|

|

市場調査レポート

商品コード

1687781

メガネレンズ-市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Spectacle Lens - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| メガネレンズ-市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 115 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

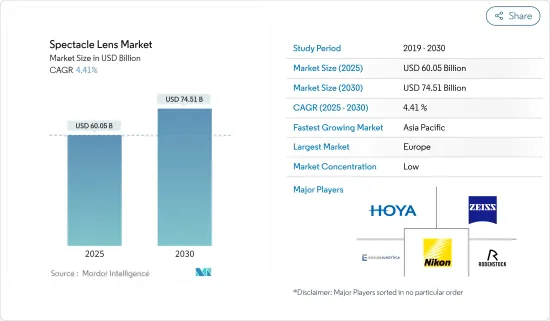

メガネレンズ市場規模は2025年に600億5,000万米ドルと推定・予測され、予測期間中(2025年~2030年)のCAGRは4.41%で、2030年には745億1,000万米ドルに達すると予測されています。

視力障害の増加と視力矯正需要の増加が、予測期間中の市場成長を促進すると予測されます。視力障害の状態や利用可能な視力矯正ソリューションに対する意識の高まりが、メガネレンズの需要を促進しています。スマートフォン、ラップトップ、コンピュータなどのデジタル技術の導入により、デジタル眼精疲労が増加し、視力に関連する問題が生じています。

眼科疾患の負担増はメガネレンズの需要を増加させると予想されます。特定の眼科疾患では、屈折率を維持するために特殊なレンズが必要となり、それによって市場の成長が促進されます。例えば、2022年11月にDigital Medicine and Healthcare Technology誌に掲載された研究によると、近年、物理的な世界からバーチャルな世界へとシフトしているため、デジタル眼精疲労の訴えが増加しています。また、ブルーライトレベルが低いと、子供の近視や近眼の開発リスクが高まる可能性があり、メガネレンズの需要がさらに高まる。

さらに、2023年緑内障レポートによると、緑内障は世界第2位の失明原因であり、米国では2023年に約300万人がこの病気と診断されました。このように、緑内障の負担が大きいことから、視力を改善するためのメガネレンズの需要が増加すると予想され、予測期間中の市場の成長に寄与すると思われます。

また、矯正レンズの需要増に対応するための製品上市や承認の増加も、調査対象市場の成長に寄与すると予想されます。例えば、2023年11月、Shamir Optical Industry社は、最新のイノベーションである最先端の近視管理メガネレンズ、Shamir Optimeeを発表しました。この新商品は、革新的なシャミール・フォーカスフロー・テクノロジーを搭載しており、子供の処方箋に合わせた明確な中央垂直ゾーンを確保します。

同様に、2022年12月、香港理工大学(PolyU)が支援する新興企業であるビジョン・サイエンス・アンド・テクノロジー(VST)は、近視の進行を遅らせることを目的とした革新的なメガネレンズを発売しました。VSTはPolyUが開発した2つの特許技術を取り入れ、子供たちの視力の健康を守っています。

このように、眼科疾患や視力障害の負担増、市場参入企業による製品発売など、前述のすべての要因が予測期間中の市場成長に寄与すると予想されます。しかし、レンズの品質問題が予測期間中の市場成長の妨げになると予想されます。

メガネレンズ市場の動向

処方眼鏡セグメントは予測期間中に著しい成長が見込まれる

処方眼鏡は、装用者の特定の視力欠陥を矯正するためにレンズがカスタマイズされた眼鏡です。近視、遠視、老眼、乱視などの状態を改善または矯正するように設計されています。眼疾患の負担が増加するにつれて、処方眼鏡の需要も増加し、予測期間中にこの分野の成長に寄与すると予想されます。

国際近視研究所(IMI)は、2023年最新版「Facts and Findings Infographic」を発表し、2050年までに世界人口の50%が近視の影響を受け、10%が強度近視になると予測しています。その結果、近視と老眼による屈折異常の罹患率の増加が処方レンズの需要を促進しており、これがセグメントの成長にさらに貢献すると予想されています。

また、処方レンズを提供し、ユーザーに最大限の利益を提供するための主要プレイヤーの継続的な努力も、このセグメントの成長を促進すると予想されます。加えて、処方眼鏡と視力矯正の分野で評判の高い企業が、世界の目の健康増進に尽力していることも、このセグメントの成長を促進する要因です。

例えば、世界の眼科企業であるエシロール・インターナショナルは、2023年最新版によると、2022年に処方レンズを世界の約74億人に提供しています。さらに、2024年5月には、革新的なアイウェアブランドであるNEVENが、製造業者であるRobertson Optical Laboratories Inc.との提携により、高品質で手頃な価格の処方眼鏡の新ラインを発売しました。したがって、このような市場プレーヤーの存在は、予測期間中の同分野の成長を促進すると予想されます。

予測期間中、北米が市場で大きなシェアを占めると予想される

北米は世界のメガネレンズ市場で大きなシェアを占めると予想されます。米国とカナダはヘルスケアシステムが整備されているため、製品開発に従事する世界の市場プレーヤーが多数存在します。さらに、対象人口の間で眼障害の有病率が増加していることも、同地域の市場成長を後押しする重要な要因となっています。

視力障害の負担増はメガネレンズの需要を増加させ、市場成長を後押しすると予想されます。例えば、米国疾病予防管理センター(CDC)の2022年12月のデータによると、米国の40歳以上の1,200万人以上が毎年視力障害に苦しんでいます。さらに、主な視力障害の経済コストは、2050年までに3,730億米ドルに増加すると予測されています。これらの数字は、北米の対象人口に大きな負担がかかっていることを示しています。

さらに、米国では高齢者人口が増加の一途をたどっており、主要人口層の視力矯正へのシフトと相まって、ほとんどの種類の眼鏡の使用率が絶対的に増加しています。例えば、2023年5月に発表された国勢調査政府のデータによると、65歳以上のアメリカ人の数は2022年の5,800万人から2050年には8,200万人に増加すると予測されています。この動向は、予測期間中の市場の成長に寄与すると予想されます。

米国では複数の企業がメガネレンズ市場で主要な役割を果たし、数多くの製品の発売やイノベーションを通じて市場の成長を加速させています。例えば、2022年3月、EssilorLuxotticaとCooperCompaniesはSightGlass Visionの合弁契約を締結しました。SightGlass Visionの拡散光学技術は、何千ものマイクロドットをレンズに組み込み、光をソフトに散乱させて網膜上のコントラストを下げ、子供の近視進行を抑えることを意図しています。

その結果、このような開発と対象人口の眼障害の負担が、北米のメガネレンズ市場の成長を促進すると予想されます。

メガネレンズ産業の概要

メガネレンズ市場は断片化されており、複数の大手企業で構成されています。市場シェアの面では、現在これらの主要企業のうち数社が市場を独占しています。Carl Zeiss Meditec AG、EssilorLuxottica(エシロール)、HOYA Corporation(セイコーオプティカルプロダクツ)、GKB Ophthalmics Ltdといった主要市場プレイヤーの存在が、市場全体の競争企業間の敵対関係を高めています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査想定と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 視力矯正需要の増加

- 視力障害の増加

- 市場抑制要因

- レンズの品質問題

- 業界の魅力- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- タイプ別

- 単焦点

- 遠近両用

- 遠近両用

- 累進屈折力

- コーティングタイプ別

- 反射防止コーティング

- 傷防止コーティング

- 防曇コーティング

- UVプロテクション

- その他のコーティング

- 用途別

- 処方用ガラス

- OTCリーディンググラス

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- その他の欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他のアジア太平洋

- 中東・アフリカ

- GCC

- 南アフリカ

- その他の中東・アフリカ

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 北米

第6章 競合情勢

- 企業プロファイル

- Carl Zeiss AG(Carl Zeiss Meditec AG)

- EssilorLuxottica(Essilor)

- GKB Ophthalmics Ltd

- Hoya Corporation(Seiko Optical Products Co. Ltd)

- Rodenstock GmbH

- Tokai Optical Co. Ltd

- Nikon Corporation

- Fielmann AG

- Wanxin Optics

- Inspecs Group PLC(Norville(20/20)Ltd)

第7章 市場機会と今後の動向

The Spectacle Lens Market size is estimated at USD 60.05 billion in 2025, and is expected to reach USD 74.51 billion by 2030, at a CAGR of 4.41% during the forecast period (2025-2030).

Increasing optical disorders and the growing demand for vision correction are anticipated to fuel market growth during the forecast period. The rising awareness of vision impairment conditions and available vision correction solutions is driving the demand for spectacle lenses. The adoption of digital technologies, such as smartphones, laptops, and computers, has led to an increase in digital eye strain, resulting in vision-related problems.

The growing burden of ophthalmic diseases is expected to increase demand for the spectacle lens. Certain ophthalmic conditions require specialized lenses to maintain the refractive index, thereby boosting market growth. For instance, according to a study published in the Digital Medicine and Healthcare Technology journal in November 2022, the shift from the physical to the virtual world in recent years has led to an increase in complaints of digital eye strain. Low blue light levels may also increase the risk of developing myopia and near-sightedness in children, further increasing the demand for spectacle lenses.

In addition, according to the 2023 Glaucoma Report, glaucoma was the second leading cause of blindness worldwide, and roughly 3 million people in the United States were diagnosed with the disease in 2023. Thus, the high glaucoma burden is expected to increase demand for spectacle lenses to improve vision, which is likely to contribute to the market's growth over the forecast period.

The increasing product launches and approvals to meet the growing demand for corrective lenses are also expected to contribute to the growth of the market studied. For instance, in November 2023, Shamir Optical Industry unveiled its latest innovation, the Shamir Optimee, a cutting-edge myopia management spectacle lens. This new offering features the innovative Shamir Focusflow technology, ensuring a distinct central vertical zone tailored to the child's prescription.

Similarly, in December 2022, Vision Science and Technology Co. Ltd (VST), a start-up backed by the Hong Kong Polytechnic University (PolyU), launched an innovative spectacle lens that aims to slow down myopia progression. VST incorporated two patented technologies developed by PolyU to safeguard children's vision health.

Thus, all aforementioned factors, such as the growing burden of ophthalmic diseases and vision impairment and product launches by the market players, are expected to contribute to the market's growth over the forecast period. However, quality issues of lenses are expected to hamper the market's growth over the forecast period.

Spectacle Lens Market Trends

The Prescription Glass Segment is Expected to Exhibit the Significant Growth over the Forecast Period

Prescription glasses are eyeglasses whose lenses are customized to correct the wearer's specific vision defects. They are designed to improve or correct conditions such as myopia (near-sightedness), hyperopia (farsightedness), presbyopia, and astigmatism. As the burden of eye diseases increases, so does the demand for prescription glasses, which is expected to contribute to the segment's growth during the forecast period.

The International Myopia Institute (IMI) released its 2023 update on the Facts and Findings Infographic, projecting that 50% of the global population will be affected by myopia, with 10% experiencing high myopia by 2050. As a result, the rising incidence of refractive errors due to myopia and presbyopia is driving the demand for prescription lenses, which is expected to further contribute to segmental growth.

Major players' continuous efforts to provide prescription lenses and offer maximum benefits to users are also expected to fuel the segment's growth. Additionally, the presence of reputable players in prescription glasses and vision correction committed to enhancing global eye health is another factor driving the segment's growth.

For example, Essilor International, a global ophthalmology company, provided prescription lenses to nearly 7.4 billion people worldwide in 2022, according to its 2023 update. Additionally, in May 2024, Innovative eyewear brand NEVEN launched a new line of high-quality, affordable prescription glasses in partnership with manufacturer Robertson Optical Laboratories Inc. Therefore, the presence of such market players is expected to fuel the segment's growth during the forecast period.

North America is Expected to Hold a Significant Share of the Market Over the Forecast Period

North America is expected to hold a significant share of the global spectacle lens market. The United States and Canada have well-structured healthcare systems, resulting in numerous global market players engaged in product development. Additionally, the increasing prevalence of eye disorders among the target population is a significant factor fueling the market's growth in the region.

The growing burden of vision impairment is expected to increase demand for spectacle lenses, thereby boosting the market growth. For instance, according to the Centers for Disease Control and Prevention's (CDC) December 2022 data, over 12 million people aged over 40 in the United States suffered from vision impairment every year. Moreover, the economic cost of major vision problems is projected to increase to USD 373 billion by 2050. These figures indicate a significant burden of disease among the target population in North America.

Furthermore, the constant increase in the elderly population in the United States, coupled with a shift toward vision correction usage among key demographics, has led to an absolute increase in the usage rates for most types of eyewear in the country. For instance, according to the Census Government data published in May 2023, the number of Americans aged 65 and older was projected to increase from 58 million in 2022 to 82 million by 2050. This trend is expected to contribute to the market's growth over the forecast period.

Several companies in the United States have been playing major roles in the spectacle lens market, accelerating the market's growth through numerous product launches and innovations. For instance, in March 2022, EssilorLuxottica and CooperCompanies finalized their joint venture agreement for SightGlass Vision. SightGlass Vision's diffusion optics technology incorporates thousands of micro-dots into the lens, softly scattering light to reduce contrast on the retina and intended to reduce myopia progression in children.

Consequently, such developments and the burden of eye disorders among the target population are expected to propel the growth of the spectacle lens market in North America.

Spectacle Lens Industry Overview

The spectacle lens market is fragmented and consists of several major players. In terms of market share, few of these major players currently dominate the market. The presence of major market players, such as Carl Zeiss Meditec AG, EssilorLuxottica (Essilor), Hoya Corporation (Seiko Optical Products Co. Ltd), and GKB Ophthalmics Ltd, is increasing the overall competitive rivalry of the market.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumption and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Demand for Vision Correction

- 4.2.2 Increasing Prevalence of Optical Disorders

- 4.3 Market Restraints

- 4.3.1 Quality Issues of Lens

- 4.4 Industry Attractiveness - Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD million)

- 5.1 By Type

- 5.1.1 Single Vision

- 5.1.2 Bifocal

- 5.1.3 Trifocal

- 5.1.4 Progressive

- 5.2 By Coating Type

- 5.2.1 Anti-reflective Coating

- 5.2.2 Scratch-Resistant Coating

- 5.2.3 Anti-fog Coating

- 5.2.4 UV Protection

- 5.2.5 Other Coating Types

- 5.3 By Usage

- 5.3.1 Prescription Glass

- 5.3.2 OTC Reading Glass

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 United Kingdom

- 5.4.2.2 Germany

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Carl Zeiss AG (Carl Zeiss Meditec AG)

- 6.1.2 EssilorLuxottica (Essilor)

- 6.1.3 GKB Ophthalmics Ltd

- 6.1.4 Hoya Corporation (Seiko Optical Products Co. Ltd)

- 6.1.5 Rodenstock GmbH

- 6.1.6 Tokai Optical Co. Ltd

- 6.1.7 Nikon Corporation

- 6.1.8 Fielmann AG

- 6.1.9 Wanxin Optics

- 6.1.10 Inspecs Group PLC (Norville (20/20) Ltd)