|

市場調査レポート

商品コード

1689955

ガス分離膜:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Gas Separation Membrane - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ガス分離膜:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

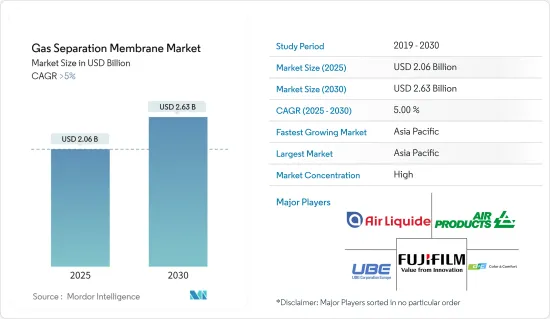

ガス分離膜の市場規模は2025年に20億6,000万米ドルと推定され、2030年には26億3,000万米ドルに達すると予測され、予測期間中(2025-2030年)のCAGRは5%を超えると予測されています。

COVID-19パンデミックはガス分離膜市場にマイナスの影響を与えました。パンデミックは世界のサプライチェーンを混乱させ、ガス分離膜の製造に必要な原材料、部品、装置の入手に影響を与えました。生産と出荷の遅れは、膜システムとコンポーネントの一時的な不足につながりました。しかし、各国が徐々に封鎖規制を解除するにつれて、ガス分離膜システムの需要は回復し始めました。

主なハイライト

- 二酸化炭素分離プロセスにおける膜需要の高まりと、温室効果ガス排出に関する厳しい政府規制がガス分離膜市場を牽引すると予想されます。

- しかし、高温用途での高分子膜の可塑化、新しい膜のスケールアップと採用がガス分離膜市場の成長を妨げると予想されます。

- さらに、混合マトリックス膜(MMM)や用途を拡大する高分子膜の開発は、市場開拓に新たな機会を提供すると予測されています。

- アジア太平洋は、調査した市場において地域別で最大のシェアを占めています。中国、インド、日本におけるガス分離膜の需要増加により、予測期間中に最も急成長する市場になると予想されます。

ガス分離膜市場の動向

窒素生成と酸素富化セグメントが市場を独占する

- 窒素生成と酸素富化は、さまざまな産業用途で不可欠なプロセスです。石油・ガス、化学、エレクトロニクス、飲食品、医薬品などの産業では、ブランケット、パージ、不活性化、パッケージングなどのために窒素が必要とされます。同時に、酸素富化は燃焼、発酵、廃水処理などのプロセスに必要です。

- ガス分離膜を使用した窒素生成と酸素濃縮は、現場でのガス製造を可能にし、圧縮ガスや液化ガスの輸送、貯蔵、取り扱いを不要にします。これにより、物流コストを削減し、サプライチェーンの信頼性を高め、産業運営の安全性を向上させることができます。

- 窒素は飲食品業界で、食品包装の酸素を置換して保存期間を延ばし、鮮度を保つために使用されています。樽を加圧し、ビールやソーダのような炭酸飲料を供給するためにも使用されます。食品加工業務では、窒素は不活性化、ブランケット化、低温化、冷凍化に使用されます。

- 中国のビール産業も世界的に最も急速に拡大しており、その総売上は2023年末までに約1,315億米ドルに達します。

- 窒素と酸素はエレクトロニクス産業にも応用されています。窒素は、汚染を防ぎ正確な大気条件を維持するため、半導体製造工程でキャリアガスとして使用されます。また、ウェーブはんだ付け、リフローはんだ付け、コンフォーマルコーティングプロセスにも使用され、はんだ付けの品質を向上させ、酸化を防止します。

- 半導体産業協会が発表した報告書によると、2023年11月の世界半導体売上高は前年比5.3%増でした。

- 酸素富化は、製鉄、製錬、非鉄金属精錬などの冶金プロセスで、燃焼効率の向上、燃料消費量の削減、プロセスの生産性向上のために使用されます。

- そのため、ガス分離膜の需要は増加し、市場調査に好影響を与えると予想されます。

アジア太平洋地域が市場を独占する

- アジア太平洋地域には、インド、中国、日本、韓国、その他の東南アジア諸国など、急速に成長している国々があります。これらの国々は著しい産業成長を遂げており、石油・ガス、化学、エレクトロニクス、ヘルスケア、飲食品など様々な分野で気体分離膜技術の需要を牽引しています。

- アジア太平洋地域は、化学、エレクトロニクス、半導体、自動車、消費財を生産する多様な産業を擁する製造業の中心地です。ガス分離膜は多くの製造工程で不可欠な部品であり、この地域での高い需要につながっています。

- 世界鉄鋼機関によると、2023年12月の中国の鉄鋼生産量は67.4トンでした。一方、インドは世界第2位の粗鋼生産国に上り詰めました。同国は2022-23会計年度に602万トンを輸入する一方、672万トンの完成鋼を輸出しました。

- さらに、半導体協会によると、2024年1月の中国の半導体売上高は147億6,000万米ドルに急増し、前年から顕著な伸びを示しました。2023年1月の売上高が116億6,000万米ドルであったのと比べると、これはかなりの急上昇です。

- さらに、この地域の酸性ガス分離市場におけるガス分離膜の需要は、この地域におけるエネルギー生産の上昇によって刺激されると予想されます。

ガス分離膜産業の概要

ガス分離膜市場は部分的に統合されており、少数の大手企業が市場を独占しています。市場に参入している主要企業には、Air Products and Chemicals Inc.、UBE Corporation、Air Liquide Advanced Separations、DIC Corporation、FUJIFILM Corporationなどがあります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 二酸化炭素分離プロセスにおけるメンブレン需要の増加

- 温室効果ガス排出に対する政府の厳しい規範

- 抑制要因

- 高温用途におけるポリマー膜の可塑化

- 新しい膜の大規模化と採用

- 業界バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション

- 材料タイプ

- ポリイミドとポリアミド

- ポリスルホン

- セルロースアセテート

- その他の材料タイプ(ナノ構造膜)

- 用途

- 窒素生成および酸素富化

- 水素回収

- 二酸化炭素除去

- 硫化水素除去

- その他の用途(炭酸化)

- 地域

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- マレーシア

- タイ

- インドネシア

- ベトナム

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- スペイン

- トルコ

- ロシア

- ノルディック

- その他欧州

- 南米

- ブラジル

- アルゼンチン

- コロンビア

- その他南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- ナイジェリア

- カタール

- エジプト

- アラブ首長国連邦

- その他中東とアフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア(%)**/ランキング分析

- 主要企業の戦略

- 企業プロファイル

- Air Liquide Advanced Separations

- Air Products and Chemicals Inc.

- DIC CORPORATION

- Evonik Industries AG

- FUJIFILM Corporation

- GENERON

- Honeywell International Inc.

- Linde PLC

- Membrane Technology and Research Inc.

- Parker Hannifin Corp.

- SLB(schlumberger)

- Toray Industries Inc.

- UBE Corporation

第7章 市場機会と今後の動向

- 混合マトリックス膜(MMM)の開発

- 高分子膜の開発と用途拡大

The Gas Separation Membrane Market size is estimated at USD 2.06 billion in 2025, and is expected to reach USD 2.63 billion by 2030, at a CAGR of greater than 5% during the forecast period (2025-2030).

The COVID-19 pandemic negatively affected the gas separation membrane market. The pandemic disrupted the global supply chain, which affected the availability of raw materials, components, and equipment for manufacturing gas separation membranes. Delays in production and shipping led to temporary shortages of membrane systems and components. However, as countries gradually lifted lockdown restrictions, demand for gas separation membrane systems started to rebound.

Key Highlights

- The rising demand for membranes in carbon dioxide separation processes and strict government regulations for GHG emissions are expected to drive the gas separation membrane market.

- However, the plasticization of polymeric membranes in high-temperature applications and the upscaling and adoption of new membranes are expected to hamper the market growth of gas separation membranes.

- Furthermore, developing mixed matrix membranes (MMMs) and polymeric membranes with expanding applications is projected to provide new opportunities for the market studied.

- Asia-Pacific holds the largest share by geography in the market studied. It is expected to be the fastest-growing market over the forecast period due to the rising demand for gas separation membranes in China, India, and Japan.

Gas Separation Membrane Market Trends

The Nitrogen Generation and Oxygen Enrichment Segment to Dominate the Market

- Nitrogen generation and oxygen enrichment are essential processes in various industrial applications. Industries such as oil and gas, chemicals, electronics, food and beverage, and pharmaceuticals require nitrogen for blanketing, purging, inerting, and packaging. At the same time, oxygen enrichment is necessary for processes such as combustion, fermentation, and wastewater treatment.

- Nitrogen generation and oxygen enrichment using gas separation membranes enable onsite gas production, eliminating the need for transportation, storage, and handling of compressed or liquified gases. This reduces logistic costs, enhances supply chain reliability, and improves safety in industrial operations.

- Nitrogen is used in the food and beverage industry to displace oxygen in food packaging to extend the shelf life and preserve freshness. It is used to pressurize kegs and dispense carbonated beverages like beer and soda. In food processing operations, nitrogen is used for inerting, blanketing, cryogenic, and freezing.

- China's beer industry is also experiencing the quickest expansion globally, with its total revenue reaching about USD 131.5 billion by the close of 2023.

- Nitrogen and oxygen find applications in the electronics industry. Nitrogen is used as a carrier gas in semiconductor fabrication processes to prevent contamination and maintain precise atmospheric conditions. It is also used for wave soldering, reflow soldering, and conformal coating processes to improve soldering quality and prevent oxidation.

- According to the report released by the Semiconductor Industry Association, global semiconductor sales increased by 5.3 % year-to-year in November 2023.

- Oxygen enrichment is used in metallurgical processes such as steelmaking, iron smelting, and non-ferrous metal refining to increase combustion efficiency, reduce fuel consumption, and improve process productivity.

- Therefore, the demand for gas separation membranes is expected to increase and thus have a positive impact on the market studied.

Asia-Pacific to Dominate the Market

- Asia-Pacific is home to rapidly growing countries such as India, China, Japan, South Korea, and other Southeast Asian countries. These countries are experiencing significant industrial growth, driving demand for gas separation membrane technologies across various sectors, including oil and gas, chemicals, electronics, healthcare, and food and beverage.

- Asia-Pacific is a central manufacturing hub with a diverse range of industries producing chemicals, electronics, semiconductors, automobiles, and consumer goods. Gas separation membranes are essential components in many manufacturing processes, leading to high demand in the region.

- According to the World Steel Organization, in December 2023, China produced 67.4 metric tons of steel. Meanwhile, India has risen to become the second-largest producer of crude steel globally. The country exported 6.72 million metric tons of finished steel while only importing 6.02 million metric tons in the fiscal year 2022-23.

- Furthermore, according to the Semiconductor Association, in January 2024, China's semiconductor sales soared to USD 14.76 billion, marking a notable rise from the previous year. This is a considerable jump compared to the sales in January 2023, which stood at USD 11.66 billion.

- In addition, the demand for gas separation membranes in the region's acid gas separation market is expected to be stimulated by the rising energy production in this area.

Gas Separation Membrane Industry Overview

The gas separation membrane market is partially consolidated in nature, with a few major players dominating the market. The major companies operating in the market include Air Products and Chemicals Inc., UBE Corporation, Air Liquide Advanced Separations, DIC Corporation, and FUJIFILM Corporation.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Demand for Membranes in Carbon Dioxide Separation Processes

- 4.1.2 Strict Government Norms Toward GHG Emissions

- 4.2 Restraints

- 4.2.1 Plasticization of Polymeric Membranes in High-temperature Applications

- 4.2.2 Upscaling and Adoption of New Membranes

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Material Type

- 5.1.1 Polyimide and Polyamide

- 5.1.2 Polysulfone

- 5.1.3 Cellulose Acetate

- 5.1.4 Other Material Types (Nanostructured Membrane)

- 5.2 Application

- 5.2.1 Nitrogen Generation and Oxygen Enrichment

- 5.2.2 Hydrogen Recovery

- 5.2.3 Carbon Dioxide Removal

- 5.2.4 Removal of Hydrogen Sulphide

- 5.2.5 Other Applications (Carbonation)

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Malaysia

- 5.3.1.6 Thailand

- 5.3.1.7 Indonesia

- 5.3.1.8 Vietnam

- 5.3.1.9 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Spain

- 5.3.3.6 Turkey

- 5.3.3.7 Russia

- 5.3.3.8 NORDIC

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Nigeria

- 5.3.5.4 Qatar

- 5.3.5.5 Egypt

- 5.3.5.6 UAE

- 5.3.5.7 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Air Liquide Advanced Separations

- 6.4.2 Air Products and Chemicals Inc.

- 6.4.3 DIC CORPORATION

- 6.4.4 Evonik Industries AG

- 6.4.5 FUJIFILM Corporation

- 6.4.6 GENERON

- 6.4.7 Honeywell International Inc.

- 6.4.8 Linde PLC

- 6.4.9 Membrane Technology and Research Inc.

- 6.4.10 Parker Hannifin Corp.

- 6.4.11 SLB (schlumberger)

- 6.4.12 Toray Industries Inc.

- 6.4.13 UBE Corporation

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Development of Mixed Matrix Membranes (MMM)

- 7.2 Development in Polymeric Membranes and Expanding Applications