|

市場調査レポート

商品コード

1444649

低侵襲手術装置:市場シェア分析、業界動向と統計、成長予測(2024~2029年)Minimally Invasive Surgery Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 低侵襲手術装置:市場シェア分析、業界動向と統計、成長予測(2024~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 164 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

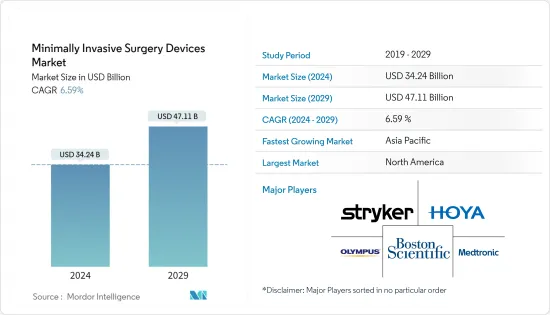

低侵襲手術(MIS)装置の市場規模は、2024年に342億4,000万米ドルと推定され、2029年までに471億1,000万米ドルに達すると予測されており、予測期間(2024年から2029年)中に6.59%のCAGRで成長します。

COVID-19のパンデミックは市場に大きな影響を与えました。入院の制限と手術の遅れにより、パンデミックの初期段階ではMISデバイスの需要が減少し、市場の成長が妨げられました。しかし、ロックダウンと制限は解除され、2021年の初めから専門的な規制に従って外科手術が実施され始めました。たとえば、2022年 7月にGlobal Journal of Medical Pharmaceutical and Biomedical Updateに掲載された記事によると、最小限のアクセスアプローチは、適切な患者の選択と追加の予防措置があれば、COVID-19症のパンデミック中でも安全であることがわかりました。 MISは入院期間を短縮するため、病気の伝播を減らす手段として考慮する必要があります。したがって、適切なガイドラインを開発して実施することで、後期段階でのCOVID-19感染症の発生率が最小限に抑えられたことは間違いありません。その結果、パンデミックはMISの需要創出に大きな影響を及ぼし、今後もその影響が続く可能性があります。したがって、分析によると、市場の成長は予測期間中に増加し、パンデミック前のレベルに達すると予想されます。

生活習慣関連疾患や慢性疾患の有病率の増加や、低侵襲手術に対する嗜好の高まりなどが、市場の成長に大きく貢献しています。

MISには、切開が少なく、感染の可能性が低く、回復時間が早いなど、いくつかの利点があります。したがって、医師は、このような利点を理由に、婦人科、泌尿器科、胃腸疾患などの慢性疾患を治療するための処置を推奨しています。したがって、これらの手術の採用は増加しています。たとえば、2021年10月に『Annals of Medicine and Surgery Journal』に掲載された論文によると、近年、生存率の向上、合併症の減少、急速な回復により関心が高まっている一方で、従来の手術法のさまざまな側面がMISに取って代わられています。したがって、MISの数の増加は、将来の市場の成長を促進すると予想されます。

世界および地域の市場プレーヤーは、国内で先進的な製品を開発および革新しています。たとえば、2021年 4月に、Ambu Inc.は泌尿器科用の使い捨て内視鏡プラットフォームであるaScope 4 Cystoについてカナダ保健省から承認を取得しました。さらに、2021年4月、オリンパス株式会社は、Veran Medical Technologies Inc.と協力して、510(k)クリアのH-SteriScope単回使用気管支鏡の米国気管支鏡ポートフォリオを発売しました。診断および治療手順。したがって、このような活動は、MISデバイスの革新と開発の機会を生み出し、予測期間中の市場の成長を促進すると予想されます。

ただし、熟練した専門家の不足と低侵襲手術や機器の高コストにより、予測期間中の市場の成長が妨げられると予想されます。

低侵襲手術装置の市場動向

内視鏡装置は、予測期間中に最も急速に成長するセグメントになると予想される

内視鏡装置は低侵襲で、人体の自然な開口部に挿入して内臓や組織を詳細に観察できます。内視鏡装置を使用して行われる手術は、一般に画像診断や小規模な手術です。内視鏡検査は、消化器疾患、膵炎、胃がん、胃がん、呼吸器疾患、尿路疾患など、さまざまな疾患に適応します。内視鏡装置の臨床的意義により、これらの装置は市場の需要が高まっており、今後の期待が高まっています。今後数年間、より速いペースで成長を続けるためです。

内視鏡装置は、さまざまな病気の検出にさまざまな利点をもたらします。たとえば、Cancers Journalに2021年 12月に掲載された記事によると、時間の経過とともに続く内視鏡技術の進歩により、胃病変の検出と診断が向上しました。内視鏡技術は、胃病変の検出と診断の向上を促進するために継続的に進歩しています。したがって、世界のがんの負担により、内視鏡装置の需要は増加する可能性があります。これにより、予測期間中に内視鏡装置セグメントが推進されることが期待されます。

内視鏡市場は、有利な償還政策、技術の進歩、内視鏡装置市場における新規参入企業の増加によって牽引されると予想されます。カールストルツによる2022年 9月の更新によると、同社はオーストラリアのシドニーでクラス最高の内視鏡を製造しています。同社はシドニーの拠点に加え、世界 40か国以上で事業を展開しています。したがって、革新的な内視鏡の開発に注力するこのような世界的および地域的なメーカーの存在は、予測期間中にこのセグメントの成長を獲得すると予想されます。

北米は予測期間中に市場のかなりのシェアを保持すると予想される

北米は過去数年間、低侵襲手術装置市場で大きなシェアを占めており、主に低侵襲手術を必要とする疾患の負荷が高く、MISに対する意識が高まっているため、予測期間にわたって同様の傾向を示すと予想されています。

北米では、心血管疾患、がん、神経疾患などの慢性疾患の有病率が高いため、米国が予測期間中に主要な市場シェアを保持すると予想されます。たとえば、2022年 10月にCDCが更新したデータによると、米国では34秒ごとに1人が心血管疾患に苦しんでおり、この国におけるこの病気の負担が高く、手術の必要性を生み出していることが示されています。これにより、国内で低侵襲外科手術の機会が生まれ、予測期間中の市場の成長を促進すると予想されます。

主要な市場プレーヤーが開発したMISに使用されるさまざまな手術装置の技術進歩と新しい装置の発売により、この地域の市場の成長がさらに補完されることが期待されています。たとえば、2021年 5月に食品医薬品局は、NaviCamTM磁気制御カプセル内視鏡(MCCE)システムの市販前販売を承認しました。さらに、2021年 3月には、低侵襲治療用超音波医療機器および再生製品のプロバイダーであるMisonix Inc.が、neXus超音波手術システムのカナダ保健省ライセンスを取得しました。 neXusは、腹腔鏡手術を含むさまざまな手術の治療効率と有効性を向上させるための超音波技術の最新の進歩を組み込んだ、強力で高度に統合された使いやすいシステムです。したがって、このような製品の発売は、予測期間中にこの地域の市場の成長を促進すると予想されます。

低侵襲手術装置業界の概要

低侵襲手術装置市場は、市場にさまざまな主要企業が存在するため、競争が激しく細分化されています。多くの市場関係者は、新製品のイノベーションに多大なリソースを投資し、患者を治療するための新しいデバイスを提供し、高品質で延命治療を提供しています。市場参加者には、Abbott Laboratories、HOYA Corporation、Intuitive Surgical Inc.、Koninklijke Philips NV、Medtronic PLC、Olympus Corporation、Boston Scientific、Strykerなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 従来の手術よりも低侵襲手術の高い受け入れ率

- 生活習慣病や慢性疾患の罹患率の増加

- ますます進む技術の進歩

- 市場抑制要因

- 経験豊富な専門家の不足

- 不確実な規制枠組み

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替製品の脅威

- 競争企業間の敵対関係の激しさ

- アナリストの視点-COVID-19の市場への影響

第5章 市場セグメンテーション

- 製品

- ハンドヘルド機器

- 誘導装置

- ガイディングカテーテル

- ガイドワイヤー

- 電気手術装置

- 内視鏡装置

- 腹腔鏡装置

- 監視および可視化デバイス

- アブレーション装置

- レーザーベースのデバイス

- ロボット支援手術システム

- その他のMISデバイス

- 用途

- 美的

- 心臓血管

- 胃腸

- 婦人科

- 整形外科

- 泌尿器科

- その他の用途

- 地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他アジア太平洋地域

- 中東とアフリカ

- GCC

- 南アフリカ

- その他中東およびアフリカ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 企業プロファイル

- Abbott Laboratories

- Boston Scientific

- Intuitive Surgical Inc.

- Koninklijke Philips NV

- Medtronic PLC

- Olympus Corporation

- HOYA Corporation(Microline Surgical)

- Steris

- Stryker Corporation

- Zimmer Biomet Holdings Inc.

- Johnson &Johnson Inc.

- Renishaw PLC

- CONMED Corporation

第7章 市場機会と将来の動向

The Minimally Invasive Surgery Devices Market size is estimated at USD 34.24 billion in 2024, and is expected to reach USD 47.11 billion by 2029, growing at a CAGR of 6.59% during the forecast period (2024-2029).

The COVID-19 pandemic impacted the market significantly. Due to restricted hospital visits and delayed surgeries, the demand for MIS devices declined and hampered the market's growth during the initial phase of the pandemic. However, the lockdowns and restrictions were lifted, and the surgical procedures started operating following specialized regulations from the beginning of 2021. For instance, according to an article published in July 2022 in the Global Journal of Medical Pharmaceutical and Biomedical Update, minimal access approaches were found safe during the COVID-19 pandemic with proper patient selection and additional precautions. As MIS reduces the hospital stay, it needs to be considered as a means of decreasing disease transmission. Hence, developing and implementing proper guidelines has undeniably minimized the incidence of COVID-19 infection during the later phases. Consequently, the pandemic considerably affected the demand generation of MIS, which may continue in the future. Thus, as per the analysis, the market's growth is expected to increase and reach pre-pandemic levels during the forecast period.

Factors such as an increasing prevalence of lifestyle-related and chronic disorders and a rising preference for minimally invasive procedures are the major contributors to the market's growth.

MIS has several advantages, such as fewer incisions, less chance of infection, and rapid recovery time. Therefore, physicians recommend procedures to treat chronic disorders such as gynecological, urological, gastrointestinal, and others due to such advantages. Thus, the adoption of these surgeries is increasing. For instance, according to the article published in the Annals of Medicine and Surgery Journal in October 2021, multiple facets of the conventional surgical method have been replaced by MIS while gaining interest due to improved survival, fewer complications, and rapid recoveries in recent years. Therefore, an increasing number of MIS is anticipated to propel the market's growth in the future.

Global and regional market players are developing and innovating advanced products in the country. For instance, in April 2021, Ambu Inc. received approval from Health Canada for aScope 4 Cysto, a single-use endoscopes platform for urology. In addition, in April 2021, Olympus Corporation, in collaboration with Veran Medical Technologies Inc., launched the US bronchoscopy portfolio of the 510(k)-cleared H-SteriScope Single-Use Bronchoscopes, a line of five premium endoscopes for use in advanced diagnostic and therapeutic procedures. Thus, such activities are anticipated to create opportunities for MIS device innovation and development and fuel the market's growth over the forecast period.

However, the lack of skilled professionals and the high cost of minimally invasive surgeries and devices are expected to hinder the market's growth over the forecast period.

Minimally Invasive Surgery Devices Market Trends

Endoscopic Devices is Expected to be the Fastest-growing Segment During the Forecast Period

Endoscopic devices are minimally invasive and can be inserted into natural openings of the human body to observe an internal organ or a tissue in detail. The surgeries performed using endoscopic devices are generally imaging procedures and minor surgeries. Endoscopy can be indicated for various types of conditions, such as gastrointestinal disorders, pancreatitis, gastric/stomach cancer, respiratory tract disorders, urinary tract disorders, etc. Due to the clinical significance of endoscopic devices, these devices are gaining market demand and are expected to continue their growth at a faster rate over the next few years.

Endoscopic devices pose various advantages for the detection of various diseases. For instance, as per an article published in December 2021 in Cancers Journal, the detection and diagnosis of stomach lesions have improved due to the ongoing advancements in endoscopic technologies over time. Endoscopic technologies have been continuously advancing to facilitate improvement in the detection and diagnosis of gastric lesions. Thus, owing to the burden of cancer globally, the demand for endoscopic devices is likely to rise. This is expected to propel the endoscopic devices segment during the forecast period.

The market for an endoscope is expected to be driven by favorable reimbursement policies, technological advancements, and an increasing number of new players in the endoscopy devices market. As per the September 2022 update by KARL STORZ, the company manufactures best-in-class endoscopes in Sydney, Australia. In addition to the Sydney location, the company operates in more than 40 countries worldwide. Thus, the presence of such global and regional manufacturers focused on developing innovative endoscopes is anticipated to garner the segment's growth during the forecast period.

North America is Expected to Hold a Significant Share of the Market Over the Forecast Period

North America held a major share of the minimally invasive surgery devices market in the past few years, and it is expected to show a similar trend over the forecast period, primarily due to the high burden of diseases requiring minimally invasive procedures, increasing awareness about MIS.

In North America, the United States is expected to hold a major market share during the forecast period due to the high prevalence of chronic diseases such as cardiovascular diseases, cancer, and neurological diseases. For instance, according to the data updated by CDC in October 2022, every 34 seconds, a person suffers from cardiovascular disease in the United States, showing a high burden of the disease in the country, creating the need for surgeries. This is expected to create opportunities for minimally invasive surgical procedures in the country and drive the market's growth over the forecast period.

Technological advancements in various surgical devices used for MIS developed by key market players and new device launches are further expected to complement the growth of the market in the region. For instance, in May 2021, the Food and Drug Administration approved the NaviCamTM Magnetically Controlled Capsule Endoscopy (MCCE) system for premarketing. In addition, in March 2021, Misonix Inc., a provider of minimally invasive therapeutic ultrasonic medical devices and regenerative products, received a Health Canada license for the neXus Ultrasonic Surgical System. neXus is a powerful, highly-integrated, and easy-to-use system incorporating the latest advances in ultrasonic technology for increased efficiency and efficacy in treating procedures across various surgeries, including laparoscopic surgery. Thus, such product launches are anticipated to fuel the market's growth in the region over the forecast period.

Minimally Invasive Surgery Devices Industry Overview

The minimally invasive surgery devices market is competitive and fragmented, owing to the presence of various key players in the market. Many market players are investing significant resources in new product innovation, offering novel devices to treat patients, and delivering high-quality and life-sustaining treatment. Some of the market players are Abbott Laboratories, HOYA Corporation, Intuitive Surgical Inc., Koninklijke Philips NV, Medtronic PLC, Olympus Corporation, Boston Scientific, and Stryker.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Defintion

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Higher Acceptance Rate of Minimally Invasive Surgeries Over Traditional Surgeries

- 4.2.2 Increasing Prevalence of Lifestyle-related and Chronic Disorders

- 4.2.3 Growing Technological Advancements

- 4.3 Market Restraints

- 4.3.1 Shortage of Experienced Professionals

- 4.3.2 Uncertain Regulatory Framework

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

- 4.5 Analyst's Perspective - Impact of COVID-19 on the Market

5 MARKET SEGMENTATION (Market Size by Value - USD million)

- 5.1 Product

- 5.1.1 Handheld Instruments

- 5.1.2 Guiding Devices

- 5.1.2.1 Guiding Catheters

- 5.1.2.2 Guidewires

- 5.1.3 Electrosurgical Devices

- 5.1.4 Endoscopic Devices

- 5.1.5 Laproscopic Devices

- 5.1.6 Monitoring and Visualization Devices

- 5.1.7 Ablation Devices

- 5.1.8 Laser-based Devices

- 5.1.9 Robotic-assisted Surgical Systems

- 5.1.10 Other MIS Devices

- 5.2 Application

- 5.2.1 Aesthetic

- 5.2.2 Cardiovascular

- 5.2.3 Gastrointestinal

- 5.2.4 Gynecological

- 5.2.5 Orthopedic

- 5.2.6 Urological

- 5.2.7 Other Applications

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Middle East and Africa

- 5.3.4.1 GCC

- 5.3.4.2 South Africa

- 5.3.4.3 Rest of Middle East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Rest of South America

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Abbott Laboratories

- 6.1.2 Boston Scientific

- 6.1.3 Intuitive Surgical Inc.

- 6.1.4 Koninklijke Philips NV

- 6.1.5 Medtronic PLC

- 6.1.6 Olympus Corporation

- 6.1.7 HOYA Corporation (Microline Surgical)

- 6.1.8 Steris

- 6.1.9 Stryker Corporation

- 6.1.10 Zimmer Biomet Holdings Inc.

- 6.1.11 Johnson & Johnson Inc.

- 6.1.12 Renishaw PLC

- 6.1.13 CONMED Corporation