|

|

市場調査レポート

商品コード

1485292

トランスサイレチンアミロイドーシス治療薬市場- タイプ別、疾患タイプ別、薬剤タイプ別、投与経路別、流通チャネル別-2024年~2032年の世界予測Transthyretin Amyloidosis Treatment Market - By Type, Disease Type, Drug Type, Route of Administration, Distribution Channel - Global Forecast 2024 - 2032 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| トランスサイレチンアミロイドーシス治療薬市場- タイプ別、疾患タイプ別、薬剤タイプ別、投与経路別、流通チャネル別-2024年~2032年の世界予測 |

|

出版日: 2024年03月13日

発行: Global Market Insights Inc.

ページ情報: 英文 170 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

トランスサイレチンアミロイドーシス治療薬市場規模は、医学研究と技術の進歩に牽引され、2024年から2032年の間にCAGR 7.5%を記録すると予想されています。

最近、いくつかの治療技術革新が、病気の進行を止め、患者の転帰を改善するという有望な結果をもたらしています。トランスサイレチン型アミロイドーシスの認知度や診断率は、特に高齢化が進む地域で高まっており、市場拡大に寄与するものと思われます。例えば、遺伝性トランスサイレチンを介した(hATTR)アミロイドーシスの世界の発生は、罹患した臓器によって多様な症状を示し、およそ50,000人が罹患すると考えられています。

さらに、製薬会社と研究機関との間で、専門知識とリソースを結集して創薬プロセスを加速させ、新薬や治療法の開発を促進するための共同研究も行われています。新規治療に対する規制当局の承認が進み、トランスサイレチンアミロイドーシス治療薬に対する保険償還の対象が拡大することで、治療選択肢へのアクセス性がさらに高まると思われます。

トランスサイレチンアミロイドーシス治療薬業界は、タイプ、疾患タイプ、薬剤タイプ、投与経路、流通チャネル、地域に分けられます。

投与経路に関しては、非経口投与セグメントの市場規模は2024年から2032年の間にCAGR 7.8%を記録すると予測されます。非経口投与は、経口投与に伴う消化管での分解やばらつきを回避し、迅速かつ安定した薬物吸収を保証します。胃腸症状や吸収不良の問題をしばしば経験するトランスサイレチンアミロイドーシス患者にとって、非経口投与は治療薬を効果的に送達する信頼性の高い手段となります。

販売チャネル別では、オンライン薬局セグメントによるトランスサイレチンアミロイドーシス治療薬市場は、2032年まで8%の成長率を記録します。これらのチャネルは、トランスサイレチンアミロイドーシス治療薬薬を含む処方薬や専門治療薬を、自宅に居ながらにして購入できる便利なプラットフォームを提供しています。このアクセスのしやすさは、遠隔地に住む患者や、従来の実店舗型薬局へのアクセスに課題を抱える移動制限のある患者にとって特に有益です。

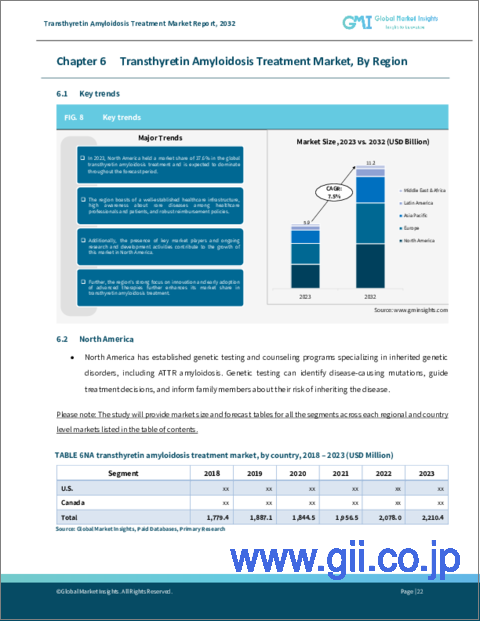

欧州のトランスサイレチンアミロイドーシス治療薬市場規模は2032年までCAGR 7.8%を示すと予想されるが、これはヘルスケアインフラへの投資と希少疾患に焦点を当てた研究イニシアチブの増加によるものです。欧州諸国はヘルスケアの進歩を優先し、革新的な治療法や治療方法を支援するために多額のリソースを割り当てています。さらに、規制当局は希少疾病用医薬品の開発を奨励するため、迅速な承認パスウェイとインセンティブを導入しており、この地域の産業拡大をさらに刺激しています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 業界への影響要因

- 促進要因

- トランスサイレチンアミロイドーシスの有病率の増加

- 新規治療法の開発

- 老年人口の増加

- 診断技術の進歩

- 業界の潜在的リスク&課題

- 限られた治療選択肢

- 高額な治療費

- 促進要因

- 成長可能性分析

- 規制状況

- パイプライン分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業マトリックス分析

- 企業シェア分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:タイプ別、2018年~2032年

- 主要動向

- 多発性神経障害を伴うATTRアミロイドーシス(ATTR-PN)

- 心筋症を伴うATTRアミロイドーシス(ATTR-CM)

第6章 市場推計・予測:疾患タイプ別、2018年~2032年

- 主要動向

- 遺伝性トランスサイレチンアミロイドーシス

- 多発性神経炎

- 心筋症

- 混合型

- 野生型トランスサイレチンアミロイドーシス

第7章 市場推計・予測:薬剤タイプ別、2018年~2032年

- 主要動向

- タファミジス

- パティシラン

- イノターゼン

- その他の薬剤タイプ

第8章 市場推計・予測:投与経路別、2018年~2032年

- 主要動向

- 経口剤

- 非経口

第9章 市場推計・予測:流通チャネル別、2018年~2032年

- 主要動向

- 病院薬局

- 小売ドラッグストア

- オンライン薬局

第10章 市場推計・予測:地域別、2018年~2032年

- 主要動向:地域別

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- その他欧州

- アジア太平洋

- 日本

- 中国

- インド

- オーストラリア

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- メキシコ

- その他ラテンアメリカ

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- その他中東とアフリカ

第11章 企業プロファイル

- Acrotech Biopharma, LLC

- Alnylam Pharmaceuticals, Inc.

- AstraZeneca PLC

- Astellas Pharma Inc.

- BridgeBio Pharma, Inc.

- Bristol-Myers Squibb Company

- Ionis Pharmaceuticals, Inc.

- Johnson & Johnson

- Prothena Biosciences Limited

- Pfizer Inc.

- SOM Innovation Biotech, S.L.

Transthyretin amyloidosis treatment market size is expected to witness 7.5% CAGR between 2024 and 2032, driven by the advancements in medical research and technologies. Lately, several therapeutic innovations are offering promising outcomes in halting disease progression and improving patient outcomes. The increasing awareness and diagnosis rate of transthyretin amyloidosis, particularly in regions with aging population will contribute to the market expansion. For instance, the worldwide occurrence of hereditary transthyretin-mediated (hATTR) is likely to affect roughly 50,000 individuals, showcasing diverse symptoms depending on the organs affected.

Moreover, there have also been collaborations between pharmaceutical companies and research institutions to facilitate the development of new drugs and therapies by leveraging combined expertise and resources to accelerate the discovery process. Growing regulatory approvals for novel treatments and the expansion of reimbursement coverage for transthyretin amyloidosis therapies will further enhance the accessibility of treatment options.

The transthyretin amyloidosis treatment industry is divided into type, disease type, drug type, route of administration, distribution channel, and region.

With respect to route of administration, the market size from the parenteral segment is slated to depict 7.8% CAGR between 2024 to 2032, due to the efficacy and convenience in delivering therapeutic agents directly into the bloodstream. Parenteral method ensures rapid and consistent drug absorption, bypassing gastrointestinal degradation and variability associated with oral administration. For patients with transthyretin amyloidosis, who often experience gastrointestinal symptoms and malabsorption issues, parenteral administration offers a reliable means of delivering therapeutic agents effectively.

Based on distribution channel, the transthyretin amyloidosis treatment market from the online pharmacy segment will record 8% growth rate through 2032. These channels provide a convenient platform for individuals to purchase prescription medications and specialty treatments, including those for transthyretin amyloidosis, from the comfort of their homes. This accessibility is particularly beneficial for patients residing in remote areas and those with mobility limitations, who may face challenges accessing traditional brick-and-mortar pharmacies.

Europe transthyretin amyloidosis treatment market size will exhibit 7.8% CAGR through 2032, attributed to increasing investments in healthcare infrastructure and research initiatives focused on rare diseases. European countries are prioritizing healthcare advancements and allocating substantial resources to support innovative therapies and treatment modalities. Additionally, regulatory agencies have implemented expedited approval pathways and incentives to encourage the development of orphan drugs, further stimulating the regional industry expansion.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Data collection

- 1.4 Forecast parameters

- 1.5 Data validation

- 1.6 Data sources

- 1.6.1 Primary

- 1.6.2 Secondary

- 1.6.2.1 Paid sources

- 1.6.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry 360 degree synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of transthyretin amyloidosis cases

- 3.2.1.2 Development of novel therapies

- 3.2.1.3 Rising geriatric population

- 3.2.1.4 Advancements in diagnostics techniques

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Limited treatment options

- 3.2.2.2 High cost of treatment

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Pipeline analysis

- 3.6 Porter's analysis

- 3.6.1 Supplier power

- 3.6.2 Buyer power

- 3.6.3 Threat of new entrants

- 3.6.4 Threat of substitutes

- 3.6.5 Industry rivalry

- 3.7 PESTEL analysis

Chapter 4 Competitive Landscape, 2023

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.4 Competitive positioning matrix

- 4.5 Strategic dashboard

Chapter 5 Market Estimates and Forecast, By Type, 2018 - 2032 ($ Mn)

- 5.1 Key trends

- 5.2 ATTR amyloidosis with polyneuropathy (ATTR-PN)

- 5.3 ATTR amyloidosis with cardiomyopathy (ATTR-CM)

Chapter 6 Market Estimates and Forecast, By Disease Type, 2018 - 2032 ($ Mn)

- 6.1 Key trends

- 6.2 Hereditary transthyretin amyloidosis

- 6.2.1 Polyneuropathy

- 6.2.2 Cardiomyopathy

- 6.2.3 Mixed type

- 6.3 Wild type transthyretin amyloidosis

Chapter 7 Market Estimates and Forecast, By Drug type, 2018 - 2032 ($ Mn)

- 7.1 Key trends

- 7.2 Tafamidis

- 7.3 Patisiran

- 7.4 Inotersen

- 7.5 Other drug types

Chapter 8 Market Estimates and Forecast, By Route of Administration, 2018 - 2032 ($ Mn)

- 8.1 Key trends

- 8.2 Oral

- 8.3 Parenteral

Chapter 9 Market Estimates and Forecast, By Distribution Channel, 2018 - 2032 ($ Mn)

- 9.1 Key trends

- 9.2 Hospital pharmacy

- 9.3 Retail drug stores

- 9.4 Online pharmacy

Chapter 10 Market Estimates and Forecast, By Region, 2018 - 2032 ($ Mn)

- 10.1 Key trends, by region

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Rest of Europe

- 10.4 Asia Pacific

- 10.4.1 Japan

- 10.4.2 China

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 Rest of Asia Pacific

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Rest of Latin America

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 Rest of Middle East and Africa

Chapter 11 Company Profiles

- 11.1 Acrotech Biopharma, LLC

- 11.2 Alnylam Pharmaceuticals, Inc.

- 11.3 AstraZeneca PLC

- 11.4 Astellas Pharma Inc.

- 11.5 BridgeBio Pharma, Inc.

- 11.6 Bristol-Myers Squibb Company

- 11.7 Ionis Pharmaceuticals, Inc.

- 11.8 Johnson & Johnson

- 11.9 Prothena Biosciences Limited

- 11.10 Pfizer Inc.

- 11.11 SOM Innovation Biotech, S.L.