|

市場調査レポート

商品コード

1444714

微生物農薬:市場シェア分析、業界動向と統計、成長予測(2024~2029年)Microbial Pesticides - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 微生物農薬:市場シェア分析、業界動向と統計、成長予測(2024~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

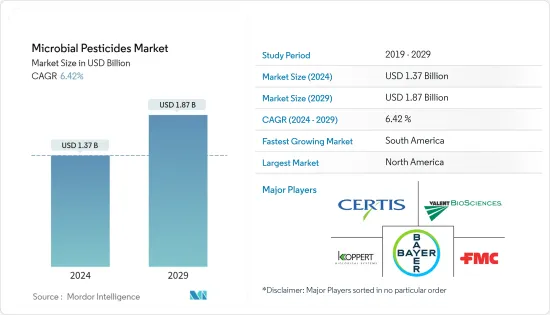

微生物農薬市場規模は2024年に13億7,000万米ドルと推定され、2029年までに18億7,000万米ドルに達すると予測されており、予測期間(2024年から2029年)中に6.42%のCAGRで成長します。

主なハイライト

- 作物保護における化学農薬または合成農薬の蔓延が続いている一方で、人間と動物の健康および環境に対する懸念が微生物農薬の増加を促進する重要な役割を果たしています。いくつかの国は、残留農薬の数の規制に重点を置き、輸入数に関して厳格なアプローチを採用しています。食品の安全性と品質に対する需要の高まりにより、合成殺虫剤よりも微生物殺虫剤の人気が高まっています。

- 統合害虫管理プログラム(IPM)に微生物殺虫剤を組み込むと、作物の収量に影響を与えることなく、合成殺虫剤の必要性が大幅に削減されます。食糧農業機関(FAO)によると、2021年の総収穫面積は14億6,500万ヘクタールで、微生物や昆虫の侵入が少ない作物生産の需要の増加により、前年の14億4,270万ヘクタールを上回った。

- 耕作可能な土地が減少する中、技術の変化が農業の生産性を高める主な促進要因となっています。収入の増加、知識の向上、コミュニケーションチャネルの向上により、多くの国の消費者は、オーガニックな方法で生産された高品質で低コストの食品を求めています。同時に、天然資源を保護し、環境圧力を制限し、農村の存続可能性と動物福祉に一層の注意を払う技術を使用して食品を生産することへの需要も高まっています。したがって、政府は持続可能な農業システムのために新しい農業技術を導入することを主張しています。

微生物農薬市場動向

有機土地の増加と新しい農業技術の適応

- 新しい農業技術の適応が進むにつれて、微生物殺虫剤などの製品がより安全に現場で使用されるようになりました。持続可能な農業の支援と主流の農業への受け入れにより、農家は化学農薬の使用を最小限に抑え、それによってコスト、生産性、環境を節約することができます。持続可能な農業における微生物農薬の使用は、いくつかの環境的および社会的懸念に対処し、生産者、労働者、消費者に革新的で経済的に実行可能な機会を提供します。これは、微生物殺虫剤市場の成長の主要な推進力の1つです。

- オーガニック貿易協会(OTA)によると、2020年の米国のオーガニック売上高は619億2,000万米ドルで、前年比12.4%の成長率となった。経済的な観点からこのオーガニック売上の成長率を、その半分以下の成長率である4.9%に達した食品および非食品の米国市場全体と比較すると、消費者行動がオーガニックへ移行していることは明らかです。

- オーガニック食品は、有毒な殺虫剤、合成肥料、遺伝子組み換え生物(GMO)を含まない食品を提供する農業システムで生産されるため、人気を集めています。そのため、オーガニック製品は高品質とみなされ、健康と環境の両方にとってより安全であると考えられています。

北米が市場を独占

- 化学除草剤や殺虫剤の影響に対する意識が高まるにつれ、特に統合的な雑草管理の場合、代替品として生物除草剤を採用することができます。生物除草剤は、植物毒、病原体、およびその他の微生物からなる除草剤です。生物学的雑草防除として使用されます。

- 生物除草剤は、真菌、細菌、原生動物などの微生物からの化合物および二次代謝産物、または植物毒性のある植物の残留物、抽出物、または他の植物種に由来する単一化合物として得られます。この地域の需要は、グリーン農業への関心の高まりや、再登録や性能の問題により従来の製品の多くが失われているなど、多くの要因によって動かされています。

- 製品開発により、微生物殺虫剤の需要も高まっています。現在の市場では、従来の化学殺虫剤と競合し、それを補うことができる、より優れた生物学的活性成分および製品が入手可能です。微生物生物農薬部門は、持続可能な食料生産に対する意識の高まり、化学物質の過剰使用に対する農家の懸念、化学作物保護の費用の増加によって推進されています。この知識の増加は、米国の生物部門の急成長に反映されており、微生物殺虫剤を使用する絶好の機会を提供しています。

- さらに、2021年6月にEPAは、新しい微生物活性成分であるBacillus velezensis RTI301株および/またはBacillus subtilis RTI477株を含む5つの生物農薬製品を登録しました。これらの生物農薬製品は、2つの製造製品と3つの最終用途製品で構成されており、天然細菌を利用して苗木や農作物を真菌の増殖から保護します。 EPAはまた、用途が登録されている製品は対象外の生物種には影響を及ぼさないと結論付けた。したがって、国内で新しい微生物成分を承認するためにEPAがとったこのような積極的な取り組みは、微生物農薬市場の成長の原動力となっています。

微生物農薬業界の概要

微生物殺虫剤の市場は非常に細分化されており、多数の企業が市場シェアの大部分を支配しており、さらにいくつかの中小企業やプライベートブランドも存在しています。 Bayer CropScience AG、FMC Corporation、Koppert Biological Systems、Valent Biosciences Corporation、およびCertis USA LLCは、調査対象市場における著名な企業の一部です。新製品の発売、提携、買収は、国内市場の大手企業が採用する主要戦略です。イノベーションと拡張に加えて、研究開発への投資と新しい製品ポートフォリオの開発は、今後数年間で重要な戦略となる可能性があります。微生物殺虫剤を開発する企業間の大規模な買収は、バイオベース製品への注目が急速に高まっていることを示しています。市場関係者は、拡大するマーケットプレースで生物学調査部門を多様化するために、この市場に多額の投資を行っています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替製品の脅威

- 競争企業間の敵対関係の激しさ

第5章 市場セグメンテーション

- 成分の種類

- 細菌ベースの殺虫剤

- 菌類ベースの殺虫剤

- ウイルスベースの殺虫剤

- その他の成分の種類

- 製品タイプ

- 微生物殺菌剤

- 微生物殺虫剤

- その他の製品タイプ

- 用途

- 穀物とシリアル

- 豆類と油糧種子

- 果物と野菜

- その他の用途

- 地域

- 北米

- 米国

- カナダ

- メキシコ

- その他北米

- 欧州

- スペイン

- 英国

- フランス

- ドイツ

- ロシア

- イタリア

- その他欧州

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- その他アジア太平洋地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- アフリカ

- 南アフリカ

- その他アフリカ

- 北米

第6章 競合情勢

- 最も採用されている戦略

- 市場シェア分析

- 企業プロファイル

- Valent BioSciences

- Certis USA LLC

- Bio Works Inc.

- Agri Life

- Marrone Bio Innovations

- Novozymes Biologicals

- Bayer CropScience

- Sumitomo Chemical Co. Ltd

- IsAgro Spa

- De Sangosse

- FMC Corporation

第7章 市場機会と将来の動向

The Microbial Pesticides Market size is estimated at USD 1.37 billion in 2024, and is expected to reach USD 1.87 billion by 2029, growing at a CAGR of 6.42% during the forecast period (2024-2029).

Key Highlights

- While the prevalence of chemical or synthetic pesticides in crop protection is continuing, concerns about human and animal health and the environment are playing key roles in driving the growth of microbial pesticides. Several countries are adopting a stringent approach concerning the number of imports, focusing on regulating the number of pesticide residues. Due to the growing demand for food safety and quality, microbial pesticides are gaining popularity over their synthetic counterparts.

- When incorporated into an integrated pest management program (IPM), the use of microbial pesticides will reduce the need for synthetic pesticides to a very large extent without affecting crop yield rates. According to the Food and Agriculture Organization (FAO), the total area harvested in 2021 accounted for 1,465.0 million hectares, higher than the previous year with 1,442.7 million hectares due to increased demand for crop production with little microbiological and insect infestation.

- Technological change is the major driving factor for boosting agricultural productivity as arable land decreases. With higher incomes, greater knowledge, and improved communication channels, consumers in many countries demand low-cost food with high quality produced through organic methods. At the same time, the demand for food to be produced using techniques that conserve natural resources, limit environmental pressures, and pay greater attention to rural viability and animal welfare is also increasing. Therefore, governments insist on adopting new farm technologies for sustainable farming systems.

Microbial Pesticides Market Trends

Increasing Organic Land and Adaptation of New Farming Technologies

- The increasing adaptation of new farm technologies led to safer field applications of products like microbial pesticides. Sustainable farming support and acceptance within mainstream agriculture drive farmers toward minimizing the use of chemical pesticides, thereby saving costs, productivity, and the environment. The use of microbial pesticides in sustainable agriculture addresses several environmental and social concerns and offers innovative and economically viable opportunities for growers, laborers, and consumers. This is one of the major drivers for the market's growth of microbial pesticides.

- According to Organic Trade Association (OTA), in 2020, Organic sale in the United States was USD 61.92 billion, with a growth rate of 12.4% from the previous year. If we compare this growth rate of organic sales from an economic perspective with the total United States market for food and non-food products, which grew at less than half the rate, at 4.9%, the consumer behavior shift towards organic is clear.

- Organic food has gained popularity because it is produced in an agricultural system that provides food free from toxic pesticides, synthetic fertilizers, and genetically modified organisms (GMOs). So organic products are seen as being of high quality and are considered safer for both health and the environment.

North America Dominates the Market

- With increasing awareness of the effects of chemical herbicides and pesticides, bioherbicides can be adopted as an alternative, especially for integrated weed management. Bioherbicides are herbicides consisting of phytotoxins, pathogens, and other microbes. It is used as biological weed control.

- Bioherbicides are obtained as compounds and secondary metabolites from microbes such as fungi, bacteria, and protozoa, or phytotoxic plant residues, extracts, or single compounds derived from other plant species. Demand in the region is driven by a number of factors, including the increased interest in green agricultural practices and the loss of many conventional products to reregistration and/or performance issues.

- Product development has also driven up the demand for microbial pesticides. Better biological active ingredients and products are available in the present market that can compete with and complement conventional chemical pesticides. The microbial biopesticide sector is driven by a growing awareness of sustainable food production, farmers' concerns about excessive chemical use, and the rising expense of chemical crop protection. This increased knowledge is reflected in the booming biological sector in the United States, which provides an excellent opportunity to use microbial pesticides.

- Furthermore, in June 2021, EPA registered five biopesticide products containing Bacillus velezensis strain RTI301 and/or Bacillus subtilis strain RTI477, new microbial active ingredients. These biopesticide products consisted of two manufacturing and three end-use products, utilizing natural bacteria to protect seedlings and/or agricultural crops from fungal growth. EPA also concluded the products with registered uses would not affect any nontarget species. Thus, such active initiatives taken by the EPA to approve new microbial ingredients in the country are a driving factor for the growth of the microbial pesticide market.

Microbial Pesticides Industry Overview

The market for microbial pesticides is extremely fragmented, with a large number of firms controlling the majority of the market share, along with several small companies and private labels. Bayer CropScience AG, FMC Corporation, Koppert Biological Systems, Valent Biosciences Corporation, and Certis USA LLC are some of the prominent companies in the market studied. New product launches, partnerships, and acquisitions are the major strategies adopted by the leading companies in the market in the country. Along with innovations and expansions, investments in R&D and developing novel product portfolios will likely be crucial strategies in the coming years. The major acquisitions between companies to develop microbial pesticides indicate that the focus on bio-based products is increasing rapidly. The players in the market are investing heavily in this market to diversify their biological research divisions in the expanding marketplace.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Ingredient Type

- 5.1.1 Bacteria-based Pesticides

- 5.1.2 Fungi-based Pesticides

- 5.1.3 Virus-based Pesticides

- 5.1.4 Other Ingredient Types

- 5.2 Product Type

- 5.2.1 Microbial Fungicide

- 5.2.2 Microbial Insecticide

- 5.2.3 Other Product Types

- 5.3 Application

- 5.3.1 Grains & Cereals

- 5.3.2 Pulses & Oilseeds

- 5.3.3 Fruits & Vegetables

- 5.3.4 Other Applications

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.1.4 Rest of North America

- 5.4.2 Europe

- 5.4.2.1 Spain

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Germany

- 5.4.2.5 Russia

- 5.4.2.6 Italy

- 5.4.2.7 Rest of Europe

- 5.4.3 Asia Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 Australia

- 5.4.3.5 Rest of Asia Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Africa

- 5.4.5.1 South Africa

- 5.4.5.2 Rest of Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Most Adopted Strategies

- 6.2 Market Share Analysis

- 6.3 Company Profiles

- 6.3.1 Valent BioSciences

- 6.3.2 Certis USA LLC

- 6.3.3 Bio Works Inc.

- 6.3.4 Agri Life

- 6.3.5 Marrone Bio Innovations

- 6.3.6 Novozymes Biologicals

- 6.3.7 Bayer CropScience

- 6.3.8 Sumitomo Chemical Co. Ltd

- 6.3.9 IsAgro Spa

- 6.3.10 De Sangosse

- 6.3.11 FMC Corporation