.2.2 Orient Corporation

- 6.2.3 Bank of Kyoto, Ltd.

- 6.2.4 MARUHAN Japan Bank Lao Co., Ltd.

- 6.2.5 The Senshu Ikeda Bank, Ltd.

- 6.2.6 Toyota Financial Services Corporation

- 6.2.7 The Kinokuni Shinkin Bank

- 6.2.8 Sompo Japan Insurance Inc

- 6.2.9 AK Kogyo Co., Ltd.

- 6.2.10 The 77 bank, Ltd.*

7 MARKET FUTURE TRENDS

8 DISCLAIMER AND ABOUT US

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 145 Pages

- 納期

- 2~3営業日