|

市場調査レポート

商品コード

1665413

無人海上車両市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Unmanned Marine Vehicles Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 無人海上車両市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2024年12月27日

発行: Global Market Insights Inc.

ページ情報: 英文 220 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

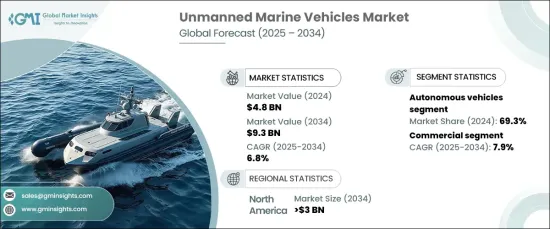

世界の無人海上車両市場は、2024年に48億米ドルと評価され、2025年から2034年にかけてCAGR 6.8%で成長すると予測されています。

海上警備と監視のニーズの高まりが、この成長の主要な推進力となっています。世界各国の政府は、国家安全保障の強化、沿岸地域の監視、航路の安全確保のために無人システムを採用しています。これらの車両は、情報収集、地雷探知、海底領域認識の強化などの用途で重要な役割を果たしています。最先端の自律性とセンサー技術の統合により、UMVは海上防衛に不可欠な存在となっています。さらに、ナビゲーション技術への投資が自律型海洋システムの進歩を加速させ、意思決定の改善、航路最適化の強化、障害物検知能力の向上を可能にしています。これらの技術革新は、人間の介入への依存を減らし、厳しい海洋条件下での効率的で長期的な任務をサポートします。

UMVは、遠隔操作車両と自律走行車両を含む制御システムに基づいて分類されます。2024年の市場シェアは、自律走行型が69.3%を占め、圧倒的でした。これらの車両は、人間の関与を最小限に抑えてリスクの高い作業を実行することで、海上作業に革命をもたらしています。高度なAIと機械学習アルゴリズムを搭載した自律型UMVは、複雑な環境をナビゲートし、さまざまな状況に適応することができ、運用効率と任務の有効性を高めています。荒海や危険地帯などの過酷な環境でも活動できるため、乗組員に関連するリスクを軽減しながら、長時間のミッションに対応できる費用対効果の高いソリューションとなっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 48億米ドル |

| 予測金額 | 93億米ドル |

| CAGR | 6.8% |

UMVの需要は、防衛、研究、商業など様々な用途で増加しています。商業分野が最も急成長しており、予測期間中のCAGRは7.9%と予測されています。この成長の背景には、海洋調査、石油・ガス探査、海底インフラ検査などのニーズの高まりがあります。UMVは過酷な条件下での自律作業を可能にし、人間が危険にさらされるのを最小限に抑えます。UMVは長時間のミッションに不可欠であり、乗組員を必要とせず、継続的なデータ収集により作業効率を高めることができます。さらに、環境モニタリングと持続可能性に重点を置くことで、海洋調査や汚染追跡への採用が進んでいます。複雑な海底地形を航行し、正確なデータを収集するその能力は、エネルギー、農業、海運などの産業にとって不可欠なものとなっています。

北米市場は、自律型海洋技術への多額の投資により、2034年までに30億米ドルを超える見通しです。同地域は持続可能な慣行と規制の枠組みに取り組んでおり、軍事・民間の海上業務の両方で成長を促進しています。UMVは、海底探査、オフショア・ロジスティクス、海洋データ収集の分野でますます活用されるようになっており、近代的な海事能力を向上させる上でその重要性を確実なものにしています。

目次

第1章 調査手法と調査範囲

- 市場範囲と定義

- 基本推定と計算

- 予測計算

- データソース

- 1次データ

- 2次データ

- 有料情報源

- 公的情報源

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- 破壊

- 将来の展望

- メーカー

- 流通業者

- サプライヤーの状況

- 利益率分析

- 主要ニュースと取り組み

- 規制状況

- 影響要因

- 促進要因

- 海上監視および防衛アプリケーションの需要増加

- 自律航行技術の進歩への投資の増加

- 世界の石油・ガス探査需要の拡大

- 海洋調査における無人海上車両の採用拡大

- 環境モニタリングや災害対応業務のニーズの高まり

- 業界の潜在的リスク&課題

- 高度なシステムの初期開発・導入コストが高い

- 国際水域での自律運用に関する規制の枠組みが限定的

- 促進要因

- 成長可能性分析

- ポーターの分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:タイプ別、2021年~2034年

- 主要動向

- 水上車両

- 水中車両

第6章 市場推計・予測:コントロール別、2021~2034年

- 主要動向

- 遠隔操作車両

- 自律走行車両

第7章 市場推計・予測:速度別、2021~2034年

- 主要動向

- 10ノットまで

- 10~30ノット

- 30ノット以上

第8章 市場推計・予測:耐久性別、2021~2034年

- 主要動向

- 100時間未満

- 100-500時間

- 500-1,000時間

- 1,000時間以上

第9章 市場推計・予測:ソリューション別、2021年~2034年

- 主要動向

- 推進システム

- 通信システム

- ペイロード

- シャーシ材料

- その他のソリューション

第10章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 防衛

- 調査

- 商業

- その他

第11章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第12章 企業プロファイル

- ASV Global

- Atlas Elektronik

- BAE Systems

- Bharat Dynamics Limited(BDL)

- ECA Group

- General Dynamics

- L3Harris Technologies

- Liquid Robotics

- Northrop Grumman

- Ocean Aero Inc.

- Pelorus Naval Systems

- Rafael Advanced Defense Systems

- Saab AB

- Sea Robotics Inc.

- Teledyne Technologies Inc.

- Textron Inc.

- Thales Group

- Unmanned Systems Technology

The Global Unmanned Marine Vehicles Market, valued at USD 4.8 billion in 2024, is anticipated to grow at a CAGR of 6.8% from 2025 to 2034. The increasing need for maritime security and surveillance is a key driver for this growth. Governments worldwide are adopting unmanned systems to strengthen national security, monitor coastal areas, and safeguard shipping lanes. These vehicles play a crucial role in applications such as intelligence gathering, mine detection, and enhancing undersea domain awareness. The integration of cutting-edge autonomy and sensor technologies has established UMVs as indispensable in maritime defense. Additionally, investments in navigation technology are accelerating advancements in autonomous marine systems, enabling improved decision-making, enhanced route optimization, and better obstacle-detection capabilities. These innovations reduce reliance on human intervention, supporting efficient and extended missions in challenging marine conditions.

UMVs are classified based on control systems, including remotely operated vehicles and autonomous vehicles. The autonomous segment dominated the market in 2024, capturing 69.3% of the market share. These vehicles are revolutionizing maritime operations by performing high-risk tasks with minimal human involvement. Equipped with advanced AI and machine learning algorithms, autonomous UMVs can navigate complex environments and adapt to varying conditions, enhancing their operational efficiency and mission effectiveness. Their ability to operate in harsh environments, such as rough seas or hazardous zones, makes them cost-effective solutions for extended missions while reducing crew-related risks.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $4.8 Billion |

| Forecast Value | $9.3 Billion |

| CAGR | 6.8% |

The demand for UMVs is increasing across various applications, including defense, research, and commercial sectors. The commercial segment is witnessing the fastest growth, with a projected CAGR of 7.9% during the forecast period. This growth is driven by rising needs in marine surveying, oil and gas exploration, and subsea infrastructure inspections. UMVs enable autonomous operations in extreme conditions, minimizing human exposure to danger. These vehicles are essential for long-duration missions, offering operational efficiency through continuous data collection without requiring a physical crew. Additionally, the focus on environmental monitoring and sustainability has boosted their adoption for oceanographic studies and pollution tracking. Their capability to navigate complex underwater terrains and collect accurate data makes them indispensable for industries such as energy, agriculture, and shipping.

The North American market is poised to exceed USD 3 billion by 2034, driven by substantial investments in autonomous marine technologies. The region's commitment to sustainable practices and regulatory frameworks fosters growth in both military and civilian maritime operations. UMVs are increasingly utilized in subsea exploration, offshore logistics, and ocean data collection, ensuring their prominence in advancing modern maritime capabilities.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Rising demand for maritime surveillance and defense applications

- 3.6.1.2 Increasing investments in autonomous navigation technology advancements

- 3.6.1.3 Expanding offshore oil and gas exploration requirements globally

- 3.6.1.4 Growing adoption of unmanned marine vehicles for ocean research

- 3.6.1.5 Rising need for environmental monitoring and disaster response operations

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 High initial development and deployment costs for advanced systems

- 3.6.2.2 Limited regulatory framework for autonomous operations in international waters

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Type, 2021-2034 (USD Million)

- 5.1 Key trends

- 5.2 Surface vehicle

- 5.3 Underwater vehicle

Chapter 6 Market Estimates & Forecast, By Control, 2021-2034 (USD Million)

- 6.1 Key trends

- 6.2 Remotely operated vehicles

- 6.3 Autonomous vehicles

Chapter 7 Market Estimates & Forecast, By Speed, 2021-2034 (USD Million)

- 7.1 Key trends

- 7.2 Up to 10 knots

- 7.3 10−30 knots

- 7.4 More than 30 knots

Chapter 8 Market Estimates & Forecast, By Endurance, 2021-2034 (USD Million)

- 8.1 Key trends

- 8.2 <100 hours

- 8.3 100−500 hours

- 8.4 500−1,000 hours

- 8.5 >1,000 hours

Chapter 9 Market Estimates & Forecast, By Solution, 2021-2034 (USD Million)

- 9.1 Key trends

- 9.2 Propulsion system

- 9.3 Communication system

- 9.4 Payload

- 9.5 Chassis material

- 9.6 Other solutions

Chapter 10 Market Estimates & Forecast, By End Use Application, 2021-2034 (USD Million)

- 10.1 Key trends

- 10.2 Defense

- 10.3 Research

- 10.4 Commercial

- 10.5 Others

Chapter 11 Market Estimates & Forecast, By Region, 2021-2034 (USD Million)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 UK

- 11.3.2 Germany

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Russia

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 South Korea

- 11.4.5 Australia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.6 MEA

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 ASV Global

- 12.2 Atlas Elektronik

- 12.3 BAE Systems

- 12.4 Bharat Dynamics Limited (BDL)

- 12.5 ECA Group

- 12.6 General Dynamics

- 12.7 L3Harris Technologies

- 12.8 Liquid Robotics

- 12.9 Northrop Grumman

- 12.10 Ocean Aero Inc.

- 12.11 Pelorus Naval Systems

- 12.12 Rafael Advanced Defense Systems

- 12.13 Saab AB

- 12.14 Sea Robotics Inc.

- 12.15 Teledyne Technologies Inc.

- 12.16 Textron Inc.

- 12.17 Thales Group

- 12.18 Unmanned Systems Technology