ポリウレタン(PU)コーティングの世界市場:市場シェア分析、産業動向・統計、成長予測(2024~2029年)

Polyurethane (PU) Coatings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)- 発行日

- ページ情報

- 英文 150 Pages

- 納期

- 2~3営業日

- 商品コード

- 1519906

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

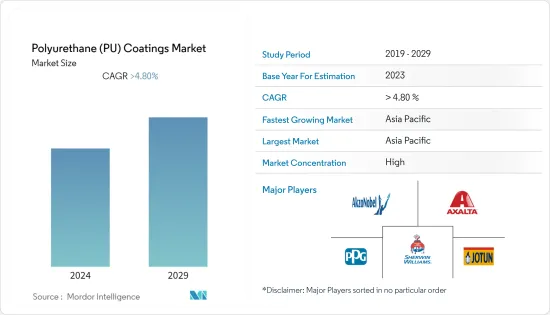

世界のポリウレタンコーティングの市場規模は、2024年に211億5,000万米ドルに達し、2024~2029年にかけてCAGR 4%以上で成長し、2029年には268億8,000万米ドルに達すると予測されています。

市場は2020年のCOVID-19によりマイナスの影響を受けました。パンデミック(世界的大流行)のシナリオにより、世界の数カ国が封鎖状態に陥りました。このため、すべての製造・建設活動が停止し、ポリウレタンコーティングの需要に悪影響が生じた。しかし、状況は回復し、ポリウレタン塗料市場の成長は回復しました。

主なハイライト

- PU塗料は外装塗料、内装塗料、床材、屋根材、断熱材として使用されるため、建設産業が市場の成長を牽引しています。さらに、木材や金属などの軽量建材の人気が高まっていることもPUコーティング市場を牽引しています。

- イソシアネートやポリオールなど、PUコーティングの生産に使用される原材料の価格は不安定で、大きく変動することがあります。これはPUコーティングメーカーの収益性に影響を与える可能性があります。

- さらに、PUコーティングはインプラントやカテーテルなどの医療機器のコーティングにも使用されています。医療機器の生体適合性を高めるためにも使用されています。

- ポリウレタンコーティングの消費量では、アジア太平洋が大きなシェアを占めています。同地域は、予測期間中に最も速い成長を遂げると予想されています。

ポリウレタンコーティングの市場動向

自動車産業が市場を独占

- 自動車産業は、世界中でポリウレタンコーティングの最大の消費者です。自動車用塗料に使用される下塗り塗料の大半は陰極電着プロセスを利用しており、ほぼ90%が陰極電着塗料です。ポリウレタン電気泳動塗料はこのプロセスで優れた役割を果たしています。

- PU塗料はOEMと再塗装の両方に使用されています。エポキシポリアミドポリウレタンとアクリルポリウレタン塗料は、この産業で一般的に好まれている塗料です。

- 過去10年間、自動車産業は有望な成長期を迎えましたが、近年その勢いは鈍化しました。

- 欧州、アジア太平洋、米国など世界各地で新車の販売と生産に影響が出ました。ほとんどの国で、それまで伸びていた自動車生産に影響が出ました。しかし、世界のシナリオの改善に伴い、生産は世界中で回復しつつあります。

- OICAのデータによると、2021年の世界の自動車販売台数は2020年に比べて約5%増加しました。2022年の販売台数は8,162万8,533台、2021年は8,275万5,197台で、2021年比で1.3%の減少にとどまりました。

- OICAによると、2022年の世界の自動車生産台数は8,501万台で、前年比6%増の8,014万台です。

- 上記の要因はすべて、自動車用途におけるポリウレタンコーティングの使用に影響を与えると予想されます。

アジア太平洋では中国が市場を独占する

- 中国はPU材料の最大市場です。この強力な消費者基盤により、世界のPUコーティング市場で重要な位置を占めることができます。

- 中国汽車工業協会(CAAM)の2002年版報告書によると、中国ではCOVID-19の大流行で乗用車の販売台数が減少したにもかかわらず、同市場の乗用車総販売台数は回復しました。2022年の販売台数は2,350万台を超え、過去4年間で最高の数字となった。PUコーティングは、自動車を腐食やその他の損傷から保護するために使用されるため、PUコーティング市場を牽引する可能性を秘めています。また、自動車の外観を向上させるためにも使用されています。

- 2022年、中国国家統計局によると、中国の建設産業は前年比6%増の31兆人民元(4兆6,000億米ドル)以上の生産高を生み出し、29兆3,100億人民元(4兆3,600億米ドル)を占めました。また、10年前と比べてほぼ100%増加しており、PUコーティング市場や、風雨から建物を保護する建設産業の技術動向の高まりに好影響を与えています。また、建物のエネルギー効率を向上させるためにも使用されています。

- さらに最近の動向では、環境保護の要求と意識の向上により、中国の水性PUコーティング産業は急速に発展し、その成長率はPU材料産業全体をはるかに上回っています。

- 2023年10月、European Coatingsによると、研究者は木材コーティング用途のバニリン系UV硬化ポリウレタン分散液の合成を実証しました。

- 中国のCovestroは最近、アジア太平洋の需要増に対応するため、上海にポリウレタン分散施設を完成させました。

- 厳しい環境監督により、同国では水性PUコーティングの新たな開発余地が生まれました。

- 以上のような要因から、予測期間中、同地域ではポリウレタンコーティングの需要が増加すると予測されます。

ポリウレタン塗料産業の概要

ポリウレタンコーティング市場は統合された性質を持っています。主要企業(順不同)には、Akzo Nobel NV、Jotun、Axalta Coating Systems、PPG Industries Inc.、The Sherwin-Williams Companyなどが含まれます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 建設産業からの需要拡大

- 自動車産業からの需要増加

- 輸送産業からの需要増加

- 抑制要因

- 不安定な原材料価格

- その他の抑制要因

- 産業バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション(市場規模:金額)

- 技術

- パウダー

- 溶剤系

- 水系

- 放射線硬化

- エンドユーザー産業

- 自動車

- 輸送

- 建築

- 電気・電子

- 木材・家具

- その他のエンドユーザー産業

- 地域

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他のアジア太平洋

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- その他の欧州

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- その他の中東・アフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア(%)/ランキング分析

- 主要企業の戦略

- 企業プロファイル

- Akzo Nobel NV

- Asian Paints

- Axalta Coating Systems

- BASF SE

- IVM Chemicals SRL

- Jotun

- Polycoat Products

- PPG Industries Inc.

- RPM International Inc.

- The Sherwin-Williams Company

第7章 市場機会と今後の動向

- 航空宇宙産業と医療産業におけるPUコーティングの新しい用途

- ナノテクノロジーとPUコーティングの融合における発展

目次

The Polyurethane Coatings Market size is estimated at USD 21.15 billion in 2024, and is expected to reach USD 26.88 billion by 2029, growing at a CAGR of greater than 4% during the forecast period (2024-2029).

The market was negatively impacted due to COVID-19 in 2020. Owing to the pandemic scenario, several countries around the world went into lockdown. It halted all manufacturing and construction activities, thus creating a negative impact on the demand for polyurethane coatings. However, the condition recovered, thereby restoring the growth of the polyurethane coatings market.

Key Highlights

- The construction industry is driving the market's growth as PU coatings are used as exterior coatings, interior coatings, flooring, roofing, and insulation. Moreover, the increasing popularity of lightweight construction materials such as wood and metal is also driving the PU coatings market.

- The prices of raw materials used in the production of PU coatings, such as isocyanates and polyols, are volatile and can fluctuate significantly. It can impact the profitability of PU coatings manufacturers.

- In addition, PU coatings are being used to coat medical devices, such as implants and catheters. They are also being used to make medical devices more biocompatible.

- Asia-Pacific holds the major share in the consumption of polyurethane coatings. The region is also expected to witness the fastest growth during the forecast period.

Polyurethane Coatings Market Trends

Automotive Industry to Dominate the Market

- The automotive industry is the largest consumer of polyurethane coatings across the world. The majority of the primers used in automotive coatings utilize a cathodic electric deposit process, which constitutes almost 90% cathode electrophoretic paint. Polyurethane electrophoretic paint plays an excellent role in the process.

- PU coatings are used for both OEM and refinish applications. Epoxy polyamide polyurethane and acrylic polyurethane coats are the commonly preferred coatings in the industry.

- Despite an encouraging term of growth in the automotive sector during the past decade, the momentum slowed down in recent years.

- The sales and production of new vehicles were affected in various parts of the world, including Europe, Asia-Pacific, and the United States. It affected the previously growing automotive production in most nations. However, with the improving global scenario, production is recovering around the globe.

- According to the OICA data, global automotive sales increased by around 5% in 2021 compared to 2020. In 2022, there was only a 1.3% decline when compared to 2021, with sales of 8,16,28,533 and 8,27,55,197 in 2022 and 2021, respectively.

- As per OICA, the global production of automotive accounted for 85.01 million units in 2022, which is an increase of 6% compared to the previous year by 80.14 million units.

- All the factors above are expected to affect the usage of polyurethane coatings in automotive applications.

China to Dominate the Market in the Asia-Pacific Region

- China is the largest market for PU materials. This strong consumer base enables it to take a key position in the global PU coatings market.

- According to the China Association of Automobile Manufacturers (CAAM) 2002 report, despite the recent decline in passenger car sales in China during the COVID-19 pandemic, total passenger car sales in the market bounced back. In 2022, the sales exceeded 23.5 million units, making it the highest figure in the past four years. It includes the potential to drive the PU coating market as it is used to protect cars from corrosion and other damage. They are also being used to improve the appearance of cars.

- In 2022, as per the National Bureau of Statistics of China, the construction industry in China generated an output of over CNY 31 trillion (USD 4.6 trillion) with an increase of 6% from the previous year, accounting for CNY 29.31 trillion (USD 4.36 trillion). It also represented an increase of almost 100 % from a decade ago, with a positive impact on the PU coating market and the growing technological trends in the construction industry to protect buildings from the elements. They are also being used to improve the energy efficiency of buildings.

- Moreover, in recent years, due to the improvement of environmental protection requirements and awareness, China's water-borne PU coatings industry developed rapidly, with the growth rate far exceeding the overall PU materials industry.

- In October 2023, according to European Coatings, researchers demonstrated the synthesis of vanillin-based UV-curable polyurethane dispersions for wood coating applications.

- Covestro in China recently completed a polyurethane dispersion facility in Shanghai to meet rising demand in the Asia Pacific region.

- Strict environmental supervision opened up a new development space for water-borne PU coatings in the country.

- All the factors above, in turn, are projected to increase the demand for polyurethane coatings in the region during the forecast period.

Polyurethane Coatings Industry Overview

The polyurethane coatings market is consolidated in nature. The major players (not in any particular order) include Akzo Nobel NV, Jotun, Axalta Coating Systems, PPG Industries Inc., and The Sherwin-Williams Company, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Demand from the Construction Industry

- 4.1.2 Increase in Demand from the Automotive Industry

- 4.1.3 Growing Demand from the Transportation Industry

- 4.2 Restraints

- 4.2.1 Volatile Raw Material Prices

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Technology

- 5.1.1 Powder

- 5.1.2 Solvent-borne

- 5.1.3 Water-borne

- 5.1.4 Radiation Cured

- 5.2 End-user Industry

- 5.2.1 Automotive

- 5.2.2 Transportation

- 5.2.3 Construction

- 5.2.4 Electrical and Electronics

- 5.2.5 Wood and Furniture

- 5.2.6 Others End-user Industries (Aerospace, Industrial, and Textile)

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share(%)**/ Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Akzo Nobel NV

- 6.4.2 Asian Paints

- 6.4.3 Axalta Coating Systems

- 6.4.4 BASF SE

- 6.4.5 IVM Chemicals SRL

- 6.4.6 Jotun

- 6.4.7 Polycoat Products

- 6.4.8 PPG Industries Inc.

- 6.4.9 RPM International Inc.

- 6.4.10 The Sherwin-Williams Company

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 New applications for PU coatings in Aerospace and Medical Industries

- 7.2 Development in Integration of Nanotechnology and PU coatings

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 150 Pages

- 納期

- 2~3営業日