|

市場調査レポート

商品コード

1519933

重力ダイカスト:市場シェア分析、産業動向・統計、成長予測(2024年~2029年)Gravity Die Casting - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 重力ダイカスト:市場シェア分析、産業動向・統計、成長予測(2024年~2029年) |

|

出版日: 2024年07月15日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

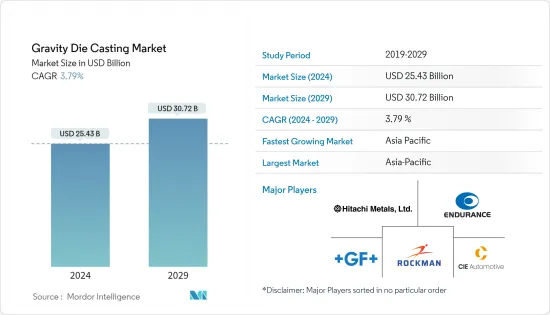

重力ダイカストの市場規模は2024年に254億3,000万米ドルとなり、2029年には307億2,000万米ドルに達すると予測され、予測期間(2024-2029年)のCAGRは3.79%で成長する見込みです。

重力ダイカストは最も古いダイカスト鋳造法のひとつです。このダイカスト鋳造法は、正確な寸法、微細な形状、滑らかな表面、または質感のある表面の金属部品を作るために使用されます。重力ダイカストの基本的な利点は、製造速度が速いことです。再利用可能な金型により、1日に数百個の鋳物を生産することができます。高精細部品は機械加工コストを削減し、高い表面仕上げは仕上げ費用を節約します。

熱伝導率が高いため、予測期間中、電気・電子産業ではアルミダイカスト部品の需要が増加する可能性が高いです。ダイカスト機械は、自動車産業が軽量金属を好むようになり、自動車販売台数が増加した結果、需要が高まっています。

長期的には、再生可能エネルギー発電の市場開拓と家電、コンピュータ、通信産業の急速な拡大から、市場は恩恵を受けると予想されます。

新技術の開発に伴い、自動車部品は最近の動向で進歩と革新を遂げています。なかでも、軽量素材を使った自動車部品製造は、全国的に注目されています。また、CAFE基準やEPA(米国環境保護庁)の自動車排出ガス削減・燃費向上政策の結果、自動車メーカーは軽量非鉄金属を使用して車両の軽量化を図っています。その結果、かつての自動車市場は、軽量化のためのダイカスト部品の使用によって大きな盛り上がりを見せています。

重力ダイカスト市場の動向

自動車産業が主要市場シェアを獲得する見込み

重力ダイカストは、一部の高精密自動車部品を製造するための標準的なプロセスです。このプロセスは、永久金型内での溶融物の高速かつ方向性のある硬化により、魅力的な機械的特性を持つ微細で緻密な構造を生成するため、エンジン関連部品のような部品には理想的です。

しかし、内燃エンジンから電気自動車のような代替エンジンへの動向は、ダイカスト部品の需要に避けられない影響を及ぼしています。例えば、内燃機関には約200個の鋳造部品がありますが、電気駆動系に必要な鋳造部品は約25個、すなわち10分の1に過ぎません。

二酸化炭素排出量の削減、自動車の軽量化を促進する政府の取り組み、自動車用ダイカストマシンの急速な技術開発などの要因が、市場の需要を押し上げると予想されます。

生態学的および経済的要件に後押しされ、世界の自動車産業は、構造ダイカスト部品が大幅な軽量化に役立つ新しいボディ・イン・ホワイト設計を生み出しています。さらに、ダイカスト構造部品の生産は、鋳物への機能組み込み、新しいアルミニウム合金コンセプト、新しい部品設計動向により、さらに増加しています。さらに、乗用車だけでなく商用車の販売台数も伸びており、市場の成長を支えるものと予想されます。

自動車産業は、世界中で使用される鋳造製品の60%以上を消費しています。そのため、自動車・運輸産業に関連する成長機会を考慮し、同市場の複数の企業が製造工場の拡張に注力しています。例えば

- 2022年11月:ゼネラル・モーターズは、電気自動車を生産するメトロ・デトロイトの2つの組立工場に供給するため、インディアナ州ベッドフォードにあるアルミダイカスト鋳造工場の拡張に4,500万米ドルを投資すると発表しました。

- 2022年8月:ステランティスは、ココモ鋳造工場への1,400万米ドルの投資を発表しました。鋳造工場への投資は、既存のダイカストマシンとセルを、ハイブリッド電気自動車(HEV)アプリケーションのための直接燃料噴射と柔軟性を備えた1.6リッター、i-4ターボチャージャーユニット用に変換するために使用されます。

この方法はまた、砂型鋳造のような他の方法よりも優れた公差と表面仕上げを実現します。そのため、1,000~1万個というかなり大量のバッチ生産が可能な、実績のある技術です。しかし、金型費用は様々で、一般的に砂型鋳造法よりも高いです。

従って、メーカーは市場環境の変化に合わせてポートフォリオを刷新することが予想され、これが予測期間中の市場を牽引すると見られています。

アジア太平洋地域が市場を独占

アジア太平洋地域では、製造業やインフラ整備への投資の増加により、急速な工業化が進んでいます。この地域では、航空宇宙、防衛、建設などの産業が大きな成長を遂げると予想されているため、重力ダイカスト市場に新たな機会が生まれると期待されています。

アジア太平洋地域は、軽量部品への需要の高まり、可処分所得の増加、エネルギー効率と持続可能性の重視の高まりなど、多くの要因により、重力ダイカスト鋳造の最大かつ最も急成長している市場です。

アジア太平洋地域の重力ダイカスト市場は、世界最大の自動車市場である中国が大きく牽引しています。軽量でエネルギー効率の高い部品の使用を奨励する政府の取り組みの結果、重力ダイカストは中国で高い需要が見込まれています。また、中国における電気自動車の普及は、市場に新たな門戸を開くものと思われます。

可処分所得が増加し、燃料効率への注目が高まっているため、アジア太平洋地域のもう一つの重要な市場であるインドでは、軽量部品への需要が高まっています。政府が軽量でエネルギー効率の高い部品の使用を奨励していることで、インドでは重力ダイカスト鋳造の需要が高まると予想されます。さらに、同市場はインドにおける電気自動車の人気上昇からも恩恵を受けると予想されます。

また、自動車に対する大きな需要が、より多くの相手先商標製品メーカーや自動車部品メーカーの出現につながりました。その結果、インドは自動車と自動車部品の専門知識を発展させ、インド製ダイカスト自動車部品の需要を押し上げ、市場成長を後押ししました。

自動車部品工業会(ACMA)の予測によれば、インドからの自動車部品輸出は2026年までに300億米ドルに達する見込みです。自動車部品産業は、2026年までに2,000億米ドルの収益を記録すると予測されています。

この地域では、重力ダイカストの利用を増加させると予測される大幅な技術進歩が見られます。材料科学、設計ソフトウェア、自動化技術の発展により、重力ダイカストの効率と品質が向上し、さまざまな部門にとってより魅力的なものになると予測されています。

重力ダイカスト業界の概要

市場の主要企業には、Rockman Industries、Endurance Group、Minda Corporation、日立金属、Georg Fischer Limited、MAN Group(Alucast)、Zollern GmbH、Esko Die Casting、CIE Automotiveなどがあります。市場の主要企業は、需要増に対応するために生産能力を拡大しています。例えば

- 2023年6月、中国の自動車部品サプライヤーAsiaway Automotive Componentsは、メキシコのサン・ルイス・ポトシに4,140万米ドルを投資して新工場の第1期を稼働させました。このティア2サプライヤーは、ダイカストプロセス(HPDC 125T~6600T)、CNC、機械加工、洗浄、テスト、組立、倉庫保管、サンルイスポトシおよびメキシコ北部のさまざまなティア1企業への配送を使用して、アルミニウムと亜鉛の自動車部品を生産しています。

- 2023年9月、Rox Motor Techと北京汽車工が共同で設立した自動車ブランドPolestonesは、山東威侠先駆集団から10億米ドルの戦略的投資を受けたと発表しました。資金はオールアルミ車体の研究開発、統合ダイカスト技術、短工程インテリジェント製造工場プロジェクトに使用されます。

- 2022年5月:シャフハウゼン(スイス)のGFの支店であるGF Casting Solutionsは、その経験を電気自動車部品(EV)の開発向上に生かすと発表しました。同社は、設計やコンセプトの初期段階から顧客と協力することで、顧客の要求を満たす製品を生み出すことができます。共同開発の段階で、GF Casting Solutionsは、ルノーの2つのハイブリッド・モデル用の軽量ダイキャスト・バッテリー・ハウジングを製作しました。この筐体はアルミニウム合金で作られており、優れた機能統合と冷却回路の統合を可能にしています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場促進要因

- 自動車産業の成長が重力ダイカスト市場の需要を牽引

- 市場抑制要因

- 高い加工コストが市場拡大の妨げになる可能性

- 業界の魅力度-ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 用途

- 自動車

- 電気・電子

- 産業用途

- その他の用途

- 原材料

- アルミニウム

- 亜鉛

- 地域

- 北米

- 米国

- カナダ

- その他北米

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- ドイツ

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他アジア太平洋地域

- 世界のその他の地域

- 南米

- 中東・アフリカ

- 北米

第6章 競合情勢

- ベンダー市場シェア

- 企業プロファイル

- Rockman Industries

- Endurance Group

- Minda Corporation

- Hitachi Metals

- Georg Fischer Limited

- MAN Group(Alucast)

- Zollern GmbH

- Harrison Castings

- Esko Die Casting

- CIE Automotive

第7章 市場機会と今後の動向

- 電気自動車の普及拡大

The Gravity Die Casting Market size is estimated at USD 25.43 billion in 2024, and is expected to reach USD 30.72 billion by 2029, growing at a CAGR of 3.79% during the forecast period (2024-2029).

Gravity-die casting is one of the oldest methods of die casting. This die-casting process is used to create accurately dimensioned, finely defined, smooth, or textured surface metal parts. The fundamental benefit of gravity die casting is its fast-manufacturing speed. The reusable die tooling enables the production of hundreds of castings per day. High-definition parts reduce machining costs, while higher surface finish saves finishing expenses.

Due to its high thermal conductivity, the electrical and electronics industry is likely to see an increase in demand for aluminum die-casting parts during the forecast period. Die-casting machinery is in high demand as a result of the automotive industry's growing preference for lightweight metals and rising automobile sales.

Over the long term, the market is anticipated to benefit from the development of renewable power generation and the rapid expansion of the consumer electronics, computers, and communication industries.

With the development of new technologies, automotive parts have seen advancement and innovation in recent years. Among them, auto component manufacturing using lightweight materials has received national attention. In addition, automakers are using lightweight non-ferrous metals to reduce the weight of vehicles as a result of CAFE standards and EPA policies to reduce automobile emissions and improve fuel economy. As a result, the former automotive market is witnessing a significant boost from the use of die-cast parts to reduce weight.

Gravity Die Casting Market Trends

Automotive Industry is Expected Capture Major Market Share

Gravity die casting is a standard process for manufacturing some high-integrity automotive parts. This process produces fine-grained and dense structures with attractive mechanical properties, due to the fast and oriented hardening of the melts in permanent metal molds, which makes it ideal for components like engine-related parts.

But the trend away from the combustion engine toward alternatives like electric powered vehicles has inevitable effects on the demand for die-casted parts. For instance, while a combustion engine contains approximately 200 casted parts, only around 25, i.e., one tenth of them, are needed for an electrical drivetrain.

Factors such as lowering carbon emissions increased government initiatives to promote the usage of lighter vehicles, and rapid development of technology in automotive die-casting machines are anticipated to boost demand in the market.

Driven by ecological and economic requirements, the global automotive industry has been creating new body-in-white designs in which structural die-cast components help significantly reduce weight. Moreover, the production of die-cast structural components has increased even more due to incorporating functions into the castings, new aluminum alloy concepts, and new component design trends. Moreover, growing vehicle sales, not only in the passenger car segment but also for commercial vehicles, are expected to support the market's growth.

The automotive industry consumes over 60% of the cast products used worldwide. Thereby, considering the growth opportunities associated with the automobile and transportation industry, several players in the market are focusing on manufacturing plant expansion. For instance,

- November, 2022: General Motors announced an investment of USD 45 million in expanding its aluminum die-casting foundry in Bedford, Indiana, to feed two metro Detroit assembly plants that will produce electric vehicles.

- August, 2022: Stellantis announced an investment of USD 14 million in the Kokomo casting plant. The investment at the Casting Plant will be used to convert existing die-cast machines and cells for 1.6-liter, I-4 turbocharged units with direct fuel injection and flexibility for hybrid-electric vehicle (HEV) applications.

This method also gives better tolerances and surface finish than other methods, like sand casting. Hence, it represents a proven technology to produce fairly large batch quantities of the order of 1,000 to 10,000. But tooling costs vary and are generally higher than the sand-casting method.

Hence, manufacturers are expected to revamp their portfolio to the changing market conditions, which is expected to drive the market over the forecast period.

Asia-Pacific Dominates the Market

The Asia-Pacific region is witnessing rapid industrialization, driven by increasing investments in manufacturing and infrastructure development. This is expected to create new opportunities for the gravity die-casting market, as several industries such as aerospace, defense, and construction are expected to witness significant growth in the region.

The Asia-Pacific region is the biggest and fastest-growing market for gravity die casting because of a number of factors, like the growing demand for lightweight components, rising disposable incomes, and a growing emphasis on energy efficiency and sustainability.

The gravity die-casting market in the Asia-Pacific region is largely driven by China, the largest automotive market in the world. Gravity die-casting is expected to be in high demand in China as a result of the government's efforts to encourage the use of lightweight and energy-efficient components. Also, the rising reception of electric vehicles in China is supposed to set out new open doors for the market.

Due to rising disposable incomes and an increasing focus on fuel efficiency, India, another significant market in the Asia-Pacific region, is experiencing a growing demand for lightweight components. Gravity die casting is expected to be in high demand in India as a result of the government's efforts to encourage the use of lightweight and energy-efficient components. Additionally, the market is anticipated to benefit from the rising popularity of electric vehicles in India.

Significant demand for automobiles also led to the emergence of more original equipment and auto components manufacturers. As a result, India developed expertise in automobiles and auto components, which helped boost the demand for Indian die-casted auto components, propelling the market growth.

As per the Automobile Component Manufacturers Association (ACMA) forecast, auto component exports from India is expected to reach USD 30 Billion by 2026. The auto component industry is projected to record USD 200 Billion in revenue by 2026.

The region is seeing substantial technological advancements, which are projected to increase the usage of gravity die casting. Developments in materials science, design software, and automation technologies are predicted to increase gravity die casting efficiency and quality, making it more appealing to a variety of sectors.

Gravity Die Casting Industry Overview

Some of the major players in the market include Rockman Industries, Endurance Group, Minda Corporation, Hitachi Metals, Georg Fischer Limited, MAN Group (Alucast), Zollern GmbH, , Esko Die Casting, and CIE Automotive. Key players in the market are expanding their production capacity to cater to the increased demand. For instance,

- June 2023, Chinese automotive supplier Asiaway Automotive Components inaugurated the first phase of its new plant in San Luis Potosi, Mexico with an investment of USD 41.4 million. The Tier 2 supplier produces aluminum and zinc automotive components using the die-casting process (HPDC 125T - 6600T), CNC, machining, cleaning, testing, assembly, warehousing and distribution to various Tier 1 companies in San Luis Potosi and throughout northern Mexico.

- September 2023, Polestones, an auto brand jointly established by Rox Motor Tech Co., Ltd. and Beijing Automobile Works, announced that it received a USD 1 billion strategic investment from Shandong Weiqiao Pioneering Group. The funds will be used for all-aluminum vehicle body R&D, integrated die casting technologies, and a short-process intelligent manufacturing plant project.

- May, 2022: GF Casting Solutions, a branch of GF, Schaffhausen (Switzerland), said that it will use its experience to improve the development of electric car parts and components (EVs). The company is able to create goods that satisfy the demands of its clients by cooperating with them from the early design and conceptual phases. In a cooperative development phase, GF Casting Solutions created a lightweight die-cast battery housing for Renault's two hybrid models. The enclosure is built of an aluminum alloy, which allows for great functional integration and an integrated cooling circuit.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.1.1 Growth of the Automotive Industry to Drive Demand in the Gravity Die Casting Market

- 4.2 Market Restraints

- 4.2.1 High Processing Cost May Hamper Market Expansion

- 4.3 Industry Attractiveness - Porter's Five Force Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Application

- 5.1.1 Automotive

- 5.1.2 Electrical and Electronics

- 5.1.3 Industrial Applications

- 5.1.4 Other Appplications

- 5.2 Raw Material

- 5.2.1 Aluminum

- 5.2.2 Zinc

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Germany

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Rest of the World

- 5.3.4.1 South America

- 5.3.4.2 Middle East & Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 Rockman Industries

- 6.2.2 Endurance Group

- 6.2.3 Minda Corporation

- 6.2.4 Hitachi Metals

- 6.2.5 Georg Fischer Limited

- 6.2.6 MAN Group (Alucast

- 6.2.7 Zollern GmbH

- 6.2.8 Harrison Castings

- 6.2.9 Esko Die Casting

- 6.2.10 CIE Automotive

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Growing Adoption of Electric Vehicles