|

市場調査レポート

商品コード

1852210

レディ、トゥ、ドリンクのプロテイン飲料:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Ready-to-Drink Protein Beverages - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| レディ、トゥ、ドリンクのプロテイン飲料:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年09月02日

発行: Mordor Intelligence

ページ情報: 英文 150 Pages

納期: 2~3営業日

|

概要

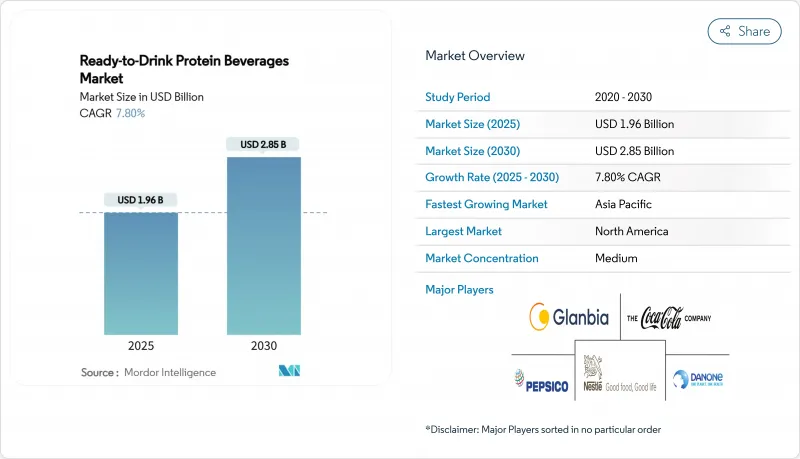

世界のRTD(Ready-to-Drink)プロテイン飲料市場は、2025年に19億6,000万米ドルに達し、2030年にはCAGR 7.80%で28億5,000万米ドルに成長すると予測されています。

この成長は、消費者の嗜好の変化に起因しており、健康意識と現代のライフスタイルにおける便利な栄養オプションの必要性が組み合わされています。消費者は、味と品質を維持しながらフィットネス、筋肉回復、ウェルネスをサポートする携帯型栄養ソリューションをますます好むようになっています。市場の成長要因としては、世界的なフィットネス文化の拡大、都市化、植物性プロテインやアレルゲンフリープロテインに対する需要の高まりなどが挙げられます。動物性タンパク質、特にホエイは、確立された酪農インフラと消費者の信頼により、依然として優位を保っています。しかし、環境意識と持続可能な食生活の嗜好により、エンドウ豆や大豆タンパク質のような植物性代替食品が市場シェアを伸ばしています。北米は、強固な小売インフラ、プレミアム製品の受容、確立されたフィットネス文化により市場を独占しています。アジア太平洋地域は、経済発展、中間層消費者の健康意識の高まり、有利な規制などに支えられ、最も高い成長率を示しています。

世界のレディ、トゥ、ドリンクのプロテイン飲料市場の動向と洞察

消費者の健康意識とウェルネス意識の高まり

消費者の健康意識とウェルネス意識の高まりが、レディ・トゥ・ドリンク(RTD)プロテイン飲料市場の成長を牽引しています。肥満、糖尿病、心血管疾患といったライフスタイルに関連する疾患への懸念から、消費者の健康に対する情報はますます増えています。こうした意識は、より健康的な食習慣や、体重管理、筋肉の健康、全体的な健康をサポートする機能性食品や飲食品の消費増加につながります。米国疾病対策予防センター(CDC)によると、2021年8月から2023年8月までの成人の肥満有病率は40.3%でした。特に40~59歳の成人におけるこの高い肥満率は、ウェルネス志向の製品の必要性を示し、レディ、トゥ、ドリンクのプロテイン飲料に対する消費者の関心を高めています。公衆衛生上の取り組みにもかかわらず肥満率が一貫して高いことは、体重管理、筋肉の健康、総合的な健康をサポートする便利な栄養製品に対する需要が継続していることを示しています。

フィットネスとアクティブ・ライフスタイルの普及拡大

フィットネスとアクティブなライフスタイルの採用が増加していることが、RTD(レディ・トゥ・ドリンク)プロテイン飲料市場の成長を牽引しています。体系化された運動やジム会員への参加の増加は、筋肉の回復、エネルギー補給、身体パフォーマンスをサポートする便利な栄養製品に対する需要を生み出しています。RTD(レディ・トゥ・ドリンク)プロテイン飲料は、高品質なタンパク質を手軽に摂取できるため、運動時に効率的な栄養補給を必要とするフィットネス愛好家のニーズに応えることができます。ヘルス&フィットネス協会(HFA)によると、2024年には6歳以上の米国人が約7,700万人(米国人口の25%)に達し、ジム、スタジオ、フィットネス施設の会員になる見込みです。フィットネススタジオ、ジム、多目的クラブの成長は、出席率の増加と相まって、筋肉増強、体重管理、疲労回復をサポートするプロテインサプリメントに対する需要の高まりを生み出しています。すぐに飲める(RTD)プロテイン飲料は、多忙なスケジュールに対応する栄養ソリューションを必要とする活動的な消費者に特にアピールします。

価格変動と原材料費の高騰

原材料価格の変動とコスト高が、世界のRTD(Ready-to-Drink)プロテイン飲料市場の成長を制約しています。この業界は、ホエイ、大豆、乳製品誘導体のような必須原料に依存しており、その価格は気候条件、サプライチェーンの混乱、貿易政策の変化によって変動します。こうした価格変動は生産コストを上昇させ、メーカーが製品の品質を確保しながら競争力のある価格設定を維持することを困難にしています。米国農務省(USDA)によると、全乳価は2025年には100重量当たり22米ドル、2026年には21.65米ドルになると予測されています。こうした乳価の高騰は、乳由来原料を使用するプロテイン飲料メーカーのコスト構造に直接影響します。価格の不安定さは利益率を低下させることで市場の成長に影響を与え、メーカーは小売価格の引き上げを余儀なくされ、消費者のアクセスが制限される可能性があります。さらに、メーカーは、正確なコスト予測が困難なため、供給計画や戦略的運営における課題に直面しています。

セグメント分析

ホエイプロテインは、確立された乳業インフラと牛乳由来プロテインに対する消費者の親しみに支えられ、2024年においても61.38%のシェアで市場のリーダーを維持します。米国農務省の報告によると、米国の乳製品生産量は2,272億ポンドに達し、牛乳中の脂肪分と脱脂粉乳の含有量の増加により、ホエイプロテインの安定供給が確保されています。このような酪農生産の基盤により、メーカーは需要を確実に満たすことができます。ホエイプロテインの市場での地位は、その栄養価の高さ、生物学的利用能の高さ、筋力回復効果に起因しており、フィットネス愛好家や健康志向の消費者にアピールしています。

エンドウ豆プロテインは、2025年から2030年までのCAGRが9.1%と予測され、最も高い成長の可能性を示しています。この成長は、植物ベースの食生活の採用の増加と、乳製品過敏症や乳糖不耐症の消費者を惹きつけるアレルゲンフリーの特性によるものです。黄色いソラマメに由来するこのタンパク質は、低アレルギーの形で必須アミノ酸を提供し、乳製品や大豆のような一般的なアレルゲンに代わるものを提供します。ビーガン、ベジタリアン、フレキシタリアンの食生活の拡大と、環境および倫理的配慮が相まって、持続可能な選択肢としてのエンドウ豆タンパク質の需要が高まっています。消費者がエンドウ豆プロテインを選ぶ理由は、心血管系の健康効果、体重管理効果、筋肉維持効果にあります。

動物性タンパク質は2024年に市場シェアの71.2%を占めるが、これは主に確立されたサプライチェーンと乳製品由来成分の消費者受容によるものです。乳業インフラは、ホエイやカゼインといった高品質のタンパク質を安定供給しています。これらのタンパク質は、完全なアミノ酸プロファイル、高い生物学的利用能、筋肉増強と回復に役立つことが実証されています。これらの伝統的な蛋白源に対する消費者の嗜好は、その馴染みやすさ、科学的に検証された健康上の利点、粉末、すぐに飲める飲料、栄養補助食品など様々な形態で入手可能なことに起因しています。クリーンラベル、牧草飼育、オーガニックといった選択肢の革新により、市場での地位はさらに強化されています。

植物性タンパク質は、食生活の嗜好の進化と環境意識の高まりによって、2025年から2030年にかけてCAGR 8.6%で急成長を遂げています。エンドウ豆、大豆、レンズ豆、米に由来するタンパク質は、アレルゲンを含まず、ビーガン、ベジタリアン、フレキシタリアンの食生活に適合することから人気が高まっています。温室効果ガスの排出、土地の使用、水の消費など、畜産が環境に与える影響に対する消費者の懸念が、植物由来の代替品の拡大を支えています。さらに、Agriculture and Agri-Food Canadaによると、インドの豆乳生産では2023年に19.5トンの植物性タンパク質原料が使用され、植物性乳製品代替品市場における大豆タンパク質の重要性が強調されています。

地域分析

北米は2024年に世界のプロテイン飲料市場をリードし、38.76%のシェアを占める。このリーダーシップは、フィットネス文化の定着と、一人当たりの消費率を高めるプレミアム機能性飲料の消費者受容に起因します。同地域の高度な小売インフラは多様な流通チャネルを支える一方、消費者は健康志向の製品にプレミアム価格を支払う意欲を示しています。このような市場環境は、特にクリーンラベル、植物由来、減糖処方などの継続的なブランド開拓と製品革新を支えています。米国とカナダが北米市場を独占しており、フィットネス動向の高まり、健康志向、ヘルスクラブ会員率の高さがプロテイン飲料の普及を促進しています。

アジア太平洋は、2025年から2030年までのCAGRが9.16%と予測され、最も急成長している地域です。経済発展と中間層の人口拡大がこの成長を牽引しています。中国、インド、日本、オーストラリアでは、健康志向の高まり、フィットネスとタンパク質豊富な食事の採用、都市化が市場拡大を支えています。メーカー各社は、植物由来やクリーンラベルの選択肢を含め、各地の風味を持つプロテイン飲料を開発することで地域の嗜好に対応しています。政府のウェルネス・プログラム、スポーツジム会員の増加、持続可能なライフスタイルに対する消費者の関心は、市場の成長をさらに加速させる。

欧州は、規制の枠組みが確立され、機能性飲料とその健康効果に対する消費者の意識が高く、成熟した安定した市場を維持しています。南米と中東・アフリカは、都市化、可処分所得の増加、健康意識の高まりを原動力とする新たな成長の可能性を示しています。スポーツ栄養やサプリメントへの関心の高まりとともに、タンパク質が豊富な食品への需要の高まりと飲食品産業の拡大が市場の発展を支えています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 消費者の健康意識とウェルネス意識の高まり

- フィットネスとアクティブなライフスタイルの採用増加

- 便利で持ち運び可能な栄養ソリューションへの需要の高まり

- 植物性菜食の消費者層の拡大

- 市場における継続的な製品革新

- 食事代替および体重管理製品に対する需要の高まり

- 市場抑制要因

- 価格変動と原材料費の高騰

- 代替品の存在と激しい市場競争

- 厳しい規制要件とコンプライアンス基準

- 味と食感の最適化における製品開発の課題

- バリュー/サプライチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- タンパク質タイプ別

- ホエイ

- カゼイン

- 大豆

- エンドウ豆

- その他の情報源

- タンパク源別

- 動物性

- 植物由来

- パッケージングタイプ別

- ボトル

- 缶

- カートン/パウチ

- その他

- 流通チャネル別

- スーパーマーケット/ ハイパーマーケット

- 薬局・ドラッグストア

- 専門小売店

- オンライン小売

- その他のチャネル

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- その他北米地域

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- スペイン

- オランダ

- ポーランド

- ベルギー

- スウェーデン

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- インドネシア

- 韓国

- タイ

- シンガポール

- その他アジア太平洋地域

- 南米

- ブラジル

- アルゼンチン

- コロンビア

- チリ

- ペルー

- その他南米

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

- ナイジェリア

- エジプト

- モロッコ

- トルコ

- その他中東・アフリカ地域

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Abbott Nutrition

- Glanbia PLC

- PepsiCo Inc.

- The Coca-Cola Company

- Post Holdings Inc.(Premier Nutrition)

- Danone SA

- Nestle S.A.

- Halen Brands Inc.

- Koia Inc.

- Labrada Nutrition

- Orgain Inc.

- Fairlife LLC

- Ascent Protein(Leprino Performance Brands)

- Atkins Nutritionals(Simply Good Foods)

- Soylent Nutrition Inc.

- Ripple Foods PBC

- MusclePharm Corp.

- Optimum Nutrition(ON)

- Transparent Labs

- Vega Brands Ltd.