|

市場調査レポート

商品コード

1852192

水酸化リチウム:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Lithium Hydroxide - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 水酸化リチウム:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年09月09日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

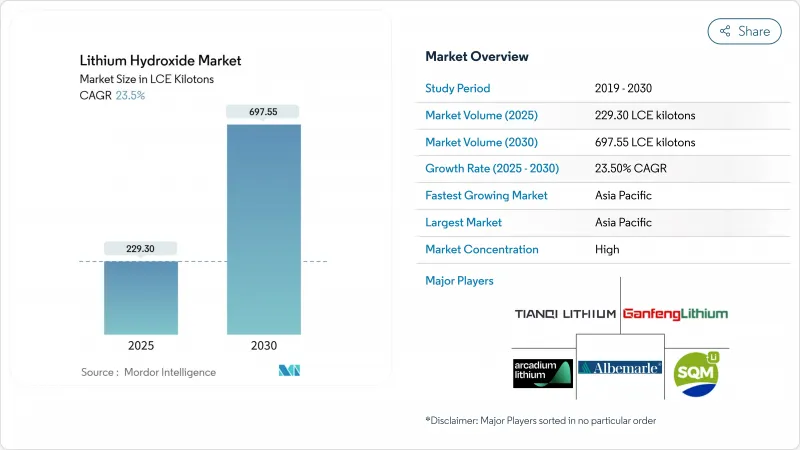

水酸化リチウム市場規模は2025年に229.30LCEキロトンと推定され、2030年には697.55LCEキロトンに達すると予測され、予測期間(2025-2030年)のCAGRは23.5%です。

電池用化学品をめぐる競争の激化、電気自動車(EV)販売の急増、リチウム直接抽出(DLE)技術の急速なスケールアップにより、世界の供給網は再構築されつつあります。アジア太平洋地域は世界消費量の40%を占める最大の地域であり、2030年までの成長率は27.66%と最も速いです。自動車メーカーは高純度原料を確保するために2024年に長期調達契約を締結し、いくつかの電池メーカーは価格変動をヘッジするために垂直統合戦略を加速させました。同時に、2023年には8万1,500米ドル/トンから2万2,500米ドル/トンへと、原料価格の変動が激しくなるため、プロジェクト・ファイナンス・モデルへの課題も残る。

世界の水酸化リチウム市場の動向と洞察

電動工具の需要増加

コードレス電動工具は、リチウムイオンパックがより長い稼働時間と優れたパワーウェイトレシオを実現するため、建設や産業保守においてコード付きの代替品に取って代わりつつあります。メーカー各社は、高放電サイクル用に最適化されたセル形式を発売しており、水酸化リチウムの豊富なニッケルーコバルトーマンガン正極が好まれています。北米と欧州では、労働市場の逼迫により生産性の向上が重視されるため、専門工事業者の間での普及が最も進んでいます。建築情報モデリング・ワークフローの継続的な採用は、作業員が現場で拘束されない機動性を必要とするため、コードレス工具の普及をさらに加速させる。EV需要よりは小さいもの、このニッチは、特殊な正極合材を供給する水酸化物メーカーにとって、平均を上回る価格実現をもたらします。

直接リチウム抽出(DLE)の商業化で低コストの原料を解き放つ

IBATのユタ工場では、モジュール式吸着カラムを利用したフィールドスケールの成功により、従来の池蒸発に必要な数ヶ月に対し、数時間で80~90%のリチウム回収が実証されました。カリフォルニア州のプロジェクトATLiSは、地熱かん水から年産2万トンの水酸化リチウムを供給するために、13億6,000万米ドルの条件付き融資保証を確保し、DLEの拡張性に対する貸し手の信頼を確かなものにしました。収率が高ければ、1トン当たりの資本集約度が下がり、水不足地域での操業が可能になります。これは、イオン交換やメンブレンの多くの種類が、池方式よりも補給水の消費量が少ないからです。こうした経済性は、環境フットプリントを削減すると同時に、水酸化リチウム市場の長期的な供給見通しを強化します。

高い生産コスト

電池グレードの水酸化リチウムプラントは、高度な不純物制御と高価な晶析回路を必要とします。アルベマール社は、オーストラリアのケマートン工場の拡張を中止し、予定生産能力を半分に減らし、現場の人員を40%削減しました。多年にわたる投資回収期間、厳しい環境許認可、限られた水力冶金の人材プールが、高い参入障壁を維持し、特にエネルギー関税の高い地域では、新設の勢いを鈍らせています。

セグメント分析

リチウムイオン電池は2024年の需要の63%を生み出し、2030年までCAGR 26.77%で拡大すると予測されます。この分野だけで水酸化リチウム市場規模の最大部分を占め、増加トン数も最大です。ニッケルーコバルトーマンガン(NCM)やニッケルーコバルトーアルミニウム(NCA)のようなレンジ指向の化学薬品は、炭酸塩ではなく水酸化リチウムを合成に必要とし、構造需要を支えています。これとは対照的に、潤滑グリース、純化空気システム、特殊合成は、安定的ではあるが小幅な寄与にとどまっています。欧州連合(EU)ではリサイクル義務化が進んでおり、予測期間後半には二次的な供給チャネルが形成され、一次的な需要は緩和されるもの、取って代わられることはないと予想されます。

エネルギー貯蔵の導入は、最も急成長しているサブアプリケーションを形成しています。再生可能エネルギー資産と連動する大規模バッテリーファームには、サイクル寿命の長い化学物質が必要です。カリフォルニア州の数ギガワット時規模の設備のようなプロジェクトでは、ニッケルを多く含むカソードを指定することが増えており、水酸化物の消費を強化しています。コストが低下するにつれて、小規模な商業用や産業用のビハインド・ザ・メーター・システムもこの機会に加わり、水酸化リチウム市場は据置型とモバイル型にまたがる多様な成長エンジンを維持しています。

バッテリーグレードの材料は2024年に70%のシェアを占め、CAGRは25.55%と予測されます。ナトリウム、カルシウム、重金属に対する厳しい不純物規制が、テクニカルグレードとの価格差を支えています。リベントのようなメーカーは、100ppm未満の不純物総量規制を達成するため、再結晶とイオン交換モジュールに追加投資しています。この投資は資本集約度を高めるが、同時に競合を深化させる。テクニカルグレードは、公差の閾値が緩いグリースやセラミック市場に対応し、工業グレードは、水処理や特定の合成ルートに対応しています。

バッテリーグレードの水酸化リチウム市場シェアは、OEMの仕様書が長くなるにつれて上昇し続けると思われます。次世代のソリッドステートおよび高シリコン負極設計は、精密な化学量論と超低含水率に依存しており、品質プレミアムを増幅する要因となっています。垂直統合された食塩水または硬質岩石原料に加え、社内で精製を行う生産者は、このマージンプールを獲得するのに最も適した立場にあります。

水酸化リチウム市場レポートは、用途(リチウムイオン電池、潤滑グリース、その他)、最終用途産業(自動車、家電、その他)、グレード(電池グレード、技術グレード、工業グレード)、形態(一水和物、無水物)、地域(アジア太平洋、北米、欧州、南米、中東アフリカ)で区分されています。

地域分析

2024年の水酸化リチウム市場シェア40%を占めるアジア太平洋地域は、他の追随を許さないセル製造能力と、川下の正極、負極、パック組立業者の密集したクラスターの恩恵を受けています。中国の政策指令は現在、国内調達を優先し、内陸の塩湖かん水の積極的な開発や海外出資を促しており、日本と韓国は長年の材料科学の専門知識を活用して競争力を維持しています。インドは、2025-26年度連邦予算のもと、国家製造業ミッションと重要鉱物の関税免除でこの争いに参入し、地元での水酸化物転換提案を刺激しました。

北米の拡大は、大規模な資金パッケージにかかっています。DOEがアルベマールに交付した1億5,000万米ドルは、年間160万台のEVに供給可能なキングスマウンテンのスポジュメン濃縮装置を支援するものです。現代自動車グループとSK Onは、ジョージア州に50億米ドルの電池セル工場を建設することを承認し、地元産の水酸化物に対する地域の正極需要を支えています。これらのイニシアチブは、アジアのサプライチェーンへの依存を削減し、米国のインフレ削減法の調達基準を満たすことを目的としています。

南米は依然として主要な供給拠点です。チリの国家リチウム戦略は、国の監視を守りつつ民間の参入を誘致し、新たな地質調査によって推定埋蔵量が28%増加しました。アルゼンチンは、リオ・ティントの25億米ドルの鉱山投資と複数のOEM引き取りを誘致しました。ブラジルのEV販売台数は2024年に85%急増し、BYDが70%のシェアを占め、将来の国内水酸化物転換の必要性を示唆しました。

欧州は、厳しいCO2規制と包括的なリサイクル義務化によって生産能力を加速。ドイツは次世代カソードの研究開発を先導し、EU電池規則では2025年以降のリチウム回収の最低割当量が設定されています。フィンランド、フランス、ポルトガルでは、2027年までにいくつかのグリーンフィールド転換プラントが稼働を開始する予定で、水酸化リチウム市場の供給基盤に多様性が加わっています。特に中国が技術輸出規制案を実施した場合、戦略的自治を推進する圏域は貿易の流れを再編成する可能性があります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 電気自動車需要の増加

- 電動工具の需要増加

- 直接リチウム抽出(DLE)の商業化低コストの水酸化物原料を解き放つ

- ラテンアメリカの水酸化物新規生産能力はOEMの長期契約によりリスクを回避

- 電池サプライチェーンを支える政府の政策

- 市場抑制要因

- 高い生産コスト

- プロジェクト資金調達の妨げとなる原料価格変動

- 毒性に対する懸念の高まり

- バリューチェーン分析

- ポーターのファイブフォース

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測(数量および金額)

- 用途別

- リチウムイオン電池

- 潤滑グリース

- 精製

- その他の用途(ポリマー・特殊化学合成)

- 最終用途産業別

- 自動車

- コンシューマー・エレクトロニクス

- エネルギー貯蔵システム

- その他(産業機械・オフロード機械)

- グレード別

- 電池グレード(56.5%以上のLiOH*H2O)

- テクニカルグレード

- 工業用グレード

- 形態別

- 一水和物

- 無水

- 地域別

- アジア太平洋地域

- 中国

- 日本

- 韓国

- インド

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- 北欧諸国

- その他欧州地域

- 南米

- ブラジル

- アルゼンチン

- チリ

- その他南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- その他中東・アフリカ地域

- アジア太平洋地域

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Albemarle Corporation

- Arcadium Lithium

- Chengxin Lithium

- Ganfeng Lithium Group Co. Ltd.

- IGO Limited

- LevertonHELM Limited

- Nemaska Lithium(Investissement Quebec)

- Piedmont Lithium Inc.

- Shandong Ruifu Lithium Co., Ltd.

- Sinomine Resource Group

- SQM S.A.

- Tianqi Lithium Corporation

- Yahua Industrial Group Co.