|

市場調査レポート

商品コード

1521321

自動車用ポリマーコンポジット:市場シェア分析、産業動向、成長予測(2024~2029年)Automotive Polymer Composites - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 自動車用ポリマーコンポジット:市場シェア分析、産業動向、成長予測(2024~2029年) |

|

出版日: 2024年07月15日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

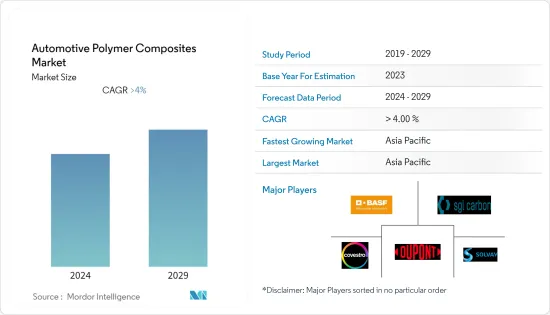

自動車用ポリマーコンポジット市場規模は、2024年には151万トンと推計され、2029年には199万トンに達すると予測され、予測期間中(2024-2029年)のCAGRは5%を超える成長が見込まれています。

COVID-19の大流行は、サプライチェーンを混乱させ、生産の減速や停止、景気後退を引き起こすことによって、自動車用ポリマーコンポジット市場に大きな影響を与えました。残された課題を克服し、市場動向を活用することで、自動車用ポリマーコンポジット市場は、その軽量で高性能な材料で自動車産業に革命を起こし、明るい未来に向かっています。

自動車が軽量化されれば燃費が向上し、汚染物質の排出量も減少するため、世界市場では鉄鋼やアルミニウムといった従来の材料よりも軽量な自動車用ポリマーコンポジットへの需要が高まっています。

その反面、鉄鋼やアルミニウムのような伝統的な材料に比べ、ポリマーコンポジットの加工と製造には複雑で労働集約的な技術が伴うことが多く、コストを押し上げ、自動車用ポリマーコンポジット市場の抑制要因になると予想されます。

ロボット工学、自動化、デジタル化における革新は、ポリマーコンポジットの生産プロセスを合理化し、コストとリードタイムを削減し、世界市場にエキサイティングな可能性をもたらしています。

アジア太平洋地域が市場を独占し、中国、インド、日本、韓国などの国による消費が最も大きいと推定されます。

自動車用ポリマーコンポジット市場の動向

軽自動車セグメントにおけるポリマー使用の増加

- 自動車産業は大きな変革期を迎えており、軽量化が燃費効率と性能向上の重要な原動力となっています。この転換の中で、ポリマーが主役の役割を果たすようになり、軽自動車では鉄鋼やアルミニウムのような従来の材料に取って代わることが増えています。

- 自動車重量は走行ダイナミクスや燃費効率に直接影響するため、自動車業界は何十年も前から車両の軽量化に注力してきました。米国エネルギー省(DOE)によれば、車両重量を10%減らすと燃費が6~8%向上します。世界中の政府が厳しい排ガス規制を実施し、今後数年間でさらに高い排ガス基準を設定する予定であるため、軽量材料の重要性はますます高まると予想されます。

- 自動車に使用される主な複合ポリマーは、ポリプロピレン、ポリウレタン、ナイロン、ポリ塩化ビニル、アクリロニトリル-ブタジエン-スチレン(ABS)などをベースとしています。ポリプロピレンとポリウレタンは、調査対象市場の40%以上を占めるにすぎません。

- 自動車メーカーもプリプレグ(ポリマーコンポジットの一種)を内装・外装部品の金属代替に使用し、軽量化によって性能と安全性を向上させています。近代化と自律走行車の開発が需要を牽引しています。

- カーボン・プリプレグは汎用性が高く、さまざまな密度、形状、サイズに成形できるため、航空業界や自動車業界ではアルミニウムやスチールの代替品として人気があります。BMW、フェラーリ、レクサスなどの大手自動車メーカーは、完全な炭素繊維車体構造を持つ新型車を積極的に設計しています。例えば、2023年5月に発売される第2世代のBMW M2は、ルーフ、インテリア、車両部品など、主にカーボンファイバーでできています。

- レーシングカー・メーカーは、燃費とスピードを向上させるために車体重量を減らしています。米国エネルギー省の報告書によると、車両重量を10%減らすと燃費が6~8%向上するといいます。このため、プリプレグは自動車および輸送業界、特にレース用車両や高速車両で高い人気を誇っています。

- 国際自動車工業会(OICA)によると、2022年の世界の自動車産業は2021年比で6%成長しました。自動車生産は、中国、ドイツ、韓国、カナダ、英国、イタリアなど、世界の先進国および新興諸国で増加しました。2022年には8,500万台以上の自動車が生産されました。

- OICAによると、2022年の小型商用車生産台数は2021年に比べ世界全体で7%増加し、1,986万台となった。生産の大半はアメリカ地域からで、世界中で生産される小型商用車の約60%を占めます。

- さらに、自動車工業会によると、英国の商用車生産台数は2022年に39.3%増(2021年比)の10万1,600台となりました。2022年の国内市場向け生産台数は前年比14.0%増の4万409台で、10万1,600台のバン、トラック、タクシー、バス、コーチが工場のラインから出荷されました。自動車製造活動の増加は、予測期間中の調査対象市場の成長を後押しすると思われます。

- したがって、自動車に占めるプラスチックの割合が増加し、自動車用ポリマーコンポジット市場を押し上げると予想されます。

アジア太平洋地域が市場を独占する見込み

- アジア太平洋地域は、中国、インド、韓国などの国々からの大量消費による需要増加によって大きな市場シェアを占めており、予測期間を通じて自動車用ポリマーコンポジット市場を独占すると予想されます。

- OICAによると、アジア太平洋地域の自動車生産台数は2022年に2021年比で7%増加しました。中国、韓国、インドなどの新興諸国は、2022年に自動車生産が急増しました。アジア太平洋地域では2022年に5,000万台以上の自動車が生産されました。

- さらに、2022年1~9月のインドの乗用車販売は、貯蓄、低金利、パーソナル・モビリティ志向の高まりにより好調を維持し、顧客に新車購入を納得させました。その結果、インドの新車登録台数は2022年第1~3四半期に約20.2%増加し、280万台に達しました。また、「Aatma Nirbhar Bharat」や「Make in India」プログラムといった政府の改革も同国の自動車産業を支えました。

- インド、韓国、中国といったアジア太平洋諸国の政府は、新しい大型トラックやその他の商用車を購入するよう大型トラック所有者に働きかけ、古くて公害を引き起こす商用車の使用を抑制しようとしています。このプログラムは、汚染レベルを下げ、ポリマーコンポジットを採用する大型トラック部門の進歩を促進すると思われます。

- さらに、中国政府は2025年までに電気自動車の普及率を20%にすると予測しています。これは、2022年に過去最高を記録した同国の電気自動車販売動向に反映されています。中国乗用車協会によると、2022年に同国で販売されたEVとプラグインは567万台で、2021年に達成した販売台数のほぼ2倍です。同国では自動車用ポリマーコンポジットの需要拡大が見込まれており、現時点でも販売は継続する構えです。

- 上記の要因や政府による規制が、同地域における自動車用ポリマーコンポジットの需要増加に寄与しています。

自動車用ポリマーコンポジット産業の概要

調査対象市場は、部分的に連結されています。主要企業(順不同)には、BASF SE、SGL Group、Covestro AG、Solvay、DuPontが含まれます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の成果

- 調査の前提

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 軽自動車セグメントにおけるポリマーコンポジットの使用増加

- 電気自動車産業の高成長

- その他の促進要因

- 抑制要因

- 火災リスクと衝突安全性に対する安全上の懸念

- 高い加工・製造コスト

- 業界のバリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション:市場規模(単位:量)

- 樹脂タイプ

- ポリプロピレン

- ポリウレタン

- ナイロン

- ポリ塩化ビニル

- ABS

- ポリエチレン

- ポリカーボネート

- その他樹脂タイプ(ポリエーテルエーテルケトン、ポリエステルなど)

- 車両タイプ

- 乗用車

- 小型商用車

- トラック・バス

- その他の車種(スポーツカー、特殊車両など)

- 地域

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- マレーシア

- タイ

- インドネシア

- ベトナム

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- 英国

- フランス

- ドイツ

- イタリア

- スペイン

- 北欧諸国

- トルコ

- ロシア

- その他欧州

- 南米

- ブラジル

- アルゼンチン

- コロンビア

- その他南米

- 中東・アフリカ

- モロッコ

- 南アフリカ

- ナイジェリア

- カタール

- エジプト

- アラブ首長国連邦

- その他中東とアフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア(%)**/ランキング分析

- 主要企業の戦略

- 企業プロファイル

- BASF SE

- Covestro AG

- DuPont

- Gurit Services AG

- Hexcel Corporation

- Johns Manville

- Kolon Industries

- Mitsubishi Chemical Corporatio

- Owens Corning

- Plasan Sasa Ltd

- Pyrophobic Systems Ltd

- SGL Carbon

- Solvay

- Teijin Carbon

- Toray Advanced Composites

- UFP Technologies Inc.

第7章 市場機会と今後の動向

- 先端製造技術の発展

- 持続可能性と循環型経済への注目

The Automotive Polymer Composites Market size is estimated at 1.51 Million tons in 2024, and is expected to reach 1.99 Million tons by 2029, growing at a CAGR of greater than 5% during the forecast period (2024-2029).

The COVID-19 pandemic significantly impacted the automotive polymer composites market by disrupting the supply chain, causing production to slow down and shut down and an economic downturn. By overcoming the remaining challenges and capitalizing on the market trends, the automotive polymer composites market is poised for a positive future, revolutionizing the automotive industry with its lightweight, high-performance materials.

Lighter vehicles are more fuel-efficient and emit less pollution, which is driving demand for automotive polymer composites in the global market, which are lighter than traditional materials such as steel and aluminum.

On the flip side, compared to traditional materials like steel and aluminum, the processing and manufacturing of polymer composites often involve complex and labor-intensive techniques, driving up costs and is expected to act as a restraint for the automotive polymer composites market.

Innovations in robotics, automation, and digitalization are streamlining composite production processes, reducing costs and lead times, and creating exciting possibilities for the global market.

Asia-Pacific is estimated to dominate the market, with the most significant consumption coming from countries like China, India, Japan, and South Korea.

Automotive Polymer Composites Market Trends

Increasing Use of Polymers in the Light Vehicle Segment

- The automotive industry is undergoing a significant transformation, with lightweight emerging as a critical driver for fuel efficiency and performance improvements. In this shift, polymers are playing a starring role, increasingly replacing traditional materials like steel and aluminum in light vehicles.

- The automotive industry has been focusing on vehicle weight reduction for decades, as vehicle weight has a direct impact on driving dynamics and fuel efficiency. As per the US Department of Energy (DOE), reducing the weight of vehicles by 10% yields an increase of 6-8% in fuel economy. As governments around the world implement stringent emission regulations and plan to set even higher emissions standards in the coming years, the importance of lightweight materials is expected to increase.

- Major composite polymers used in automobiles are based on polypropylene, polyurethanes, nylon, polyvinyl chloride, acrylonitrile-butadiene-styrene (ABS), and others. Polypropylene and polyurethanes only account for more than 40% of the market studied.

- Automakers also use prepregs(a type of polymer composite) to replace metals in interior and exterior parts, reducing weight for better performance and safety. Modernization and autonomous vehicle development drive demand.

- Carbon prepregs are versatile and can be molded into various densities, shapes, and sizes, making them a popular substitute for aluminum and steel in the aviation and automotive industries. Major automakers like BMW, Ferrari, and Lexus are actively designing new models with complete carbon fiber body structures. For example, the second-generation BMW M2, launched in May 2023, is made mainly of carbon fiber, including the roof, interior, and vehicle components.

- Racing car manufacturers reduce curb weight to improve fuel efficiency and speed. According to a US Department of Energy report, a 10% reduction in vehicle weight can improve fuel economy by 6-8%. This makes prepregs highly sought-after in the automotive and transportation industries, especially for racing and high-speed vehicles.

- According to the International Organization of Motor Vehicle Manufacturers (OICA), the global automotive industry grew by 6% in 2022 compared to 2021. Automotive production increased in developed and developing countries worldwide, including China, Germany, South Korea, Canada, the United Kingdom, and Italy. Over 85 million motor vehicles were manufactured in 2022.

- According to OICA, light commercial vehicle production across the world increased in 2022 compared to 2021 by 7%, with 19.86 million units produced in 2022. The majority of the production comes from American regions, with about 60% of the total light commercial vehicles produced across the world.

- Moreover, according to the Society of Motor Manufacturers and Traders, British commercial vehicle production grew by 39.3% (as compared to 2021) to 101,600 units in 2022. The output for the domestic market in 2022 rose by 14.0 percent year-on-year to 40,409 units, with 101,600 vans, trucks, taxis, buses, and coaches leaving factory lines. The increased automotive manufacturing activities would aid the growth of the studied market during the forecast period.

- Hence, an increasing share of plastics in automobiles is expected to boost the automobile polymer composites market.

Asia-Pacific is Expected to Dominate the Market

- The Asia-Pacific region is expected to dominate the automotive polymer composites market throughout the forecast period, with its large market share driven by increasing demand from heavy consumption from countries like China, India, South Korea, and more.

- According to the OICA, motor vehicle production in the Asia-Pacific region grew by 7% in 2022 compared to 2021. Developed and developing countries in the area, such as China, South Korea, and India, experienced an upsurge in automotive production in 2022. Over 50 million motor vehicles were manufactured in the Asia-Pacific region in 2022.

- Furthermore, in the first nine months of 2022, Indian passenger car sales remained strong due to savings, lower interest rates, and an increasing preference for personal mobility, which convinced customers to buy new cars. As a result, new car registrations in India grew by around 20.2% in the first three quarters of 2022 to reach 2.8 million units. Also, government reforms such as "Aatma Nirbhar Bharat" and "Make in India" programs supported the country's automotive industry.

- Under the new scrappage policy, governments in Asia-Pacific countries, like India, South Korea, and China, seek to push heavy-duty truck owners to acquire new heavy-duty trucks and other commercial vehicles, discouraging the use of old, polluting ones. The program would reduce pollution levels and promote the advancements of the heavy trucks segment in adopting polymer composites.

- Moreover, the Chinese government estimates a 20% penetration rate of electric vehicle production by 2025. This is reflected in the country's electric vehicle sales trend, which went to a record-breaking high in 2022. As per the China Passenger Car Association, the country sold 5.67 million EVs and plug-ins in 2022, almost double the sales figures achieved in 2021. The market is anticipated to increase the demand for automotive polymer composites in the country, and sales are poised to continue at this moment.

- The factors above and supportive government regulations are contributing to the increased demand for automotive polymer composites in the region.

Automotive Polymer Composites Industry Overview

The market studied is partially consolidated in nature. The major players (not in any particular order) include BASF SE, SGL Group, Covestro AG., Solvay, and DuPont.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Use of Composite Material in Light Vehicle Segment

- 4.1.2 High Growth of the Electric Vehicles Industry

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Safety Concerns about Fire Risk and Crashworthiness

- 4.2.2 High Processing and Manufacturing Costs

- 4.3 Industry Value-Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size In Volume)

- 5.1 Resin Type

- 5.1.1 Polypropylene

- 5.1.2 Polyurethanes

- 5.1.3 Nylon

- 5.1.4 Polyvinyl Chloride

- 5.1.5 ABS

- 5.1.6 Polyethylenes

- 5.1.7 Polycarbonate

- 5.1.8 Others Resins Type (Polyetheretherketone, Polyester, etc.)

- 5.2 Vehicle Type

- 5.2.1 Passenger Cars

- 5.2.2 Light Commercial Vehicles

- 5.2.3 Trucks and Buses

- 5.2.4 Other Vehicle Types (Sports Cars, Specialty Vehicles, etc.)

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Malaysia

- 5.3.1.6 Thailand

- 5.3.1.7 Indonesia

- 5.3.1.8 Vietnam

- 5.3.1.9 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 United Kingdom

- 5.3.3.2 France

- 5.3.3.3 Germany

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 NORDIC Countries

- 5.3.3.7 Turkey

- 5.3.3.8 Russia

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Morocco

- 5.3.5.2 South Africa

- 5.3.5.3 Nigeria

- 5.3.5.4 Qatar

- 5.3.5.5 Egypt

- 5.3.5.6 UAE

- 5.3.5.7 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 BASF SE

- 6.4.2 Covestro AG

- 6.4.3 DuPont

- 6.4.4 Gurit Services AG

- 6.4.5 Hexcel Corporation

- 6.4.6 Johns Manville

- 6.4.7 Kolon Industries

- 6.4.8 Mitsubishi Chemical Corporatio

- 6.4.9 Owens Corning

- 6.4.10 Plasan Sasa Ltd

- 6.4.11 Pyrophobic Systems Ltd

- 6.4.12 SGL Carbon

- 6.4.13 Solvay

- 6.4.14 Teijin Carbon

- 6.4.15 Toray Advanced Composites

- 6.4.16 UFP Technologies Inc.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Development in Advanced Manufacturing Technologies

- 7.2 Focus on Sustainability and Circular Economy