|

市場調査レポート

商品コード

1686660

バイオエタノール:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Bioethanol - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| バイオエタノール:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 200 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

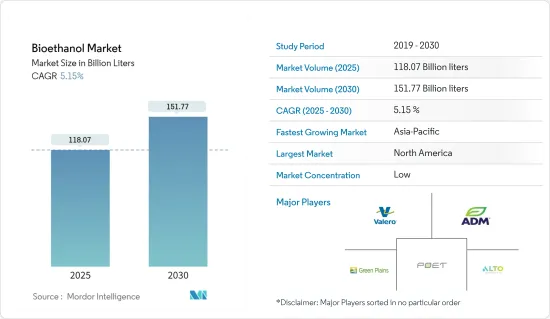

バイオエタノール市場規模は2025年に1,180億7,000万リットルと推定され、予測期間(2025-2030年)のCAGRは5.15%で、2030年には1,517億7,000万リットルに達すると予測されます。

バイオエタノール市場は、サプライチェーンの混乱によりCOVID-19の悪影響を受けました。しかし、2021年には市場は回復しました。市場を牽引する主な要因は、政府のイニシアチブの高まりと、米国でエタノールの割合が高いガソリンの販売規制が強化されたことです。

主なハイライト

- 短期的には、有利なイニシアチブの増加、規制機関による混合義務付け、化石燃料の使用とバイオ燃料の必要性に対する環境問題の高まりが市場成長の要因となっています。

- 電気自動車需要の高まりによる燃料自動車の廃止とバイオブタノールへのシフトが市場成長の阻害要因です。

- 第二世代バイオエタノール生産の開発と、航空産業におけるバイオエタノールのようなバイオ燃料の消費の増加は、将来的に市場に機会をもたらすと思われます。

- 北米が世界市場を独占し、米国が最も大きな消費量を占めています。

バイオエタノール市場の動向

自動車・運輸分野での用途拡大

- バイオエタノールの最も広範な用途は、自動車および運輸産業における燃料および燃料添加剤です。バイオエタノールは、従来のガソリンと並んで、自動車用ガソリンエンジンの燃料として使用されます。また、多くの種類のガソリンに使用されるオクタン価向上剤であるETBE(エチル-ターシャリーブチル-エーテル)を生産することもできます。

- バイオエタノールを従来の燃料に混合することで、再生可能性が向上します。E10エネルギーは、エタノールが10%含まれているため、このような名前が付けられました。バイオエタノールは低炭素燃料であり、輸送産業の脱炭素化に貢献する可能性があります。

- 米国では過去30年にわたり、バイオエタノールをオクタン価向上剤やガスエクステンダーとして使用した場合、ガソリン販売業者に税制上の優遇措置が設けられてきました。これにより、この分野でのバイオエタノールの利用が促進されました。

- 米国のバイオ燃料製造業者は、低炭素燃料製造のための資金援助と重要な税額控除を盛り込んだ最新の法律から後押しを受けました。エタノールとバイオディーゼルの混合燃料用の貯蔵タンクや関連設備を設置するバイオ燃料インフラ整備のために、5億米ドルの資金が割り当てられました。

- OICAのデータによると、2022年の自動車生産台数は2021年比で6%増加しました。2022年の世界の自動車生産台数は約8,502万台でした。

- 2022年の自動車生産台数は、アジア・オセアニア地域が5,002万台、南北アメリカ地域が1,775万台で、それぞれ2020年比で7%近く、10%近い増加を記録しました。しかし、欧州の2022年の生産台数は1,621万台で、2021年の生産台数から1%減少しました。

- さらに、米国エネルギー省は2021年に、2050年までに排出量を正味ゼロにするという米国のコミットメントを強化するため、航空機のような大型輸送手段用の化石燃料代替となる低コストのバイオ燃料の生産に特化した研究開発プロジェクトに6,470万米ドルの資金を提供すると発表しました。

- 様々な経済圏がバイオエタノールの燃料消費量を増やす計画を発表しており、バイオエタノールの需要は予測期間中に急増する可能性が高いです。

市場を独占する北米地域

- 北米地域がバイオエタノール市場シェアを独占しています。米国は世界最大のバイオエタノール生産国で、ブラジル、中国、インド、カナダがこれに続きます。また、バイオエタノールの最大消費国でもあります。

- 近年、バイオエタノールの生産量は、再生可能燃料基準(RFS)の目標値引き上げと国内ガソリン消費量の増加により増加しており、現在ではそのほとんど全てに10%のエタノールが混合されています。

- 2022年の北米の自動車生産台数は、2021年の1,346万台に対して約1,479万台でした。

- 同国の登録自動車2億6,300万台のうち、約93%がE15で走行可能です。さらに、米国では約2,200万台のフレックス燃料車(FFV)がE85までのエタノール混合燃料で走行できます。

- カナダのクリーン燃料基準は、液体燃料(ガソリン、ディーゼル、家庭用暖房油)供給業者に対し、カナダ国内で使用するために生産・販売する燃料の炭素強度を時間をかけて段階的に削減するよう求めており、その結果、2030年までにカナダで使用される液体燃料の炭素強度を約13%(2016年レベルより)削減することになります。

- カナダ政府が最近、低炭素・ゼロエミッション燃料基金に15億米ドルを投資したことで、水素やバイオ燃料のような低炭素燃料の現地生産・導入への支援が強化される可能性もあります。

- 上記のような要因から、調査対象市場の需要は北米地域で増加すると予想されます。

バイオエタノール産業の概要

バイオエタノール市場は適度に断片化されています。同市場の主要企業(順不同)には、POET LLC、Valero、ADM、Green Plains Inc.、Alto Ingredients Inc.などがあります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 規制当局による好意的な取り組みと混合義務化の増加

- 化石燃料の使用による環境問題の高まりとバイオ燃料の必要性

- 抑制要因

- 電気自動車需要の高まりによる燃料自動車の廃止

- バイオブタノールへのシフト

- 産業バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション

- 原料タイプ

- サトウキビ

- トウモロコシ

- 小麦

- その他の原料タイプ

- 用途

- 自動車および輸送

- 飲食品

- 医薬品

- 化粧品・パーソナルケア

- その他の用途

- 地域

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- その他欧州

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- その他中東とアフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア(%)**/ランキング分析

- 主要企業の戦略

- 企業プロファイル

- Abengoa

- ADM

- Alto Ingredients Inc.

- Blue Bio Fuels Inc.

- Cenovus Inc.

- Cristalco

- Cropenergies AG

- Ethanol Technologies

- Granbio Investimentos SA

- Green Plains Inc

- Henan Tianguan Group Co. Ltd

- Jilin Fuel Ethanol Co. Ltd

- KWST

- Lantmannen

- Poet LLC

- Raizen

- Sekab

- Suncor Energy Inc.

- Tereos

- Valero

- Verbio Vereinigte Bioenergie AG

第7章 市場機会と今後の動向

- 第二世代バイオエタノール生産の開発

- 航空業界におけるバイオ燃料消費の増加

The Bioethanol Market size is estimated at 118.07 billion liters in 2025, and is expected to reach 151.77 billion liters by 2030, at a CAGR of 5.15% during the forecast period (2025-2030).

The Bioethanol Market was adversely affected by COVID-19 due to disruptions in the supply chain. However, the market rebounded in 2021. The major factors driving the market were the increasing government initiatives and the increased restrictions on marketing gasoline containing a higher percentage of ethanol in the United States.

Key Highlights

- Over the short term, increasing favorable initiatives, blending mandates by regulatory bodies, and rising environmental concerns about the use of fossil fuels and the need for biofuels are the factors driving the market's growth.

- Phasing out of fuel-based vehicles due to rising demand for electric cars and shifting focus to bio-butanol are the factors hindering the market's growth.

- Developing second-generation bio-ethanol production and increasing consumption of biofuels like bioethanol in the aviation industry is likely to create opportunities for the market in the future.

- North America dominated the global market, with the United States having the most significant consumption.

Bioethanol Market Trends

Increasing Usage in the Automotive and Transportation Sector

- The most extensive bioethanol applications are fuel and fuel additives in the automotive and transportation industries. It is used alongside conventional petrol to fuel petrol engines in road vehicles. It can also produce ETBE (ethyl-tertiary-butyl-ether), an octane booster used in many types of petrol.

- Blending bioethanol with conventional fuels improves its renewability. E10 energy is so named because it contains 10% ethanol. Bioethanol is a low-carbon fuel that may help to decarbonize the transport industry.

- In the United States, tax incentives have been provided to gasoline marketers for using bio-ethanol as an octane enhancer and gas extender over the past three decades. This has driven boosted the usage of bio-ethanol in this sector.

- Biofuel producers in the United States received a boost from the latest legislation, which encompasses funding and critical tax credits for producing low-carbon fuels. Funding of USD 500 million was allocated for biofuel infrastructure improvements by installing storage tanks and related equipment for ethanol-biodiesel blends.

- In 2022, according to OICA data, the overall production of automobiles increased by 6% compared to 2021. The global automotive production in 2022 was around 85.02 million units.

- The Asia-Oceania and Americas regions recorded automotive production of 50.02 million and 17.75 million units in 2022, registering an increase of nearly 7% and 10%, respectively, compared to 2020. However, Europe recorded a production of 16.21 million units in 2022, a decrease of 1% from the production achieved in 2021.

- Furthermore, in 2021, the United States Department of Energy announced to provide USD 64.7 million in funds for research and development projects dedicated to producing low-cost biofuels as fossil-fuel replacements for heavy-duty transportation like airplanes to bolster America's commitment to reaching net-zero emissions by 2050.

- With various economies announcing their plans to increase bio-ethanol consumption in fuels, the demand for bio-ethanol will likely surge during the forecast period.

North America Region to Dominate the Market

- The North American region is dominating the bioethanol market share. The United States is the largest producer of bioethanol globally, followed by Brazil, China, India, and Canada. It is also the largest consumer of bioethanol.

- In recent years, bioethanol production has increased due to higher renewable fuel standard (RFS) targets and growth in domestic motor gasoline consumption, almost all of which is now blended with 10% ethanol by volume.

- In 2022, the overall production of automobiles in North America was around 14.79 million units compared to 13.46 million units in 2021.

- Around 93% of the country's 263 million registered automobiles may operate on E15. Furthermore, around 22 million flex-fuel vehicles (FFVs) in the United States can run on ethanol blends up to E85.

- The Canadian Clean Fuel Standard requires liquid fuel (gasoline, diesel, and home heating oil) suppliers to gradually reduce the carbon intensity of the fuels they produce and sell for use in Canada over time, resulting in a reduction in the carbon intensity of liquid fuels used in Canada of approximately 13% (below 2016 levels) by 2030.

- Some initiatives include the Canadian government's recent USD 1.5 billion investment in a Low-carbon and Zero-Emissions Fuels Fund, which may enhance support for local production and adoption of low-carbon fuels like hydrogen and biofuels.

- Due to all the factors mentioned above, the demand in the market studied is expected to increase in the North American region.

Bioethanol Industry Overview

The Bioethanol Market is moderately fragmented. Some major players in the market (not in any particular order) include POET LLC, Valero, ADM, Green Plains Inc., and Alto Ingredients Inc., among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Report

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Favorable Initiatives and Blending Mandates by Regulatory Bodies

- 4.1.2 Rising Environmental Concerns by the Use of Fossil Fuels and Need for the Bio-fuels

- 4.2 Restraints

- 4.2.1 Phasing out of Fuel-based Vehicles Due to Rising Demand for Electric Vehicles

- 4.2.2 Shifting Focus to Bio-butanol

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Feedstock Type

- 5.1.1 Sugarcane

- 5.1.2 Corn

- 5.1.3 Wheat

- 5.1.4 Other Feedstock Types

- 5.2 Application

- 5.2.1 Automotive and Transportation

- 5.2.2 Food and Beverage

- 5.2.3 Pharmaceutical

- 5.2.4 Cosmetics and Personal Care

- 5.2.5 Other Applications

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Abengoa

- 6.4.2 ADM

- 6.4.3 Alto Ingredients Inc.

- 6.4.4 Blue Bio Fuels Inc.

- 6.4.5 Cenovus Inc.

- 6.4.6 Cristalco

- 6.4.7 Cropenergies AG

- 6.4.8 Ethanol Technologies

- 6.4.9 Granbio Investimentos SA

- 6.4.10 Green Plains Inc

- 6.4.11 Henan Tianguan Group Co. Ltd

- 6.4.12 Jilin Fuel Ethanol Co. Ltd

- 6.4.13 KWST

- 6.4.14 Lantmannen

- 6.4.15 Poet LLC

- 6.4.16 Raizen

- 6.4.17 Sekab

- 6.4.18 Suncor Energy Inc.

- 6.4.19 Tereos

- 6.4.20 Valero

- 6.4.21 Verbio Vereinigte Bioenergie AG

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Development of Second-generation Bio-ethanol Production

- 7.2 Increasing Consumption of Bio-fuels in the Aviation Industry