|

市場調査レポート

商品コード

1693597

核酸ベースの治療- 市場シェア分析、産業動向と統計、成長予測(2025年~2030年)Nucleic Acid Based Therapeutics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 核酸ベースの治療- 市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 166 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

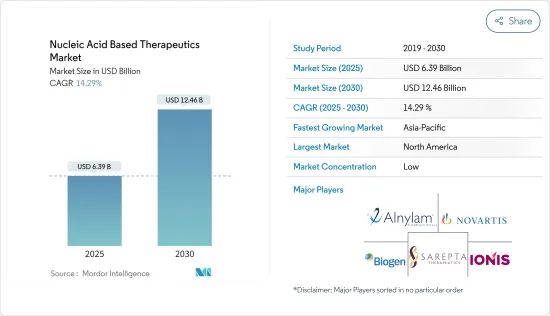

核酸ベースの治療市場規模は2025年に63億9,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは14.29%で、2030年には124億6,000万米ドルに達すると予測されます。

核酸ベースの治療は、COVID-19疾患治療の開発に効果的に使用されたため、過去2年間で需要が増加しました。MDPIが2022年2月に発表した記事によると、COVID-19ウイルスに対抗するために最も有望なのは、低分子干渉RNA(siRNA)、アンチセンスオリゴヌクレオチド(ASO)、マイクロRNA(miRNA)を含む核酸ベースの技術でした。これらの治療は、転写中と転写後のウイルス遺伝子発現を抑制することができ、大きな成長機会をもたらします。MDPIに掲載された紙製によると、2022年8月、世界全体で400以上のRNA標的医薬品開発プロジェクトが実施され、その3分の2が治験前新薬(pre-IND)段階、3分の1が初期臨床検査(第I相または第II相)段階、約3%が第III相段階にあり、一部はCOVID-19治療として規制当局の承認を待っています。このように、RNA治療の開発が進むにつれて、調査対象市場は予測期間中に成長すると予想されます。

遺伝性疾患の急増、医療セグメントへの投資の増加、革新的な生物製剤への製薬産業の急速なシフトといった要因が、予測期間中の市場の成長を後押しすると予想されます。

がん、嚢胞性線維症、鎌状赤血球貧血、デュシェンヌ型筋ジストロフィー、サラセミアなどの遺伝性疾患の有病率の増加は、特定の遺伝子の異常発現を修正することで疾患を治療する核酸ベースの治療に対する需要を促進する主要因です。例えば、嚢胞性線維症財団が2022年7月に発表したデータによると、米国では4万人の幼児と成人が嚢胞性線維症(CF)を患っています。同じ供給源によると、2022年には94カ国で推定105,000人がこの病気と診断されました。このように、人口の間で嚢胞性線維症の高い負担は、市場にプラスの影響を与えると予想されます。

慢性疾患、遺伝性疾患、その他の疾患の有病率の高さに起因する核酸治療への投資件数の増加は、市場の成長を増大させると予想されます。例えば、2023年3月、Switch Therapeuticsは、Insight PartnersとUCB Venturesが共同主導するシリーズA資金調達ラウンドで5,200万米ドルを調達しました。同社はこれらの資金を、中枢神経系疾患治療用のsiRNA治療候補の選定と開発の推進、RNAi技術の進歩に充てた。市場参入企業は、核酸ベースの治療における製品ポートフォリオを拡大するため、核酸ベースの研究開発に投資しています。例えば、2023年1月、アジレント技術社は核酸ベースの治療に7億2,500万米ドルを投資しました。この投資により、医薬品原薬(API)の製造能力は倍増します。

企業による共同研究、提携、新製品の上市、その他の取り組みへの注目の高まりは、市場における新規治療の入手可能性を高め、市場の成長を促進する可能性があります。例えば、2023年2月、CMT研究財団は、シャルコー・マリー・トゥース病におけるアンチセンス・オリゴヌクレオチドの治療効果を高めるため、Nanite Inc.と提携しました。2022年10月、Neuway Pharma GmbHとWackerは、EnPC(Engineered Protein Capsules)タンパク質ベースのドラッグデリバリー技術を使用して、中枢神経系疾患の治療のためのRNAベースの治療を同定・製造する研究プロジェクトを開始しました。

そのため、遺伝性疾患の負担が大きいこと、投資が増加していること、新製品が上市されていることなどから、予測期間中に市場は成長すると見込まれています。しかし、核酸ベースの治療の調査コストが高いことが、市場の成長を阻害する可能性が高いです。

核酸ベースの治療市場動向

アンチセンスオリゴヌクレオチド(ASO)セグメントは予測期間中に大幅な成長が見込まれる

アンチセンス・オリゴヌクレオチド(ASOs)は、特定のメッセンジャーRNA(mRNA)配列に結合することができる短い一本鎖DNAまたはRNA分子であり、標的mRNAの分解またはタンパク質への翻訳の阻害につながります。この特性により、ASOは遺伝性疾患、感染症、がんを含む様々な疾患に対する有望な治療戦略となります。ASOは、疾患の進行に寄与する異常なタンパク質や酵素の産生に関与する遺伝子など、特定の疾患原因遺伝子を標的とすることができます。

承認されているASO治療の例としては、脊髄性筋萎縮症の治療Spinraza(ヌシネルセン)、デュシェンヌ型筋ジストロフィーの治療Exondys51(エテプリルセン)、遺伝性トランスサイレチンを介するアミロイドーシスの治療Onpattro(パチシラン)、遺伝性トランスサイレチンを介するアミロイドーシスの治療Tegsedi(イノテルセン)などがあります。

ASOsセグメントは、アンチセンスオリゴヌクレオチド医薬品に対する高い需要、主要企業による研究開発活動の活発化、新製品の上市などにより、予測期間中に大きな成長が見込まれています。

希少疾患や遺伝性疾患に対する新規治療の研究開発を加速させるため、提携、共同研究、買収、その他の取り組みなど、さまざまな事業戦略を採用する企業の注目度が高まっていることが、同セグメントの成長を後押しすると予想されます。例えば、2022年9月、Vanda Pharmaceuticals Inc.とOliPassCorporationは、修飾ペプチド核酸による一連のアンチセンスオリゴヌクレオチド(ASO)分子を共同開発するための研究開発提携契約を締結しました。2021年2月、米国FDAはサレプタ社のアモンディス45(カジメルセン)注射剤を、DMD遺伝子の変異が確認されたデュシェンヌ型筋ジストロフィー(DMD)患者の治療として承認しました。

アンチセンスオリゴヌクレオチド製剤の市場投入、企業活動の活発化、新製品の上市などにより、同セグメントは予測期間中に成長すると予想されます。

予測期間中、北米が大きな市場シェアを占める見込み

北米は、さまざまな核酸ベースの治療法に関する調査の増加、遺伝性疾患やその他の慢性疾患の有病率の増加、同地域における研究開発投資の増加により、市場で大きなシェアを占めると予想されます。

人口の間で自己免疫疾患の有病率が上昇していることから、核酸ベースの治療に対する需要が高まっており、これが市場の成長を増大させる可能性があります。例えば、2022年6月の自己免疫協会の発表によると、自己免疫疾患は約80~150のユニークな慢性疾患からなり、毎年3,100万人以上のアメリカ人が罹患しています。このことは、対象集団における自己免疫疾患の負担の大きさを示しています。2023年2月にClinical Rheumatology Journalに掲載された紙製によると、カナダでは全身性自己免疫性リウマチ性疾患(SARDs)の負担が大きく、住民1,000人当たり2~5人の患者が罹患しています。

がんの増加により、がん細胞の進行を抑制する効果的な新薬の需要が高まっています。これが、この地域における核酸ベースの薬剤の需要を促進しています。例えば、Cancer Facts and Figures 2023によると、2023年には国内で約190万人が新たにがんと診断されると推定されています。カナダ政府が2022年6月に更新した統計によると、カナダでは2022年末までに約23万3,900人ががんと診断されると推定され、肺がん、乳がん、前立腺がん、大腸がんがカナダの対象人口の中で最も多く診断されるがんと予測されています。

革新的な製品の上市や承認、提携、買収、拡大、提携が、この地域における市場の成長を促進すると予測されています。例えば、2022年9月、Next Generation Manufacturing Canada(NGen)は、OmniaBio Inc.とパートナーのExCellThera、MorphoCell Technologies、Aspect Biosystems、Canadian Advanced Therapies Training Institute(CATTI)が主導する3,480万米ドルのプロジェクトに1,050万米ドルを投資しました。2021年12月、NovartisAGは、低比重リポタンパクコレステロール(悪玉コレステロールまたはLDL-Cとしても知られる)を低下させる最初で唯一のsiRNA(small interfering RNA)療法であるLeqvio(インクビオ)について、初回投与と3ヵ月後の1回投与の後、1年に2回の投与でFDAから承認を取得しました。

核酸ベースの治療産業概要

核酸ベースの治療市場は、世界的・地域的に多くの大小参入企業が存在するため、適度にセグメント化されています。各社は、様々な慢性疾患、遺伝性疾患、感染性疾患の治療のために、核酸ベースの治療の研究開発に取り組んでいます。同市場の主要企業としては、Silence Therapeutics PLC、Ionis Pharmaceuticals Inc.、Sarepta Therapeutics、Novartis Pharma AG、Alnylam Pharmaceuticals Inc.、Biogen Inc.などが挙げられます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場の促進要因

- 遺伝性疾患の急増

- 医療セグメントへの投資拡大

- 革新的な生物製剤への製薬産業の急速なシフト

- 市場抑制要因

- 核酸調査コストの高さ

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 製品タイプ別

- RNA干渉[RNAi]と短鎖干渉RNA[siRNA]

- アンチセンスオリゴヌクレオチド(ASOs)

- その他

- 用途別

- 自己免疫疾患

- 感染症

- 遺伝子疾患

- がん

- その他

- エンドユーザー別

- 病院とクリニック

- 学術・研究機関

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他の欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他のアジア太平洋

- 中東・アフリカ

- GCC諸国

- 南アフリカ

- その他の中東・アフリカ

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 北米

第6章 競合情勢

- 企業プロファイル

- Silence Therapeutics PLC

- Ionis Pharmaceuticals Inc.

- Novartis Pharma AG

- Arrowhead Pharmaceuticals Inc.

- Stoke Therapeutics Inc.

- Moderna Inc.

- Alnylam Pharmaceuticals Inc.

- Biogen Inc.

- Wave Life Sciences

- Sarepta Therapeutics Inc.

第7章 市場機会と今後の動向

The Nucleic Acid Based Therapeutics Market size is estimated at USD 6.39 billion in 2025, and is expected to reach USD 12.46 billion by 2030, at a CAGR of 14.29% during the forecast period (2025-2030).

The demand for nucleic acid-based therapeutics increased over the past two years as they were effectively used to develop COVID-19 disease therapeutics. As per the article published by MDPI in February 2022, nucleic acid-based technologies, including small interfering RNAs (siRNAs), antisense oligonucleotides (ASOs), and micro RNAs (miRNAs), were the most promising ones to combat the COVID-19 virus. These therapeutics can suppress viral gene expression during and after transcription, presenting significant growth opportunities. As per an article published in MDPI, in August 2022, over 400 RNA-targeting drug development projects were conducted globally, two-thirds of which are in the pre-investigational new drug (pre-IND) stage, one-third in early clinical trials (Phase I or II), about 3% in Phase III, and some awaiting regulatory approval for COVID-19 treatment. Thus, with the increasing development of RNA therapeutics, the studied market is expected to grow over the forecast period.

Factors such as the surging prevalence of genetic disease, growing investments in the healthcare sector and rapid shift of the pharmaceutical industry toward innovative biologics are expected to boost the market's growth over the forecast period.

The increasing prevalence of genetic diseases such as cancer, cystic fibrosis, sickle cell anemia, Duchenne muscular dystrophy, thalassemia, and others is the key factor driving the demand for nucleic acid-based therapeutics to treat diseases by correcting the abnormal expression of specific genes. For instance, according to the Cystic Fibrosis Foundation data published in July 2022, in the United States, 40,000 children and adults have cystic fibrosis (CF). As per the same source, an estimated 105,000 people were diagnosed with the disease in 94 countries in 2022. Thus, the high burden of cystic fibrosis among the population is expected to positively impact the market.

The rising number of investments in nucleic acid therapeutics owing to the high prevalence of chronic, genetic, and other diseases is anticipated to augment the market's growth. For instance, in March 2023, Switch Therapeutics raised USD 52 million in a Series A financing round co-led by Insight Partners and UCB Ventures. The company used these funds to select and advance the development of siRNA therapeutic candidates for the treatment of a central nervous system disease, as well as to advance its RNAi technology. Market players are investing in nucleic acid-based therapy R&D to expand the product portfolio in nucleic acid-based therapy. For instance, in January 2023, Agilent Technologies Inc. invested USD 725 million in nucleic acid-based therapeutics. The investment will double the manufacturing capacity to produce active pharmaceutical ingredients (APIs).

Companies' growing focus on collaborations, partnerships, new product launches, and other initiatives increases the availability of novel therapeutic drugs in the market, which may propel the market's growth. For instance, in February 2023, the CMT Research Foundation partnered with Nanite Inc. to enhance the therapeutic efficacy of antisense oligonucleotides in Charcot-Marie-Tooth disease. In October 2022, Neuway Pharma GmbH and Wacker launched a research project to identify and manufacture RNA-based therapeutics for the treatment of central nervous system disorders with the use of EnPC (Engineered Protein Capsules) protein-based drug delivery technology.

Therefore, owing to the high burden of genetic diseases, increasing investments, and new product launches, the market studied is anticipated to grow over the forecast period. However, the high cost of nucleic acid-based therapeutics research is likely to impede the market's growth.

Nucleic Acid-Based Therapeutics Market Trends

Antisense Oligonucleotides (ASOs) Segment is Expected to Witness Significant Growth Over the Forecast Period

Antisense oligonucleotides (ASOs) are short, single-stranded DNA or RNA molecules that can bind to specific messenger RNA (mRNA) sequences, leading to the degradation of the targeted mRNA or inhibition of its translation into protein. This property makes ASOs a promising therapeutic strategy for a variety of diseases, including genetic disorders, infectious diseases, and cancer. These can target specific disease-causing genes, such as those responsible for the production of abnormal proteins or enzymes that contribute to disease progression.

Some examples of approved ASO therapies include Spinraza (nusinersen) for the treatment of spinal muscular atrophy, Exondys51 (eteplirsen) for the treatment of Duchenne muscular dystrophy, Onpattro (patisiran) for the treatment of hereditary transthyretin-mediated amyloidosis, and Tegsedi (inotersen) for the treatment of hereditary transthyretin-mediated amyloidosis.

The ASOs segment is expected to witness significant growth over the forecast period due to the high demand for antisense oligonucleotide drugs, increasing R&D activities by key players, and new product launches.

The increasing focus of the companies to adopt various business strategies such as partnerships, collaborations, acquisitions, and other initiatives to accelerate the R&D of novel therapeutics for rare and genetic disorders is anticipated to fuel the segment's growth. For instance, in September 2022, Vanda Pharmaceuticals Inc. and OliPassCorporation entered an R&D collaboration agreement to jointly develop a set of antisense oligonucleotide (ASO) molecules based on modified peptide nucleic acids. In February 2021, the US FDA approved Sarepta's Amondys 45 (casimersen) injection for the treatment of Duchenne muscular dystrophy (DMD) in patients with a confirmed mutation of the DMD gene.

Therefore, the segment is expected to grow over the forecast period due to the availability of several antisense oligonucleotide products in the market, increasing company activities, and new product launches.

North America is Expected to Have the Significant Market Share Over the Forecast Period

North America is expected to hold a significant share of the market due to the growing research on various nucleic acid-based therapies, the increasing prevalence of genetic disorders and other chronic disorders, and growing R&D investments in the region.

The rising prevalence of autoimmune diseases among the population increases the demand for nucleic acid-based therapies, which may augment the market's growth. For instance, as per the Autoimmune Association in June 2022, autoimmune diseases comprise approximately 80-150 unique, chronic conditions and affect more than 31 million Americans annually. This shows the high burden of autoimmune disorders among the target population. As per an article published in the Clinical Rheumatology Journal in February 2023, the burden of systemic autoimmune rheumatic diseases (SARDs) is large in Canada, affecting between 2 and 5 cases per 1,000 residents.

The increasing burden of cancer raises the demand for effective and novel drugs that inhibit the progression of cancer cells. This fuels the demand for nucleic acid-based drugs in the region. For instance, according to the Cancer Facts and Figures 2023, about 1.9 million new cancer cases are estimated to be diagnosed in the country in 2023. According to the statistics updated by the Government of Canada in June 2022, nearly 233,900 people in Canada were estimated to be diagnosed with cancer by the end of 2022, and lung, breast, prostate, and colorectal cancers were predicted to be the most diagnosed cancers among the target population in Canada.

The innovative product launches and approvals, partnerships, acquisitions, expansions, and collaborations are anticipated to fuel the market's growth in the region. For instance, in September 2022, Next Generation Manufacturing Canada (NGen) invested USD 10.5 million in a USD 34.8 million project led by OmniaBio Inc. and partners ExCellThera, MorphoCell Technologies, Aspect Biosystems, and Canadian Advanced Therapies Training Institute (CATTI). In December 2021, Novartis AG received approval from the FDA for Leqvio (inclisiran), the first and only small interfering RNA (siRNA) therapy to lower low-density lipoprotein cholesterol (also known as bad cholesterol or LDL-C) with two doses a year, after an initial dose and one at three months.

Nucleic Acid-Based Therapeutics Industry Overview

The nucleic acid-based therapeutics market is moderately fragmented due to the presence of many small and large players globally and regionally. The companies are engaging in the research and development of nucleic acid-based therapeutics for the treatment of various chronic, genetic, and infectious diseases. Some of the key companies in the market are Silence Therapeutics PLC, Ionis Pharmaceuticals Inc., Sarepta Therapeutics, Novartis Pharma AG, Alnylam Pharmaceuticals Inc., and Biogen Inc., among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging Prevalence of Genetic Diseases

- 4.2.2 Growing Investments in Healthcare Sector

- 4.2.3 Rapid Shift of the Pharmaceutical Industry Toward Innovative Biologics

- 4.3 Market Restraints

- 4.3.1 High Cost of Nucleic Acid Research

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value in USD million)

- 5.1 By Product Type

- 5.1.1 RNA interference [RNAi] and short interfering RNAs [siRNAs]

- 5.1.2 Antisense Oligonucleotides (ASOs)

- 5.1.3 Other Product Types

- 5.2 By Application

- 5.2.1 Autoimmune Disorders

- 5.2.2 Infectious Diseases

- 5.2.3 Genetic Disorders

- 5.2.4 Cancer

- 5.2.5 Other Applications

- 5.3 By End User

- 5.3.1 Hospitals and Clinics

- 5.3.2 Academic and Research Institutes

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East & Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East & Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Silence Therapeutics PLC

- 6.1.2 Ionis Pharmaceuticals Inc.

- 6.1.3 Novartis Pharma AG

- 6.1.4 Arrowhead Pharmaceuticals Inc.

- 6.1.5 Stoke Therapeutics Inc.

- 6.1.6 Moderna Inc.

- 6.1.7 Alnylam Pharmaceuticals Inc.

- 6.1.8 Biogen Inc.

- 6.1.9 Wave Life Sciences

- 6.1.10 Sarepta Therapeutics Inc.