|

市場調査レポート

商品コード

1445939

体温管理: 市場シェア分析、業界動向と統計、成長予測(2024~2029年)Temperature Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 体温管理: 市場シェア分析、業界動向と統計、成長予測(2024~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 111 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

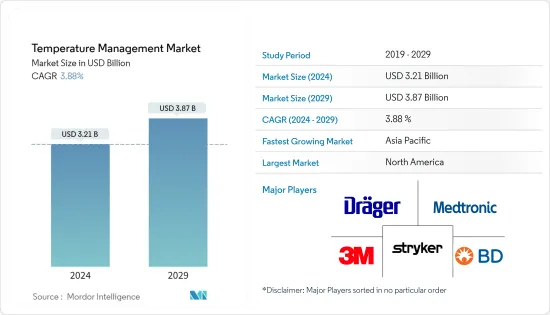

体温管理市場規模は2024年に32億1,000万米ドルと推定され、2029年までに38億7,000万米ドルに達すると予測されており、予測期間(2024年から2029年)中に3.88%のCAGRで成長します。

COVID-19のパンデミックの発生は、体温管理市場に影響を与えました。パンデミックの初期段階では、多くの外科手術がキャンセルまたは延期され、術後の必須要件の1つである体温管理システムの需要が減少しました。たとえば、2021年に発表されたNCBIの調査研究によると、COVID-19の影響で多数の外科手術が中止または無期限延期されました。したがって、このようなシナリオはパンデミックの初期段階で市場にわずかな悪影響を及ぼしました。しかし、世界中の多くのヘルスケア機関は、COVID-19による汚染を避けるために正常体温環境を維持することの重要性を強調する推奨事項やガイドラインを発表しています。たとえば、2021年に3Mが発表した調査論文によると、AORN(周術期登録看護師協会)は、低体温症のリスクを軽減するために、新型コロナウイルス感染症陽性患者の外科手術中に強制カイロを使用することを推奨しています。したがって、このようなガイドラインと外科手術の再開により、市場は勢いを増し始め、予測期間にわたって上昇傾向が続くと予想されます。

がん、感染症、心血管疾患の罹患率の増加、外科手術件数の増加、技術的に進歩した血管内システムの開発が、市場の主な促進要因となっています。たとえば、WHO 2022によると、WHO GISRS研究所は、2021年 12月から2022年 1月までに317,198件を超える検体を検査しました。16,862人がインフルエンザウイルス陽性となり、このうち10,744人(63.7%)がインフルエンザ A型、6,118人(36.3%)がインフルエンザウイルスに陽性反応を示しました。サブタイプ化されたインフルエンザ Aウイルスのうち、224(4.3%)がインフルエンザ A(H1N1)pdm09であり、4930(95.7%)がインフルエンザ A(H3N2)でした。同様に、欧州 CDCが2021年 3月に発表した報告書によると、欧州連合、欧州経済領域(EEA)、英国では毎年約50万件の性感染症が検出されていると報告されています。さらに、GLOBOCAN Report 2020によると、世界中で約19,292,789人の新たながん症例が報告され、9,958,133人ががんによる死亡を報告しています。主に影響を与えるがんは、乳がん、肺がん、結腸直腸がん、前立腺がんです。温熱療法はがんや感染症の重要な治療法であり、体温管理システムを使用することで実現できます。したがって、世界中でがんや感染症の症例が増加しているため、予測期間中に市場の成長が促進されると予想されます。

外科手術の件数の増加と主要企業による製品発売も市場の成長を加速させています。例えば、保健・家族福祉省と保健・家族福祉省が2021年から2022年にかけて発表した報告書によると、2021年9月までに約829万人がOPDを訪れ、インドのサフダルジュン病院では約3万3,830件の手術が行われました。同情報筋はまた、2020年から2021年にかけてインドで約25,101件の軽度の手術が行われ、約9,327件の大規模手術が行われたと報告しました。正常な体温を維持することは、手術部位感染のリスク軽減、死亡率の低下、術後の心臓イベントの減少、失血の減少、回復時間の短縮、患者の入院期間の短縮など、外科患者に貴重な利益をもたらします。体温管理システムは、病院や臨床医に、手術前、手術中、手術後に患者を暖かく保つための安全で効果的な方法を提供します。体温管理システムは必須要件の1つであるため、外科手術の数の増加は市場の成長を促進すると予想されます。

さらに、主要企業による新製品ラインの発売も、市場に新たな機会を生み出すと予想されます。たとえば、デンマークの医療技術企業MEQUは、2021年 4月に血液および点滴加温システム M Warmer System用の院内ソリューションM Stationを発売しました。 M加温システム、病院前および軍事部門で採用されているポータブル血液および点滴加温システムです。特許取得済みの加温技術を使用したMウォーマーは、10秒以内に輸液を冷たい温度から体温まで温めることができます。したがって、製品の発売の増加と外科手術の数の増加により、予測期間中の市場の成長が促進されると予想されます。

ただし、体温管理システムと製品リコールのコストが高いため、予測期間中の市場の成長が抑制される可能性があります。

体温管理市場の動向

従来型温暖化システムセグメントは、予測期間中に大幅な成長が見込まれる

従来型加温システムは手術患者の低体温症の予防に役立ち、標準的で効果的なケアと考えられています。従来型加温システムは強制空気を提供しており、基本的に患者を囲むカバーを通して温風を吹き出します。多くの研究では、強制空気で温められた患者は手術終了時に正常な体温になっていることが示されています。従来型加温システムでは、手術室内に大きな温度勾配が生じる可能性があり、層流パターンが乱れ、対流によって流動する床面の空気で手術部位が汚染される可能性があります。したがって、いくつかの利点により、従来型加温システムは世界中で広く使用されています。

外科手術件数の増加は、この分野の主な促進要因の1つです。たとえば、ジャーナル・オブ・サージェリー・アンド・サージカル・調査が2021年10月に発行した調査誌によると、インドでは2021年に公衆衛生施設で18,882,734件以上の手術が行われ、そのうち約48件は51,788件は大手術、1,4030,946件は軽度の手術でした。同情報筋はまた、アーンドラ・プラデーシュ州で約1,443,913件の手術が行われ、マディヤ・プラデーシュ州で約59,08,59件の手術が行われ、マハーラーシュトラ州で約82,55,90件の手術が行われ、インドで約3,047,973件の手術が行われたと報告しました。 2020年には、タミル・ナドゥ州で約1,225,766件の手術がデリーで行われました。2021年にはインドでは合計1,888,2734件の手術が行われました。従来型加温システムは一般に、手術前後の体温を暖かく維持するのに役立ちます。したがって、外科手術の数を増やすことで、このセグメントの成長が促進されると予想されます。

感染症の症例数の増加も、予測期間中のこの部門の成長を推進しています。たとえば、2021年11月にWHOが発表した報告書によると、世界中で100万人以上の性感染症が感染しており、そのほとんどは無症状です。また、毎年推定3億7,400万人が新たに感染しており、性感染症の4つのうち1つが淋病、クラミジア、トリコモナス症、梅毒であると報告しました。同様に、CDCが2022年4月に発表した報告書によると、2020年には約67万7,769件の淋病症例が報告され、2016年から約5.7%増加しました。また、淋病は2021年に米国で2番目に一般的な注目すべき性感染症となった。体温管理は感染症の治療において重要な部分の1つです。したがって、感染症の症例の増加により、予測期間中にセグメントの成長が押し上げられる可能性があります。

北米は予測期間中に大幅な成長を遂げると予想される

北米は予測期間中に大幅な成長を遂げると予想されます。この成長の要因としては、この地域における感染症、がんの症例の増加、外科手術の増加などが挙げられます。例えば、疫学監視・疾病管理センターとメキシコ州保健研究所(ISEM)のHIV/AIDS/STI部門によると、2021年現在、後天性梅毒の症例は6件以上、梅毒の感染者は9件以上です。淋菌感染症、483人以上のトリコモナス症、15人以上の性器ヘルペス、1,042人以上のカンジダ症(イースト菌感染症)、5,585人以上の外陰膣炎、そして136人以上の無症候性HIV感染症が新たに報告されています。UNAIDS 2021が発表したデータによれば、23万人以上のメキシコ人がHIVとともに暮らしています。したがって、感染症の増加により体温管理システムの需要が増加し、それによって北米地域の市場の成長を促進する可能性があります。

主要製品の発売、市場プレーヤーやメーカーの存在感の集中、大手プレーヤー間の買収や提携、米国における外科手術や病気の数の増加などが、この国の体温管理市場の成長を促進する要因の一部です。例えば、CDCは2022年5月、2021年に米国およびその属領で30,635人がHIVに感染したと報告しました。また、同じ情報源は、2022年末までにHIVとともに生きる米国人の数は1,189,700人になると予測されるとも述べた。さらに、革新的な製品の承認により、米国でも市場の成長が加速する可能性があります。たとえば、2020年 10月に、Genthermは米国FDAから510(k)認可を取得し、米国でASTOPADTM患者加温システムを発売したと発表しました。 ASTOPADシステムはすべての外科手術に利用でき、周術期手術全体を通じて患者の低体温症の予防と治療に役立ちます。したがって、感染症の蔓延と製品の承認の高さにより、米国では予測期間中に市場が成長すると予想されます。

体温管理業界の概要

体温管理市場は、世界的および地域的に事業を展開している複数の企業の存在により、適度に細分化されています。競合情勢には、大きな市場シェアを保持しよく知られている数社の国際企業と地元企業の分析が含まれています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- がん、感染症、心血管疾患の罹患率の増加

- 外科手術件数の増加

- 最先端の血管内システムの開発

- 市場抑制要因

- 体温管理システムのコストが高い

- 製品のリコールと故障

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替製品の脅威

- 競争企業間の敵対関係の激しさ

第5章 市場セグメンテーション

- 製品タイプ別

- 患者加温システム

- 従来型加温システム

- 表面加温システム

- 血管内加温システム

- 患者冷却システム

- 従来型冷却システム

- 血管内冷却システム

- 表面冷却システム

- 患者加温システム

- 用途別

- 心臓病

- 整形外科

- 神経内科

- その他

- エンドユーザー別

- 手術室

- ICU

- ER

- その他

- 地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他アジア太平洋

- 中東とアフリカ

- GCC

- 南アフリカ

- その他中東とアフリカ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 企業プロファイル

- 3M

- Atom Medical Corporation

- Becton, Dickinson and Company

- Cincinnati Sub-Zero Products, LLC

- Dragerwerk AG &Co. KGaA

- Geratherm Medical AG

- Medtronic PLC

- Smith Medical Inc.

- Stryker Corporation

- Zoll Medical Corporation

第7章 市場機会と将来の動向

The Temperature Management Market size is estimated at USD 3.21 billion in 2024, and is expected to reach USD 3.87 billion by 2029, growing at a CAGR of 3.88% during the forecast period (2024-2029).

The outbreak of the COVID-19 pandemic impacted the temperature management market. During the initial phase of the pandemic, many surgical procedures were canceled or postponed, which reduced the demand for temperature management systems as it is one of the essential requirements of post-surgery. For instance, according to the NCBI research study published in 2021, a large number of surgical procedures were canceled or postponed during COVID-19 for an indefinite period. Thus, such a scenario imposed a slight adverse impact on the market during the initial phase of the pandemic. However, many healthcare organizations across the globe published recommendations or guidelines emphasizing the importance of maintaining a normothermia environment to avoid COVID-19 contamination. For instance, as per the research article published by 3M in 2021, AORN (Association of periOperative Registered Nurses) has recommended using forced air warmers during surgical procedures in COVID-19-positive patients to decrease the risk of hypothermia. Therefore, owing to such guidelines and with the resumption of surgical procedures, the market started to gain traction and is expected to continue the upward trend over the forecast period.

The increasing prevalence of cancer, infectious diseases, and cardiovascular diseases, the rising number of surgical procedures, and the development of technologically advanced intravascular systems are the major drivers for the market. For instance, according to the WHO 2022, the WHO GISRS laboratories tested more than 317198 specimens from December 2021 to January 2022. 16862 people were positive for influenza viruses, of which 10744 (63.7%) were typed as influenza A and 6118 (36.3%) as influenza B. Of the sub-typed influenzaA viruses, 224 (4.3%) were influenza A(H1N1) pdm09, and 4930 (95.7%) were influenza A(H3N2). Similarly, according to the report published by the European CDC in March 2021, it was reported that every year around 500,000 sexually transmitted infections detected in the European Union, European Economic Area (EEA), and the United Kingdom. Furthermore, according to the GLOBOCAN Report 2020, globally, around 19,292,789 new cancer cases have been reported, and 9,958,133 reported cancer deaths. The majorly affecting cancers are breast cancer, lung cancer, colorectum cancer, and prostate cancer. Hyperthermia is an essential treatment for cancer and infectious diseases, which can be attained by using temperature management systems. Therefore, increasing cases of cancer and infectious diseases across the globe is anticipated to propel market growth over the forecast period.

The increasing number of surgical procedures and product launches by the key players are also surging the market growth. For instance, according to the report published by the Department of Health & Family Welfare and Ministry of Health & Family Welfare in 2021-2022, till September 2021, about 8.29 lakh people visited OPDs, and around 33,830 surgeries were performed in Safdarjung Hospital, India. The same source also reported that around 25,101 minor surgeries were performed, and about 9,327 major surgeries were performed in India for the year 2020-21. Maintaining normal body temperature provides valuable benefits to surgical patients, including risk reduction of surgical site infection, reduced mortality, fewer post-operative cardiac events, reduced blood loss, faster recovery times, and shorter patient hospitalizations. Temperature management systems offer hospitals and clinicians with a safe and effective method of keeping patients warm before, during, and after surgery. Since temperature management systems are one of the essential requirements, thus increasing the number of surgical procedures is expected to boost the market growth.

Furthermore, the launch of new product lines by the key players are also anticipated to create new opportunities in the market. For instance, in April 2021, Danish medtech company MEQU launched an in-hospital solution, M Station, for its blood and IV fluid warming device, M Warmer System. M Warmer System is a portable blood and IV fluid warming device that is adopted in the pre-hospital and military sectors. Using a patented warming technology, the M Warmer is able to warm infusion fluids from cold to body temperature in under 10 seconds. Thus, increasing product launches and a rising number of surgical procedures are anticipated to propel the market growth over the forecast period.

However, the high cost of temperature management systems and product recalls may restrain the market growth over the forecast period.

Temperature Management Market Trends

Conventional Warming System Segment is Expected to Witness Considerable Growth Over the Forecast Period

Conventional warming system helps to prevent hypothermia in surgical patients and is considered standard and effective care. Conventional warming systems offers forced air, which essentially blows warm air through a cover that surrounds the patient. Many studies show that patients warmed with forced air have a normal body temperature at the end of surgery. Conventional warming systems can create significant temperature gradients within the operating room that have the potential to disrupt laminar airflow patterns and contaminate the surgical site with floor-level air mobilized by convection currents. Thus, owing to several advantages, conventional warming systems are widely used across the globe.

The increasing number of surgical procedures is one of the major drivers for the segment. For instance, according to the research journal published by the Journal of Surgery and Surgical Research published in October 2021, in India, more than 1,88,82,734 surgeries were carried out in 2021 in public health facilities, and of them, around 48,51,788 and 1,40,30,946 were major and minor surgeries, respectively. The same source also reported that around 14,43,913 surgeries were performed in Andhra Pradesh, around 59,08,59 surgeries were performed in Madhya Pradesh, about 82,55,90 surgeries were performed in Maharashtra, around 30,47,973 surgeries were performed in Tamil Nadu, and about 12,25,766 surgeries were performed in Delhi in 2020. A total of 18,88,2734 surgeries were performed in India in 2021. Conventional warming systems generally help maintain warm temperatures during pre and post-surgeries; thus, increasing the number of surgical procedures is expected to propel the segment growth.

The increasing number of cases of infectious diseases is also propelling the segment's growth over the forecast period. For instance, according to the report published by the WHO in November 2021, more than 1.0 million sexually transmitted infections were acquired globally, most of which are asymptomatic. It also reported that every year there are an estimated 374.0 million new infections, with 1 out of 4 sexually transmitted infections: gonorrhea, chlamydia, trichomoniasis, and syphilis. Similarly, as per the report published by the CDC in April 2022, around 677,769 cases of gonorrhea were reported in 2020, around a 5.7% increase from 2016. Gonorrhea also emerged as the second most common noticeable sexually transmitted infection in the United States in 2021. Temperature management is one of the essential parts of the treatment of infectious diseases; therefore, increasing cases of infectious diseases may boost segment growth over the forecast period.

North America is Expected to Witness Significant Growth Over the Forecast Period

North America is expected to witness significant growth over the forecast period. The growth is due to factors such as the rising cases of infectious diseases, cancer and increasing surgical procedures in the region. For instance, according to the Epidemiological Surveillance and Disease Control Center and the HIV/AIDS/STI Department at the Health Institute of the State of Mexico (ISEM), as of 2021, more than 6 cases of acquired syphilis, more than 9 cases of gonococcal infection, more than 483 cases of trichomoniasis, more than 15 cases of genital herpes, more than 1,042 cases of candidiasis (yeast infection), more than 5,585 cases of vulvovaginitis, and more than 136 new cases of asymptomatic HIV infection have already been reported in Mexico. As per the data published by UNAIDS 2021, more than 230,000 Mexican population was living with HIV. Thus, the increasing number of infectious diseases may increase the demand for temperature management systems, thereby driving market growth in the North American region.

Key product launches, high concentration of market players or manufacturer's presence, acquisitions and partnerships among major players, and a rising number of surgical procedures and diseases in the United States are some of the factors driving the growth of the temperature management market in the country. For instance, the CDC reported in May 2022 that 30,635 people in the United States and dependent territories acquired an HIV in 2021. The same source also stated that, by the end of 2022, the number of Americans living with HIV was predicted to be 1,189,700. Furthermore, innovative product approvals may also surge the market growth in the United States. For instance, in October 2020, Gentherm announced that it has received 510(k) clearance from the U.S. FDA and has launched the ASTOPADTM Patient Warming System in the United States. The ASTOPAD system can be utilized in all surgical procedures and helps prevent and treat hypothermia in patients throughout the perioperative procedures. Therefore, owing to the high prevalence of infectious diseases and product approvals, the market is anticipated to grow over the forecast period in the United States.

Temperature Management Industry Overview

The Temperature Management Market is moderately fragmented due to the presence of several companies operating globally as well as regionally. The competitive landscape includes an analysis of a few international as well as local companies which hold significant market shares and are well known, including 3M, Atom Medical Corporation, Becton, Dickinson and Company, Cincinnati Sub-Zero Products, Dragerwerk AG & Co. KGaA, Geratherm Medical, Medtronic PLC, Smith Medical, and Stryker Corporation among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Prevalence of Cancer, Infectious Diseases, and Cardiovascular Diseases

- 4.2.2 Rising Number of Surgical Procedures

- 4.2.3 Development of Technologically Advanced Intravascular Systems

- 4.3 Market Restraints

- 4.3.1 High Cost of Temperature Management Systems

- 4.3.2 Products Recalls & Failures

- 4.4 Porter's Five Force Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD Million)

- 5.1 By Product Type

- 5.1.1 Patient Warming Systems

- 5.1.1.1 Conventional Warming System

- 5.1.1.2 Surface Warming System

- 5.1.1.3 Intravascular Warming System

- 5.1.2 Patient Cooling Systems

- 5.1.2.1 Conventional Cooling System

- 5.1.2.2 Intravascular Cooling System

- 5.1.2.3 Surface Cooling System

- 5.1.1 Patient Warming Systems

- 5.2 By Application

- 5.2.1 Cardiology

- 5.2.2 Orthopedics

- 5.2.3 Neurology

- 5.2.4 Other

- 5.3 By End User

- 5.3.1 Operating Rooms

- 5.3.2 Intensive Care Units

- 5.3.3 Emergency Rooms

- 5.3.4 Others

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 3M

- 6.1.2 Atom Medical Corporation

- 6.1.3 Becton, Dickinson and Company

- 6.1.4 Cincinnati Sub-Zero Products, LLC

- 6.1.5 Dragerwerk AG & Co. KGaA

- 6.1.6 Geratherm Medical AG

- 6.1.7 Medtronic PLC

- 6.1.8 Smith Medical Inc.

- 6.1.9 Stryker Corporation

- 6.1.10 Zoll Medical Corporation