|

市場調査レポート

商品コード

1640369

中東・アフリカのポリウレタン市場シェア分析、産業動向、成長予測(2025年~2030年)Middle East And Africa Polyurethane - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 中東・アフリカのポリウレタン市場シェア分析、産業動向、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

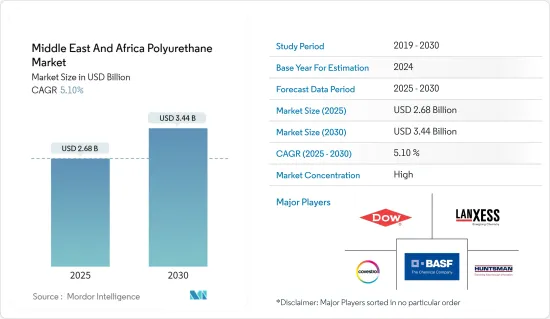

中東・アフリカのポリウレタン市場規模は2025年に26億8,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは5.1%で、2030年には34億4,000万米ドルに達すると予測されます。

主要ハイライト

- COVID-19の発生は市場にマイナスの影響を与えました。COVID-19の発生を食い止めるためのプロジェクトの停止や減速、移動制限、生産停止、労働力不足などがポリウレタン市場の成長低下を招いた。しかし、家具、内装、自動車を含む様々な最終用途からの消費の増加により、2021年からは大幅に回復しました。

- 短期的には、建築・建設産業からの需要の増加や、電子・民生用電子機器産業からの断熱材に対する要求の高まりが、調査した市場の成長を促進する主要要因となっています。

- その反面、原料価格の変動やポリウレタン塗料の有毒性が市場成長の妨げになると予想されます。

- 中東地域における建築物に関するエネルギー効率化施策に対する意識の高まりは、今後の市場成長の機会となりそうです。

- サウジアラビアが市場を独占し、予測期間中に最も高いCAGRで推移すると予想されます。

中東・アフリカのポリウレタン市場動向

建築・建設産業からの需要の増加

- ポリウレタンの最も広範な用途は建築・建設産業です。ポリウレタンは、強度がありながら軽量で、性能が高く、耐久性と汎用性に優れた高性能製品の製造に使用されます。

- 建築・建設産業は硬質ポリウレタン・フォームの最大の消費者です。硬質ポリウレタン・フォーム断熱材を使用することには、エネルギー効率、高性能、多用途性、熱的/機械的性能、環境に優しい性質など、多くの利点があります。

- 「クウェートビジョン2035」の「サステイナブル生活環境」の軸には5つの柱があり、その中で最も重要なのは、2029年までに終了する32億2,000万KWD(105億米ドル)規模の5つのプロジェクトを通じて6万5,500戸の住宅供給を確保する計画で、市民に住宅ケアを提供することです。

- これらのプロジェクトが実施されれば、現在91,000戸ある住宅需要の約72%を満たすことになります。住宅ケア計画の最初のプロジェクトは、ジャベル・アル・アハマド市のクウェート2035(新クウェート)構想を中心としたもので、完成率は95%です。2番目のプロジェクトはアル・ムトラア市で、完成率は64%で、2023年末までに完成する予定です。

- 3つ目のプロジェクトは郊外のサウス・アブドゥラ・アル・ムバラク市で、完成率は72%、2025年末までに完成予定。4つ目のプロジェクトである南サバ・アル・アハマドの完成率は、まだ準備段階であるため約14%で、2029年に完成する予定です。この南サード・アル・アブドゥラは、まだ準備段階で2029年に終了するため、完成率は13%です。このため、クウェートでの住宅建設の増加により硬質フォームが必要となり、クウェートでのポリウレタン市場の需要がさらに高まるとみられます。

- このように、前述の要因は予測期間中にポリウレタン市場を押し上げると予想されます。

サウジアラビアが市場を独占

- 中東・アフリカのポリウレタン市場では、サウジアラビアが最大のシェアを占めています。同国では投資や建設、家具、電子機器の活動が活発化しているため、ポリウレタンの需要は予測期間を通じて増加するとみられます。人口と可処分所得の増加により、より質の高い住宅の開発需要が高まった。

- サウジアラビアの建設市場は、「ビジョン2030」、「NTP2020」、石油からの多角化のためのいくつかの進行中の改革により、大きな成長を示し、有利な可能性を提供すると予想されます。ビジョン2030、NTP2020、民間セクターの投資促進、進行中の改革は、予測期間中、サウジアラビアの建設産業によるポリウレタン市場の成長促進要因になると予想されます。サウジアラビアの「ビジョン2030」は、地方自治体による全国的な住宅インフラ開発への多額の投資とともに、建設産業を活性化させ、増加する国際的な参入企業への関心を生み出しています。

- さらに、「ビジョン2030」の下、2030年までにサウジアラビア全土で11,000室以上の豪華な客室を持つホテルが新たに80軒開業する予定です。そのため、建設やホテル家具への投資が増加し、軟質フォームの需要が見込まれます。

- 現在、サウジアラビア経済はポスト石油の時代を迎えており、建設中のメガシティが将来の成長をもたらすと考えられます。産業筋によると、サウジアラビアでは現在5,200以上の建設プロジェクトが進行中で、その総額は8,190億米ドルに上ります。これらのプロジェクトは、湾岸協力会議(GCC)全体で進行中のプロジェクト総額の約35%を占めています。

- サウジアラビアの主要な都市建設プロジェクトには、マッカの自治体・農村問題省が開発した、それぞれ213億米ドルのアブドラ国王警備施設(フェーズ5)やグランドモスク(聖ハラーム・モスク拡大工事)などがあります。

- サウジアラビアの上位建設プロジェクトには、Neom、紅海プロジェクト、Qiddiyaエンターテインメント・シティ、Amaala、Al-UlaのJean Nouvel's Sharaanリゾート、Makkah Grand Mosque-Third Expansion、Jeddah Tower、住宅省のSakani Homes、Jabal Omar、Al Widyan、Riyadh Metroなどがある、リヤド高速バス輸送システム、キング・ファハド・メディカル・シティ拡大工事、キング・アブドゥラ・ビン・アブドゥルアジーズ・メディカル・コンプレックス、キング・サルマン・エナジー・パーク(スパーク)、Saudi Aramcoのベリとマルジャン、ハナジー・ソーラー・パーク、ドゥマット・アル・ジャンダル風力発電所、Saudi Aramco-TotalのPIB工場、パン・アジアのボトリング施設。

- サウジアラビアの「アミッド・ビジョン2030」は、国のインフラの成長を目的とした巨大プロジェクトに支えられた重要な開発計画です。環境への取り組み、市民の生活の質の向上、強力な経済の創造に重点を置き、ビジョン2030は変革をもたらすことを目指しています。ビジョン2030とそれに対応する国家改造計画(NTP)の導入により、医療、教育、インフラなどいくつかのセグメントへの投資が拡大しています。

- サウジアラビアでは多くの住宅・商業プロジェクトが開始されており、同国の建設活動の活発化が期待されています。例えば、サウジアラビア政府は観光客を誘致するため、国内各地で複数のメガプロジェクトを開始し、順調に進行しています。集合住宅を持つメガプロジェクトの中には、Qiddiyaがあります。2025年までに4,000戸、2030年までに1万1,000戸の住宅が建設され、著名な文化的ランドマークとなります。ディリヤ・ゲートでは、リヤドのプロジェクトで、2027年までに2万戸の住宅が建設されます。ニュー・ムラバでは、リヤドのダウンタウンプロジェクトで、10万4,000戸の住宅が建設される予定です。

- サウジアラビアは開発途上にあり、目覚しい額の投資を受けています。サウジアラビアは2022年3月、8,000キロメートルの新しい軌道を敷設し、鉄道網の規模を3倍以上に拡大すると宣言しました。2021年7月には、1,470億米ドルが輸送・物流部門に割り当てられました。目標が達成される2030年までに、これらの産業は国のGDPの10%を占めることになり、現在より4%増加します。

- Gulf Council Corporationによると、サウジアラビアは医療施設に664億9,000万米ドルの投資を計画しており、民間セクターの協力も得て、その参加率は2030年までに65%上昇する見込みです。

- これらのことから、サウジアラビアのポリウレタン市場は今後数年間、安定した成長が見込まれています。

中東・アフリカのポリウレタン産業概要

中東・アフリカのポリウレタン市場は高度に統合されています。同市場の主要企業には、Covestro AG、BASF SE、Dow、LANXESS、Huntsman International LLCなどがあります(順不同)。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 電子機器産業からの断熱材需要の増大

- 建築・建設産業からの需要増加

- その他の促進要因

- 抑制要因

- 不安定な原料価格

- ポリウレタン・コーティングの毒性

- 産業バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション(金額ベース市場規模)

- 用途

- 発泡体

- 硬質フォーム

- 軟質フォーム

- コーティング剤

- 接着剤とシーラント

- エラストマー

- その他

- 発泡体

- エンドユーザー産業

- 家具・インテリア

- 建築・建設

- 電子機器

- 自動車

- フットウェア

- 包装

- その他

- 地域

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

- エジプト

- クウェート

- カタール

- モロッコ

- その他の中東・アフリカ

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア(%)**/ランキング分析

- 主要企業の戦略

- 企業プロファイル

- BASF SE

- BCI Holding SA

- Covestro AG

- Dow

- Huntsman International LLC

- Kuwait Polyurethane Industries W.L.L

- LANXESS

- Mitsui Chemicals, Inc.

- Perfect Rubber

- Wanhua Chemical Group Co.,Ltd

第7章 市場機会と今後の動向

- 中東地域における建築物に関するエネルギー効率化施策への意識の高まり

- バイオベースポリウレタンへの需要の高まり

目次

Product Code: 52029

The Middle East And Africa Polyurethane Market size is estimated at USD 2.68 billion in 2025, and is expected to reach USD 3.44 billion by 2030, at a CAGR of 5.1% during the forecast period (2025-2030).

Key Highlights

- The COVID-19 outbreak negatively impacted the market. Stoppage or slowdown of projects, movement restrictions, production halts, and labor shortages to contain the COVID-19 outbreak led to a decline in the polyurethane market growth. However, it recovered significantly from 2021, owing to rising consumption from various end-use applications, including furnishing, interiors, and automotive.

- Over the short term, increasing demand from the building and construction industry and growing requirement for thermal insulation from the electronics and appliances industry are some of the major factors driving the growth of the market studied.

- On the flip side, volatile raw material prices and the toxic nature of polyurethane coatings are expected to hinder the growth of the market.

- Growing awareness of the Energy Efficiency Policy related to buildings in the Middle Eastern region is likely to act as an opportunity for market growth in the future.

- Saudi Arabia is expected to dominate the market and will also witness the highest CAGR during the forecast period.

Middle East and Africa Polyurethane Market Trends

Increasing Demand from the Building and Construction Industry

- The most extensive application of polyurethane is in the building and construction industry. Polyurethanes are used to make high-performance products that are strong but lightweight, perform well, and are durable and versatile.

- The building and construction industry is the largest consumer of rigid polyurethane foam. There are many benefits of using rigid polyurethane foam insulation, including its energy efficiency, high performance, versatility, thermal/mechanical performance, and environment-friendly nature.

- The sustainable living environment axis in Kuwait Vision 2035 includes five pillars, the most prominent of which is to provide housing care to citizens through what is planned to ensure the provision of 65.5 thousand housing units through five projects costing about KWD 3.22 billion (USD 10.5 billion), the last of which ends by 2029.

- When these projects are implemented, the state will have met approximately 72% of the current housing requests, which stands at 91,000. The first project of the residential care plan revolves around the vision of Kuwait 2035 (New Kuwait) in the city of Jaber Al-Ahmad, which has a completion rate of 95%. The second project is in the city of Al-Mutla'a, with a completion rate of 64%, to be completed by the end of 2023.

- The third project is in the suburb of South Abdullah Al-Mubarak, which has a completion rate of 72% and will be completed by the end of 2025. The completion rate in the fourth project, which is the South Sabah Al-Ahmad, is about 14%, as it is still in the preparation stage, and it is expected to be completed in 2029. This south of Saad Al-Abdullah has a completion rate of 13% as it is still in its preparatory phase and ends in 2029. Therefore, the growing residential housing construction in Kuwait will demand rigid foams, which will further rise the demand for the polyurethane market in Kuwait.

- Thus, the aforementioned factors are expected to boost the market for polyurethanes during the forecast period.

Saudi Arabia to Dominate the Market

- Saudi Arabia holds the largest share in the Middle East and African polyurethane market. The demand for polyurethane is expected to rise throughout the forecast period due to rising investments and construction, furniture, and electronics activities in the country. The rise in the population and disposable income increased the demand for the development of better-quality residential buildings.

- The Saudi Arabian construction market is expected to witness significant growth and offer lucrative potential due to its Vision 2030, NTP 2020, and several ongoing reforms to diversify away from oil. Vision 2030, NTP 2020, the private sector investment boost, and the ongoing reforms are expected to be the growth drivers for the Saudi polyurethane market from the country's construction industry during the forecasted period. Saudi Arabia's Vision 2030, along with a significant investment in housing and infrastructure development promoted across the country by local authorities, is revitalizing the construction industry and generating interest in a growing number of international players.

- Moreover, under Vision 2030, 80 new hotels with more than 11,000 luxurious rooms will be opened across Saudi Arabia by 2030. Therefore, increasing investments in construction and hotel furniture are expected to create demand for flexible foam.

- Currently, the country's economy is entering a post-oil era in which the kingdom's mega-cities, which are under construction, will provide future growth. According to industry sources, more than 5,200 construction projects are currently ongoing in Saudi Arabia at a value of USD 819 billion. These projects account for approximately 35% of the total value of active projects across the Gulf Cooperation Council (GCC).

- Some of the major urban construction projects in Saudi Arabia include the King Abdullah Security Compounds (Phase 5) and the Grand Mosque (Holy Haram Mosque expansion), each valued at USD 21.3 billion and developed by the Ministry of Municipalities and Rural Affairs in Makkah.

- The top construction projects in Saudi Arabia include Neom, the Red Sea Project, Qiddiya entertainment city, Amaala, Jean Nouvel's Sharaan resort in Al-Ula, Makkah Grand Mosque - Third Expansion, Jeddah Tower, Ministry of Housing's Sakani Homes, Jabal Omar, Al Widyan, Riyadh Metro, Riyadh Rapid Bus Transit System, King Fahd Medical City Expansion, King Abdullah Bin Abdulaziz Medical Complexes, King Salman Energy Park (Spark), Saudi Aramco's Berri and Marjan, Hanergy Solar Park, Dumat Al Jandal Wind Power Plant, Saudi Aramco-Total's PIB factory, and Pan-Asia bottling facility.

- Saudi Arabia's Amid Vision 2030 is a significant development plan supported by megaprojects aimed at the growth of the nation's infrastructure. With an emphasis on environmental commitments, enhancing citizen quality of life, and creating a strong economy, Vision 2030 aspires to bring about change. Investments in several fields, including healthcare, education, and infrastructure, have expanded as a result of the introduction of Vision 2030 and the corresponding National Transformation Plan (NTP).

- Many residential and commercial projects are being launched in Saudi Arabia, which is anticipated to increase the country's construction activity. For instance, the Saudi government has started several mega projects, which are well underway around the country to attract tourists. Some of the mega projects that will have residential complexes are Qiddiya: The project will become a prominent cultural landmark with 4,000 residential units by 2025 and 11,000 units by 2030. Diriyah Gate: The project in Riyadh will include 20,000 residential units by 2027. New Murabba: The Riyadh downtown project is likely to house 104,000 residential units.

- Saudi Arabia is developing, and the nation is receiving impressive amounts of investment. The nation declared in March 2022 that it would more than triple the size of its rail network by installing 8,000 kilometers of new track. In July 2021, USD 147 billion was allocated to the transportation and logistics sectors. By 2030, when the targets have been met, these industries will contribute 10% of the nation's GDP, a 4% increase from today.

- According to the Gulf Council Corporation, Saudi Arabia has planned to invest USD 66.49 billion in healthcare facilities, with help from the private sector, whose participation is expected to rise by 65% by 2030.

- With all of these things, the Saudi Arabian polyurethane market is expected to grow steadily over the next few years.

Middle East and Africa Polyurethane Industry Overview

The Middle East and African polyurethane market is highly consolidated in nature. Some of the major players in the market include Covestro AG, BASF SE, Dow, LANXESS, and Huntsman International LLC, among others (not in any particular order).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Requirement of Thermal Insulation from the Electronics and Appliances Industry

- 4.1.2 Rising Demand from the Building and Construction Industry

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Volatile Raw Material Prices

- 4.2.2 Toxic Nature of Polyurethane Coatings

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Application

- 5.1.1 Foams

- 5.1.1.1 Rigid Foam

- 5.1.1.2 Flexible Foam

- 5.1.2 Coatings

- 5.1.3 Adhesives and Sealants

- 5.1.4 Elastomers

- 5.1.5 Other Applications

- 5.1.1 Foams

- 5.2 End-user Industry

- 5.2.1 Furniture and Interiors

- 5.2.2 Building and Construction

- 5.2.3 Electronics and Appliances

- 5.2.4 Automotive

- 5.2.5 Footwear

- 5.2.6 Packaging

- 5.2.7 Other End-user Industries

- 5.3 Geography

- 5.3.1 Saudi Arabia

- 5.3.2 United Arab Emirates

- 5.3.3 South Africa

- 5.3.4 Egypt

- 5.3.5 Kuwait

- 5.3.6 Qatar

- 5.3.7 Morocco

- 5.3.8 Rest of Middle-East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 BASF SE

- 6.4.2 BCI Holding SA

- 6.4.3 Covestro AG

- 6.4.4 Dow

- 6.4.5 Huntsman International LLC

- 6.4.6 Kuwait Polyurethane Industries W.L.L

- 6.4.7 LANXESS

- 6.4.8 Mitsui Chemicals, Inc.

- 6.4.9 Perfect Rubber

- 6.4.10 Wanhua Chemical Group Co.,Ltd

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Growing Awareness of Energy Efficiency Policy related to Buildings in the Middle Eastern Region

- 7.2 Increasing Demand for Bio-based Polyurethane