|

|

市場調査レポート

商品コード

1640491

溶射:市場シェア分析、産業動向・統計、成長予測(2025~2030年)Thermal Spray - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 溶射:市場シェア分析、産業動向・統計、成長予測(2025~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

溶射市場規模は2025年に130億3,000万米ドルと推計され、予測期間中(2025-2030年)のCAGRは4%を超え、2030年には158億5,000万米ドルに達すると予測されます。

溶射市場はCOVID-19の大流行によってマイナスの影響を受けました。当初は、操業停止やサプライチェーンの混乱により製造活動が鈍化し、溶射皮膜の需要が一時的に減少しました。しかし、産業界が新しい規範を採用し、衛生と保護を重視するようになると、ヘルスケア、自動車、航空宇宙などの産業で溶射コーティングの需要が拡大しました。

主なハイライト

- 溶射セラミックコーティングの医療機器への使用による人気の高まり、航空宇宙産業における溶射コーティングの使用の増加、硬質クロムコーティングの代替は、溶射市場の需要を促進する要因の一つです。

- しかし、プロセスの信頼性と一貫性に関する問題や、近年の硬質3価クロムコーティングの出現は、市場の成長を妨げる可能性が高いです。

- 石油・ガス産業からの溶射需要の増加、溶射処理材料のリサイクル、溶射技術(コールドスプレー・プロセス)の進歩は、今後数年間、市場に有利な成長機会をもたらすと予想されます。

- 予測期間中、アジア太平洋が溶射市場を独占すると予想されます。

溶射市場の動向

航空宇宙産業が市場を独占する見込み

- 航空宇宙部品は、高温、腐食性化学物質、極端な気象条件などの過酷な環境にさらされることが多いです。溶射コーティングは腐食に対する効果的なバリアを提供し、タービンブレード、エンジン部品、機体などの重要部品の寿命を延ばします。

- 溶射皮膜は航空宇宙部品に軽量化ソリューションを提供し、燃費効率と航空機全体の性能向上に貢献します。特性を調整したコーティングは、構造的完全性を維持しながら、より重い材料を置き換えることができます。

- 航空宇宙産業は急速な技術の進歩と革新の中にあり、航空機製造の好況を生み出しています。ボーイング・コマーシャル・アウトルック2023-2042によると、国際線の利用が復活し、国内線の利用が大流行前のレベルに戻っていることから、同社は2042年までに48,575機の新たな民間ジェット機の世界需要を予測しています。

- 国際航空旅客協会によると、2023年8月の国内民間航空機旅客輸送量は、パンデミック前の時期より9.2%増加しました。航空輸送量の増加は民間航空機の需要を高め、予測期間中の接着剤需要を促進する可能性があります。

- 世界の主要航空機メーカーであるエアバスは、2023年に735機の民間航空機を納入し、前年比11%増となった。

- 上記の要因は、予測期間中に航空宇宙産業における溶射需要を押し上げると予想されます。

アジア太平洋地域が市場を独占する

- アジア太平洋地域は、特に中国、インド、日本、韓国などの国々で急速な工業化が進んでいます。自動車、航空宇宙、エレクトロニクス、エネルギー産業など、この地域の製造業は活況を呈しており、部品の性能と耐久性を向上させる溶射コーティングの需要が大きく伸びています。

- アジア太平洋地域の政府は、輸送、エネルギー、建設などのインフラプロジェクトに多額の投資を行っています。溶射コーティングは、重要なインフラ部品を腐食、摩耗、侵食から保護することで、寿命を延ばし、メンテナンスコストを削減します。

- 中国は世界最大の航空機メーカーのひとつであり、中国民用航空局の発表によれば、国内航空旅客市場でもあります。また、小型航空機部品メーカーが200社以上あり、部品・組立産業が急成長しています。

- 中国は世界最大の電子機器製造基地です。スマートフォン、テレビ、ケーブル、モバイル・コンピューター、ゲーム機、その他の家電製品などの電子製品は、中国で活発に生産されています。CEICによると、2023年12月の中国電子製品の輸出額は216億3,000万米ドルでした。

- 2023年、韓国は海外から総額188億米ドルの投資を受け、前年比3.4%増を記録しました。特に、電子産業はこの投資の中で最大のシェアを占め、30億米ドルが割り当てられ、小産業のトップとして際立っています。

- 中国は世界最大の鉄鋼生産国のひとつです。公式発表によると、2023年の年初11ヵ月間の一次鉄鋼生産量は9億5,214万トンに達し、前年同期比1.5%増となった。

- インドの自動車産業は、技術の進歩やマクロ経済の拡大において重要な役割を果たしています。インド自動車工業会(SIAM)によると、2023年4月から2024年3月までの自動車販売台数は2,385万3,463台に達し、2023年度の同時期の2,120万4,846台から12.5%増加しました。

- 上記の要因から、予測期間中、この地域が市場を独占すると予測されます。

溶射産業の概要

溶射市場は細分化されています。主要企業(順不同)には、OC Oerlikon Management AG、Linde PLC(Praxair ST Technologies Inc.)、Chromalloy Gas Turbine LLC、Bodycote、Kennametal Inc.などがあります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 医療機器における溶射コーティングの用途拡大

- 溶射セラミックコーティングの人気上昇

- 硬質クロム皮膜の代替

- 航空宇宙産業における溶射皮膜の使用増加

- 抑制要因

- 硬質3価クロムコーティングの出現

- プロセスの信頼性と一貫性に関する問題

- 業界バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の度合い

第5章 市場セグメンテーション(金額ベース市場規模)

- 製品タイプ別

- コーティング材料

- 粉体

- セラミックス

- 金属

- ポリマーとその他のパウダー

- ワイヤー/ロッド

- その他コーティング材料(補助材料)

- 溶射装置

- 溶射システム

- 集塵装置

- スプレーガンとノズル

- 供給装置

- スペアパーツ

- 防音カバー

- その他の溶射装置

- 溶射コーティングと仕上げ

- 燃焼

- 電気エネルギー

- コーティング材料

- エンドユーザー産業別

- 航空宇宙

- 産業用ガスタービン

- 自動車

- エレクトロニクス

- 石油・ガス

- 医療機器

- エネルギー・電力

- 製鉄

- 繊維

- 印刷・製紙

- 地域別

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- マレーシア

- タイ

- インドネシア

- ベトナム

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- トルコ

- ロシア

- ノルディック

- その他欧州

- 南米

- ブラジル

- アルゼンチン

- コロンビア

- その他南米

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- ナイジェリア

- エジプト

- カタール

- アラブ首長国連邦

- その他中東とアフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア(%)**/ランキング分析

- 主要企業の戦略

- 企業プロファイル

- Thermal Spray Material Companies

- Aimtek Inc.

- AISher APM LLC

- AMETEK Inc.

- C&M Technologies GmbH

- CASTOLIN EUTECTIC

- CenterLine(Windsor)Limited(Supersonic Spray Technologies Division)

- CRS Holdings LLC

- Fisher Barton

- Global Tungsten & Powders

- H.C. Starck Inc.

- HAI Inc

- Hoganas AB

- Hunter Chemical LLC

- Kennametal Inc.

- Linde PLC(Praxair ST Technologies Inc.)

- LSN Diffusion Limited

- Metallisation Limited

- Metallizing Equipment Co. Pvt. Ltd

- OC Oerlikon Management AG

- Polymet

- Powder Alloy Corporation

- Saint-Gobain

- Sandvik AB

- Thermion

- Thermal Spray Coatings Companies

- APS Materials Inc.

- Bodycote

- Chromalloy Gas Turbine LLC

- Curtiss-Wright Corporation(FW Gartner)

- Fisher Barton

- FM Industries

- Hannecard Roller Coatings, Inc(ASB Industries Inc.)

- Lincotek Trento SpA

- Linde PLC(Praxair ST Technologies Inc.)

- OC Oerlikon Management AG

- Thermion

- TOCALO Co. Ltd

- Thermal Spray Equipment Companies

- Air Products and Chemicals Inc.

- Arzell Inc.

- ASB Industries Inc.(Hannecard Roller Coatings Inc.)

- Bay State Surface Technologies Inc.(Aimtek Inc.)

- Camfil Air Pollution Control(APC)

- CASTOLIN EUTECTIC

- Centerline(Windsor)Ltd(SUPERSONIC SPRAY TECHNOLOGIES)

- Donaldson Company Inc.

- Flame Spray Technologies BV

- GTV Verschleibschutz GmbH

- HAI Inc.

- Imperial Systems Inc.

- Kennametal Inc.

- Lincotek Equipment SpA

- Linde PLC(Praxair ST Technologies Inc.)

- Metallisation Limited

- Metallizing Equipment Co. Pvt. Ltd

- OC Oerlikon Management AG

- Plasma Powders

- Powder Feed Dynamics Inc.

- Progressive Surface

- Saint-Gobain

- Thermion

- Thermal Spray Material Companies

第7章 市場機会と今後の動向

- 溶射技術の進歩(コールドスプレープロセス)

- 溶射材料のリサイクル

- 石油・ガス産業からの需要増加

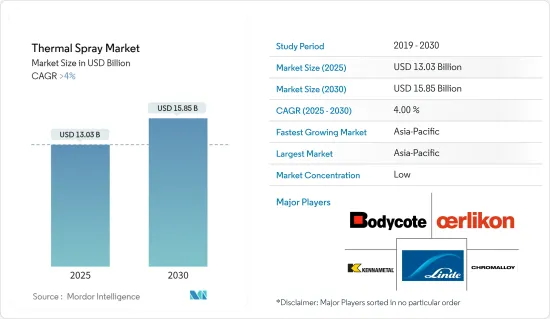

The Thermal Spray Market size is estimated at USD 13.03 billion in 2025, and is expected to reach USD 15.85 billion by 2030, at a CAGR of greater than 4% during the forecast period (2025-2030).

The thermal spray market was negatively affected by the COVID-19 pandemic. Initially, there was a slowdown in manufacturing activities due to lockdowns and supply chain disruptions, leading to a temporary decrease in demand for thermal spray coatings. However, as industries adopted new norms and increased their emphasis on hygiene and protection, there was a growing demand for thermal spray coatings in industries such as healthcare, automotive, and aerospace.

Key Highlights

- The increasing popularity of thermal spray ceramic coatings due to their usage in medical devices, the rising use of thermal spray coatings in the aerospace industry, and the replacement of hard chrome coatings are some factors driving the demand for the thermal spray market.

- However, issues regarding process reliability and consistency and the emergence of hard trivalent chrome coatings in recent years are likely to hinder the market's growth.

- The increasing demand for thermal spray from the oil and gas industry, recycling of thermal spray processing materials, and advancements in spraying technology (cold spray process) are expected to provide lucrative growth opportunities for the market in the coming years.

- Asia-Pacific is expected to dominate the thermal spray market over the forecast period.

Thermal Spray Market Trends

The Aerospace Industry is Expected to Dominate the Market

- Aerospace components are often exposed to harsh environments, including high temperatures, corrosive chemicals, and extreme weather conditions. Thermal spray coatings provide an effective barrier against corrosion, extending the lifespan of critical components such as turbine blades, engine parts, and airframes.

- Thermal spray coatings offer lightweight solutions for aerospace components, contributing to fuel efficiency and overall aircraft performance. Coatings with tailored properties can replace heavier materials while maintaining structural integrity.

- The aerospace industry is undergoing rapid technological advancements and innovation, creating upswings for aircraft manufacturing. According to the Boeing Commercial Outlook 2023-2042, with a resurgence in international traffic and domestic air travel back to pre-pandemic levels, the company has projected global demand for 48,575 new commercial jets by 2042.

- According to the International Air Travel Association, domestic commercial aircraft passenger traffic increased by 9.2% over the pre-pandemic timeline in August 2023. Increased air traffic may raise the demand for commercial aircraft and propel the demand for adhesives during the forecast period.

- Airbus, a major aircraft manufacturer worldwide, delivered 735 commercial aircraft in 2023, an increase of 11% compared to the previous year.

- The factors mentioned above are expected to boost the demand for thermal spray in the aerospace industry during the forecast period.

Asia-Pacific to Dominate the Market

- Asia-Pacific is experiencing rapid industrialization, particularly in countries like China, India, Japan, and South Korea. The region's booming manufacturing sector, including the automotive, aerospace, electronics, and energy industries, is driving significant demand for thermal spray coatings to enhance component performance and durability.

- Governments in Asia-Pacific are investing heavily in infrastructure projects, including transportation, energy, and construction. Thermal spray coatings protect critical infrastructure components from corrosion, wear, and erosion, thereby extending their lifespan and reducing maintenance costs.

- China is one of the world's biggest aircraft manufacturers and a market for domestic air passengers, as stated by the Chinese Civil Aviation Administration. In addition, with more than 200 small aircraft component manufacturers, there has been rapid growth in the parts and assembly industry.

- China is the largest electronics manufacturing base in the world. Electronic products such as smartphones, televisions, cables, mobile computers, gaming systems, and other consumer electronic equipment are being produced in China on an active basis. According to the CEIC, in December 2023, the export value of Chinese electronics products was USD 21.63 billion.

- In 2023, South Korea received a total of USD 18.8 billion in investments from abroad, marking a 3.4% increase from the previous year. Specifically, the electronics industry saw the largest share of this investment, with USD 3 billion allocated, standing out as the top sub-industry.

- China is one of the largest producers of steel globally. According to official figures, the nation's primary steel production reached 952.14 million tons during the initial 11 months of 2023, marking a 1.5% increase compared to the same period in the previous year.

- The automotive industry in India plays a crucial role in technological advancements and macroeconomic expansion. According to the Society of Indian Automobile Manufacturers (SIAM), the number of vehicles sold from April 2023 to March 2024 reached 23,853,463, marking an increase of 12.5% from the 21,204,846 units sold in the same timeframe during FY 2023.

- Due to the above-mentioned factors, the region is projected to dominate the market during the forecast period.

Thermal Spray Industry Overview

The thermal spray market is fragmented in nature. The major players (not in any particular order) include OC Oerlikon Management AG, Linde PLC (Praxair ST Technologies Inc.), Chromalloy Gas Turbine LLC, Bodycote, and Kennametal Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Usage of Thermal Spray Coatings in Medical Devices

- 4.1.2 Rising Popularity of Thermal Spray Ceramic Coatings

- 4.1.3 Replacement of Hard Chrome Coating

- 4.1.4 Rising Use of Thermal Spray Coatings in the Aerospace Industry

- 4.2 Restraints

- 4.2.1 Emergence of Hard Trivalent Chrome Coatings

- 4.2.2 Issues Regarding Process Reliability and Consistency

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Product Type

- 5.1.1 Coatings Materials

- 5.1.1.1 Powders

- 5.1.1.1.1 Ceramics

- 5.1.1.1.2 Metal

- 5.1.1.1.3 Polymers and Other Powders

- 5.1.1.2 Wires/Rods

- 5.1.1.3 Other Coating Materials (Auxiliary Material)

- 5.1.2 Thermal Spray Equipment

- 5.1.2.1 Thermal Spray Coating System

- 5.1.2.2 Dust Collection Equipment

- 5.1.2.3 Spray Gun and Nozzle

- 5.1.2.4 Feeder Equipment

- 5.1.2.5 Spare Parts

- 5.1.2.6 Noise-reducing Enclosures

- 5.1.2.7 Other Thermal Spray Equipment

- 5.1.1 Coatings Materials

- 5.2 Thermal Spray Coatings and Finishes

- 5.2.1 Combustion

- 5.2.2 Electric Energy

- 5.3 End-user Industry

- 5.3.1 Aerospace

- 5.3.2 Industrial Gas Turbines

- 5.3.3 Automotive

- 5.3.4 Electronics

- 5.3.5 Oil and Gas

- 5.3.6 Medical Devices

- 5.3.7 Energy and Power

- 5.3.8 Steel Making

- 5.3.9 Textile

- 5.3.10 Printing and Paper

- 5.4 Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Malaysia

- 5.4.1.6 Thailand

- 5.4.1.7 Indonesia

- 5.4.1.8 Vietnam

- 5.4.1.9 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Turkey

- 5.4.3.7 Russia

- 5.4.3.8 NORDIC

- 5.4.3.9 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Colombia

- 5.4.4.4 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 South Africa

- 5.4.5.2 Saudi Arabia

- 5.4.5.3 Nigeria

- 5.4.5.4 Egypt

- 5.4.5.5 Qatar

- 5.4.5.6 United Arab Emirates

- 5.4.5.7 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Thermal Spray Material Companies

- 6.4.1.1 Aimtek Inc.

- 6.4.1.2 AISher APM LLC

- 6.4.1.3 AMETEK Inc.

- 6.4.1.4 C&M Technologies GmbH

- 6.4.1.5 CASTOLIN EUTECTIC

- 6.4.1.6 CenterLine (Windsor) Limited (Supersonic Spray Technologies Division)

- 6.4.1.7 CRS Holdings LLC

- 6.4.1.8 Fisher Barton

- 6.4.1.9 Global Tungsten & Powders

- 6.4.1.10 H.C. Starck Inc.

- 6.4.1.11 HAI Inc

- 6.4.1.12 Hoganas AB

- 6.4.1.13 Hunter Chemical LLC

- 6.4.1.14 Kennametal Inc.

- 6.4.1.15 Linde PLC (Praxair ST Technologies Inc.)

- 6.4.1.16 LSN Diffusion Limited

- 6.4.1.17 Metallisation Limited

- 6.4.1.18 Metallizing Equipment Co. Pvt. Ltd

- 6.4.1.19 OC Oerlikon Management AG

- 6.4.1.20 Polymet

- 6.4.1.21 Powder Alloy Corporation

- 6.4.1.22 Saint-Gobain

- 6.4.1.23 Sandvik AB

- 6.4.1.24 Thermion

- 6.4.2 Thermal Spray Coatings Companies

- 6.4.2.1 APS Materials Inc.

- 6.4.2.2 Bodycote

- 6.4.2.3 Chromalloy Gas Turbine LLC

- 6.4.2.4 Curtiss-Wright Corporation (FW Gartner)

- 6.4.2.5 Fisher Barton

- 6.4.2.6 FM Industries

- 6.4.2.7 Hannecard Roller Coatings, Inc (ASB Industries Inc.)

- 6.4.2.8 Lincotek Trento SpA

- 6.4.2.9 Linde PLC (Praxair ST Technologies Inc.)

- 6.4.2.10 OC Oerlikon Management AG

- 6.4.2.11 Thermion

- 6.4.2.12 TOCALO Co. Ltd

- 6.4.3 Thermal Spray Equipment Companies

- 6.4.3.1 Air Products and Chemicals Inc.

- 6.4.3.2 Arzell Inc.

- 6.4.3.3 ASB Industries Inc. (Hannecard Roller Coatings Inc.)

- 6.4.3.4 Bay State Surface Technologies Inc. (Aimtek Inc.)

- 6.4.3.5 Camfil Air Pollution Control (APC)

- 6.4.3.6 CASTOLIN EUTECTIC

- 6.4.3.7 Centerline (Windsor) Ltd (SUPERSONIC SPRAY TECHNOLOGIES)

- 6.4.3.8 Donaldson Company Inc.

- 6.4.3.9 Flame Spray Technologies BV

- 6.4.3.10 GTV Verschleibschutz GmbH

- 6.4.3.11 HAI Inc.

- 6.4.3.12 Imperial Systems Inc.

- 6.4.3.13 Kennametal Inc.

- 6.4.3.14 Lincotek Equipment SpA

- 6.4.3.15 Linde PLC (Praxair ST Technologies Inc.)

- 6.4.3.16 Metallisation Limited

- 6.4.3.17 Metallizing Equipment Co. Pvt. Ltd

- 6.4.3.18 OC Oerlikon Management AG

- 6.4.3.19 Plasma Powders

- 6.4.3.20 Powder Feed Dynamics Inc.

- 6.4.3.21 Progressive Surface

- 6.4.3.22 Saint-Gobain

- 6.4.3.23 Thermion

- 6.4.1 Thermal Spray Material Companies

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Advancements in Spraying Technology (Cold Spray Process)

- 7.2 Recycling of Thermal Spray Processing Materials

- 7.3 Increasing Demand From The Oil and Gas Industry