|

市場調査レポート

商品コード

1851234

ポリウレタン:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Polyurethane - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ポリウレタン:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年07月28日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

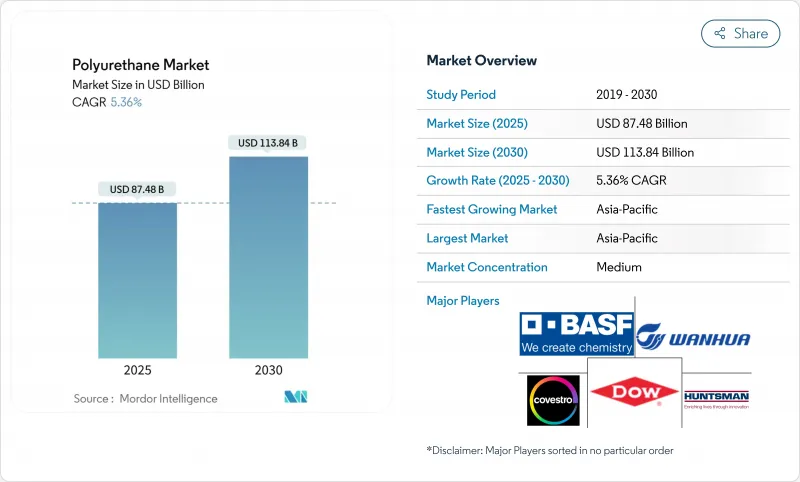

ポリウレタン市場規模は2025年に874億8,000万米ドルと推計され、2030年には1,138億4,000万米ドルに達し、2025-2030年のCAGRは5.36%で拡大すると予測されています。

この堅調な成長は、ポリウレタンの断熱性、軽量化、耐久性などの利点を評価する建設、自動車、家具、電子機器など幅広い分野での採用によるものです。アジア太平洋地域は、中国における大規模な生産能力増強とインドにおける堅調な石油化学投資に支えられ、46%の売上高をリードしており、世界的な供給は引き続きアジア太平洋地域に傾いています。建築セクターはエネルギー基準の厳格化を通じてベースライン量を維持し、自動車メーカーは自動車の軽量化と燃費向上のために先進的なポリウレタン複合材料への需要を加速させています。イノベーションの勢いは、バイオベースのポリオール、クローズド・ループ・リサイクル技術、ライフサイクルの排出量と規制への露出を削減する低VOC塗料への投資によって強化されます。MDI/TDI価格の乱高下や今後の貿易調査においても、ポリウレタン市場は、バリューチェーン統合の定着と持続可能性を重視した用途の拡大というメリットを享受しています。

世界のポリウレタン市場の動向と洞察

自動車用軽量材料

自動車メーカーは、車体重量の軽量化、燃費規制への対応、テールパイプCO2の抑制のために、金属部品を繊維強化ポリウレタンに置き換えています。ダウの成型PUシートは、快適性を保ちながら、シート1枚当たりのフットプリントを50%削減し、サーキュラーグレードのフォームが大量生産に適していることを証明しています。コベストロの音響的に最適化されたヘッドライナーとインテリアトリムは、騒音と揮発性有機化合物(VOC)の放出を削減し、最小限の設計変更でキャビン内の空気の質を向上させます。これらの複合材料を採用するTier-1サプライヤーは、新たな資本支出なしに組立ラインに適合することを報告し、2030年までの採用見通しを強化しています。

建築と建設の成長

世界のエネルギー基準では現在、より高いR値とより厳しい気密性が規定されており、リジッドポリウレタンの熱および蒸気制御の強みが直接的に活かされています。アジア太平洋の建設ブームは、北米の改修奨励策と相まって、建築家を薄いが高性能の吹付け断熱材やボードストック断熱材に依存させています。メーカーは、生産能力を拡大し、化石ポリオールの20%を代替するCO2改質硬質フォームを発売することで、加工パラメータを変更することなく、ゆりかごからゲートまでの排出量を削減することで対応しています。政策主導の機運は、新築および改修市場全体の着実な需要拡大を支えています。

MDI/TDI原料のボラティリティ

MDIの原材料シェアは41.20%であり、ポリウレタンメーカーはベンゼンと原油の変動に左右されます。Wanhuaの寧波の操業停止のような予定されたターンアラウンドや、2025年に米国に入る中国製MDIに対する反ダンピング措置は、価格高騰と割当削減を引き起こします。加工業者は契約期間の延長でヘッジしているが、マージンの圧縮は続いており、供給が安定するまで川下の拡張ラインへの投資は延期されます。

セグメント分析

2024年のポリウレタン市場シェアでは、軟質フォームが32%を占め、寝具、家具、自動車座席の快適性主導の優位性を維持しています。軟質フォームのポリウレタン市場規模は2030年までCAGR 6.07%で成長すると予測され、体圧分散を改善する粘弾性のアップグレードや、圧縮され素早く回復するフォームに依存する「ベッド・イン・ボックス」フルフィルメントモデルがこれを後押しします。生産者は弾力性と通気性を向上させ、人間工学に基づくプレミアムな期待に応える薄型マットレスを可能にします。リサイクル業者は、ポリオールの流れを82%の収率で再生する酸分解プロセスを改良し、この分野を循環型供給ループに近づけています。

硬質フォームは、1インチ当たりのR値が高く、1パスで気密性を確保できることから、建築用断熱材として支持され、第2位に位置します。壁の空洞で厚みが制限される改修プロジェクトでの採用が加速し、温帯だけでなく極端な気候の市場でも持続的な数量需要が強化されます。CASEサブセグメント(コーティング、接着剤、シーラント、エラストマー)は、振動減衰、工業用床材、耐腐食性ライニングにポリウレタンの有用性を拡大します。熱可塑性ポリウレタン(TPU)は、製造炭素を最大59%削減するルーブリゾールのバイオマスバランスESTANE RNWグレードに後押しされ、フットウェアとエレクトロニクス筐体でシェアを獲得しています。

地域分析

アジア太平洋地域は、2024年のポリウレタン市場売上高の46%を占め、中国が生産の中心であると同時に消費大国でもあります。Wanhuaのような地元のリーダーはMDIとポリオールの生産能力を積極的に拡大し、インドの870億米ドルの石油化学パイプラインは地域の原料確保と派生製品の成長を促進します。公共および民間の建設ブームが急速なモータリゼーションと相まって、この地域が2030年まで最高のCAGR 6.01%を維持することを確実にしています。

北米は、成熟しつつも革新的な市場としてこれに続きます。米国は、住宅改修用の高R値断熱材に注目し、企業の環境目標を達成するためにサーキュラーグレードの自動車用シートフォームを追求しています。中国製MDIに対する2025年のアンチダンピング調査などの政策的動きは、調達戦略を再構築し、国内生産能力への投資を促進します。カナダのネット・ゼロ・ビルディング計画は、この地域の堅調な需要をさらに支えています。

欧州のポリウレタン市場は、厳しい化学物質規制によって形成されています。迫り来るPFAS規制は、広範囲に及ぶ配合の見直しを迫り、先進的な添加物の研究開発と迅速な規制遵守プロセスを持つサプライヤーに有利です。同時に、グリーンな公共調達基準は低VOC・低炭素製品に報いるものであり、メーカーをバイオマスバランスやCO2改良グレードへと誘導しています。

南米、中東・アフリカは、ポリウレタン市場に占める割合は小さいが、インフラ、家具、包装の需要から成長します。ブラジルは輸入依存度を下げるために国内石油化学製品の拡大を推進し、サウジアラビアはポリウレタンの輸出を模索するために原料の優位性を活用しています。大市場からの技術とベストプラクティスの普及は、新興地域が国際的な持続可能性ベンチマークへの準拠を迅速に進めるのに役立っています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 自動車産業における軽量・高性能複合材料の需要増加

- 建築・建設業界からの需要増加

- 寝具、カーペット、クッション産業からの需要増加

- エネルギー効率の高い素材への需要の高まり

- 低VOC(揮発性有機化合物)と水性ポリウレタンへのシフト

- 市場抑制要因

- メタキシレンと原油価格の変動に連動するMDI/TDI原料の変動性

- PFAS系PU添加剤に関するEUのREACH規制と中国のRoHS規制

- 環境問題

- バリューチェーン分析

- ポーターのファイブフォース

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場規模と成長予測

- タイプ別

- 硬質フォーム

- 軟質フォーム

- CASE(コーティング剤、接着剤、シーリング剤、エラストマー)

- 熱可塑性樹脂ポリウレタン(TPU)

- その他のタイプ

- 原材料別

- メチレンジフェニルジイソシアネート(MDI)

- トルエンジイソシアネート(TDI)

- ポリエーテルポリオール

- ポリエステルポリオール

- その他(バイオベースポリオール)

- エンドユーザー業界別

- 家具

- 建築・建設

- エレクトロニクスとアプライアンス

- 自動車

- フットウェア

- パッケージ

- その他のエンドユーザー産業

- 地域別

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- ASEAN

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- 北欧諸国

- ロシア

- その他欧州地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

- ナイジェリア

- その他中東・アフリカ地域

- アジア太平洋地域

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア(%)/ランキング分析

- 企業プロファイル

- BASF SE

- Carpenter Co.

- Covestro AG

- DIC Corporation

- Dow

- Huntsman International LLC

- INOAC Corporation

- LANXESS

- Mitsui Chemicals Inc.

- Momentive

- PPG Industries, Inc.

- Rogers Corporation

- Saint-Gobain

- Sekisui Chemical Co., Ltd.

- Sheela Foam Ltd.

- The Lubrizol Corporation

- Tosoh Corporation

- Wanhua