|

市場調査レポート

商品コード

1911406

義肢装具市場:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)Prosthetics And Orthotics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 義肢装具市場:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 111 Pages

納期: 2~3営業日

|

概要

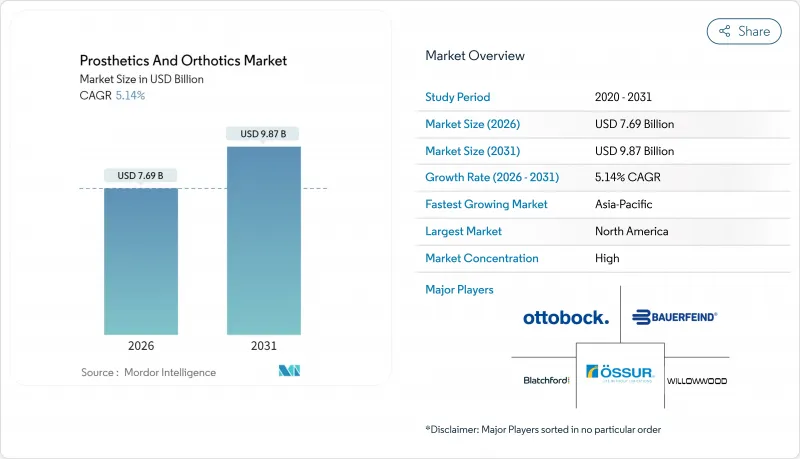

義肢装具市場は2025年に73億1,000万米ドルと評価され、2026年の76億9,000万米ドルから2031年までに98億7,000万米ドルに達すると予測されています。

予測期間(2026-2031年)におけるCAGRは5.14%と見込まれます。

糖尿病関連の四肢切断の増加、急速な人口高齢化、そして着実な保険償還の改善が、持続的な需要の追い風となっています。マイクロプロセッサ制御膝関節やセンサーガイド式装具などの技術革新は、臨床適応症を拡大すると同時に、プレミアム価格設定を支えています。メーカーがサービスネットワークを統合して継続的な収益を確保する動きが加速する中、業界再編が進んでいます。一方、サプライチェーンの混乱や医療従事者の不足は依然として主要な逆風であり、企業が材料の多様化や人材育成への投資を促進する要因となっています。

世界の義肢装具市場の動向と洞察

糖尿病関連切断の急増

糖尿病合併症は現在、下肢切断症例の約3分の2を占めており、糖尿病患者の切断率は21.7%、末梢神経障害の有病率は44.4%に達しています。カナダだけでも、2024年には糖尿病関連の切断手術により7,720件の入院が発生し、医療システムに7億5,000万米ドルの費用がかかりました。アジアの新興国では発生率が最も急速に上昇しており、2030年まで下肢用装具の需要は堅調に推移する見込みです。

高齢化と変形性関節症の負担

アジア太平洋地域の高齢者人口は2050年までに9億2,300万人に達し、地域人口の18%を占めると予測されています。変形性関節症の有病率も同時に上昇しており、装具の使用目的が急性外傷ケアから長期的な可動性維持へと移行しています。日本とシンガポールでは、民間セクターの参入により高機能装具ソリューションへのアクセスが拡大しています。関節手術を回避するための先進的なサポート装置への支払いが保険者によって増加するにつれ、装具の需要は持続的な成長が見込まれます。

高額な機器費用と不均一な償還制度

四肢欠損を抱える230万人のアメリカ人のうち、義肢を装着しているのは半数に満たない状況です。これは主に、保険適用上限や事前承認の障壁が原因です。Genium X4マイクロプロセッサー膝関節のような先進義肢技術は多額の投資を必要とし、その価格は高度な技術と機能的成果の向上を反映しています。これは長期的なコストを相殺する可能性があります。しかし、地域によって異なる保険適用基準が地理的な不平等を助長し、機能的優位性が実証されているにもかかわらず、先進機器の導入を抑制しています。

セグメント分析

2025年の収益の57.65%を装具が占め、慢性関節疾患や脊椎疾患への汎用性を裏付けています。下肢装具は糖尿病関連の足部合併症に対応し、脊椎装具は外傷回復と変性疾患の両方を対象とします。装具による早期介入が手術に代わるケースが増加しており、支払者戦略に影響を与えています。義肢分野は規模こそ小さいもの、知能型膝関節やカスタマイズ可能なソケットによる歩行効率の向上により、6.53%というより高いCAGRで成長しています。糖尿病による切断手術の増加を背景に下肢ソリューションが主流である一方、上肢分野の需要は筋電義肢の進歩と3Dプリントによる個別部品の普及で支えられています。ライナーやモジュラー関節などの部品カテゴリーは、定期的な交換需要を基盤として成長を強化しています。

マイクロプロセッサの継続的な採用と外傷生存率の向上により、予測期間において義肢セグメントの市場規模は業界平均を上回る成長が見込まれます。カスタマイズされた積層造形ソケットは調整回数を削減し、クラウドベースの成果追跡は価値ベースの購入契約を支援することで、義肢導入をさらに促進します。

地域別分析

北米は2025年の収益の41.90%を占め、機能低下の切断者向けマイクロプロセッサー膝関節の償還を認めるメディケア規則改正と、密な臨床医ネットワークに支えられています。米国はイノベーションを主導し、DARPA資金による神経インターフェース試験を実施し、商業スピンアウトを加速させています。カナダでは国民皆保険制度が基本的な肢体装置を保証し、メキシコは中産階級の支出増加とマキラドーラ(輸出加工区)ベースの部品生産の恩恵を受けています。

欧州の成長はドイツ、英国、フランスが牽引しており、包括的な保険制度が高度な装具・義肢をカバーしています。医療機器規則(MDR)に基づく規制調和により越境製品発売が効率化されていますが、償還上限額は地域により異なります。イタリアとスペインは高齢化人口と公的医療予算の増加により成長余地を有しています。

アジア太平洋地域は8.12%のCAGRで最も急速に成長しています。中国では官民連携クリニックによる障害者サービスの拡充が進み、現地メーカーは大量需要に対応するため中価格帯製品の生産規模を拡大中です。インドでは政府補助金と低コスト3Dプリント技術が農村部の切断者における普及を促進しています。日本と韓国はロボット装具とセンサー統合技術で主導的立場を維持し、地域全体への展開前の実証拠点としての役割を果たしています。オーストラリアでは、整備された償還制度と臨床医育成プログラムが、AIを活用した歩行分析技術の早期導入を支えています。

これらの地域的な動向が相まって、義肢装具市場は着実な拡大を続けており、地域ごとの成長率の差異がメーカーに製品ポートフォリオや現地化戦略の最適化機会を提供しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 糖尿病関連切断手術の急増

- 高齢化社会と変形性関節症の負担

- マイクロプロセッサ及び筋電技術における進歩

- 先進国市場における償還範囲の拡大

- AI駆動型予測歩行解析技術の採用状況

- 軍事研究開発の民間機器への波及効果

- 市場抑制要因

- 高価な機器費用と不均一な償還

- 認定義肢装具士(O&P)の不足

- 炭素繊維サプライチェーンの変動性

- 成果連動型償還のリスク

- バリュー/サプライチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース

- 新規参入業者の脅威

- 供給企業の交渉力

- 買い手の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

- 償還環境

第5章 市場規模と成長予測

- タイプ別

- 装具

- 下肢装具

- 上肢装具

- 脊椎装具

- 義肢

- 下肢義肢

- 上肢義肢

- ライナー、ソケット及びモジュラー部品

- 装具

- 技術別

- 従来型/身体動力式

- 電動式/筋電式

- マイクロプロセッサ制御式

- ハイブリッド

- 3Dプリント/積層造形

- エンドユーザー別

- 病院

- 義肢装具クリニック

- リハビリテーションセンター

- 在宅医療環境

- 軍事・退役軍人関連施設

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- その他アジア太平洋地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東・アフリカ

- GCC

- 南アフリカ

- その他中東・アフリカ地域

- 北米

第6章 競合情勢

- 市場集中度

- 市場シェア分析

- 企業プロファイル

- Ossur

- Ottobock

- Hanger Inc.

- Zimmer Biomet

- Blatchford Group

- Fillauer LLC

- Steeper Group

- WillowWood Global

- College Park Industries

- Proteor

- Bauerfeind AG

- DJO Global(Enovis)

- Trulife

- Ortho Europe

- Spinal Technology Inc.

- Thuasne

- 3M Health Care

- Stryker Corporation

- Johnson & Johnson(DePuy Synthes)

- Smith & Nephew