|

市場調査レポート

商品コード

1521417

空港用除雪車両および機器:市場シェア分析、産業動向、成長予測(2024~2029年)Airport Snow Removal Vehicle And Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 空港用除雪車両および機器:市場シェア分析、産業動向、成長予測(2024~2029年) |

|

出版日: 2024年07月15日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

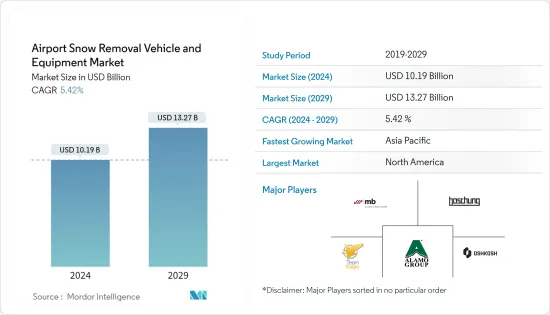

空港用除雪車両および機器市場規模は2024年に101億9,000万米ドルと推定され、2029年には132億7,000万米ドルに達すると予測され、予測期間(2024-2029年)のCAGRは5.42%で成長する見込みです。

主なハイライト

- 世界中の空港で、信頼性が高く効果的な除雪ソリューションへの需要が高まっていることが、主に市場を牽引しています。航空交通量の増加とそれに伴う飛行回数の増加により、さまざまな気象条件下での空港運営を管理するための高度な除雪車両の必要性が高まっています。

- さらに、滑走路の整備や運用効果に関して航空当局が課す厳しい安全要件が、市場の成長を後押ししています。空港の除雪設備は高価で、メンテナンス費用が高いことが、拡大する市場の主な制約の一つです。航空会社の運航の中断や機体の腐食も市場を制限する可能性があります。

- GPSシステム、温度センサー、自動除雪システムにおける材料使用量の向上といった高度な技術の統合も、市場の拡大に寄与しています。除雪作業における性能と精度の向上により、空港は悪天候による混乱を最小限に抑えようと努力しています。

空港用除雪車両の市場動向

予測期間中、国内空港が市場の優位性を維持

- 国内空港セグメントは、主に国内の国内便を扱う空港の除雪ニーズに対応します。同セグメントは、空港インフラの拡張と航空需要の増加が除雪装置の改良ニーズにつながっているインドやブラジルなどの新興経済国で大きな成長が見込まれています。国内空港の総数は国際空港に比べて多いです。

- オペレータの安全性を向上させ、作業効率を高める自律型または遠隔操作型の除雪機器へのニーズが高まっています。2022年9月、シュトゥットガルト空港は自律型除雪車両の配備を開始しました。AirfieldPilotは掃雪ブロワーで、運転手なしで滑走路、誘導路、エプロンの雪や氷を除去することができます。Aebi Schmidt Group(ASG)とFlughafen GmbHは、シュトゥットガルト空港に自律型除雪車両と装置を配備しました。

- 最も革新的な除雪技術としては、滑走路のコンディションの将来を予測するBoschung社の氷早期警告システムや、ストックホルムとオスロの空港に納入されたYeti Move社の自律除雪車があります。オスロ空港では、2022-23年以降、全12台が自力で稼動しています。国内航空業界の大幅な拡大と、航空機のスムーズな発着を確保するために誘導路の氷を除去する技術的に高度な除雪装置へのニーズの高まりが、市場成長を促進する主な要因となっています。

予測期間中、北米が市場シェアを独占

- 航空会社は、2022年に少なくとも1つの北米空港を含む650以上の新規路線を開設し、2021年には、北米(カナダと米国を含む)の空港を含む1,200以上の新規路線が航空会社によって開設され、そのうち約890は新規の米国内路線でした。このように、航空会社が増加する航空旅客数を取り込むために接続性を高めることを目指す中、空港インフラは重要な役割を果たす可能性があります。

- 航空旅客の急増に伴い、航空会社の機材拡大計画をサポートするための新たな空港やターミナルの必要性が高まっています。2022年7月、米連邦航空局は、現米国政府によって可決されたインフラ法の一環として、10億米ドルの資金を管理する計画を発表しました。2022年11月には、FAAの空港改善計画のもと、28州85空港が空港運営を安全かつ円滑に維持するための準備を整えました。米国運輸省連邦航空局は2022年度、除雪車、除氷装置、およびこれらの装置を保管するための建物の新設・改修のために7,620万米ドル以上を支給しました。このプログラムでは、空港施設の新設や改良、滑走路や誘導路の補修、照明や標識などの飛行場要素の整備など、さまざまなプロジェクトに費用が支払われます。

- 同様に、カナダ政府は2022年3月、セント・ジョンズ国際空港の重要インフラ・プロジェクトに2,200万米ドルの新規資金を提供しました。増加する航空旅客輸送量を処理するための北米の空港における航空インフラに対する需要の存在は、市場を支援すると予想されます。

空港用除雪車産業の概要

同市場は、以下のような主要企業が存在する半固有市場です。 M-B Companies, Boschung Holding AG, Alamo Group Inc., Team Eagle Ltd., and Oshkosh Corporation. Key players are engaging in strategic partnerships and collaborations to expand their product portfolios and market presence. Technological innovation remains a key driver for gaining a competitive advantage.

各社は、最先端の効率的で環境に優しい除雪ソリューションを開発するため、研究開発に多額の投資を行っています。空港用除雪車市場は、主要プレイヤーの統合によって特徴付けられ、中小プレイヤーはニッチセグメントに集中するか、この競争の激しい業界で競争力を得るためにチームを組むことを余儀なくされています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の成果

- 調査の前提

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- バリューチェーン/サプライチェーン分析

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 製品

- 送風機

- 除氷装置

- ローダー

- 回転ほうきと散布車

- 散布機

- 用途

- 海外

- 国内

- 地域

- 北米

- 米国

- カナダ

- 欧州

- 英国

- フランス

- ドイツ

- スペイン

- その他欧州

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- メキシコ

- その他ラテンアメリカ

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

- その他中東とアフリカ

- 北米

第6章 競合情勢

- ベンダー市場シェア

- 企業プロファイル

- M-B Companies Inc.

- Oshkosh Corporation

- Alamo Group Inc.

- Kiitokori Oy

- Team Eagle Ltd.

- Boschung Holding AG

- Aebi Schmidt Holding AG

- Kodiak America

第7章 市場機会と今後の動向

The Airport Snow Removal Vehicle And Equipment Market size is estimated at USD 10.19 billion in 2024, and is expected to reach USD 13.27 billion by 2029, growing at a CAGR of 5.42% during the forecast period (2024-2029).

Key Highlights

- The growing demand for dependable and effective snow removal solutions in airports around the world mainly drives the market. The growth in air traffic and the resulting increase in flight frequency have increased the need for sophisticated snow removal vehicles to manage airport operations in different weather conditions.

- Furthermore, stringent safety requirements imposed by aviation authorities concerning runway maintenance and operational effectiveness are driving the growth of the market. The airport snow removal equipment is expensive with a high maintenance cost is one of the main limitations of the expanding market. The disruption of the airline operations and the corrosion of the airframes may also limit the market.

- The integration of sophisticated technologies such as GPS systems, temperature sensors, and enhanced material usage in automatic snow removal systems also contribute to the expansion of the market. With improved performance and accuracy in snow removal operations, airports strive to minimize disruption caused by bad weather.

Airport Snow Removal Vehicles Market Trends

Domestic Airports to Continue Market Dominance During the Forecast Period

- The domestic airport segment caters to snow removal needs at airports that primarily handle domestic flights within a country. The segment is expected to witness significant growth in emerging economies such as India and Brazil, where the expansion of airport infrastructure and increasing air travel demand are driving the need for improved snow removal equipment. The total number of domestic airports is more when compared to international airports.

- There is an increasing need for autonomous or remote-controlled snow removal equipment that improves operator safety and enhances operational efficiency. In September 2022, the airport of Stuttgart started the deployment of autonomous snow-clearing vehicles. The AirfieldPilot is a sweeping blower and can be used to clear the snow and ice from the runways, the taxiways, and the aprons without the need for a driver. Aebi Schmidt Group (ASG) and Flughafen GmbH deployed autonomous snow-clearing vehicles and equipment at the airport Stuttgart.

- Some of the most innovative snow clearance technologies are Boschung's ice early warning system, which forecasts the future of runway conditions, and Yeti Move's autonomous snowploughs, which have been delivered to the airports in Stockholm and Oslo. All 12 units in Oslo Airport have been operating on their own since 2022-23. The considerable expansion in the domestic aviation industry and the rising need for technologically advanced snow removal equipment to remove ice from taxiways to ensure smooth arrival and departure of aircraft are major factors driving the market growth.

North America to Dominate Market Share During the Forecast Period

- The airlines launched over 650 new routes involving at least one North American airport in 2022, and in 2021, over 1,200 new routes were launched by airlines, including airports in North America (comprising Canada and the US), of which about 890 were new US domestic routes. Thus, as airlines aim to increase connectivity to capture the growing air passenger traffic, airport infrastructure may play a vital role.

- With the rapid growth in air travel, there is a significant need for new airports and terminals to support the fleet expansion plans of airlines. In July 2022, the Federal Aviation Administration announced its plans to administer USD 1 billion in funds as part of the Infrastructure Law passed by the current US government. Under the FAA's Airport Improvement Programme, in November 2022, 85 airports in 28 states were better prepared to keep airport operations running safely and smoothly. The US Department of Transportation's Federal Aviation Administration has awarded more than USD 76.2 million in FY2022 for snowplows, de-icing equipment, and new or upgraded buildings to store this equipment. The program pays for a variety of projects, including the construction of new and improved airport facilities, repairs to runways and taxiways, and maintenance of airfield elements such as lighting or signage.

- Similarly, in March 2022, the Canadian government provided USD 22 million in a new funding round for a critical infrastructure project at St. John's International Airport. The presence of demand for aviation infrastructure in North American airports to handle the increasing air passenger traffic is expected to aid the market.

Airport Snow Removal Vehicles Industry Overview

The market is semi-consolidated in nature with a presence of major players such as M-B Companies, Boschung Holding AG, Alamo Group Inc., Team Eagle Ltd., and Oshkosh Corporation. Key players are engaging in strategic partnerships and collaborations to expand their product portfolios and market presence. Technological innovation remains a key driver for gaining a competitive advantage.

Companies are investing heavily in R&D to develop cutting-edge, efficient, and eco-friendly snow removal solutions. The airport snow removal vehicle market is characterized by the consolidation of key players, which forces smaller players to concentrate on niche segments or team up to gain a competitive edge in this highly competitive industry.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Value Chain / Supply Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers/Consumers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Product

- 5.1.1 Blowers

- 5.1.2 De-Icers

- 5.1.3 Loaders

- 5.1.4 Rotary Brooms and Sprayer Trucks

- 5.1.5 Spreaders

- 5.2 Application

- 5.2.1 International

- 5.2.2 Domestic

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.2 Europe

- 5.3.2.1 United Kingdom

- 5.3.2.2 France

- 5.3.2.3 Germany

- 5.3.2.4 Spain

- 5.3.2.5 Rest of Europe

- 5.3.3 Asia Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 Latin America

- 5.3.4.1 Brazil

- 5.3.4.2 Mexico

- 5.3.4.3 Rest of Latin America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 South Africa

- 5.3.5.4 Rest of Middle-East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 M-B Companies Inc.

- 6.2.2 Oshkosh Corporation

- 6.2.3 Alamo Group Inc.

- 6.2.4 Kiitokori Oy

- 6.2.5 Team Eagle Ltd.

- 6.2.6 Boschung Holding AG

- 6.2.7 Aebi Schmidt Holding AG

- 6.2.8 Kodiak America