|

市場調査レポート

商品コード

1852058

無人海洋機:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Unmanned Marine Vehicles - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 無人海洋機:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年08月04日

発行: Mordor Intelligence

ページ情報: 英文 125 Pages

納期: 2~3営業日

|

概要

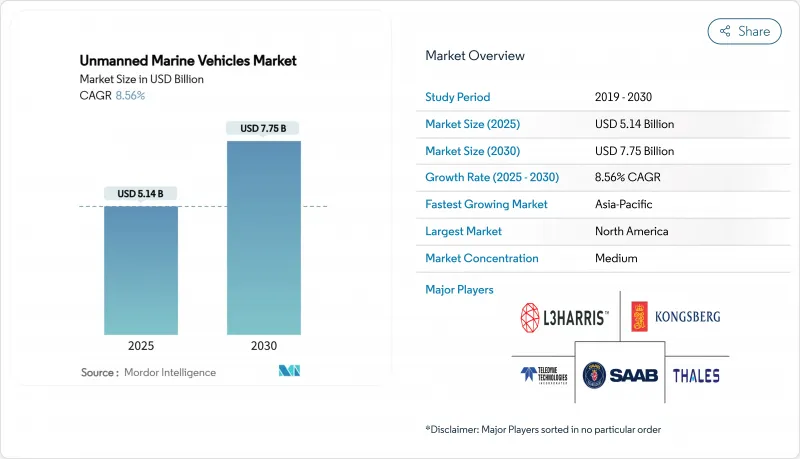

無人海洋機市場規模は2025年に51億4,000万米ドルと推定され、2030年には77億5,000万米ドルに達し、CAGR 8.56%で成長すると予測されています。

この成長軌道を支えているのは、海軍の近代化計画の活発化、オフショアエネルギーの足跡の拡大、持続的な海洋データ収集に対する需要の急増です。非クリュー式プラットフォームは、実験的なツールから、防衛力の範囲を広げ、石油・ガス・風力事業者の検査コストを下げ、長期的な気候変動ミッションの範囲を広げる不可欠な資産へと移行しつつあります。地政学的な対立が激化すれば、ステルス海底システムの調達に拍車がかかり、持続可能性の義務化によって低排出ガスパワートレインへの軸足が加速します。ベンチャーキャピタルの支援を受けた新興企業は、防衛プライムが支配する分野に迅速な反復の文化を注入し、より迅速なプロトタイプ・サイクルを可能にし、より小型のスウォーム・キャパブル・クラフトの二桁のオーダーブックを推進します。エコシステムの参加者は、ソフトウェア・オートノミー・アルゴリズムとデータ・フュージョン・エンジンが、次世代フリートにとって決定的な差別化要因となるとの見方を強めています。

世界の無人海洋機市場の動向と洞察

ISRおよび対潜水艦戦能力への防衛投資の増加

海上の緊張が高まるにつれ、海軍は紛争海域でのカバーギャップを埋める高度な無人艦隊に資金を投入するようになります。米国海軍は、2025会計年度に無人システムに1億7,730万米ドルの予算を計上し、自律型海中艇の大量生産を目標とする「レプリカント」構想を打ち出しています。アンドゥリルのロードアイランド工場は現在、年間200台以上のDive-LDを製造しています。オーストラリアのゴーストシャークやインドのXLUUV入札などの並行プログラムは、複数地域の調達の波を強化しています。フランスの海軍グループによるドローン実証機には、欧州の連携が見て取れます。黒海での戦闘のサクセスストーリーは、運用コンセプトを検証し、取得スケジュールを短縮します。

海洋石油・ガスの点検・保守にUMVの活用が進む

エネルギーメジャーは現在、自律型水中探査機(AUV)を導入しており、検査にかかる経費を、繋留式のROVに比べて最大55%削減しています。TotalEnergies社による遠隔操作ロボットの試験運用は、オフショアの人員を削減する陸上コマンドハブへのシフトを示しています。AUVは異常検知を迅速化し、ドライドック間隔を短縮し、環境フットプリントを半減させるため、湾岸のオペレーターや北海のコントラクターは、予知保全のためにデジタル・ツインを後付けするよう促しています。アラブ首長国連邦(UAE)の再生可能エネルギーで動く非乗組型水上船舶は、脱炭素化の目標と自動化の効率性を融合させています。DNVのSolitudeのような概念研究は、完全無人の浮体式LNGユニットが20%の運用コスト削減を実現することを想定しています。

多額の設備投資と運用コストの負担

大型無人水上車両の価格は船体1隻あたり2億5,000万米ドルに達し、米海軍のXLUUVプログラムだけでも2025年度に2,150万米ドルの予算がりますます。水素燃料電池AUVのコンセプトは排出ガスを排除するが、特注の燃料補給が必要で、初期予算が膨らみます。ノーティカス・ロボティクスは2023年に5,070万米ドルの損失を計上し、画期的な海底モーフィング・プラットフォームの投資回収期間が長期化していることを浮き彫りにしています。Blue Water Autonomyの1,400万米ドルのシード資金などのベンチャーラウンドは、アーリーステージのイノベーターが最初の収益を得るまでに登らなければならない険しい資本のはしごを強調しています。

セグメント分析

無人潜水機(UUV)は、2024年に無人海洋機市場シェアの54.21%を維持し、2030年までのCAGRも11.17%と最も高く、この分野の成長と収益の両輪としての役割を確固たるものにしています。需要は、対潜水艦戦のアップグレードや深海のインフラ点検から湧き上がり、中国の台風に強い「シロナガスクジラ」は30日間の潜水耐久性のベンチマークを示しています。

水上車両は無人海洋機市場のバランスを吸収しているが、沿岸監視、機雷対策、ロジスティクスの牽引役となっています。米国のハイブリッド艦隊モデルは、持続的な水上パトロールを活用し、秘密裏の海中資産を補完します。コンバージェンス動向は、潜水艦発射型UAVと、従来のミッション・ドクトリンを塗り替える水上・水中合同任務を示しています。

中型機は、ペイロードと耐久性のバランスが取れたプロファイルにより、2024年の売上高の31.34%を確保したましが、超小型機は、群ロボット工学とバリアフリー発射要件に後押しされ、CAGR 10.01%で躍進します。コンパクトなノードは、消耗リスクを最小限に抑えながら、沿岸地帯を包括的にカバーすることを可能にします。

モジュール設計により、規模にとらわれないシャーシが実現し、海上でミッションパックを交換することで、サイズの境界が曖昧になります。ソフトマテリアル・スラスターと圧電アクチュエーションが、狭いパイプラインや岩礁の隙間での操縦性を研ぎ澄ます。キプロスでのスウォームベースの人工サンゴ礁モニタリングは、1ヶ月間の無人配備を検証し、調査船をチャーターすることなく生物多様性に関する洞察を広げています。

地域分析

北米は2024年の売上高の33.27%を占め、国防総省の数十億米ドル規模の船隊再編と、150フィートのマローダー無人偵察機を製造するサロニックのルイジアナ造船所のようなベンチャー資金によるスケールアップに支えられています。カナダの北極圏プログラムやメキシコの深海カンペチェの検査は、需要のループを増加させる。この地域は、成熟した防衛産業基盤、AIの人材プール、アーリーアダプター規制のサンドボックス化から恩恵を受けています。

アジア太平洋は、中国の艦隊増強、オーストラリアのAUKUSと連動したGhost Sharkのプロトタイプ、インドが海上領域認識を拡張する12機のXLUUVの入札を実施したことにより、10.40%のCAGRを記録しました。ウクライナでUSVを共同生産するノルウェーの決定を含む共同プロジェクトは、より広いインド太平洋四分円全体に技術の分散が高まっていることを示すものです。

欧州は、統合された造船クラスターとまとまった研究開発資金を活用し、自律型試験の強固なパイプラインを維持しています。EUのAI法は、規制面での先行者利益をもたらす可能性のあるハーモナイゼーションの先例を示しています。英国は機雷掃海パッケージのためにKongsberg Vanguardマザーシップを評価し、フランスのNaval Groupは大口径船型における大陸の専門知識を定着させる。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- ISRおよび対潜水艦戦能力への防衛投資の増加

- オフショア石油・ガスの点検・保守におけるUMVの利用拡大

- 海洋・気候研究における自律型システムの利用拡大

- 海洋再生可能エネルギーの操業と保守におけるUMVの新たな役割

- UMVフリートが可能にする定額制海洋データサービスの普及

- 海洋データ・アズ・ア・サービス・サブスクリプションモデルの出現

- 市場抑制要因

- 多額の資本支出と運用コストの負担

- 統一された規制と分類の枠組みの欠如

- 水中通信ネットワークにおけるサイバーセキュリティの新たな脆弱性

- コンパクトなUMVプラットフォームにおける限られた耐久性と積載量の制約

- バリューチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- ライバルの激しさ

第5章 市場規模と成長予測

- 車両タイプ別

- 無人海上機(USV)

- 無人潜水機(UUV)

- 車両サイズ別

- マイクロ

- 小型

- 中型

- 大型

- 推進力別

- ディーゼル

- 電気

- ハイブリッド

- ソーラー

- 制御タイプ別

- 遠隔操作

- 自律

- 用途別

- 防衛と安全保障

- 対潜水艦戦(ASW)

- 情報、監視、偵察(ISR)

- 地雷対策

- 商業

- オフショア石油・ガス

- 洋上風力発電と再生可能エネルギー

- 港湾・インフラ検査

- 科学研究と探査

- 捜索救助(SAR)

- 防衛と安全保障

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- 英国

- フランス

- ドイツ

- イタリア

- スペイン

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- その他アジア太平洋地域

- 南米

- ブラジル

- その他南米

- 中東・アフリカ

- 中東

- アラブ首長国連邦

- サウジアラビア

- その他中東

- アフリカ

- 南アフリカ

- その他アフリカ

- 北米

第6章 競合情勢

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- General Dynamics Mission Systems(General Dynamics Corporation)

- Thales Group

- BAE Systems plc

- Northrop Grumman Corporation

- Textron Inc.

- L3Harris Technologies, Inc.

- Kongsberg Gruppen ASA

- Saab AB

- Teledyne Technologies Incorporated

- ATLAS ELEKTRONIK GmbH

- Exail SAS

- The Boeing Company

- Ocean Aero, Inc.

- SeaRobotics Corporation

- Huntington Ingalls Industries, Inc.

- Fugro N.V.

- Anduril Industries, Inc.

- Cellula Robotics Ltd.

- Sea Machines Robotics Inc.