|

|

市場調査レポート

商品コード

1906992

ポリイミド(PI):市場シェア分析、業界動向と統計、成長予測(2026年~2031年)Polyimides (PI) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ポリイミド(PI):市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

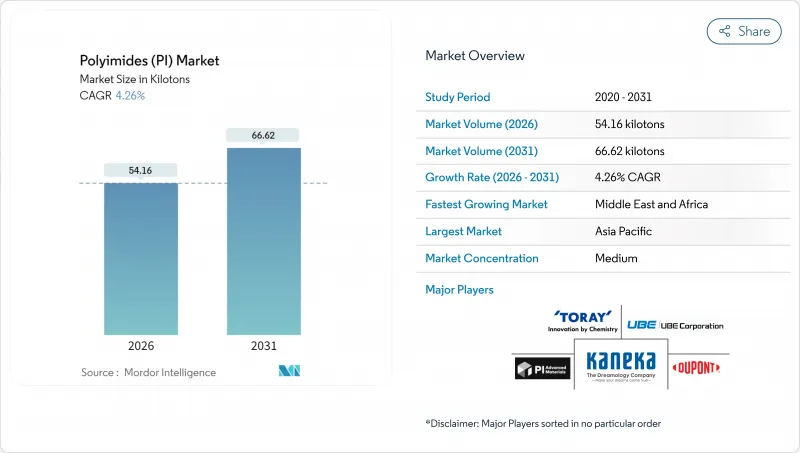

ポリイミド(PI)市場は、2025年の51.95キロトンから2026年には54.16キロトンへ成長し、2026年から2031年にかけてCAGR4.26%で推移し、2031年までに66.62キロトンに達すると予測されています。

高性能用途からの持続的な需要がこの成長軌道を支えています。先進パッケージング、特に高帯域幅メモリストックやヘテロジニアス統合により、ポリイミドフィルムは層間誘電体および応力緩衝材設計の中心的な位置を占め続けています。電気自動車のパワートレイン電動化が進む中、800Vシステムが絶縁安定性のためにポリイミド誘電体を好むことから、顧客基盤が拡大しています。5Gおよび初期6Gインフラへの採用が加速している背景には、低損失正接値がミリ波周波数帯における信号完全性を維持する特性があります。宇宙分野の商業化も新たな成長要因となり、軽量断熱ブランケットでは極限温度下での耐久性を確保するためポリイミドが指定されています。

世界のポリイミド(PI)市場の動向と洞察

電子機器の小型化と折りたたみ式ディスプレイの急成長

より薄く軽量な携帯機器への需要の高まりにより、次世代フレキシブル回路や折りたたみ式ディスプレイにおいて、ポリイミド基板は不可欠な存在となっております。サムスン社の試験では、フィルムが半径1.4mm以下で20万回以上の折り曲げに耐え、光学的な歪みを生じないことが確認されております。自動車のコックピットでは、-40℃から150℃の範囲で安全に動作する曲面OLEDパネルが採用されており、ここでもポリイミドの柔軟性が活用されております。チップレットベースの半導体パッケージも同様に恩恵を受けています。この材料の低い熱膨張係数が、脆い誘電体を割れさせる機械的応力を吸収するためです。フォームファクターの革新が続く中、ポリイミド(PI)市場は、熱的・寸法的安定性を妥協できない設計者からの堅調な需要を獲得しています。

EV高電圧絶縁材の需要急増

電気自動車プラットフォームは現在800V以上で動作するため、従来の絶縁材料は安全限界を超えています。ポリイミドフィルムは250kV/mmを超える絶縁耐力を提供し、-40℃から200℃の間で1,000回の熱サイクル後もその完全性を維持します。テスラ社は、駆動モーターにおける部分放電故障を軽減するため、ポリイミドで被覆した銅巻線を統合しています。シリコンよりも高温で動作する炭化ケイ素インバーターへの移行は、高温ポリマーパッケージングの必要性をさらに強固なものとしています。バッテリー容量の拡大に伴い、熱暴走抑制システムにおいてもポリイミドバリアが指定されており、ポリイミド市場の長期的な成長見通しを高めています。

溶剤鋳造におけるVOC排出規制対応コスト

欧州の産業排出指令基準値およびカリフォルニア州SCAQMD規制では、揮発性有機化合物(VOC)排出量を20mg/m3に制限しています。N-メチル-2-ピロリドンを用いた溶剤鋳造ポリイミドラインでは、ラインあたり数百万米ドル規模の再生式熱酸化装置(RTO)の導入が必須となります。投資回収期間は5年以上となるため、水系イミド化学への移行が進んでいます。しかしながら、生産歩留まりは依然として低く、環境問題の緊急性にもかかわらず、急速な普及は抑制されています。

セグメント分析

電気・電子用途は2025年にポリイミド(PI)市場シェアの36.42%を占め、フレキシブルプリント回路や半導体パッケージングにおける本材料の歴史的役割を裏付けています。この分野の収益は、薄膜に依存する相互接続層を増やすチップレット構造の普及に伴い、今後も拡大を続ける見込みです。自動車分野は、電気自動車用モーター絶縁材やバッテリー用断熱バリアの需要に牽引されています。産業機械分野では高温シール材の耐薬品性が重視され、航空宇宙分野では耐放射線ラミネートが不可欠です。

その他のエンドユーザー産業は規模こそ小さいもの成長が速く、5.18%のCAGRを記録し、2031年までにポリイミド市場規模への貢献度を15.6キロトン以上に押し上げる見込みです。難燃性ファサードシステムを規定する建築基準や、耐滅菌性ポリマーを採用する医療機器メーカーが、顕著な成長分野として挙げられます。これらの用途が成熟するにつれ、民生用電子機器への依存度は薄れ、ポリイミド市場全体の循環リスクは低下する見込みです。

ポリイミド市場レポートは、エンドユーザー産業別(自動車、電気・電子機器、包装、産業・機械、航空宇宙、建築・建設、その他エンドユーザー産業)、形態別(フィルム、樹脂、繊維、その他)、地域別(アジア太平洋、北米、欧州、南米、中東・アフリカ)に分類されています。市場予測は、数量(トン)および金額(米ドル)で提供されます。

地域別分析

アジア太平洋地域は2025年に世界の需要の40.55%を占め、フレキシブルPCB製造および折りたたみ式ディスプレイ組立の中心地であり続けています。中国は規模面で貢献し、日本は半導体バックエンドパッケージング企業に供給する超低欠陥化学技術を完成させています。韓国のディスプレイ大手企業は、大規模な自社消費を維持しています。マレーシアなどの東南アジア諸国は、多国籍電子機器グループからの移転投資を吸収しており、ポリイミド市場を支える地域クラスターを強化しています。

北米地域は着実ながら目立った伸びは見せていません。航空宇宙・防衛プロジェクト分野では優位性を発揮しており、汎用品の3倍の価格帯の飛行認定フィルムが一般的です。高速ネットワーク展開が現地の積層板需要を刺激しています。国内半導体工場への連邦政府の優遇措置は樹脂の追加需要を喚起する見込みですが、特殊ポリマー加工分野の人材不足が急速な拡大を抑制しています。

欧州の見通しは北米と類似しております。自動車の電動化や洋上風力タービン用インバーターではポリイミド絶縁材が採用されていますが、エネルギー価格と厳格な揮発性有機化合物(VOC)規制が転換コストを押し上げております。政策立案者は新規生産能力への補助を伴うサプライチェーン自立化策を検討中ですが、当面は輸入依存が続く見込みです。

中東・アフリカ地域は現在、絶対トン数では小規模ながら、湾岸諸国がハイテク製造業へ多角化を進めることでCAGR6.05%で進展しています。大規模データセンターや5G展開では高周波PCBが求められ、ポリイミドコアが有利です。またインフラ近代化により、ケーブルメーカーは高温絶縁材の採用を推進しています。投資枠組みは未成熟なため、材料の大半は輸入に依存していますが、アジアの化学グループとの合弁事業が協議中です。予測期間内には、地域需要を取り込むためのパイロットラインがポリイミド市場に設立される可能性があります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 電子機器の小型化と折りたたみ式ディスプレイのブーム

- 電気自動車向け高電圧絶縁材の需要急増

- 5G/6G高周波プリント基板の採用

- 宇宙分野における軽量熱シールドの拡大

- 中国主導の生産能力増強が価格障壁を低下させている

- 市場抑制要因

- 揮発性ジアンヒドライドおよびジアミン原料価格の変動

- 溶剤鋳造における揮発性有機化合物(VOC)排出規制対応コスト

- 東アジア以外の地域における加工技術のギャップ

- バリューチェーン分析

- ポーターのファイブフォース

- 新規参入業者の脅威

- 供給企業の交渉力

- 買い手の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

- 規制の枠組み

- アルゼンチン

- オーストラリア

- ブラジル

- カナダ

- 中国

- EU

- インド

- 日本

- マレーシア

- メキシコ

- ナイジェリア

- ロシア

- サウジアラビア

- 南アフリカ

- 韓国

- アラブ首長国連邦

- 英国

- 米国

- 最終用途セクター動向

- 航空宇宙(航空宇宙部品生産収益)

- 自動車(自動車生産)

- 建築・建設(新築床エリア)

- 電気・電子機器(電気・電子機器生産収益)

- 包装(プラスチック包装数量)

第5章 市場規模と成長予測(金額および数量)

- エンドユーザー産業別

- 自動車

- 電気・電子機器

- 包装

- 産業・機械

- 航空宇宙

- 建築・建設

- その他のエンドユーザー産業

- 形態別

- フィルム

- 樹脂

- 繊維

- その他

- 地域別

- アジア太平洋地域

- 中国

- 日本

- インド

- 韓国

- オーストラリア

- マレーシア

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- フランス

- イタリア

- 英国

- ロシア

- その他欧州地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- ナイジェリア

- 南アフリカ

- その他の中東・アフリカ

- アジア太平洋地域

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア(%)/順位分析

- 企業プロファイル

- Arakawa Chemical Industries,Ltd.

- Arkema

- China Wanda Group

- DUNMORE

- DuPont

- JIAOZUO TIANYI TECHNOLOGY CO.,LTD

- Kaneka Corporation

- Kolon Industries Inc.

- Mitsui Chemicals Inc.

- PI Advanced Materials Co., Ltd.

- Shenzhen Ruihuatai Film Technology Co., Ltd.

- SKC

- Taimide Tech. Inc.

- Toray Industries Inc

- UBE Corporation